India Prefabricated Buildings Market Outlook to 2030

Region:India

Author(s):Yogita Sahu

Product Code:KROD5835

Region:India

Author(s):Yogita Sahu

Product Code:KROD5835

November 2024

83

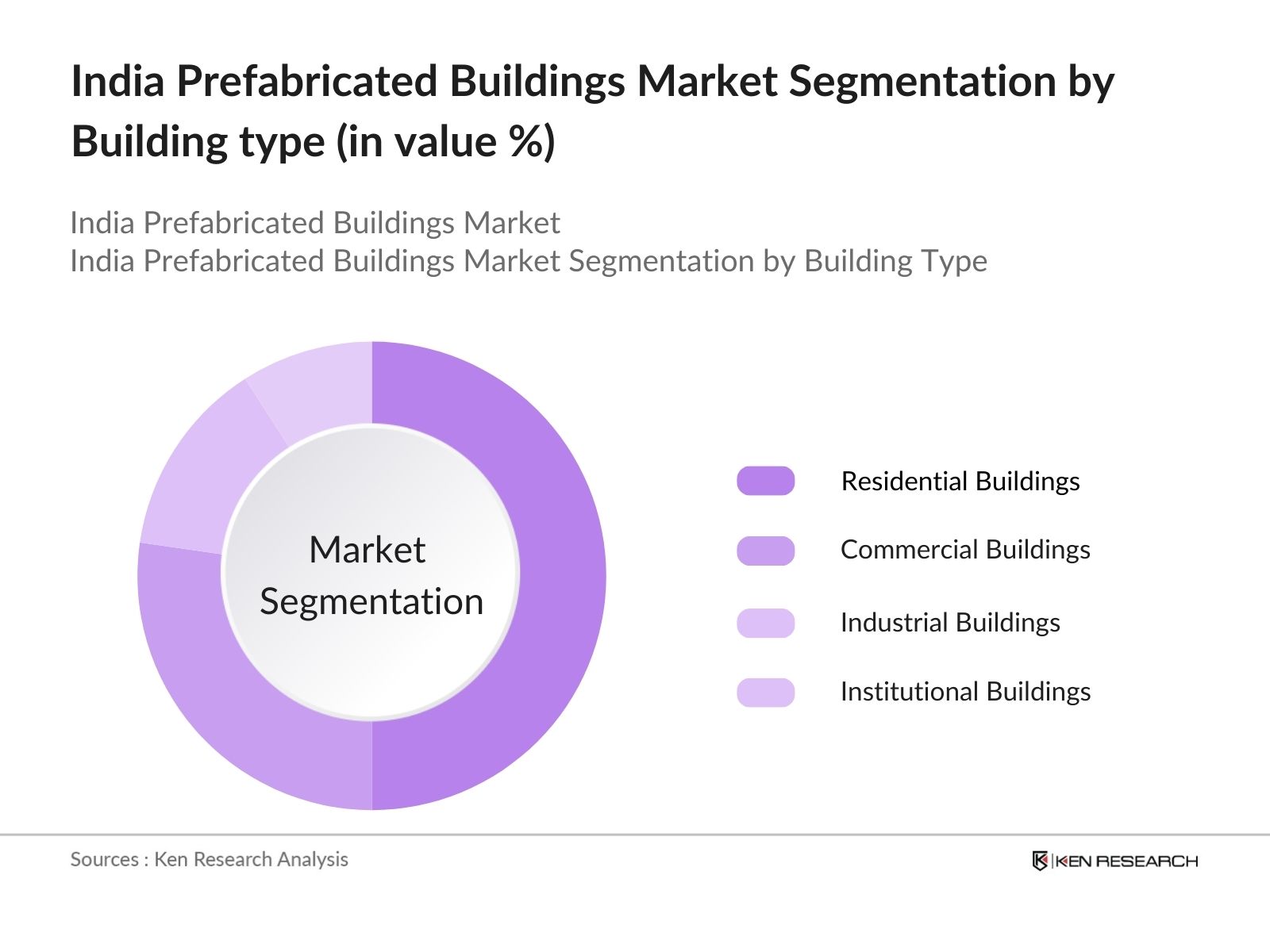

By Building Type: The market is segmented by building type into residential buildings, commercial buildings, industrial buildings, and institutional buildings. Residential buildings hold a dominant market share under this segmentation. This dominance is due to the rising demand for affordable housing, supported by government schemes like PMAY, which promotes faster construction techniques for urban low-income households.

