India Telecom Equipment Market Outlook to 2030

Region:India

Author(s):Yogita Sahu

Product Code:KROD9293

Region:India

Author(s):Yogita Sahu

Product Code:KROD9293

November 2024

87

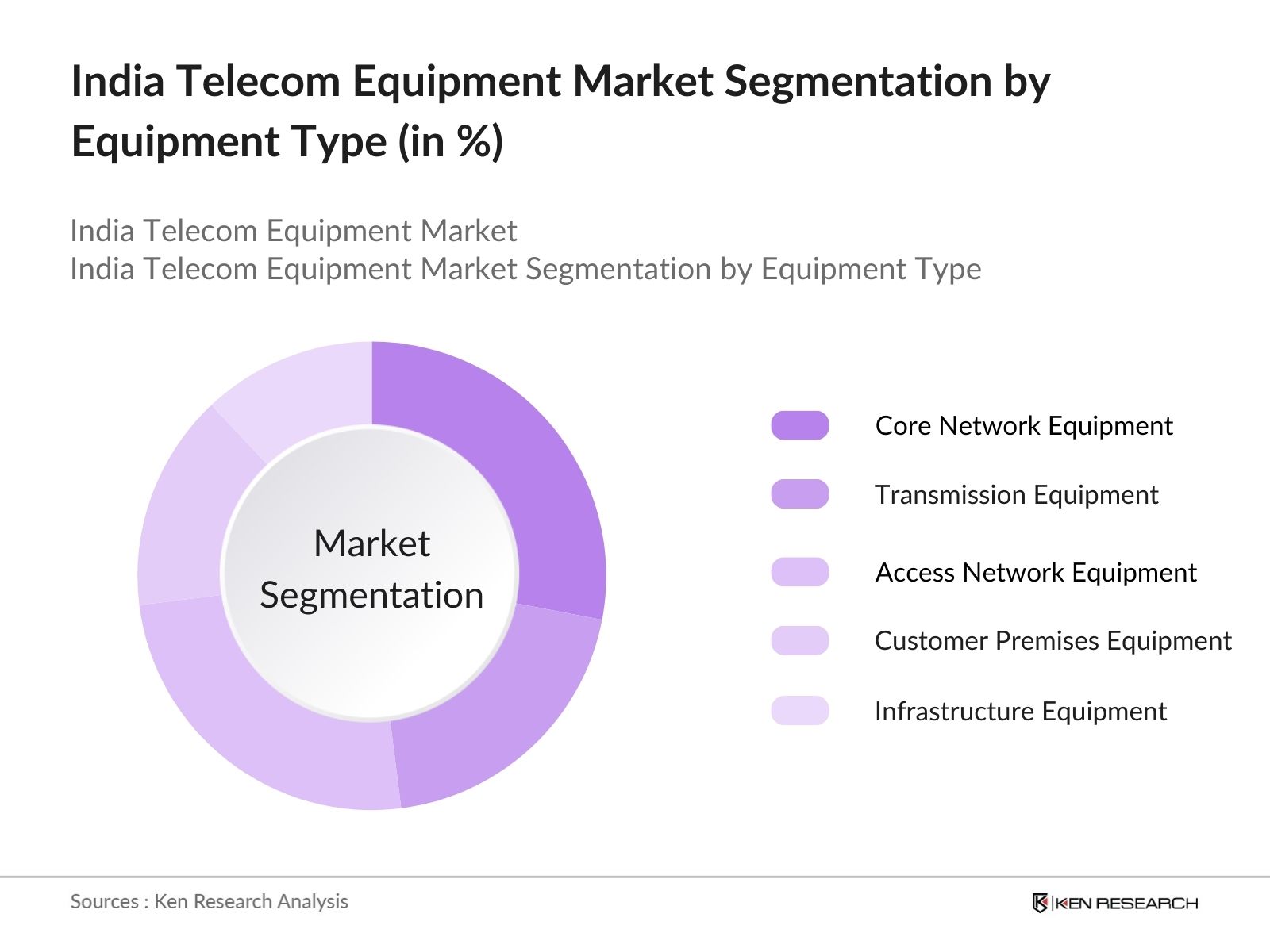

By Equipment Type: The market is segmented by equipment type into Core Network Equipment, Transmission Equipment, Access Network Equipment, Customer Premises Equipment (CPE), and Infrastructure Equipment. Recently, Core Network Equipment has dominated this segment due to increased demand for network upgrades in urban and semi-urban areas. The primary driver behind this dominance is the high requirement for advanced network hardware to support growing 4G and 5G data traffic, ensuring optimal speed and quality for users.

