India Software Defined Radio Market Outlook to 2030

Region:India

Author(s):Paribhasha Tiwari

Product Code:KROD9223

Region:India

Author(s):Paribhasha Tiwari

Product Code:KROD9223

December 2024

83

Listen to the audio summary

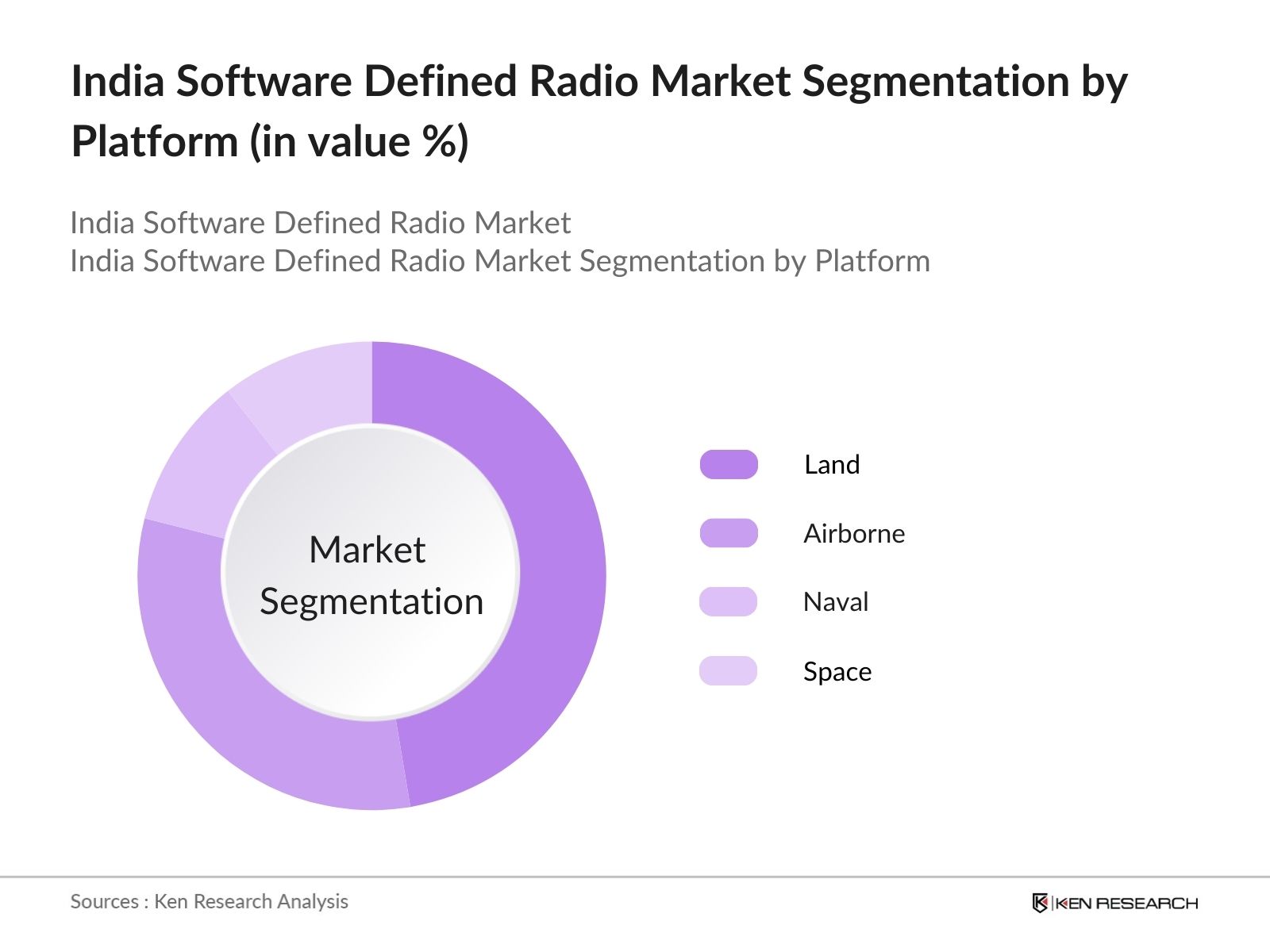

By Platform: The India SDR market is segmented by platform into land, airborne, naval, and space platforms. Land platforms dominate the market due to extensive usage in military communications and disaster management systems. These platforms ensure seamless communication across various terrains and scenarios, a critical factor for Indias vast and diverse geography. The demand for secure and interoperable communication systems by defense forces underpins the segments dominance.