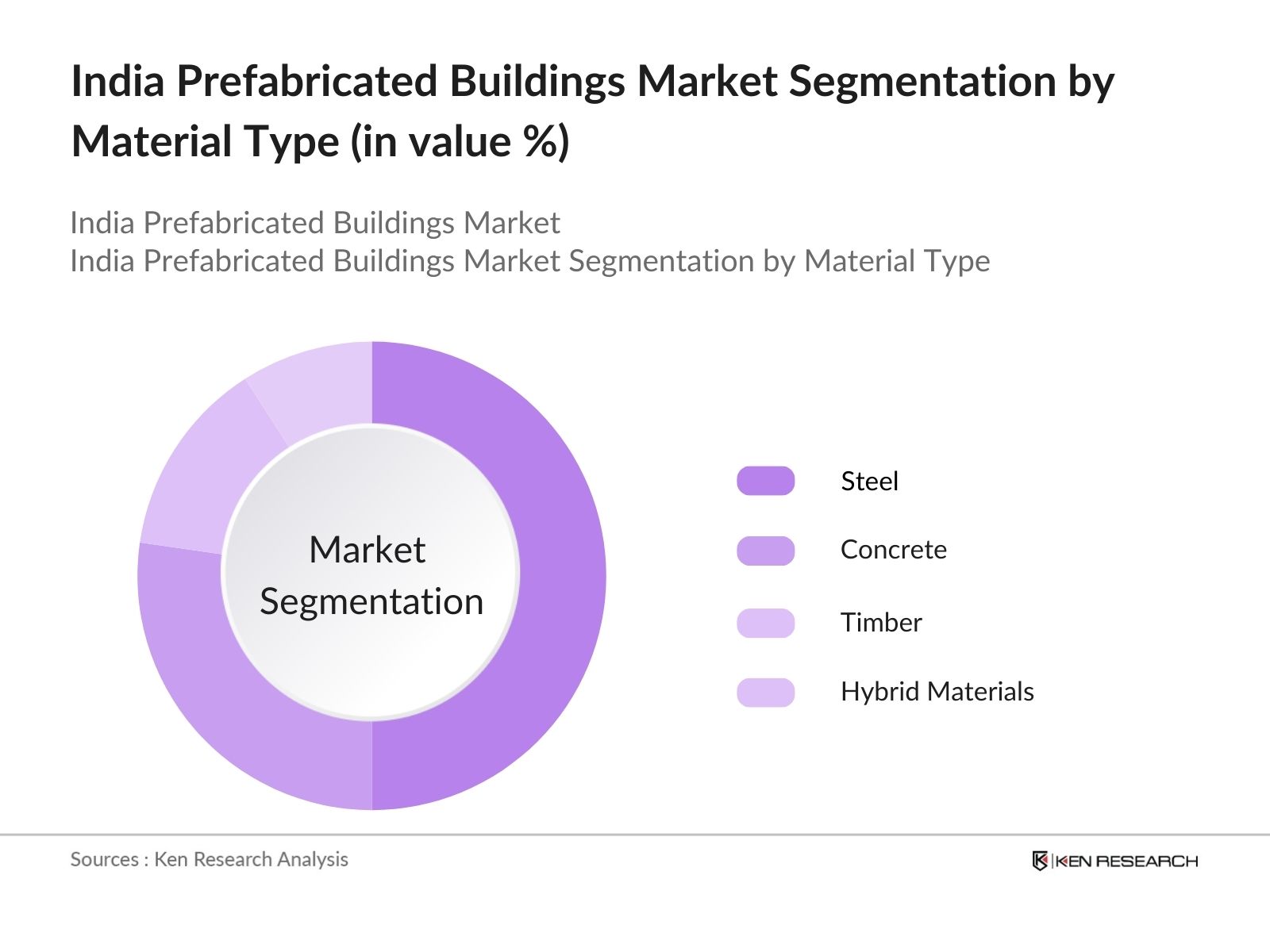

By Material Type: The market is also segmented by material type into steel, concrete, timber, and hybrid materials. The steel segment dominates the market, primarily due to its strength, durability, and ability to withstand harsh environmental conditions. Steel prefabrication allows for faster construction, which is particularly attractive in industrial and large-scale commercial projects. Additionally, it aligns with sustainability initiatives, as steel is recyclable, reducing the environmental footprint of construction activities.

The market is dominated by a few major players, including local manufacturers and global firms. These companies are leading the charge in the construction of modular buildings, utilizing advanced technologies and materials to cater to the rising demand for efficient construction methods.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (INR Cr) |

