India Shampoo Market Outlook to 2030

Region:India

Author(s):Paribhasha Tiwari

Product Code:KROD4561

Region:India

Author(s):Paribhasha Tiwari

Product Code:KROD4561

December 2024

90

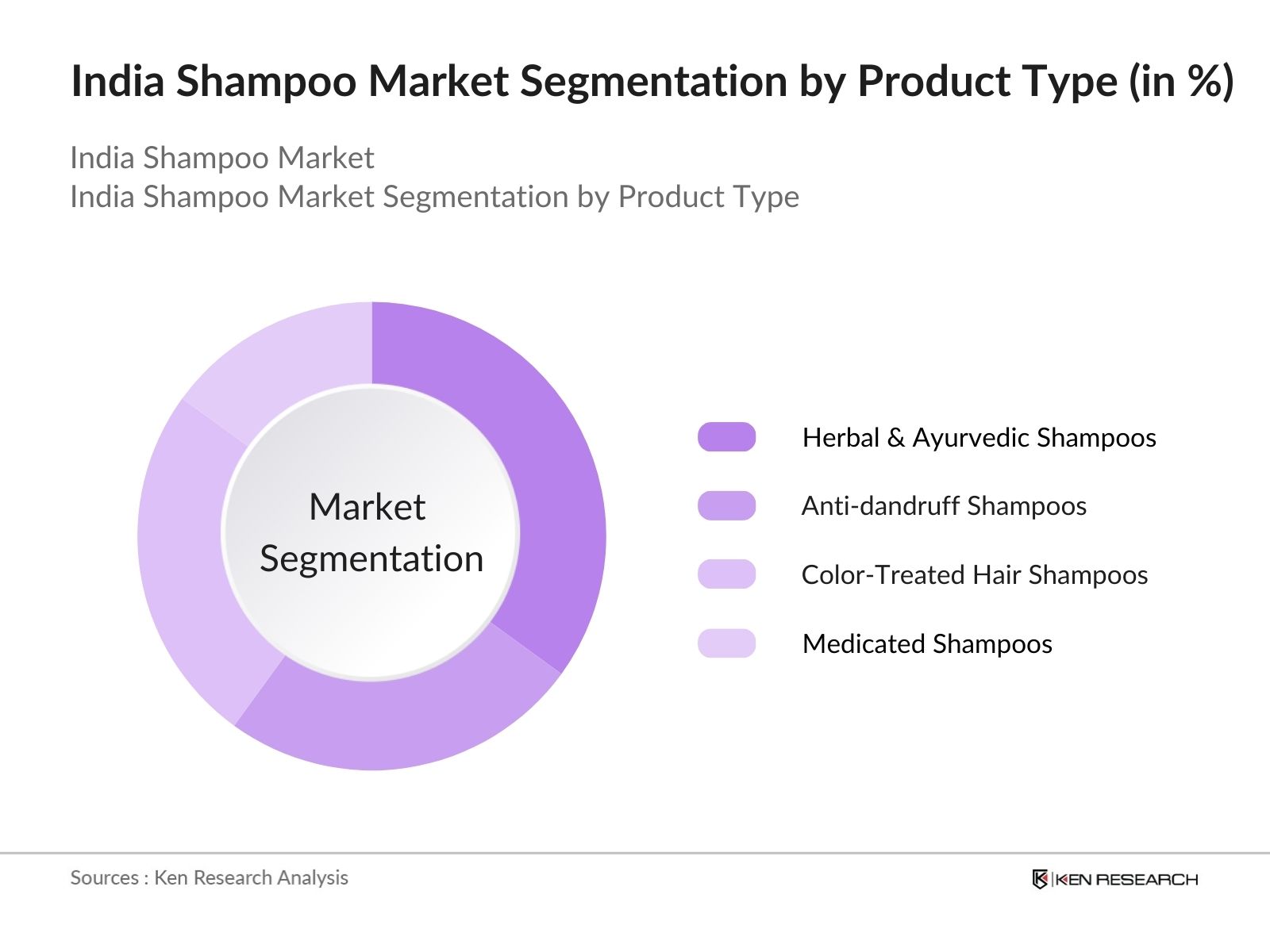

By Product Type: The India shampoo market is segmented by product type into anti-dandruff shampoos, herbal & ayurvedic shampoos, medicated shampoos, and color-treated hair shampoos. Herbal & ayurvedic shampoos dominate the product type segment, owing to the rising consumer preference for natural and organic ingredients. These shampoos are considered safer for long-term use, as they contain fewer synthetic chemicals and are closely aligned with traditional Indian beauty practices. The popularity of herbal brands such as Patanjali and Dabur, along with international interest in natural products, has further bolstered this sub-segment's share.

