India Rheumatoid Arthritis Market Outlook to 2030

Region:Asia

Author(s):Shambhavi

Product Code:KROD3234

Region:Asia

Author(s):Shambhavi

Product Code:KROD3234

November 2024

82

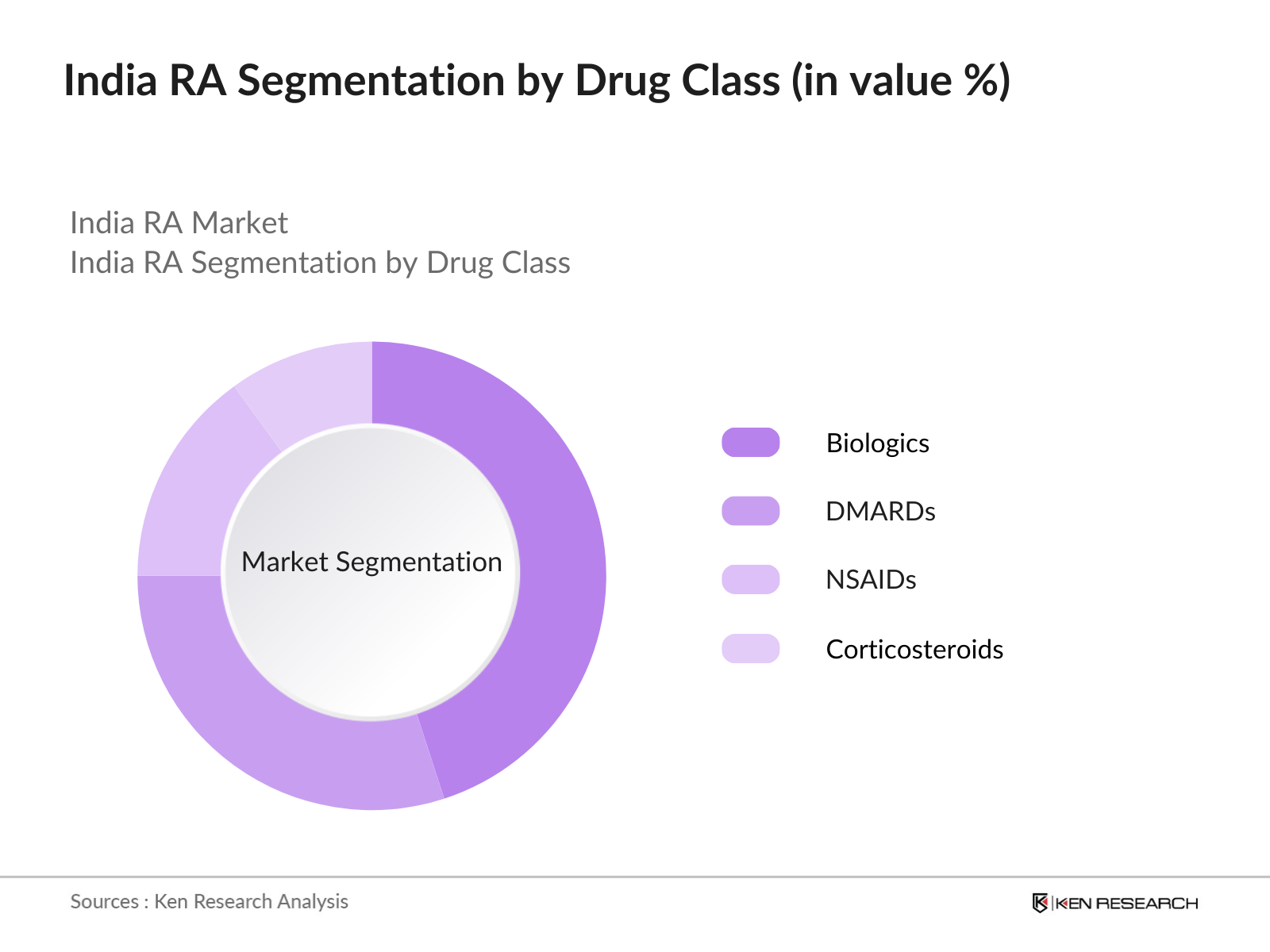

By Drug Class: The India Rheumatoid Arthritis market is segmented by drug class into biologics, DMARDs (Disease Modifying Anti-Rheumatic Drugs), NSAIDs, and corticosteroids. Among these, biologics have emerged as the dominant segment. The prominence of biologics in the Indian Rheumatoid Arthritis market stems from their targeted approach in inhibiting specific pathways involved in the disease process, leading to better patient outcomes. Moreover, the introduction of biosimilars, which offer cost-effective alternatives to expensive biologics, has contributed to their increased uptake across the country.

