India Residential Construction Market Outlook to 2030

Region:India

Author(s):Naman Rohilla

Product Code:KROD5850

Region:India

Author(s):Naman Rohilla

Product Code:KROD5850

December 2024

100

The India residential construction market is dominated by both national and regional players. The competitive landscape is characterized by established companies that focus on large-scale residential projects, as well as smaller firms that cater to specific local markets. Leading firms are investing heavily in smart home technology and green buildings to differentiate themselves in an increasingly competitive market. The market is also witnessing consolidation, with larger players acquiring smaller, regional companies to expand their footprint.

|

Company Name |

Establishment Year |

Headquarters |

No. of Projects |

Revenue (USD Bn) |

Geographic Presence |

Focus on Sustainability |

R&D Investment |

Technology Adoption |

|

DLF Limited |

1946 |

New Delhi |

- |

- |

- |

- |

- |

- |

|

Godrej Properties |

1990 |

Mumbai |

- |

- |

- |

- |

- |

- |

|

Prestige Estates Projects |

1986 |

Bengaluru |

- |

- |

- |

- |

- |

- |

|

Sobha Limited |

1995 |

Bengaluru |

- |

- |

- |

- |

- |

- |

|

Brigade Enterprises |

1986 |

Bengaluru |

- |

- |

- |

- |

- |

- |

The India residential construction market is set to experience substantial growth over the next five years, driven by an increasing population, urbanization, and government support for affordable housing initiatives. Key trends such as the adoption of sustainable construction practices, rising demand for smart homes, and the use of modular and prefabricated building techniques are expected to shape the market. As the demand for luxury housing grows, developers are likely to focus on incorporating cutting-edge technologies, green certifications, and advanced materials to meet consumer expectations.