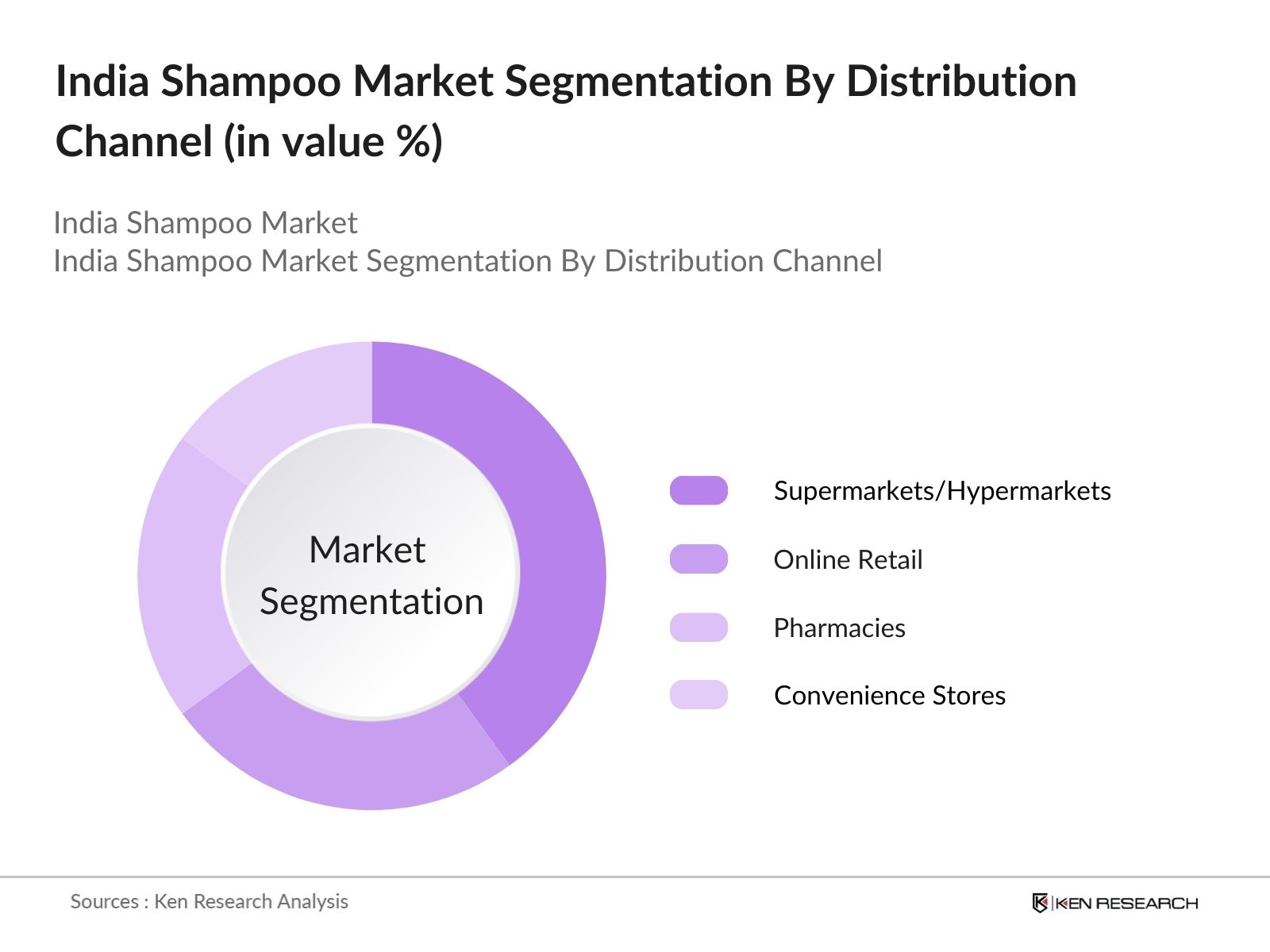

By Distribution Channel: Indias shampoo market is also segmented by distribution channel into supermarkets/hypermarkets, online retail, pharmacies, and convenience stores. Supermarkets and hypermarkets dominate the distribution channel in terms of market share. This is largely due to their widespread presence in urban and semi-urban areas, offering a broad range of product choices. Consumers often prefer to physically assess the quality and variety of shampoos before purchasing, making these channels a convenient option. Moreover, these outlets frequently offer discounts, which attracts cost-conscious shoppers.

The India shampoo market is dominated by a mixture of multinational and domestic players, each vying for a larger consumer base. Major companies, such as Hindustan Unilever Limited, Dabur India Ltd., and Procter & Gamble Co., lead the market due to their extensive distribution networks, strong brand equity, and consistent innovation in product offerings. The local players, with a strong focus on ayurvedic and herbal products, have carved out significant niches, challenging the dominance of established global brands. The competition has intensified with the entry of smaller startups that are focusing on sustainable, organic, and personalized shampoo products.

|

Company Name |

Established |

Headquarters |

Product Portfolio |

R&D Investment |

Sustainability Initiatives |

Distribution Network |

Brand Awareness |

|

Hindustan Unilever Limited |

1931 |

Mumbai, India |

- | - | - | - | - |

|

Dabur India Ltd. |

1884 |

Ghaziabad, India |

- | - | - | - | - |

|

Procter & Gamble Co. |

1837 |

Cincinnati, USA |

- | - | - | - | - |

|

L'Oral India |

1957 |

Mumbai, India |

- | - | - | - | - |

|

Patanjali Ayurved Limited |

2006 |

Haridwar, India |

- | - | - | - | - |

Growth Drivers

Market Challenges

The India shampoo market is expected to experience significant growth over the next five years, driven by rising consumer demand for premium and natural hair care products. The increasing penetration of e-commerce platforms, coupled with growing consumer awareness around ingredient safety and environmental sustainability, will further drive growth. Furthermore, rural expansion efforts by both multinational and local brands are expected to significantly contribute to market size in the coming years.