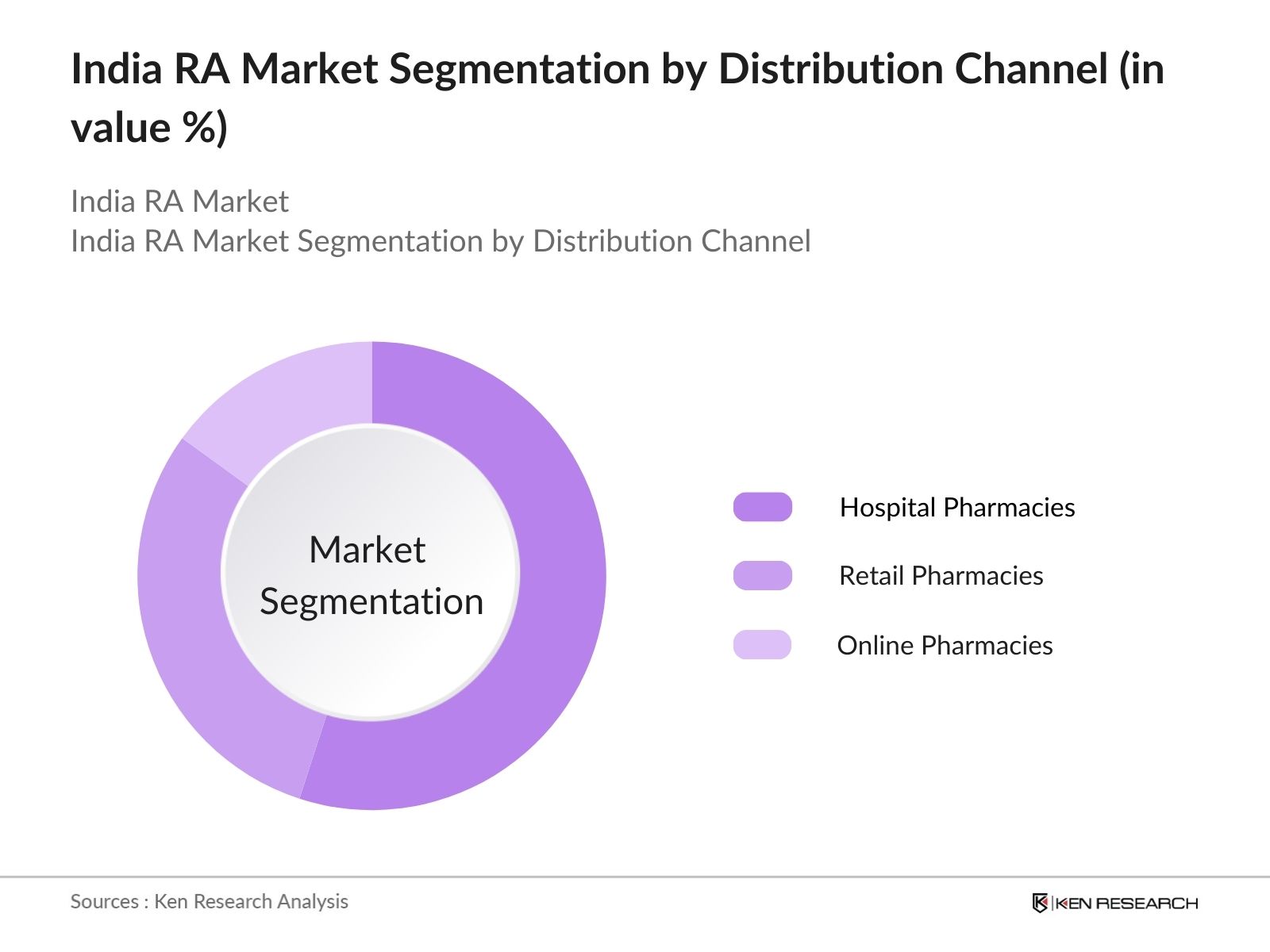

By Distribution Channel: The distribution of Rheumatoid Arthritis treatments is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. Hospital pharmacies hold the dominant market share due to the complex nature of Rheumatoid Arthritis treatments, which often require specialized handling and administration. Additionally, biologic drugs, which are often injected, are commonly dispensed through hospital networks to ensure proper administration under medical supervision.

The India Rheumatoid Arthritis market is consolidated with key pharmaceutical players dominating the market. The major companies leverage extensive distribution networks, strong research and development pipelines, and strategic partnerships with international brands. The India Rheumatoid Arthritis market is dominated by a few major players, including Sun Pharmaceuticals, Cipla, and Dr. Reddys Laboratories, which have strong research and development capabilities and broad distribution networks. Their dominance is further enhanced by their ability to navigate regulatory pathways efficiently and offer innovative treatment options such as biologics and biosimilars.