Production Capacity |

Key Clients |

Technology Adoption |

Sustainability Initiatives |

|

Tata BlueScope Steel |

2005 |

Pune, India |

|||||

|

B.G. Shirke Construction Technology |

1944 |

Pune, India |

|||||

|

Kirby Building Systems |

1976 |

Hyderabad, India |

|||||

|

Everest Industries Ltd. |

1934 |

New Delhi, India |

|||||

|

Jindal Steel & Power |

1952 |

New Delhi, India |

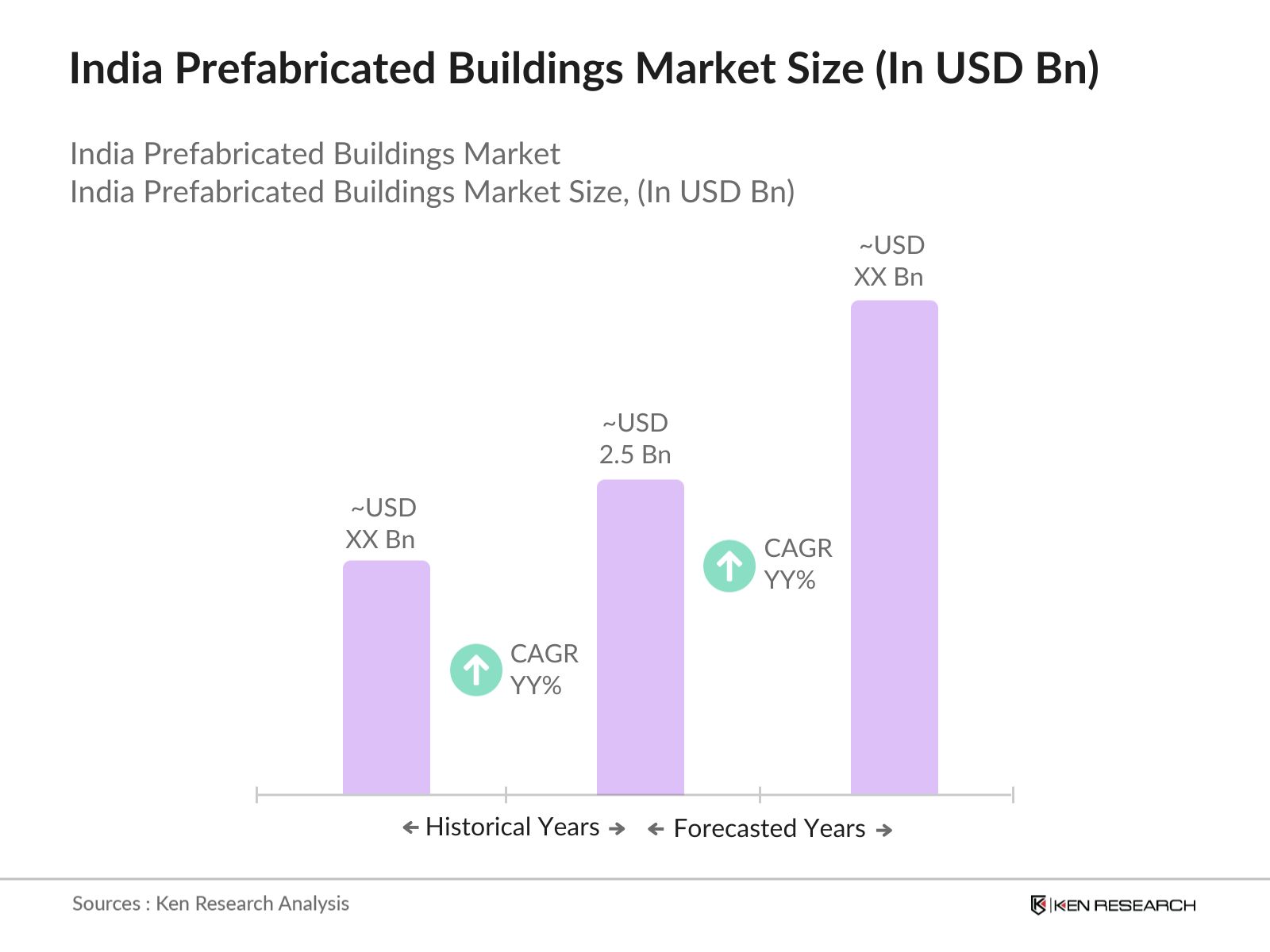

Over the next five years, the India Prefabricated Buildings industry is expected to show growth driven by the expanding urban population, government-backed infrastructure projects, and the rise in sustainable construction practices. The push for affordable housing, particularly through initiatives like PMAY, will continue to promote the adoption of prefabricated structures.

|

By Building Type |

Residential Buildings Commercial Buildings Industrial Buildings Institutional Buildings |

|

By Material Type |

Steel Concrete Timber Hybrid Materials |

|

By Component Type |

Walls Roofs Floors Staircases |

|

By Construction Method |

Panelized Construction Modular Construction Pre-Engineered Buildings (PEBs) |

|

By Region |

North South East West |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (Market Expansion)