Market Opportunities

|

By Product Type |

Anti-dandruff Shampoos Herbal & Ayurvedic Shampoos Medicated Shampoos Dry Shampoos Color-Treated Hair Shampoos |

|

By Hair Type |

Normal Hair Oily Hair Dry & Damaged Hair Curly Hair Color-Treated Hair |

|

By Distribution Channel |

Supermarkets/Hypermarkets Convenience Stores Online Retail Pharmacies, Salons |

|

By Packaging Type |

Bottles Sachets Tubes |

|

By Region |

North South East West |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Disposable Income (Per Capita Income Growth, Middle-Class Expansion)

3.1.2. Increased Personal Hygiene Awareness (Government Campaigns, FMCG Penetration)

3.1.3. Product Innovation (Herbal, Anti-Hair Fall, Color-Treated Hair Specific)

3.1.4. Urbanization (Migration to Cities, Western Beauty Standards Influence)

3.2. Market Challenges

3.2.1. High Competition (Local vs. International Brands)

3.2.2. Rising Raw Material Costs (Chemical Ingredients, Natural Extracts)

3.2.3. Supply Chain Disruptions (Logistics, Pandemic Impact)

3.2.4. Distribution Bottlenecks (Rural India, Unorganized Sector Penetration)

3.3. Opportunities

3.3.1. Growth of Online Retail (E-Commerce Adoption, D2C Models)

3.3.2. Expansion in Tier 2 & Tier 3 Cities (Increased Affordability, Improved Distribution)

3.3.3. Organic & Sustainable Products Demand (Eco-friendly Packaging, Clean Labels)

3.3.4. Customization & Personalization (AI-based Hair Care Recommendations, Subscription Models)

3.4. Trends

3.4.1. Shift to Organic & Natural Products (Ayurvedic, Plant-based Ingredients)

3.4.2. Gender-Specific Shampoos (Men's Grooming, Female-Specific Hair Care)

3.4.3. Eco-friendly Packaging (Recyclable, Zero-Waste Packaging)

3.4.4. Salon Professional Shampoos (Premiumization, Salon Partnerships)

3.5. Government Regulation

3.5.1. FDA Regulations for Cosmetic Products (Certification for Herbal Products)

3.5.2. Import Tariffs on Ingredients (Impact on Imported Raw Materials)

3.5.3. CSR Initiatives by Companies (Sustainable Sourcing, Social Impact)

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.8.1. Bargaining Power of Suppliers

