India Real Estate Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD4557

December 2024

92

About the Report

India Real Estate Market Overview

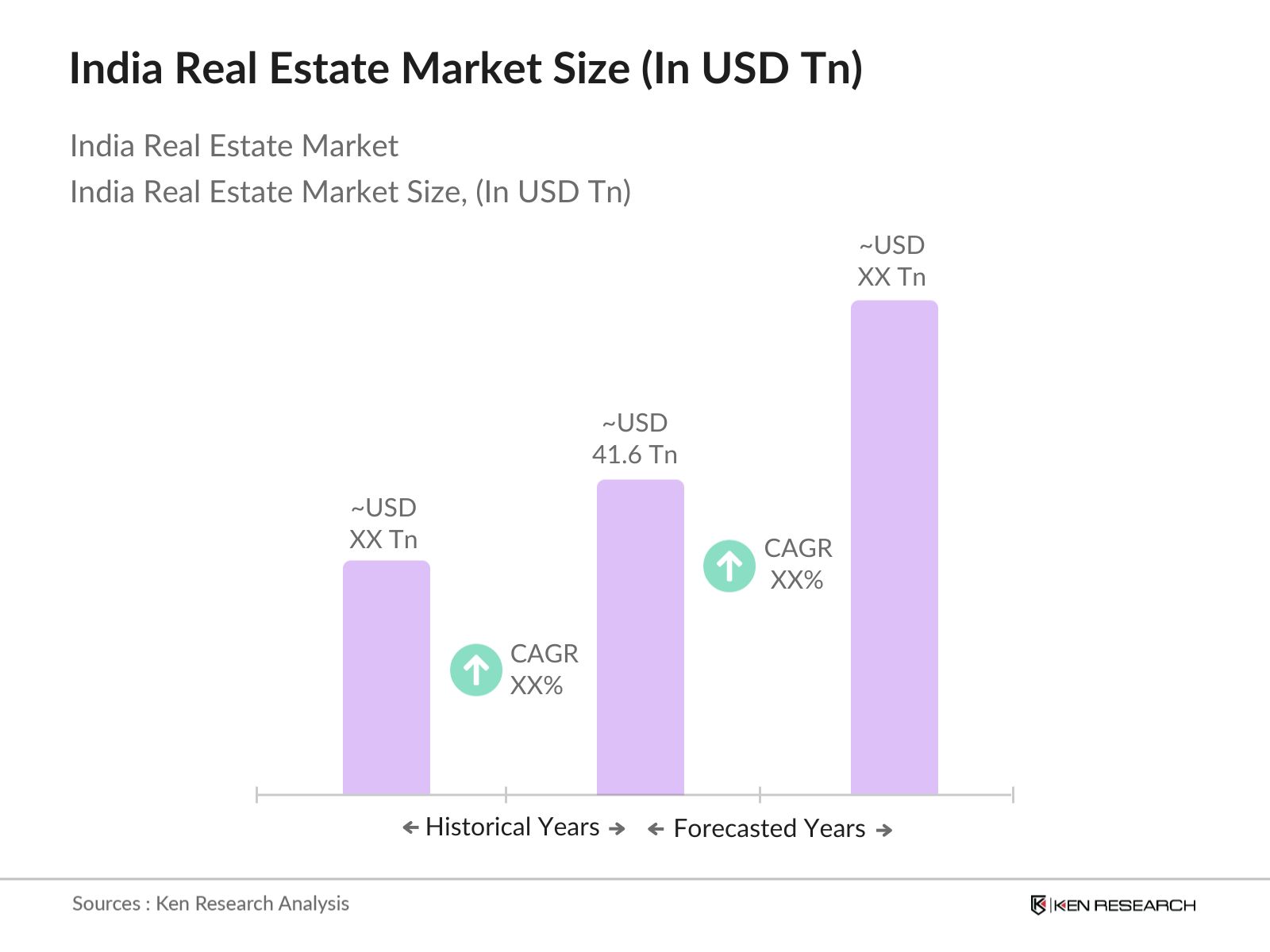

- The India Real Estate market, valued at USD 41.6 trillion, has been driven by rapid urbanization and increasing demand for both residential and commercial properties. Government schemes like the Pradhan Mantri Awas Yojana and investment in Smart Cities have played a crucial role in this growth. The market is also fueled by foreign direct investments (FDI) and technological advancements in real estate operations, creating an ecosystem ripe for further development. The rise in disposable income among the middle-class population has spurred growth, especially in urban areas.