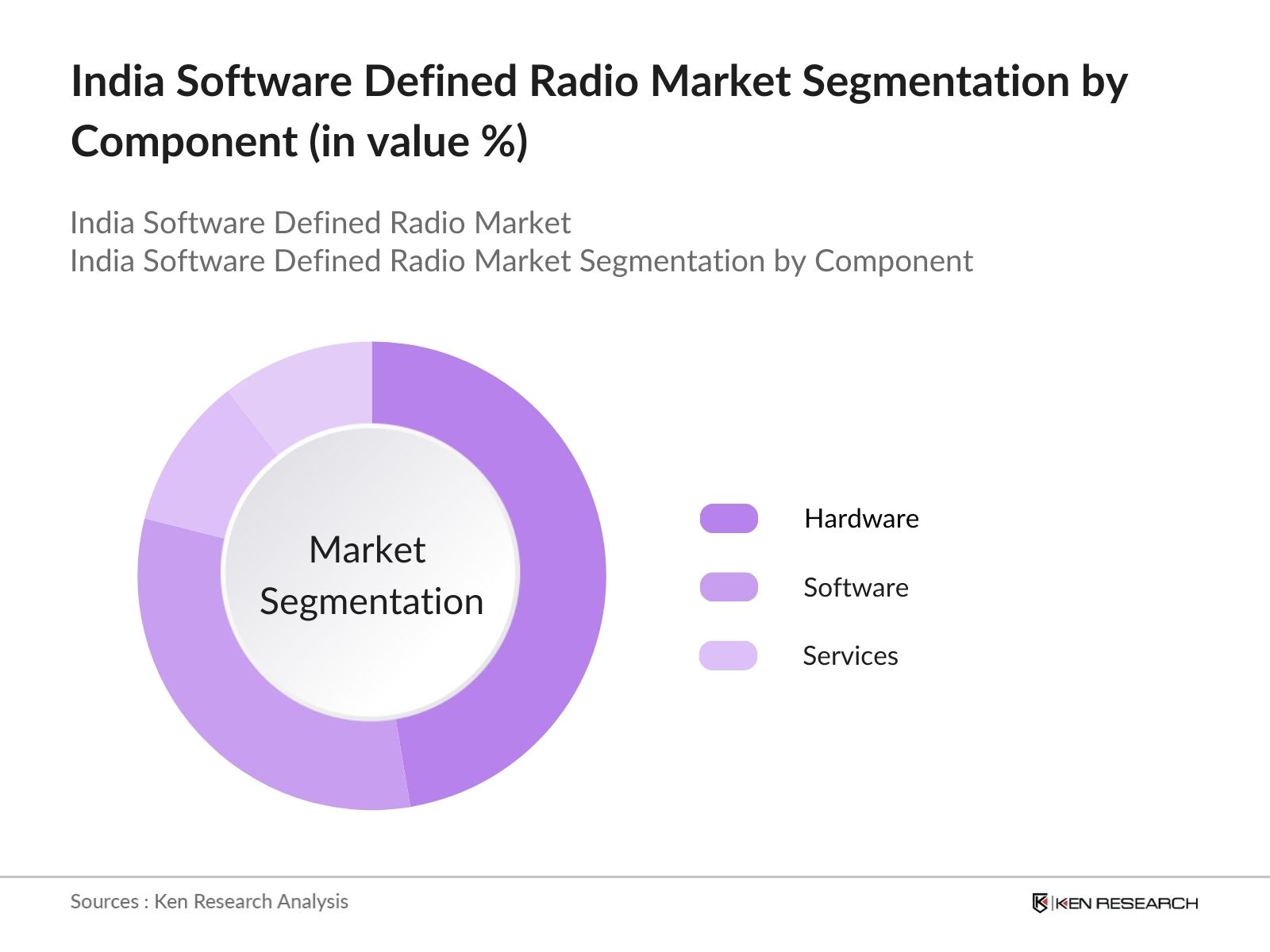

By Component: The India SDR market is segmented by component into hardware, software, and services. Hardware holds the largest share in this segment due to the high cost and demand for sophisticated transmitters, receivers, and auxiliary systems. Advanced technologies like field-programmable gate arrays (FPGAs) and digital signal processors (DSPs) are widely used, contributing to its market leadership.

The India SDR market is dominated by both domestic players and international companies, indicating a competitive and collaborative ecosystem. Companies like Bharat Electronics Limited (BEL) and Tata Power SED lead the market due to their strong ties with government projects and R&D capabilities.