|

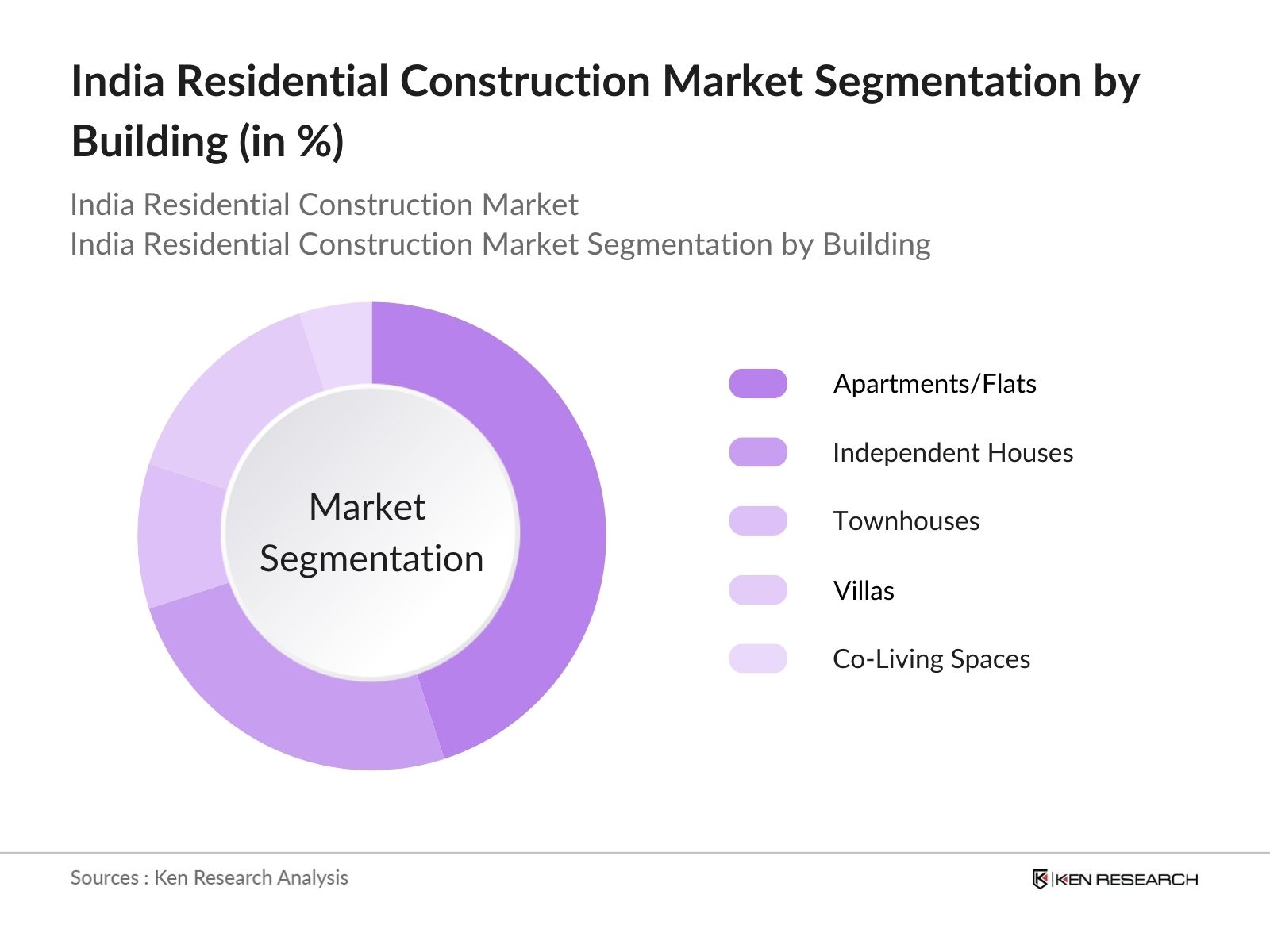

Building Type |

Apartments/Flats Independent Houses Townhouses Villas Co-Living Spaces |

|

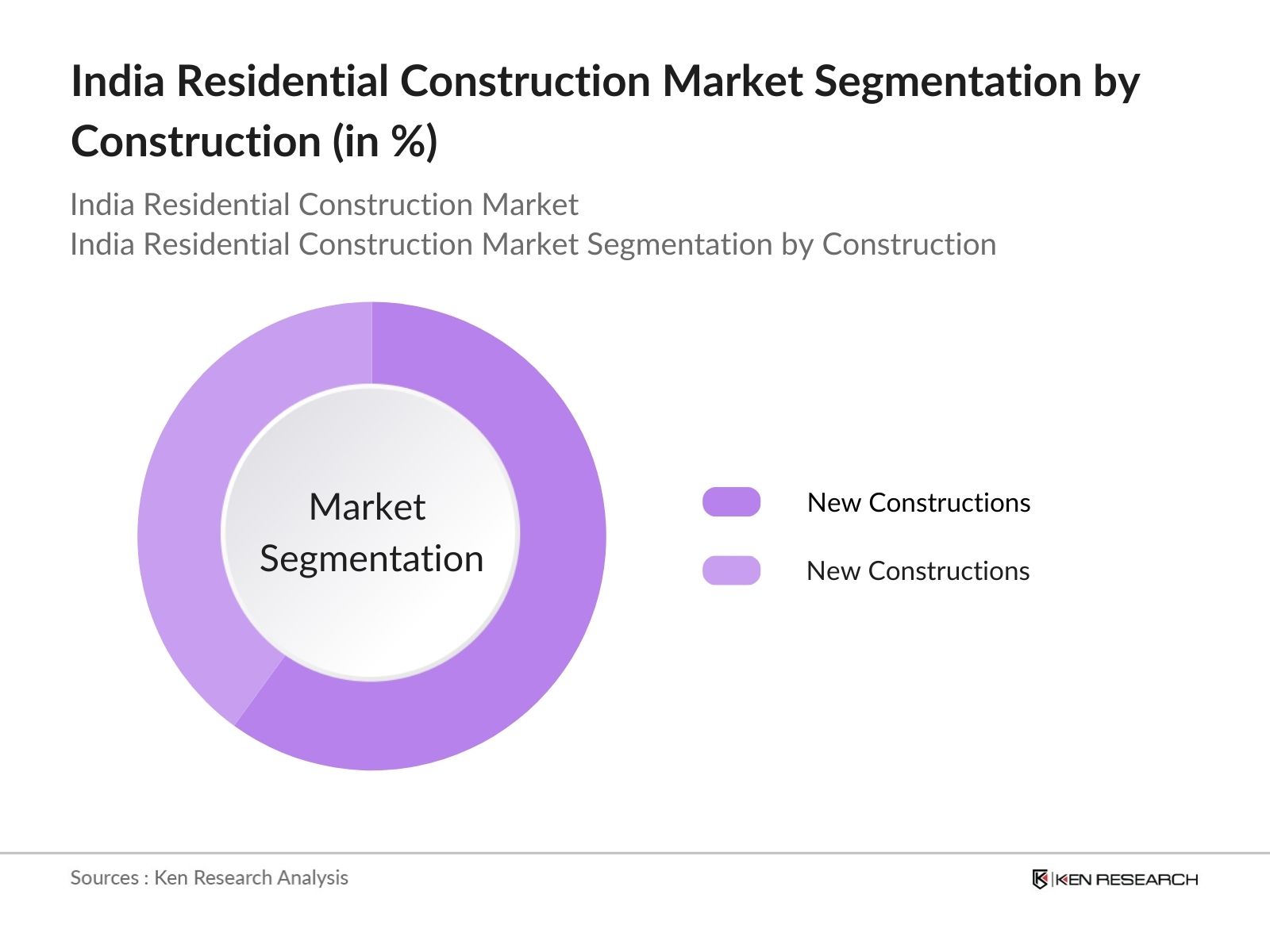

Construction Type |

New Constructions Renovation & Reconstruction |

|

Material Type |

Concrete Steel Wood Glass |

|

Technology Adoption |

Smart Home Technologies Green Building Materials Modular & Prefabrication |

|

Region |

North India South India East India West India |

Key Target Audience

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Urbanization and Migration Patterns

3.1.2 Government Initiatives (e.g., Pradhan Mantri Awas Yojana)

3.1.3 Increasing Demand for Affordable Housing

3.1.4 Technological Advancements in Construction

3.2 Market Challenges

3.2.1 High Land Acquisition Costs

3.2.2 Regulatory Delays and Bureaucratic Hurdles

3.2.3 Fluctuations in Raw Material Prices

3.2.4 Skilled Labor Shortages

3.3 Opportunities

3.3.1 Expansion into Tier 2 and Tier 3 Cities

3.3.2 Green Building Certifications and Sustainability

3.3.3 Smart Homes and Automation Trends

3.4 Trends

3.4.1 Adoption of Pre-Fabrication and Modular Construction

3.4.2 Rising Demand for Co-Living Spaces

3.4.3 Growth in Luxury Residential Projects

3.5 Government Regulations

3.5.1 RERA (Real Estate Regulatory Authority)

3.5.2 Affordable Housing Policies

3.5.3 Smart City Mission

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (Real Estate Developers, Contractors, Architects, Consultants)

3.8 Porters Five Forces

3.9 Competitive Ecosystem

4.1 By Building Type (In Value %)

4.1.1 Apartments/Flats

4.1.2 Independent Houses

4.1.3 Townhouses

4.1.4 Villas

4.1.5 Co-Living Spaces

4.2 By Construction Type (In Value %)

4.2.1 New Constructions

4.2.2 Renovation & Reconstruction

4.3 By Material Type (In Value %)

4.3.1 Concrete

4.3.2 Steel

4.3.3 Wood

4.3.4 Glass

4.4 By Technology Adoption (In Value %)

4.4.1 Smart Home Technologies

4.4.2 Green Building Materials

4.4.3 Modular & Prefabrication

4.5 By Region (In Value %)

4.5.1 North India

4.5.2 South India

4.5.3 East India

4.5.4 West India

5.1 Detailed Profiles of Major Companies