- Dominant cities in the India Real Estate market include Mumbai, Delhi-NCR, and Bengaluru. These cities lead the market due to their established infrastructure, high commercial demand, and ongoing real estate projects catering to both residential and corporate clients. Mumbai's financial significance, Delhi-NCR's political and industrial relevance, and Bengalurus tech-driven expansion contribute to their dominance in the market. Their prominence is also reinforced by higher land valuations, making these regions attractive for investors.

- The Real Estate (Regulation and Development) Act (RERA) has revolutionized Indias real estate landscape, ensuring transparency and safeguarding consumer interests. As of 2024, over 76,000 projects and 65,000 agents have been registered under RERA, promoting accountability in project timelines and reducing malpractices. This regulatory framework has strengthened buyer confidence and streamlined the real estate sector, particularly benefiting residential projects.

India Real Estate Market Segmentation

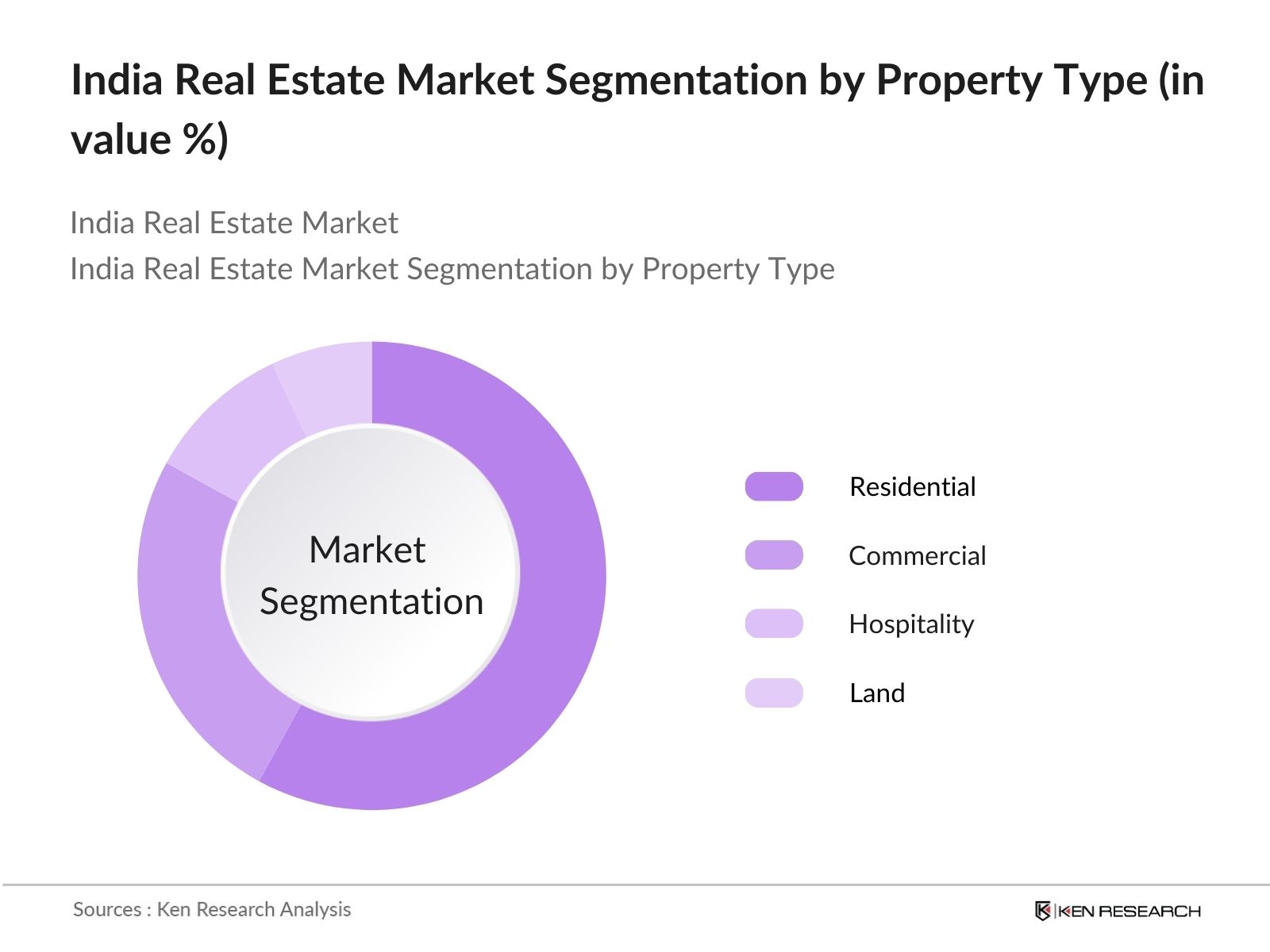

- By Property Type: The India Real Estate market is segmented by property type into residential, commercial, hospitality, and land. Recently, the residential segment has been dominant due to rising demand for affordable housing and increasing population migration to urban centers. Government policies promoting housing for all and low-interest home loans have encouraged home ownership. The commercial segment is growing rapidly, driven by the rise in demand for office spaces and co-working hubs, especially in Tier-1 cities.

