India Rigid Plastic Packaging Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD2546

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD2546

October 2024

91

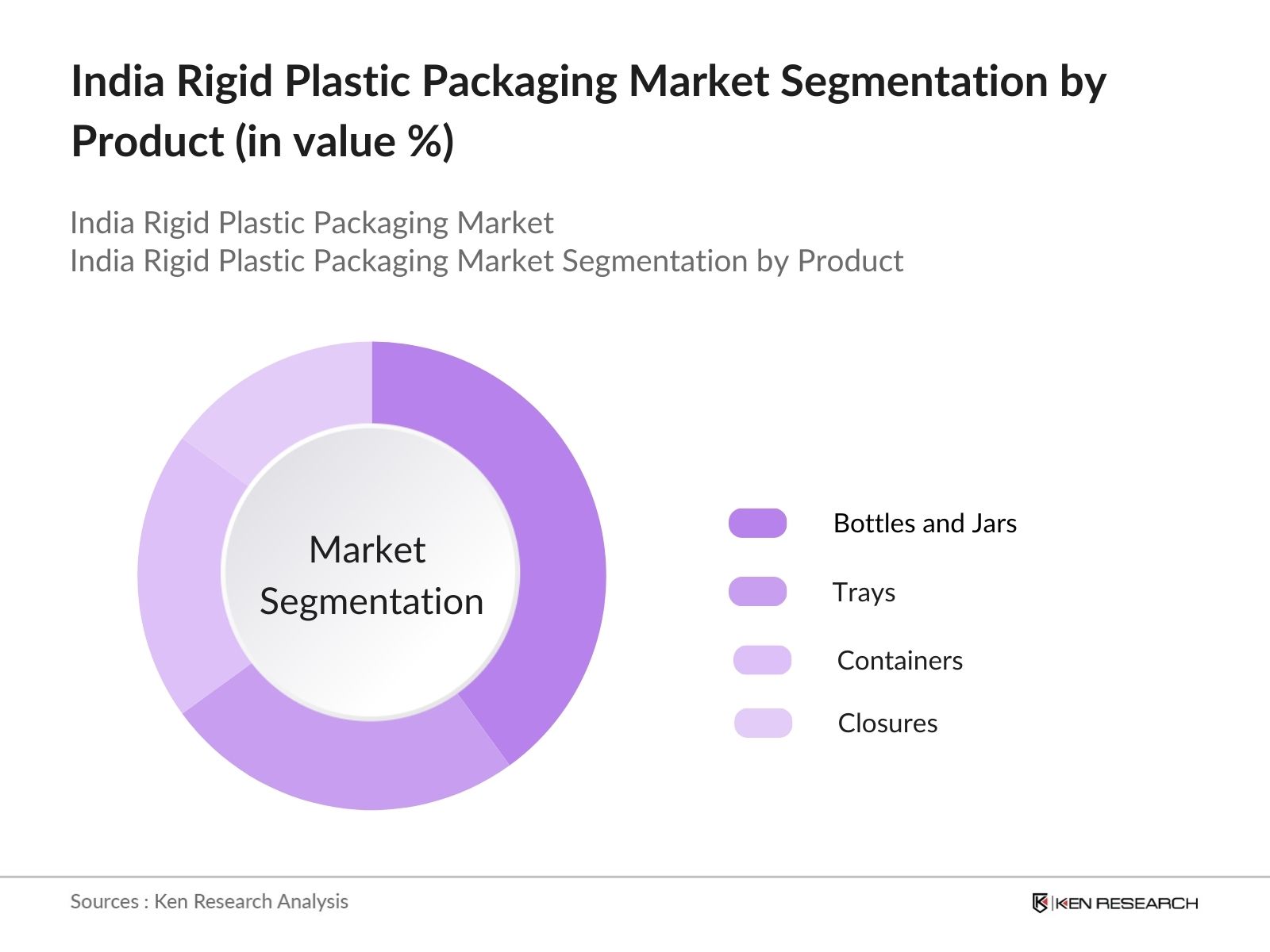

The market is segmented into various factors like product, material, and region.

By Product: The market is segmented by product into bottles and jars, trays, containers, and closures. Bottles and jars held the dominant market share due to their widespread use in the food & beverage and personal care industries. Their dominance is attributed to the increasing consumption of packaged drinks and personal care products.

By Material: The market is segmented by material into PET (Polyethylene Terephthalate), PE (Polyethylene), and PP (Polypropylene). PET dominated the market due to its extensive application in beverage bottles and personal care products. PET is favored for its strength, clarity, and recyclability, which aligns with the growing preference for eco-friendly packaging materials.