5.1.1 DLF Limited

5.1.2 Godrej Properties

5.1.3 Oberoi Realty

5.1.4 Prestige Estates Projects

5.1.5 Sobha Limited

5.1.6 Brigade Enterprises

5.1.7 Puravankara Limited

5.1.8 Lodha Group

5.1.9 Tata Housing Development Company

5.1.10 Mahindra Lifespace Developers

5.1.11 Shriram Properties

5.1.12 Raheja Developers

5.1.13 Unitech Group

5.1.14 Hiranandani Group

5.1.15 Sunteck Realty

5.2 Cross Comparison Parameters (Market Share, Project Portfolio, Geographic Presence, Revenue, No. of Projects Completed, Sustainability Initiatives, R&D Investment, Innovation in Design)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

6.1 RERA Guidelines

6.2 Building Codes and Standards

6.3 Environmental Regulations (Green Building Certifications)

6.4 Land Acquisition Laws

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Building Type (In Value %)

8.2 By Construction Type (In Value %)

8.3 By Material Type (In Value %)

8.4 By Technology Adoption (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsThis phase involves mapping the entire residential construction ecosystem in India. Extensive desk research, supported by secondary databases and proprietary sources, is used to identify the key variables influencing market dynamics. The goal is to define the critical parameters shaping the market.

Here, historical data is analyzed to understand market penetration, key construction methods, and revenue generation patterns in the residential sector. Additionally, regional trends are assessed to evaluate the performance of different building types and construction methods.

Through interviews with industry experts from leading residential construction companies, market hypotheses are tested. These consultations provide operational insights and validate the data obtained from secondary research, ensuring the accuracy of projections.

The final stage involves synthesizing all research findings. Multiple residential construction projects across India are examined to confirm market trends, validate segmentation data, and deliver a comprehensive, accurate analysis of the India residential construction market.