Over the next five years, the India SDR market is expected to experience robust growth driven by increasing defense expenditures, demand for secure communication systems, and advancements in SDR technologies. The government's focus on indigenization and collaboration with global manufacturers is expected to enhance market opportunities further. Key areas such as cognitive radio and space-based SDR systems are likely to gain prominence, aligning with India's strategic initiatives.

|

By Type |

Joint Tactical Radio System (JTRS) Cognitive Radio General Purpose Radio Terrestrial Trunked Radio (TETRA) Others |

|

By Application |

Aerospace and Defense Commercial Telecommunication Others |

|

By Component |

Transmitter Receiver Auxiliary System Software |

|

By Platform |

Land Airborne Naval Space |

|

By Frequency Band |

High Frequency (HF) Very High Frequency (VHF) Ultra-High Frequency (UHF) Others |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Defense Modernization Initiatives

3.1.2. Advancements in Wireless Communication Technologies

3.1.3. Increasing Demand for Interoperable Communication Systems

3.1.4. Government Investments in Communication Infrastructure

3.2. Market Challenges

3.2.1. High Development and Implementation Costs

3.2.2. Technical Complexities in Integration

3.2.3. Regulatory and Spectrum Allocation Issues

3.3. Opportunities

3.3.1. Expansion into Commercial and Civil Sectors

3.3.2. Development of Indigenous SDR Technologies

3.3.3. Collaborations with International Defense Contractors

3.4. Trends

3.4.1. Adoption of Cognitive Radio Technologies

3.4.2. Integration with Internet of Things (IoT) Applications

3.4.3. Miniaturization and Portability Enhancements

3.5. Government Regulations

3.5.1. Defense Procurement Policies

3.5.2. Spectrum Management and Licensing

3.5.3. Standards for Communication Security

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4.1. By Type (In Value %)

4.1.1. Joint Tactical Radio System (JTRS)

4.1.2. Cognitive Radio

4.1.3. General Purpose Radio

4.1.4. Terrestrial Trunked Radio (TETRA)

4.1.5. Others

4.2. By Application (In Value %)

4.2.1. Aerospace and Defense

4.2.2. Commercial

4.2.3. Telecommunication

4.2.4. Others

4.3. By Component (In Value %)

4.3.1. Transmitter

4.3.2. Receiver

4.3.3. Auxiliary System

4.3.4. Software

4.4. By Platform (In Value %)

4.4.1. Land

4.4.2. Airborne

4.4.3. Naval

4.4.4. Space

4.5. By Frequency Band (In Value %)

4.5.1. High Frequency (HF)

4.5.2. Very High Frequency (VHF)

4.5.3. Ultra-High Frequency (UHF)

4.5.4. Others

5.1. Detailed Profiles of Major Companies

5.1.1. Bharat Electronics Limited (BEL)

5.1.2. Tata Power SED

5.1.3. Larsen & Toubro (L&T)

5.1.4. Elbit Systems Ltd.

5.1.5. L3Harris Technologies Inc.

5.1.6. Thales Group

5.1.7. Raytheon Technologies Corporation

5.1.8. Collins Aerospace

5.1.9. General Dynamics Corporation

5.1.10. Leonardo S.p.A.

5.1.11. BAE Systems plc

5.1.12. Rohde & Schwarz GmbH & Co. KG

5.1.13. Indra Sistemas S.A.

5.1.14. Huawei Technologies Co. Ltd.

5.1.15. Ultra Electronics Holdings

5.2. Cross Comparison Parameters

5.2.1. Revenue

5.2.2. Market Share

5.2.3. Product Portfolio

5.2.4. R&D Investment

5.2.5. Regional Presence

5.2.6. Strategic Initiatives

5.2.7. Partnerships and Collaborations

5.2.8. Technological Innovations

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.6.1. Venture Capital Funding

5.6.2. Government Grants

5.6.3. Private Equity Investments

6.1. Defense Communication Standards

6.2. Spectrum Allocation Policies

6.3. Compliance and Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Type (In Value %)

8.2. By Application (In Value %)

8.3. By Component (In Value %)

8.4. By Platform (In Value %)

8.5. By Frequency Band (In Value %)

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The research begins by mapping all major stakeholders in the India SDR market. Extensive desk research and data extraction from credible proprietary databases are conducted to identify variables like defense communication policies, technology adoption rates, and procurement budgets.

Historical data is compiled to evaluate market dynamics, including hardware and software integration trends. A detailed assessment of the interplay between government projects and private sector contributions is also conducted.

Market hypotheses are validated through structured interviews with industry experts and SDR manufacturers. Insights into product performance, technological advancements, and competitive positioning are collected to ensure data reliability.

Comprehensive insights are synthesized through a bottom-up approach, validating segmentation data and cross-referencing it with primary findings. The result is a validated, data-driven report tailored for business professionals in the SDR industry.