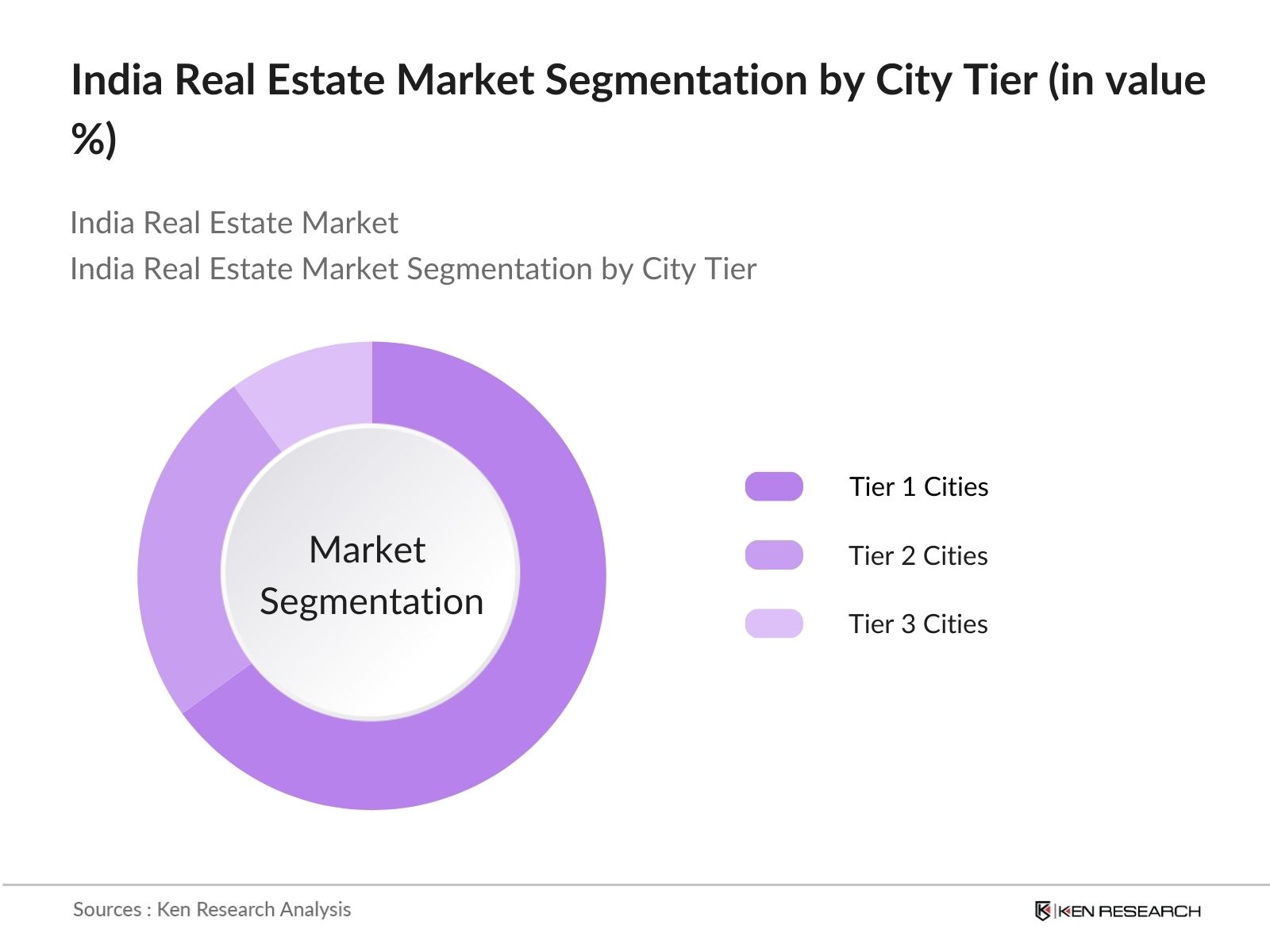

- By City Tier: India's real estate market is segmented by city tiers into Tier 1, Tier 2, and Tier 3 cities. Tier 1 cities such as Mumbai, Delhi, and Bengaluru dominate the market, driven by high demand for both residential and commercial spaces. These cities offer better job prospects and infrastructure, making them attractive for real estate investment. However, Tier 2 cities like Pune and Jaipur are gaining traction due to lower property prices and increasing demand for affordable housing. This is further complemented by rising investments in infrastructure in these emerging cities.

India Real Estate Market Competitive Landscape

The India Real Estate market is highly competitive, with a mix of national developers and local builders driving the market forward. Major players dominate large-scale projects in Tier 1 cities, while regional developers focus on smaller cities and towns. The rise in institutional investments and the growth of Real Estate Investment Trusts (REITs) have further fueled competition in the market.

|

Company |

Established |

Headquarters |

Projects Completed |

Revenue (USD Bn) |

Geographical Presence |

Market Specialization |

Total Area Developed (Sq Ft) |

Awards |

Joint Ventures |

|

DLF Limited |

1946 |

New Delhi |

- |

- |

- |

- |

- |

- |

- |

|

Godrej Properties |

1990 |

Mumbai |

- |

- |

- |

- |

- |

- |

- |

|

Oberoi Realty |

1980 |

Mumbai |

- |

- |

- |

- |

- |

- |

- |

|

Prestige Estates Projects |

1986 |

Bengaluru |

- |

- |

- |

- |

- |

- |

- |

|

Sobha Limited |

1995 |

Bengaluru |

- |

- |

- |

- |

- |

- |

- |

India Real Estate Market Analysis

India Real Estate Market Growth Drivers

- FDI Inflows: Foreign Direct Investment (FDI) in India's real estate sector saw an increase to $5.4 billion in 2023. This growth is largely attributed to reforms such as the Real Estate Regulatory Authority (RERA) and the introduction of Real Estate Investment Trusts (REITs), which have improved transparency and investment attractiveness. India has attracted global investors due to these regulatory frameworks, boosting both residential and commercial real estate sectors. The ongoing FDI inflow has played a pivotal role in accelerating real estate projects and large-scale developments.