3.8.2. Bargaining Power of Buyers

3.8.3. Threat of New Entrants

3.8.4. Threat of Substitutes

3.8.5. Competitive Rivalry

3.9. Competition Ecosystem

3.9.1. Local vs. International Brands (Brand Equity, Consumer Preferences)

3.9.2. Entry Barriers (Investment in R&D, Regulatory Approvals)

3.9.3. Innovation Drivers (R&D, Ingredient Sourcing, Technology Adoption)

4.1. By Product Type (In Value %)

4.1.1. Anti-dandruff Shampoos

4.1.2. Herbal & Ayurvedic Shampoos

4.1.3. Medicated Shampoos

4.1.4. Dry Shampoos

4.1.5. Color-Treated Hair Shampoos

4.2. By Hair Type (In Value %)

4.2.1. Normal Hair

4.2.2. Oily Hair

4.2.3. Dry & Damaged Hair

4.2.4. Curly Hair

4.2.5. Color-Treated Hair

4.3. By Distribution Channel (In Value %)

4.3.1. Supermarkets/Hypermarkets

4.3.2. Convenience Stores

4.3.3. Online Retail

4.3.4. Pharmacies

4.3.5. Salons

4.4. By Packaging Type (In Value %)

4.4.1. Bottles

4.4.2. Sachets

4.4.3. Tubes

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West India

5.1. Detailed Profiles of Major Companies

5.1.1. Hindustan Unilever Limited

5.1.2. Procter & Gamble Co.

5.1.3. L'Oral India

5.1.4. Dabur India Ltd.

5.1.5. ITC Limited

5.1.6. Patanjali Ayurved Limited

5.1.7. Marico Limited

5.1.8. Emami Ltd.

5.1.9. Godrej Consumer Products Limited

5.1.10. Johnson & Johnson Pvt. Ltd.

5.1.11. Himalaya Wellness Company

5.1.12. Colgate-Palmolive India

5.1.13. Parachute

5.1.14. Nivea India Pvt. Ltd.

5.1.15. Garnier (India)

5.2. Cross Comparison Parameters (Market Share %, Distribution Network, Sales Growth %, Innovation Capability, Product Portfolio Size, Sustainability Initiatives, Advertisement Spend %, Price Competitiveness)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. FDA Approval Process

6.2. BIS Standards for Cosmetic Products

6.3. Labeling Regulations (Ingredients, Expiry Dates)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Hair Type (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By Packaging Type (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

In this step, we map the shampoo ecosystem in India by identifying major stakeholders, including manufacturers, retailers, and consumers. Extensive desk research using secondary and proprietary databases helps outline the critical market variables that affect growth, such as consumer preferences, distribution channels, and pricing strategies.

This phase involves compiling historical data on the shampoo market in India, focusing on penetration levels across urban and rural sectors. We analyze revenue trends and consumer preferences, comparing this data against industry standards to ensure its accuracy and reliability.

Our research hypotheses are validated through CATIs with industry experts from FMCG companies and market analysts. These interviews provide valuable insights into market trends, consumer behavior, and company strategies, enabling us to refine our analysis.

We engage with key market players to gain detailed insights into product segmentation, sales performance, and customer feedback. This step helps corroborate our data and ensure that the final report provides an accurate, comprehensive analysis of the India shampoo market.