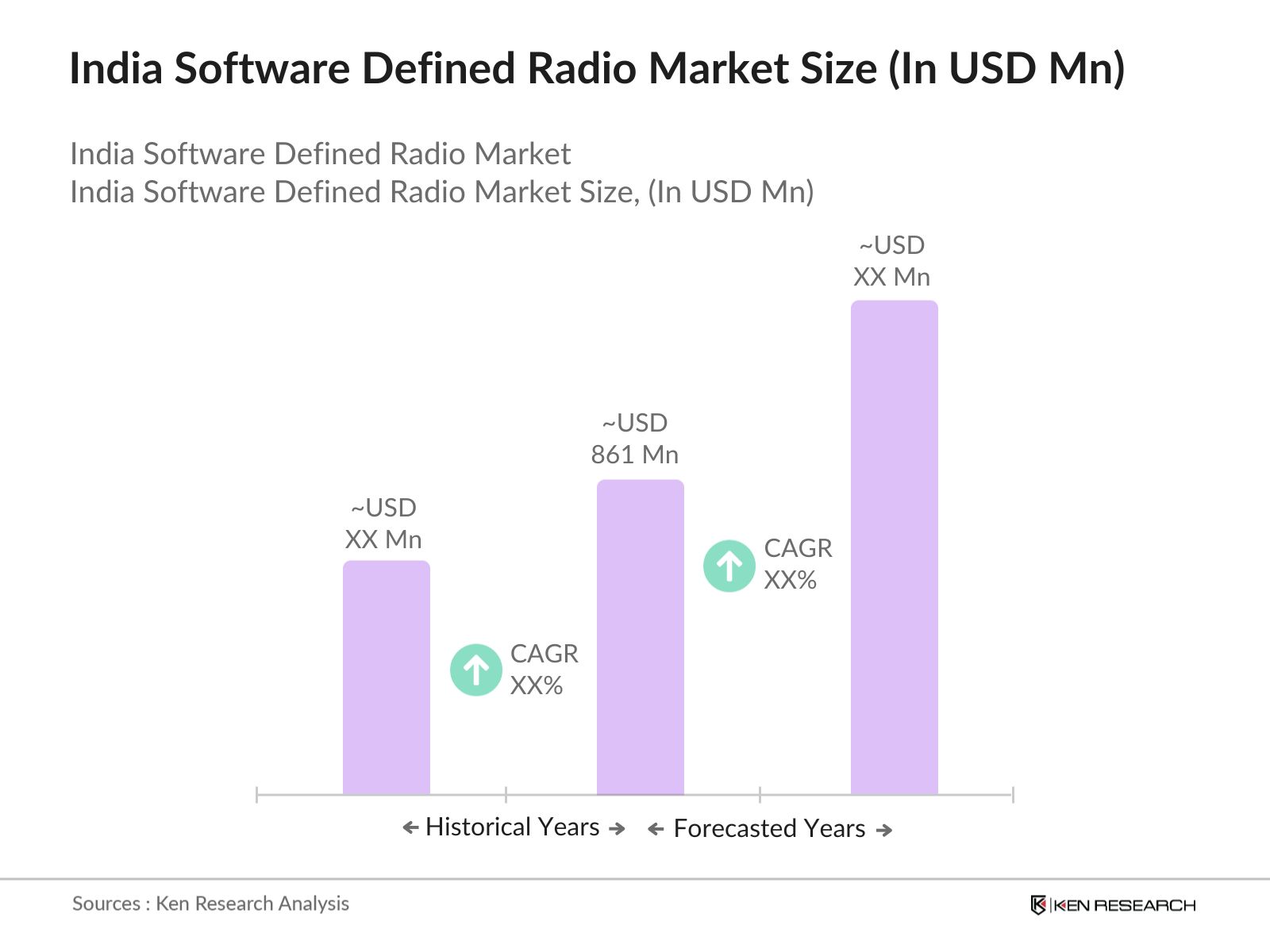

The India Software Defined Radio Market is valued at USD 861 million, primarily driven by defense modernization, demand for secure communication systems, and technological advancements in wireless communication.

Challenges in the India Software Defined Radio Market include high initial costs of development, regulatory and spectrum allocation hurdles, and integration complexities due to diverse application requirements.

Key players in the India Software Defined Radio Market include Bharat Electronics Limited, Tata Power SED, Larsen & Toubro, Harris Corporation, and Thales Group, known for their advanced technologies and strategic collaborations.

The India Software Defined Radio Market is driven by defense modernization, demand for interoperable communication systems, and government initiatives to boost domestic manufacturing.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.