- Urbanization and Smart City Projects: India's urban population is projected to reach 600 million by end of 2024, driving the demand for residential and commercial spaces. The Smart Cities Mission aims to develop sustainable urban infrastructure, with over 5,000 projects worth 2.05 lakh crore currently under implementation. Cities like Pune, Ahmedabad, and Kochi have become major real estate hubs due to these initiatives. The rapid urbanization trend necessitates real estate development, especially in housing, transportation, and commercial real estate, transforming the market landscape.

- Regulatory Frameworks (RERA, GST): The implementation of the Real Estate (Regulation and Development) Act (RERA) in 2016 has improved transparency, accountability, and investor confidence. As of 2024, more than 76,000 real estate projects have been registered under RERA, ensuring timely completion and protection for buyers. The Goods and Services Tax (GST) has streamlined tax structures for real estate developers, leading to smoother transactions and lower tax burdens for buyers. Together, RERA and GST reforms have enhanced trust, promoting investments in both residential and commercial real estate sectors.

India Real Estate Market Challenges

- High Construction Costs: The construction costs in India have risen steadily due to increased raw material prices. In 2024, cement prices reached 400 per bag, and steel prices are hovering around 70,000 per tonne, putting pressure on developers. Labor costs have also surged, with skilled labour shortages adding to the challenge. These high costs affect project viability, leading to a delay in project completion and, in some cases, abandonment of developments, which hinders the real estate market growth.

- Delayed Project Approvals: Delays in acquiring necessary approvals for real estate projects remain a persistent issue. In 2023, it took an average of 18-24 months to secure all permissions, causing delays in project execution. This regulatory bottleneck discourages timely project completion, increases overall costs, and affects investor confidence. Despite regulatory reforms like RERA, delays in obtaining environmental clearances, land approvals, and building permits continue to pose challenges.