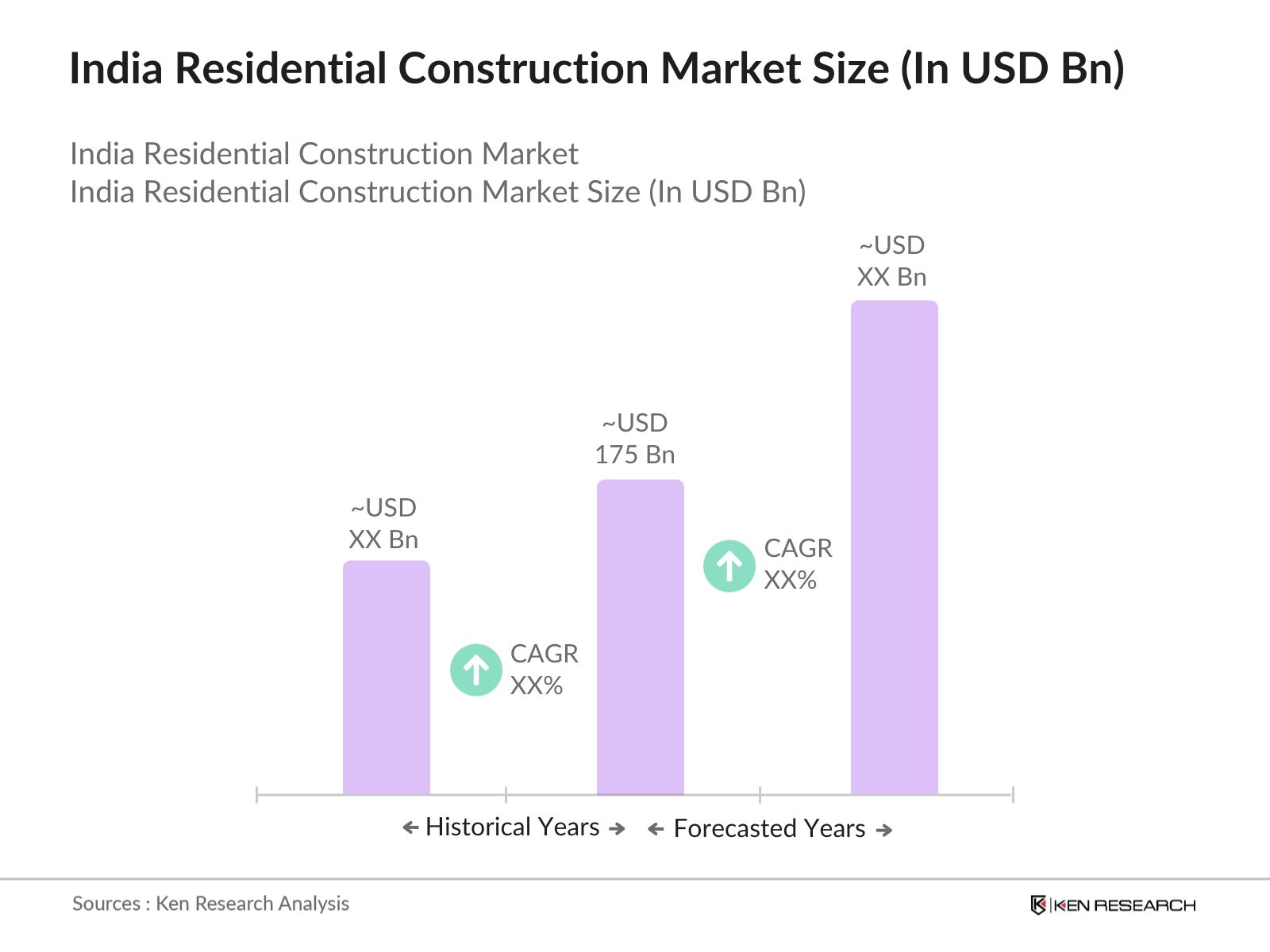

The India residential construction market is valued at USD 175 billion, driven by urbanization, government housing schemes, and rising disposable income among middle-class consumers.

Challenges in the India residential construction market include high land acquisition costs, regulatory delays, and fluctuating prices of raw materials. Additionally, labor shortages and bureaucratic hurdles can slow down project completions.

Key players in the India residential construction market include DLF Limited, Godrej Properties, Prestige Estates Projects, Sobha Limited, and Brigade Enterprises. These companies dominate the market through extensive project portfolios and strong financial positions.

The India residential construction market is propelled by rising urbanization, government support for affordable housing, and increasing demand for luxury homes. Technological advancements and green building practices also play a major role in driving growth.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.