|

Company |

Year Established |

Headquarters |

Drug Portfolio |

Market Reach |

R&D Investments |

Regulatory Approvals |

Therapeutic Focus |

Collaborations |

|

Sun Pharmaceuticals |

1983 |

Mumbai, India |

||||||

|

Cipla Ltd. |

1935 |

Mumbai, India |

||||||

|

Lupin Limited |

1968 |

Mumbai, India |

||||||

|

Dr. Reddys Laboratories |

1984 |

Hyderabad, India |

||||||

|

Torrent Pharmaceuticals |

1959 |

Ahmedabad, India |

Growth Drivers

Market Challenges

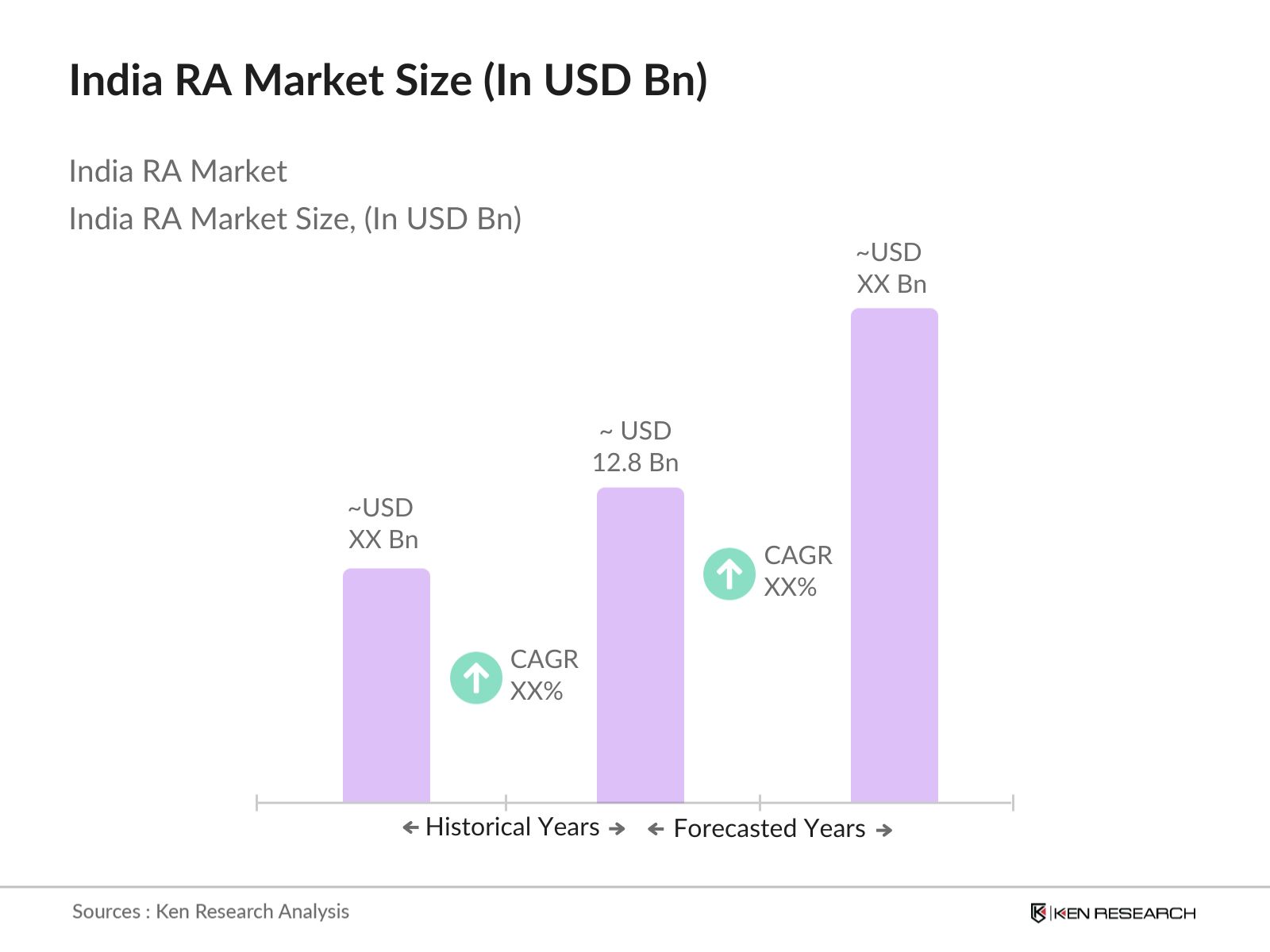

Over the next few years, the India Rheumatoid Arthritis market is expected to experience substantial growth driven by a combination of factors, including the introduction of new biologic therapies, improved patient access to treatment, and a growing elderly population. Government initiatives to improve healthcare access in rural areas and advancements in personalized medicine are also set to fuel market expansion. The increasing prevalence of lifestyle diseases and autoimmune disorders, including rheumatoid arthritis, will necessitate ongoing innovation in drug development and delivery.

Market Opportunities

|

Segment |

Sub-segments |

|

By Treatment Type |

NSAIDs, DMARDs, Biologics, Corticosteroids |

|

By Route of Administration |

Oral, Injectable, Intravenous |

|

By End-User |

Hospitals, Specialty Clinics, Homecare Settings |

|

By Distribution Channel |

Hospital Pharmacies, Retail Pharmacies, Online Pharmacies |

|

By Region |

North India, South India, East India, West India |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Aging Population and Increased Incidence of RA