India Real Estate Market Future Outlook

Over the next five years, the India Real Estate market is expected to experience steady growth, driven by sustained demand for residential properties, ongoing government initiatives like Smart Cities Mission, and the rising trend of digital transformation in the real estate sector. Commercial real estate will continue to grow due to the expansion of office spaces, co-working hubs, and retail infrastructure. Additionally, advancements in real estate technologies such as PropTech, and an increased focus on green buildings and sustainable development, will shape the future market.

India Real Estate Market Opportunities

- Affordable Housing Demand: Indias affordable housing segment remains one of the fastest-growing segments in the real estate market. As of 2024, there is a demand for 29 million affordable housing units in urban areas. Government initiatives, including tax rebates for first-time homebuyers and PMAY, have accelerated growth in this sector. Developers have responded by focusing on smaller, more affordable projects to cater to middle-income groups. The rise in demand presents a substantial opportunity for expansion within the affordable housing market.

- Commercial Real Estate Boom (IT Parks, Co-Working Spaces): Indias commercial real estate market has witnessed rapid growth, particularly in the IT and co-working space sectors. In 2024, approximately 50 million square feet of office space was leased in key cities like Bengaluru, Pune, and Hyderabad. The growth of the IT sector, along with the shift towards flexible working environments, has driven demand for co-working spaces, which occupy over 30% of office leasing in major cities. This trend represents a booming opportunity for developers in commercial real estate.

Scope of the Report

|

By Property Type |

Residential Commercial Hospitality Land |

|

By Construction Stage |

Pre-Construction Under-Construction Ready-to-Move-In |

|

By City Tier |

Tier 1 Cities Tier 2 Cities Tier 3 Cities |

|

By End-User |

Residential Buyers Institutional Buyers NRI Buyers |

|

By Region |

North India South India West India East India |

Products

Key Target Audience

Real Estate Developers and Builders

Property Investors

Institutional Investors

Residential Homebuyers

Corporate Tenants (Commercial Office Spaces)

Government and Regulatory Bodies (RERA, Ministry of Housing and Urban Affairs)

Financial Institutions and Banks

Investor and Venture Capitalist Firms

Companies

India Real Estate Market Major Players

DLF Limited

Godrej Properties

Oberoi Realty

Prestige Estates Projects Ltd.

Sobha Limited

Brigade Group

Tata Housing

Lodha Group

Indiabulls Real Estate

Puravankara

Mahindra Lifespace Developers

Shapoorji Pallonji Real Estate

L&T Realty

Raheja Developers

Hiranandani Group

Table of Contents

1. India Real Estate Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Urbanization, Rising Disposable Income, Migration Trends)

1.4. Market Segmentation Overview

2. India Real Estate Market Size (In INR Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Policy Reforms, Infrastructure Developments, Affordable Housing Initiatives)

3. India Real Estate Market Analysis

3.1. Growth Drivers

3.1.1. Government Housing Schemes (Pradhan Mantri Awas Yojana, Smart Cities Mission)

3.1.2. FDI Inflows

3.1.3. Urbanization and Smart City Projects

3.1.4. Regulatory Frameworks (RERA, GST)

3.2. Market Challenges

3.2.1. High Construction Costs

3.2.2. Delayed Project Approvals

3.2.3. Environmental Concerns

3.3. Opportunities

3.3.1. Affordable Housing Demand

3.3.2. Commercial Real Estate Boom (IT Parks, Co-Working Spaces)

3.3.3. Real Estate Technology Adoption (PropTech)

3.4. Trends

3.4.1. Sustainable Real Estate (Green Buildings, LEED Certification)

3.4.2. Rise of Co-Living and Co-Working Spaces

3.4.3. Integration of Smart Home Technologies

3.5. Government Regulation

3.5.1. RERA Implementation

3.5.2. Affordable Housing Policy

3.5.3. Infrastructure Status for Affordable Housing

3.5.4. Real Estate Investment Trusts (REITs) Framework

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Developers, Builders, Investors, Government Bodies)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. India Real Estate Market Segmentation