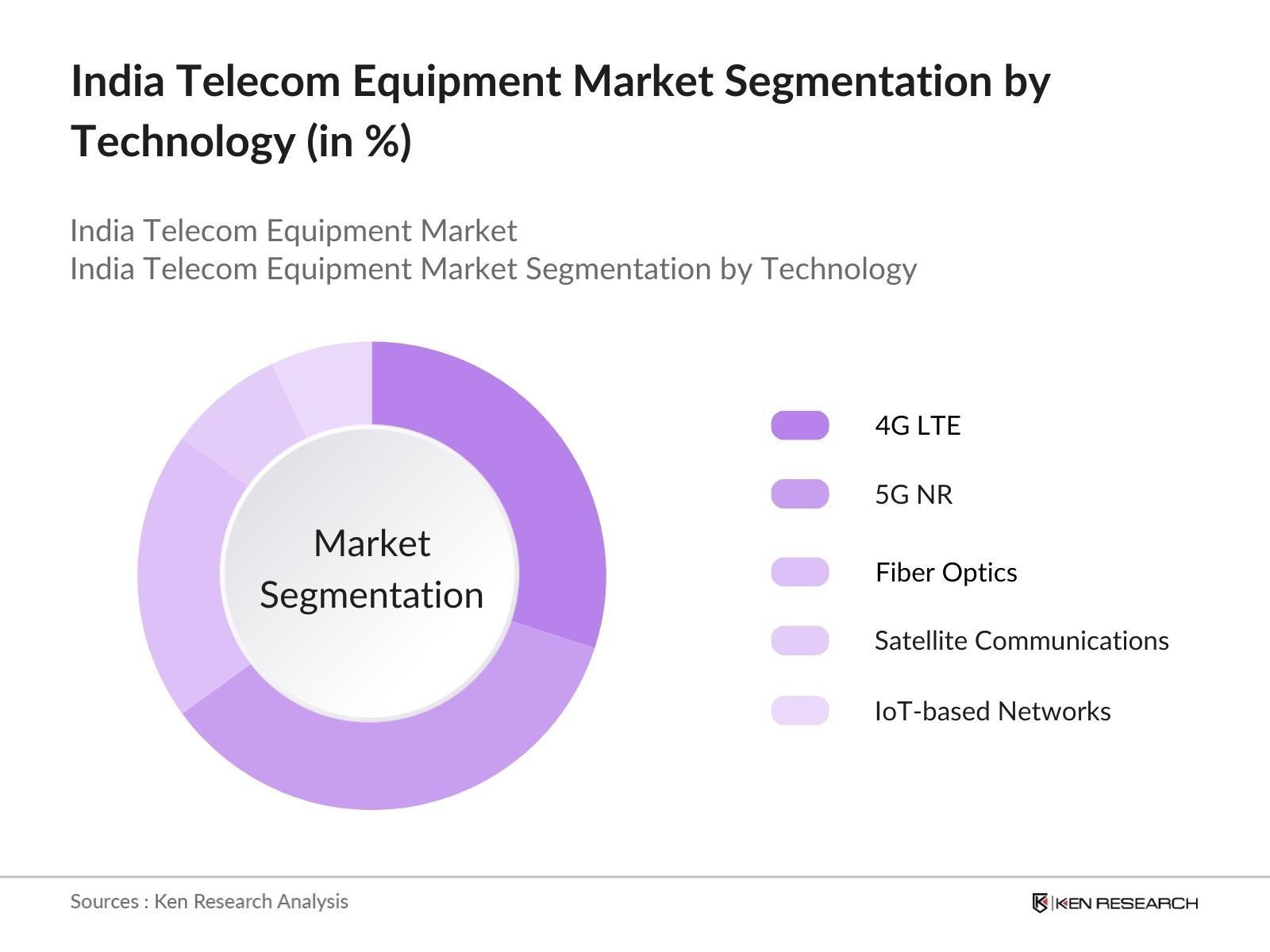

By Technology: The market is also segmented by technology into 4G LTE, 5G NR, Fiber Optics, Satellite Communications, and IoT-based Networks. 5G NR currently leads in market share due to telecom providers heavy investments in deploying 5G infrastructure nationwide. The demand for 5G is fueled by the increased reliance on high-speed mobile internet for applications like video streaming, remote work, and IoT solutions, which have accelerated since the recent surge in digital connectivity.

The market is dominated by several leading players, including both domestic and international firms, which have consolidated their presence through strategic partnerships and product innovations. This competitive concentration allows for technological influence from these players, who set trends and standards within the industry.