3.1.2. Increasing Healthcare Spending (Healthcare Expenditure % of GDP)

3.1.3. Advancements in Biologics and Biosimilars (Biologics Market Contribution)

3.1.4. Government Initiatives for Chronic Disease Management (Healthcare Programs)

3.2. Market Challenges

3.2.1. High Cost of RA Treatments (Cost Analysis)

3.2.2. Lack of Early Diagnosis (Patient Access to Diagnosis Rates)

3.2.3. Limited Access to Biologics in Rural Areas (Healthcare Infrastructure)

3.2.4. Competition from Generic Drug Manufacturers (Market Penetration)

3.3. Opportunities

3.3.1. Growth of Telemedicine for RA Care (Telemedicine Adoption Rate)

3.3.2. Expansion of Private Health Insurance (Insurance Penetration)

3.3.3. Increasing Research into New Treatment Modalities (R&D Investment)

3.3.4. Global Clinical Trials in India (Trial Participation Rates)

3.4. Trends

3.4.1. Personalized Treatment for RA Patients (Genomic Applications)

3.4.2. Increasing Adoption of Biosimilars (Biosimilar Market Share)

3.4.3. Collaborations Between Hospitals and Pharma Companies (Partnership Deals)

3.4.4. Use of AI in RA Diagnostics (AI Implementation)

3.5. Government Regulations

3.5.1. Regulation of Biologics and Biosimilars (Approval Process)

3.5.2. Patent Laws Affecting RA Drug Manufacturers (Patent Expirations)

3.5.3. Government Subsidies for RA Drugs (Subsidy Allocation)

3.5.4. National Health Mission for Chronic Diseases (Program Scope)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competitive Ecosystem

4.1. By Treatment Type (In Value %)

4.1.1. Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

4.1.2. Disease-Modifying Anti-Rheumatic Drugs (DMARDs)

4.1.3. Biologics and Biosimilars

4.1.4. Corticosteroids

4.2. By Route of Administration (In Value %)

4.2.1. Oral

4.2.2. Injectable

4.2.3. Intravenous

4.3. By End-User (In Value %)

4.3.1. Hospitals

4.3.2. Specialty Clinics

4.3.3. Homecare Settings

4.4. By Distribution Channel (In Value %)

4.4.1. Hospital Pharmacies

4.4.2. Retail Pharmacies

4.4.3. Online Pharmacies

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West India

5.1. Detailed Profiles of Major Companies

5.1.1. Cipla Ltd.

5.1.2. Sun Pharmaceutical Industries Ltd.

5.1.3. Lupin Limited

5.1.4. Dr. Reddys Laboratories Ltd.

5.1.5. Biocon Limited

5.1.6. Zydus Cadila

5.1.7. Torrent Pharmaceuticals

5.1.8. Glenmark Pharmaceuticals

5.1.9. Aurobindo Pharma

5.1.10. Intas Pharmaceuticals Ltd.

5.1.11. Pfizer Inc.

5.1.12. AbbVie Inc.

5.1.13. Amgen Inc.

5.1.14. Novartis AG

5.1.15. Roche Holding AG

5.2. Cross Comparison Parameters (Revenue, Market Presence, Drug Pipeline, R&D Investment, Geographic Reach, Treatment Portfolio, Strategic Initiatives, No. of Employees)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Indian Drug Approval Process

6.2. Compliance and Regulatory Requirements

6.3. Certification and Licensing

6.4. Guidelines for Biosimilars

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Treatment Type (In Value %)

8.2. By Route of Administration (In Value %)

8.3. By End-User (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

In this phase, we construct an ecosystem map of all key stakeholders in the India RA Market. This includes hospitals, pharmaceutical companies, healthcare providers, and regulatory bodies. We collect data from secondary sources, including industry reports and government publications, to identify critical market variables.

This phase involves analyzing historical data, focusing on key market drivers such as drug availability, the ratio of hospital admissions for RA patients, and treatment outcomes. The data provides a foundation for understanding market penetration and growth patterns.

We validate our market hypotheses through interviews with industry experts, rheumatologists, and pharmaceutical executives. This allows us to refine the market data and gain insights into emerging trends and treatment adoption.

The final phase synthesizes all the collected data, including insights from manufacturers and healthcare providers, into a cohesive report. This phase ensures that the data is accurate and provides actionable insights for industry stakeholders.

The India RA market is valued at INR 12.8 billion, driven by increased awareness, rising prevalence of autoimmune diseases, and a focus on biologic drugs for advanced treatment.

The key challenges in the India RA market include high treatment costs, limited access to biologic drugs in rural areas, and the regulatory complexities surrounding drug approvals.

Key players in the market include Sun Pharmaceuticals, Cipla Ltd., Lupin Limited, and Dr. Reddys Laboratories. These companies have established strong footholds due to their extensive drug portfolios and distribution networks.

The market is propelled by factors such as an aging population, the introduction of cost-effective biosimilars, and increased government initiatives to improve healthcare access, particularly in rural regions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.