4.1. By Property Type (In Value %)

4.1.1. Residential (Affordable Housing, Premium Housing)

4.1.2. Commercial (Office Spaces, Retail, Industrial)

4.1.3. Hospitality (Hotels, Resorts, Service Apartments)

4.1.4. Land (Agricultural, Non-Agricultural, Special Economic Zones)

4.2. By Construction Stage (In Value %)

4.2.1. Pre-Construction

4.2.2. Under-Construction

4.2.3. Ready-to-Move-In

4.3. By City Tier (In Value %)

4.3.1. Tier 1 Cities (Delhi, Mumbai, Bengaluru)

4.3.2. Tier 2 Cities (Pune, Jaipur, Surat)

4.3.3. Tier 3 Cities (Coimbatore, Kanpur, Kochi)

4.4. By End-User (In Value %)

4.4.1. Residential Buyers (First-Time Homebuyers, Investors)

4.4.2. Institutional Buyers (Corporates, Investment Trusts)

4.4.3. NRI Buyers

4.5. By Region (In Value %)

4.5.1. North India (Delhi-NCR, Punjab)

4.5.2. South India (Bengaluru, Hyderabad)

4.5.3. West India (Mumbai, Pune)

4.5.4. East India (Kolkata, Bhubaneswar)

5. India Real Estate Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. DLF Limited

5.1.2. Godrej Properties

5.1.3. Oberoi Realty

5.1.4. Prestige Estates Projects Ltd.

5.1.5. Sobha Limited

5.1.6. Brigade Group

5.1.7. Tata Housing

5.1.8. Lodha Group

5.1.9. Indiabulls Real Estate

5.1.10. Puravankara

5.1.11. Mahindra Lifespace Developers

5.1.12. Shapoorji Pallonji Real Estate

5.1.13. L&T Realty

5.1.14. Raheja Developers

5.1.15. Hiranandani Group

5.2. Cross Comparison Parameters (No. of Projects, Revenue, Market Share, Geographical Presence, Property Types)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Joint Ventures, Strategic Partnerships)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Private Equity Investments

5.8. Real Estate Investment Trusts (REITs)

6. India Real Estate Market Regulatory Framework

6.1. RERA Compliance

6.2. Land Acquisition Laws

6.3. Stamp Duty and Registration Charges

6.4. Building Bylaws and Zoning Regulations

7. India Real Estate Future Market Size (In INR Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. India Real Estate Future Market Segmentation

8.1. By Property Type (In Value %)

8.2. By Construction Stage (In Value %)

8.3. By City Tier (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9. India Real Estate Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Marketing Initiatives

9.3. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In the first phase, we conducted extensive desk research to map the India Real Estate market's ecosystem, including primary stakeholders such as developers, regulatory bodies, and financial institutions. The objective was to identify critical factors that influence the market, such as urbanization trends, investment inflows, and government policies.

Step 2: Market Analysis and Construction

In this phase, historical market data was analyzed to assess trends in property pricing, supply-demand dynamics, and regional growth patterns. The focus was on understanding the different segments within the real estate sector, including residential, commercial, and hospitality. The resulting market estimates were validated through secondary sources.

Step 3: Hypothesis Validation and Expert Consultation

We engaged in expert consultations through telephonic interviews with real estate professionals, property consultants, and government officials. These interactions helped refine market hypotheses, focusing on project approvals, land acquisition policies, and technological advancements in construction.

Step 4: Research Synthesis and Final Output

In the final step, our data was synthesized through engagements with key real estate developers and financial institutions. This collaboration helped to confirm market estimates and provided insights into consumer preferences, investment trends, and future growth opportunities.

Frequently Asked Questions

01. How big is the India Real Estate Market?

The India Real Estate market was valued at USD 41.6 trillion, driven by factors such as urbanization, demand for affordable housing, and growth in commercial infrastructure.

02. What are the challenges in the India Real Estate Market?

India Real Estate market challenges include high construction costs, regulatory delays in project approvals, and environmental regulations. Rising land prices and financing constraints also pose many hurdles.

03. Who are the major players in the India Real Estate Market?

Key players in the India Real Estate market include DLF Limited, Godrej Properties, Oberoi Realty, Prestige Estates Projects, and Sobha Limited, all of whom have a strong presence across residential and commercial real estate sectors.

04. What are the growth drivers of the India Real Estate Market?

The India Real Estate market is driven by government housing schemes, increasing foreign investments, demand for commercial office spaces, and a shift towards sustainable and smart real estate solutions.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.