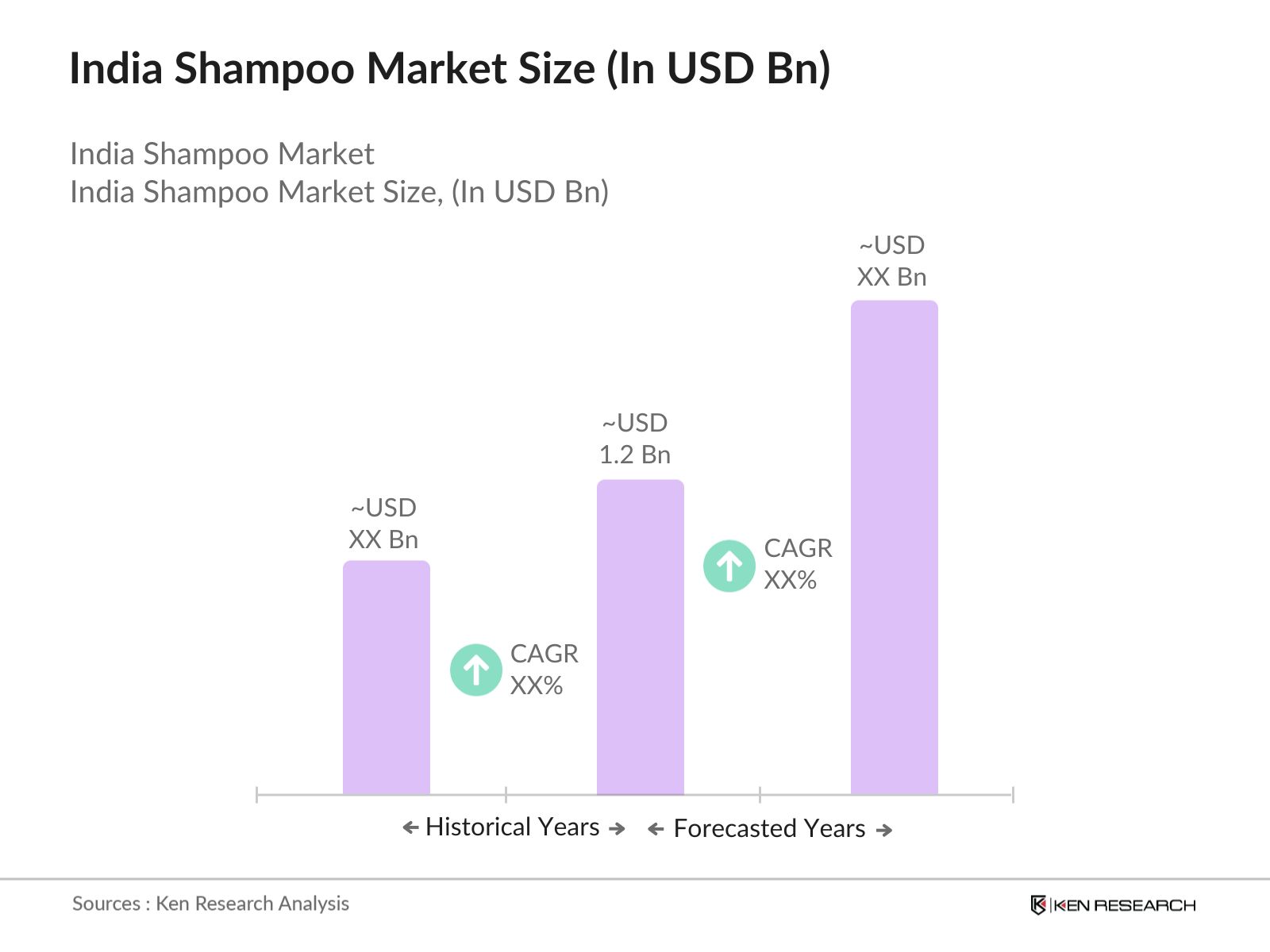

The India shampoo market is valued at USD 1.2 billion, driven by increased demand for personal care products, rising disposable incomes, and greater consumer awareness of grooming and hygiene.

Challenges in the India shampoo market include rising competition, increasing raw material costs, and supply chain disruptions. In addition, penetrating rural markets and addressing the demands for sustainability are key obstacles for companies.

Key players in the India shampoo market include Hindustan Unilever Limited, Dabur India Ltd., Procter & Gamble Co., Patanjali Ayurved Limited, and L'Oral India, driven by their strong distribution networks and innovative product lines.

Growth of India shampoo market is fueled by factors such as urbanization, rising disposable incomes, and the demand for natural and organic products. Additionally, the expansion of e-commerce platforms has contributed to the ease of product availability.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.