India Self Drive Car Rental Market

India Self Drive Car Rental Market: Growth Driven by Urbanization and Tourism Trends 2024–2030

Region:India

Author(s):Aditya

Product Code:KR914

Region:India

Author(s):Aditya

Product Code:KR914

November 2019

164

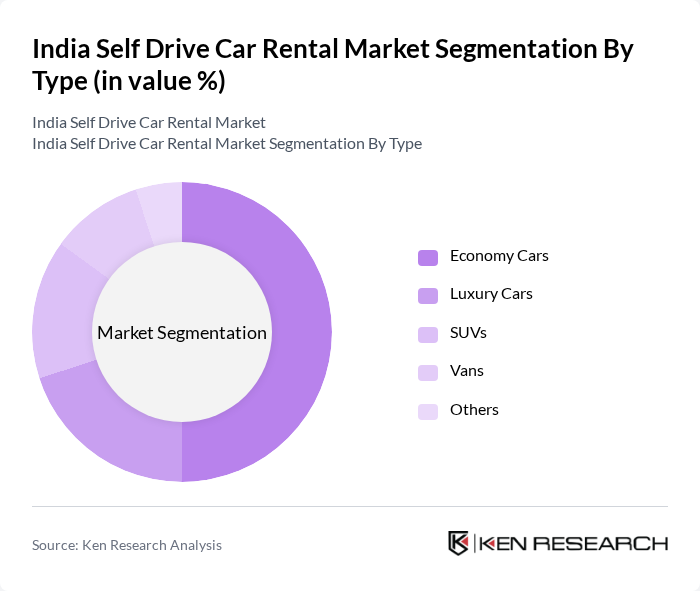

By Type:

The self-drive car rental market is segmented into various types, including Economy Cars, Luxury Cars, SUVs, Vans, and Others. Among these, Economy Cars dominate the market due to their affordability and practicality for everyday use. The rising trend of budget travel and the increasing number of young professionals seeking cost-effective transportation options have significantly contributed to the popularity of this segment. Luxury Cars and SUVs are also gaining traction, particularly among affluent customers and families looking for comfort and space during their travels.

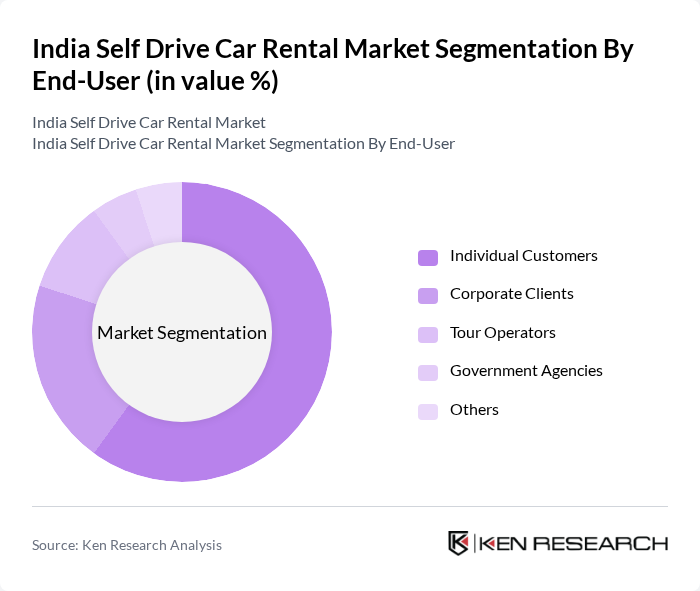

By End-User:

The market is segmented by end-users, including Individual Customers, Corporate Clients, Tour Operators, Government Agencies, and Others. Individual Customers represent the largest segment, driven by the growing trend of personal travel and the increasing preference for self-drive options among millennials and young professionals. Corporate Clients and Tour Operators also contribute significantly to the market, as businesses seek flexible transportation solutions for their employees and tourists look for convenient travel options during their trips.

The India Self Drive Car Rental Market is characterized by a dynamic mix of regional and international players. Leading participants such as Zoomcar, Revv, Myles, Drivezy, Savaari Car Rentals, Ola Rentals, Carzonrent, Avis India, Hertz India, Eco Rent A Car, Trawelltag Cover-More, Gozo Cabs, Bharat Taxi, Drive India Enterprise Solutions, Car Rental India contribute to innovation, geographic expansion, and service delivery in this space.

| Zoomcar | 2013 | Bangalore, India | – | – | – | – | – | – |

| Revv | 2015 | Noida, India | – | – | – | – | – | – |

| Myles | 2013 | Gurgaon, India | – | – | – | – | – | – |

| Drivezy | 2015 | Bangalore, India | – | – | – | – | – | – |

| Savaari Car Rentals | 2006 | Bangalore, India | – | – | – | – | – | – |

| Company | Establishment Year | Headquarters | Group Size (Large, Medium, or Small as per industry convention) | Fleet Utilization Rate | Customer Satisfaction Score | Average Rental Duration | Revenue per Available Car | Pricing Strategy |

|---|

The future of the self-drive car rental market in India appears promising, driven by increasing urbanization and a growing preference for flexible travel options. As domestic tourism continues to rise, companies are likely to expand their services to meet the evolving needs of consumers. Additionally, the integration of advanced technologies and sustainable practices will play a crucial role in shaping the market landscape, ensuring that businesses remain competitive and responsive to customer demands.