3.1.1. Urban Infrastructure Projects

3.1.2. Government Housing Initiatives (PMAY, Smart City Mission)

3.1.3. Reduction in Construction Time

3.1.4. Sustainable and Green Building Certifications

3.2. Market Challenges (Industry Constraints)

3.2.1. High Initial Investment

3.2.2. Perception of Lower Quality in Prefab Structures

3.2.3. Lack of Standardized Building Codes

3.3. Opportunities (Expansion Horizons)

3.3.1. Growth of Tier 2 and Tier 3 Cities

3.3.2. Technological Advancements (Automation, 3D Printing)

3.3.3. Private Sector Adoption

3.4. Trends (Market Evolution)

3.4.1. Increased Use of Lightweight Materials

3.4.2. Rise of Modular Construction

3.4.3. Digital Integration in Building Information Modeling (BIM)

3.5. Government Regulation (Policy Impact)

3.5.1. FDI in Construction Development

3.5.2. Ease of Doing Business Initiatives

3.5.3. RERA Compliance

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem

4.1. By Building Type (In Value %)

4.1.1. Residential Buildings

4.1.2. Commercial Buildings

4.1.3. Industrial Buildings

4.1.4. Institutional Buildings

4.2. By Material Type (In Value %)

4.2.1. Steel

4.2.2. Concrete

4.2.3. Timber

4.2.4. Hybrid Materials

4.3. By Component Type (In Value %)

4.3.1. Walls

4.3.2. Roofs

4.3.3. Floors

4.3.4. Staircases

4.4. By Construction Method (In Value %)

4.4.1. Panelized Construction

4.4.2. Modular Construction

4.4.3. Pre-Engineered Buildings (PEBs)

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West India

5.1 Detailed Profiles of Major Companies

5.1.1. Tata BlueScope Steel

5.1.2. B.G. Shirke Construction Technology Pvt. Ltd.

5.1.3. Everest Industries Ltd.

5.1.4. Kirby Building Systems

5.1.5. Jindal Steel & Power

5.1.6. Pennar Industries Ltd.

5.1.7. L&T Construction

5.1.8. Champion Prefabs

5.1.9. Reliance Infrastructure

5.1.10. Tata Projects Ltd.

5.1.11. EPACK Prefab

5.1.12. Nippon Koei India Pvt. Ltd.

5.1.13. Era Infra Engineering

5.1.14. Simplex Infrastructures Ltd.

5.1.15. IL&FS Engineering and Construction

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Production Capacity, R&D Investment, Technology Adoption, Key Clients)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Contracts and Tenders

5.8. Private Equity Investments

6.1. Compliance with Building Codes

6.2. Certification Processes (BIS, ISO Standards)

6.3. Environmental and Sustainability Standards

6.4. Safety Regulations

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Building Type (In Value %)

8.2. By Material Type (In Value %)

8.3. By Component Type (In Value %)

8.4. By Construction Method (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Strategic Marketing Initiatives

9.4. White Space Opportunity Analysis

The first step involves identifying the critical variables within the India Prefabricated Buildings Market. This is accomplished by conducting a thorough desk analysis of industry reports, government initiatives, and proprietary databases. The focus here is on understanding the factors driving the market, such as government policies, urbanization trends, and technological advancements.

In the second phase, historical market data is gathered and analyzed to assess the penetration of prefabricated construction methods. This includes analyzing market shares, trends, and the performance of key market players. The data compiled is then cross-referenced with revenue and production estimates to ensure accuracy.

To validate the initial findings, consultations are conducted with industry experts and stakeholders. These consultations are aimed at obtaining insights from manufacturers, contractors, and government bodies, ensuring that the gathered data accurately reflects market dynamics.

The final stage of research synthesis involves consolidating the validated data to form a comprehensive overview of the India Prefabricated Buildings Market. The synthesized data is then used to generate insights into key trends, growth drivers, and challenges in the market, ensuring the final report provides actionable intelligence for stakeholders.

The India Prefabricated Buildings Market is valued at USD 2.5 billion, driven by government initiatives like PMAY and the increasing demand for cost-effective construction solutions.

Challenges in the India Prefabricated Buildings Market include high initial investment costs, limited consumer awareness regarding prefabricated structures, and the lack of standardized building codes, which can slow adoption.

Key players in the India Prefabricated Buildings Market include Tata BlueScope Steel, B.G. Shirke Construction Technology Pvt. Ltd., Everest Industries Ltd., Kirby Building Systems, and Jindal Steel & Power, who dominate due to their advanced technology, large production capacities, and strategic government partnerships.

The India Prefabricated Buildings Market is propelled by rapid urbanization, government-backed affordable housing initiatives, and the need for quicker construction solutions. Prefabrication significantly reduces construction timelines, offering an efficient solution to meet growing demand.

The residential building segment dominates the India Prefabricated Buildings Market, driven by government initiatives to provide affordable housing for urban populations, as well as rising demand for sustainable and cost-effective homes.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.