The India Telecom Equipment industry is projected to witness substantial growth, driven by continued investment in 5G infrastructure, fiber-optic networks, and the demand for high-speed internet connectivity.

|

Equipment Type |

Core Network Equipment |

|

Technology |

4G LTE |

|

End-User |

Telecom Operators |

|

Sales Channel |

Direct Sales |

|

Region |

North India |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Key Market Insights

1.4 Market Growth Rate Analysis

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1. Digital Infrastructure Expansion

3.1.2. Government Initiatives for Telecom Sector

3.1.3. Surge in Data Consumption

3.1.4. 5G Deployment Plans

3.2. Market Challenges

3.2.1. High Import Dependency

3.2.2. Regulatory Constraints

3.2.3. Infrastructure Costs

3.3. Opportunities

3.3.1. Emerging 5G Applications

3.3.2. Growth in IoT Ecosystem

3.3.3. Increase in Smart City Projects

3.4. Trends

3.4.1. Adoption of Cloud-based Solutions

3.4.2. Demand for Energy-efficient Equipment

3.4.3. Rise in Local Manufacturing under "Make in India"

3.5. Government Regulations

3.5.1. Spectrum Allocation Policies

3.5.2. Compliance and Quality Standards

3.5.3. Import Tariffs and Subsidies

3.5.4. SWOT Analysis

3.5.5. Stakeholder Ecosystem

3.5.6. Porters Five Forces Analysis

3.5.7. Competitive Landscape Overview

4.1. By Equipment Type (In Value %)

4.1.1. Core Network Equipment

4.1.2. Transmission Equipment

4.1.3. Access Network Equipment

4.1.4. Customer Premises Equipment (CPE)

4.1.5. Infrastructure Equipment

4.2. By Technology (In Value %)

4.2.1. 4G LTE

4.2.2. 5G NR

4.2.3. Fiber Optics

4.2.4. Satellite Communications

4.2.5. IoT-based Networks

4.3. By End-User (In Value %)

4.3.1. Telecom Operators

4.3.2. Internet Service Providers (ISPs)

4.3.3. Enterprises

4.3.4. Residential

4.4. By Sales Channel (In Value %)

4.4.1. Direct Sales

4.4.2. Distributors and Resellers

4.4..3 Online Sales

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West India

4.5.5. Central India

5.1. Detailed Profiles of Major Companies

5.2. Huawei Technologies Co., Ltd.

5.3. Ericsson India Pvt. Ltd.

5.4. Nokia India Pvt. Ltd.

5.5.Samsung Electronics Co., Ltd.

5.6. Cisco Systems, Inc.

5.7. ZTE Corporation

5.8. Ciena Corporation

5.9. Juniper Networks

5.10. NEC Corporation

5.11. Bharti Infratel

5.12. Sterlite Technologies Ltd.

5.13. HFCL Limited

5.14. Tejas Networks

5.15. ITI Limited

5.16. Corning Incorporated

5.17. Cross Comparison Parameters (Headquarters, Revenue, Product Portfolio, Market Share, R&D Investments, Global vs. Domestic Revenue Ratio, Service Offerings, Customer Reach)

5.17.1. Market Share Analysis

5.17.2. Strategic Initiatives

5.17.3. Mergers and Acquisitions

5.17.4. Investment Analysis

5.17.5. Venture Capital Funding

5.17.6. Government Grants

5.17.7. Private Equity Investments

6.1. Licensing and Spectrum Management

6.2. Import and Export Regulations

6.3. Safety and Compliance Standards

6.4. Telecom Licensing Policies

7.1. Future Market Size Projections

8.1. Key Factors Driving Future Market Growth

8.1. By Equipment Type (In Value %)

8.2. By Technology (In Value %)

8.3. By End-User (In Value %)

8.4. By Sales Channel (In Value %)

8.5 By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Suggested Marketing Strategies

9.4. White Space Opportunity Analysis

Disclaimer Contact Us

This initial step involved building an ecosystem map for the India Telecom Equipment Market, identifying primary stakeholders through desk research and secondary databases. Key variables influencing the market, such as infrastructure demand and regulatory changes, were isolated.

Historical data was aggregated to analyze market penetration and identify patterns in equipment demand. Additionally, telecom provider data was examined to gauge market demand across different segments and technology adoption.

Hypotheses were tested via interviews with industry experts across telecom firms, gaining insights on financial trends, strategic priorities, and customer needs. This process validated the derived market data and refined our projections.

Insights were synthesized through discussions with telecom providers, validating the findings against primary market metrics to ensure precision. The final analysis provided a comprehensive and well-validated overview of the market.