| By Type |

Economy Cars Luxury Cars SUVs Vans Others |

| By End-User |

Individual Customers Corporate Clients Tour Operators Government Agencies Others |

| By Region |

North India South India East India West India |

| By Duration of Rental |

Short-Term Rentals Long-Term Rentals Hourly Rentals Others |

| By Booking Channel |

Online Platforms Offline Agencies Mobile Applications Others |

| By Customer Demographics |

Age Group Income Level Travel Purpose Others |

| By Payment Method |

Credit/Debit Cards Digital Wallets Cash Payments Others |

| Scope Item/Segment | Sample Size | Target Respondent Profiles |

|---|---|---|

| Urban Self-Drive Rental Users | 150 | Frequent Renters, Business Travelers |

| Tourism Sector Rental Demand | 100 | Travel Agents, Tour Operators |

| Corporate Fleet Management | 80 | Corporate Travel Managers, HR Executives |

| Consumer Preferences in Vehicle Types | 120 | General Consumers, Car Enthusiasts |

| Impact of Technology on Rental Services | 90 | Tech Developers, Industry Analysts |

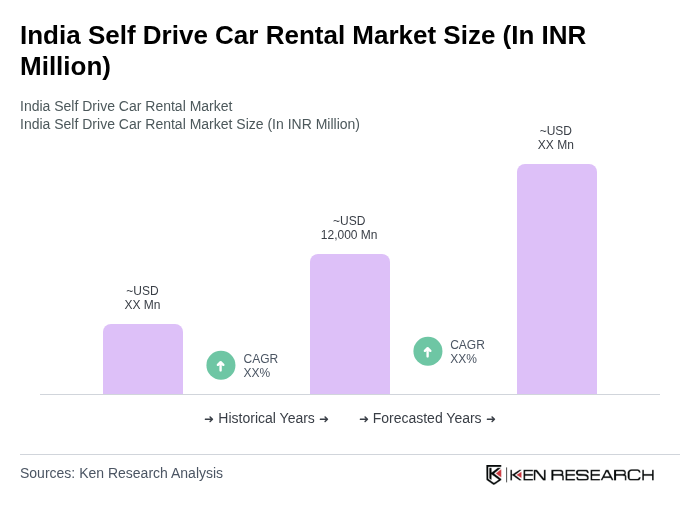

The India Self Drive Car Rental Market is valued at approximately INR 12,000 million, reflecting a significant growth driven by urbanization, increased disposable incomes, and the demand for flexible travel options among consumers.

Key cities dominating the India Self Drive Car Rental Market include Delhi, Mumbai, Bangalore, and Hyderabad. These urban centers are major economic hubs with a high influx of tourists and business travelers, enhancing the demand for self-drive rentals.

Growth drivers include increasing urbanization, a rise in domestic tourism, and technological advancements in booking systems. These factors contribute to a higher demand for flexible and convenient transportation options among consumers.

The Indian government implemented the Motor Vehicle (Amendment) Act in 2023, streamlining the process for obtaining driving licenses and vehicle registrations. This regulation facilitates easier access to self-drive car rentals, promoting market growth.

The self-drive car rental market is segmented into Economy Cars, Luxury Cars, SUVs, Vans, and Others. Economy Cars dominate due to their affordability, while Luxury Cars and SUVs are gaining popularity among affluent customers seeking comfort.

The primary end-users include Individual Customers, Corporate Clients, Tour Operators, and Government Agencies. Individual Customers represent the largest segment, driven by the growing trend of personal travel and the preference for self-drive options.

Challenges include high competition among service providers, regulatory compliance issues, and vehicle maintenance costs. The intense competition can lead to price wars, affecting profit margins and operational efficiency for companies in the market.

Opportunities include expanding services into Tier 2 and Tier 3 cities, introducing electric vehicles into fleets, and developing subscription-based models. These strategies can help companies tap into underserved markets and meet evolving consumer demands.

Technological advancements, such as mobile app usage and enhanced booking systems, are transforming the self-drive car rental market. Companies leveraging technology can streamline operations, improve customer experience, and attract a larger customer base.

The future outlook for the self-drive car rental market in India is promising, driven by increasing urbanization and a growing preference for flexible travel options. Companies are likely to expand services and integrate advanced technologies to remain competitive.

Common payment methods in the self-drive car rental market include Credit/Debit Cards, Digital Wallets, and Cash Payments. The availability of multiple payment options enhances convenience for customers during the rental process.

Self-drive car rental companies focus on customer satisfaction by offering a variety of vehicle options, competitive pricing, and user-friendly booking systems. Additionally, they often implement feedback mechanisms to continuously improve their services.

Corporate clients significantly contribute to the self-drive car rental market by seeking flexible transportation solutions for employees. Companies often utilize rental services for business travel, enhancing the demand for self-drive options in the corporate sector.

Key players in the India Self Drive Car Rental Market include Zoomcar, Revv, Myles, Drivezy, and Savaari Car Rentals. These companies are known for their innovative services and geographic expansion within the market.

Urbanization increases the demand for self-drive car rentals as urban dwellers seek convenient transportation options. The growth of urban centers leads to a higher need for flexible travel solutions, making self-drive rentals an attractive choice for residents and tourists alike.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.