By Region: The market is segmented by region into North, South, East, and West. Western India led the largest market share due to the region's strong industrial base and easy access to export channels. The presence of leading FMCG and pharmaceutical manufacturers in states like Maharashtra and Gujarat further consolidates the regions dominance.

|

Company |

Establishment Year |

Headquarters |

|

Amcor Limited |

1860 |

Zurich, Switzerland |

|

RPC Group Plc |

1991 |

Northamptonshire, UK |

|

Berry Global, Inc. |

1967 |

Indiana, USA |

|

Graham Packaging |

1970 |

Pennsylvania, USA |

|

Sonoco Products Co. |

1899 |

South Carolina, USA |

Future trends include a shift toward biodegradable materials, advanced manufacturing technologies, increased adoption of circular economy practices, and stricter government regulations on plastic waste management.

|

By Product |

Bottles and Jars Trays Containers Closures |

|

By Application |

PET PE PP |

|

By Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate and Forecast

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Demand from FMCG Industry

3.1.2. Rising Demand in Pharmaceuticals

3.1.3. E-commerce and Retail Growth

3.1.4. Adoption of Recyclable Plastics

3.2. Market Restraints

3.2.1. Limited Recycling Infrastructure

3.2.2. Raw Material Price Fluctuations

3.2.3. Environmental Concerns Over Plastic Waste

3.2.4. Competition from Alternative Materials

3.3. Market Opportunities

3.3.1. Expansion of Sustainable Packaging

3.3.2. Investments in Recycling Technologies

3.3.3. Growth in Biodegradable Packaging Solutions

3.3.4. Government Regulations Supporting Sustainability

3.4. Market Trends

3.4.1. Rising Consumer Demand for Sustainable Packaging

3.4.2. Technological Advancements in Manufacturing

3.4.3. Circular Economy Adoption in Packaging

3.4.4. Introduction of Smart Packaging Solutions

3.5. Government Regulations and Initiatives

3.5.1. Plastic Waste Management Rules

3.5.2. Ban on Single-Use Plastics

3.5.3. Extended Producer Responsibility (EPR) Programs

3.5.4. Make in India Initiative

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

4.1. By Product Type (in value %)

4.1.1. Bottles and Jars

4.1.2. Trays and Clamshells

4.1.3. Containers

4.1.4. Closures

4.2. By Material Type (in value %)

4.2.1. Polyethylene Terephthalate (PET)

4.2.2. Polypropylene (PP)

4.2.3. Polyethylene (PE)

4.3. By Region (in value %)

4.3.1. North India

4.3.2. South India

4.3.3. East India

4.3.4. West India

5.1. Competitive Parameters (Revenue, Operational Footprint, Production Capacity)

5.1.1. Amcor Limited

5.1.2. Berry Global, Inc.

5.1.3. RPC Group Plc

5.1.4. Graham Packaging Company

5.1.5. Sonoco Products Company

5.1.6. Huhtamaki Group

5.1.7. Alpla Group

5.1.8. Constantia Flexibles

5.1.9. UFlex Ltd.

5.1.10. Essel Propack Ltd.

5.1.11. Jindal Poly Films Ltd.

5.1.12. Tetra Pak India

5.1.13. Pluss Advanced Technologies

5.1.14. Time Technoplast Ltd.

5.1.15. Supreme Industries

5.2. Cross Comparison Parameters (Production Capacity, Number of Employees, Market Presence)

6.1. Market Share Analysis

6.2. Strategic Initiatives (Mergers & Acquisitions, Joint Ventures)

6.3. Key Financial and Operational Metrics

6.4. Investment Landscape (Foreign Direct Investments, Private Equity, Venture Capital

7.1. Environmental Regulations

7.2. Plastic Recycling Policies

7.3. Compliance Standards for Packaging Materials

7.4. Certification Processes

8.1. Forecasted Market Size

8.2. Key Growth Projections

8.3. Impact of Future Regulations on Market Growth

9.1. By Product Type

9.2. By Material Type

9.3. By Region

10.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

10.2. Customer Behavior Analysis

10.3. Marketing Strategies for Expansion

10.4. White Space and Opportunity Analysis

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Collating statistics on this industry over the years, penetration of marketplaces and service providers ratio to compute revenue generated for India Rigid Plastic Packaging industry. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Building market hypothesis and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple packaging companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from such packaging companies.

The India Rigid Plastic Packaging Market was valued at USD 8.2 billion. This expansion is driven by rising demand for durable and lightweight packaging in industries like food & beverage, pharmaceuticals, and consumer goods

Challenges in the India Rigid Plastic Packaging market include limited recycling infrastructure, fluctuating raw material costs, environmental concerns about plastic waste, and competition from alternative packaging materials like glass and biodegradable options.

Key players in the India Rigid Plastic Packaging market include Amcor Limited, Berry Global, RPC Group, Graham Packaging, and Sonoco Products Company. These companies dominate due to their innovations in sustainable packaging and extensive market reach.

The growth of the India Rigid Plastic Packaging market is driven increasing demand in the FMCG and pharmaceutical sectors, rising e-commerce activities, government initiatives promoting recycling, and a shift toward sustainable packaging solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.