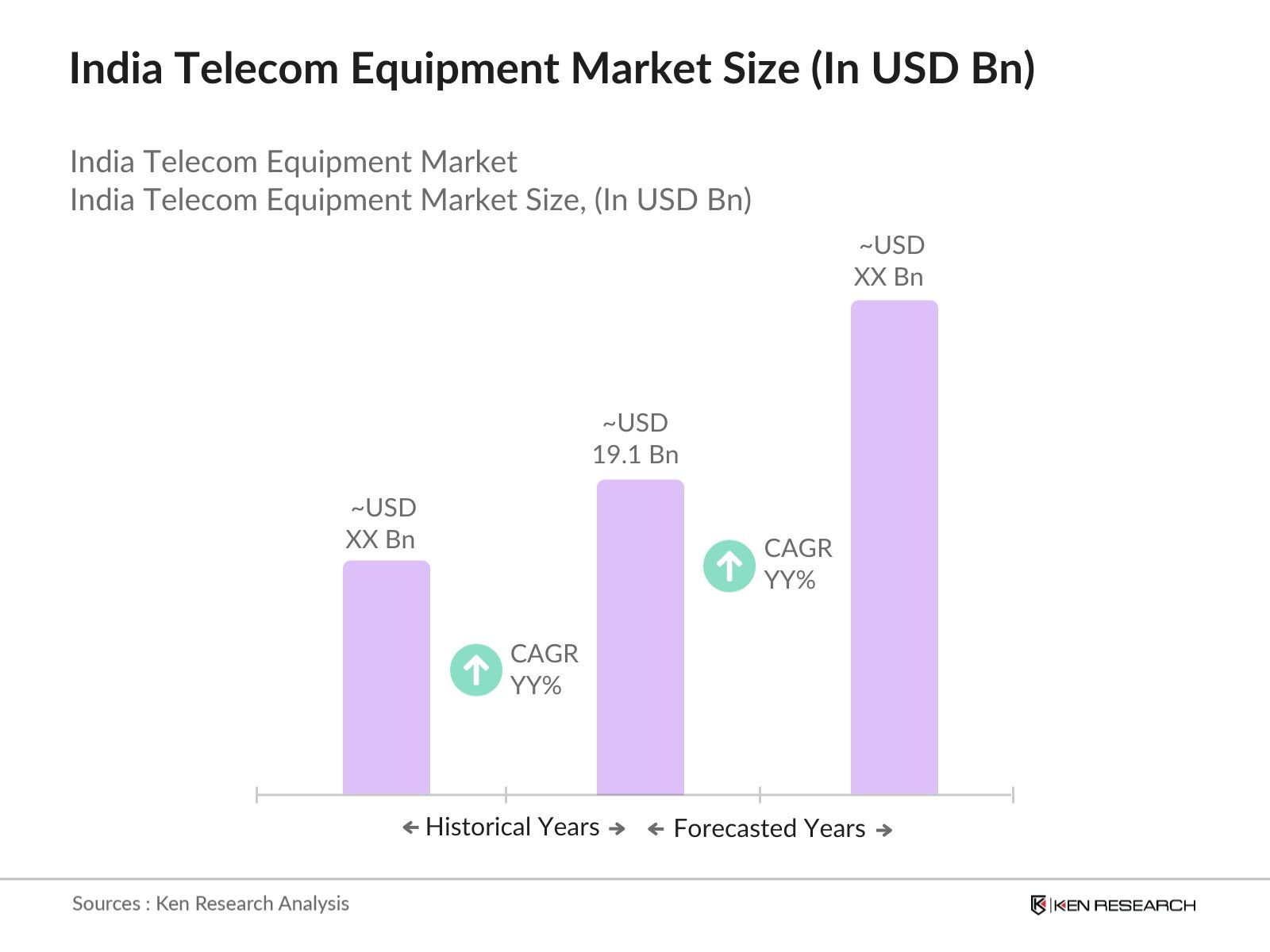

The India Telecom Equipment Market is valued at USD 19.1 billion, with substantial demand driven by government-backed initiatives and the expansion of 4G and 5G networks.

Challenges in the India Telecom Equipment Market include high import dependency, regulatory restrictions, and the escalating cost of network infrastructure, which impact market expansion and profitability.

Key players in the India Telecom Equipment Market include Huawei Technologies, Ericsson India, Nokia India, Samsung Electronics, and Cisco Systems, which dominate due to their advanced product portfolios and extensive distribution networks.

Growth in the India Telecom Equipment Market is propelled by the Digital India initiative, increasing data consumption, and the rollout of 5G infrastructure, supporting digital transformation and connectivity.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.