India Telecom Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD3488

November 2024

94

About the Report

India Telecom Market Overview

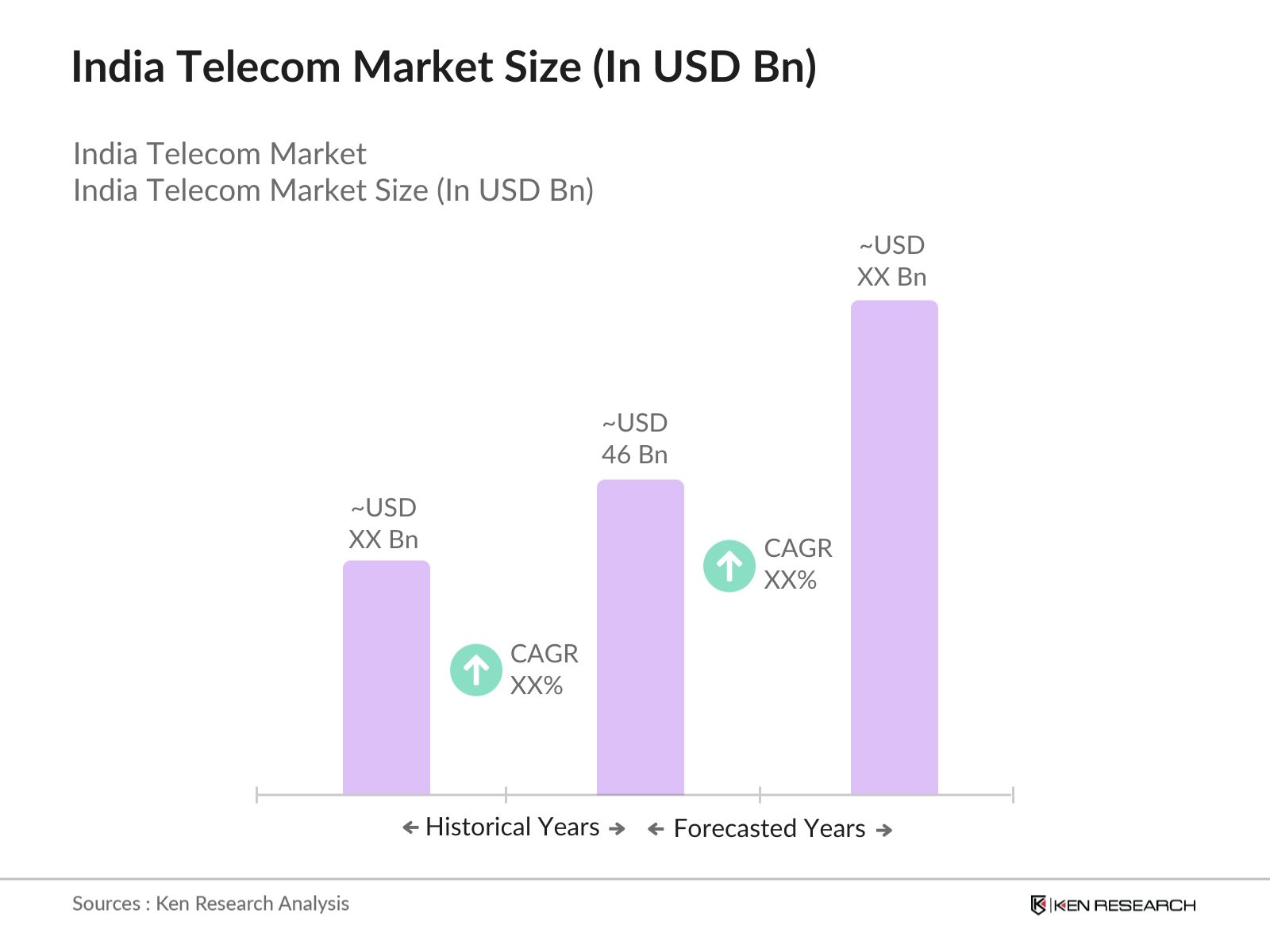

- The India Telecom market, valued at USD 46 billion, is driven by an exponential increase in data consumption, affordability of mobile services, and the expansion of 4G and 5G infrastructure. Major initiatives like the Digital India program have catalyzed growth, alongside investments in network infrastructure, which have been critical in enhancing internet access and mobile coverage across urban and rural areas. These factors have combined to shape a robust and evolving telecom market.

- Metropolitan cities such as Mumbai, Delhi, and Bengaluru dominate the telecom market due to their large population bases, high income levels, and demand for advanced telecommunications services. Additionally, these cities serve as tech hubs with a highly concentrated user base for internet and mobile services, which drives investments from telecom providers in terms of network upgrades and technology deployments, ensuring that these cities remain dominant in the market.

- Indias OTT market, driven by platforms like Netflix, Amazon Prime, and Hotstar, is expected to have over 480 million active users by end of 2024. With telecom operators offering bundled data and subscription packages, OTT content consumption is witnessing a surge. In 2023, Indian viewers consumed over 1.5 billion hours of content across streaming platforms. Telecom operators have become critical partners for OTT providers, leveraging data packs and offering content delivery services. This trend fuels further data consumption, providing telecom operators with new opportunities for revenue generation.

India Telecom Market Segmentation

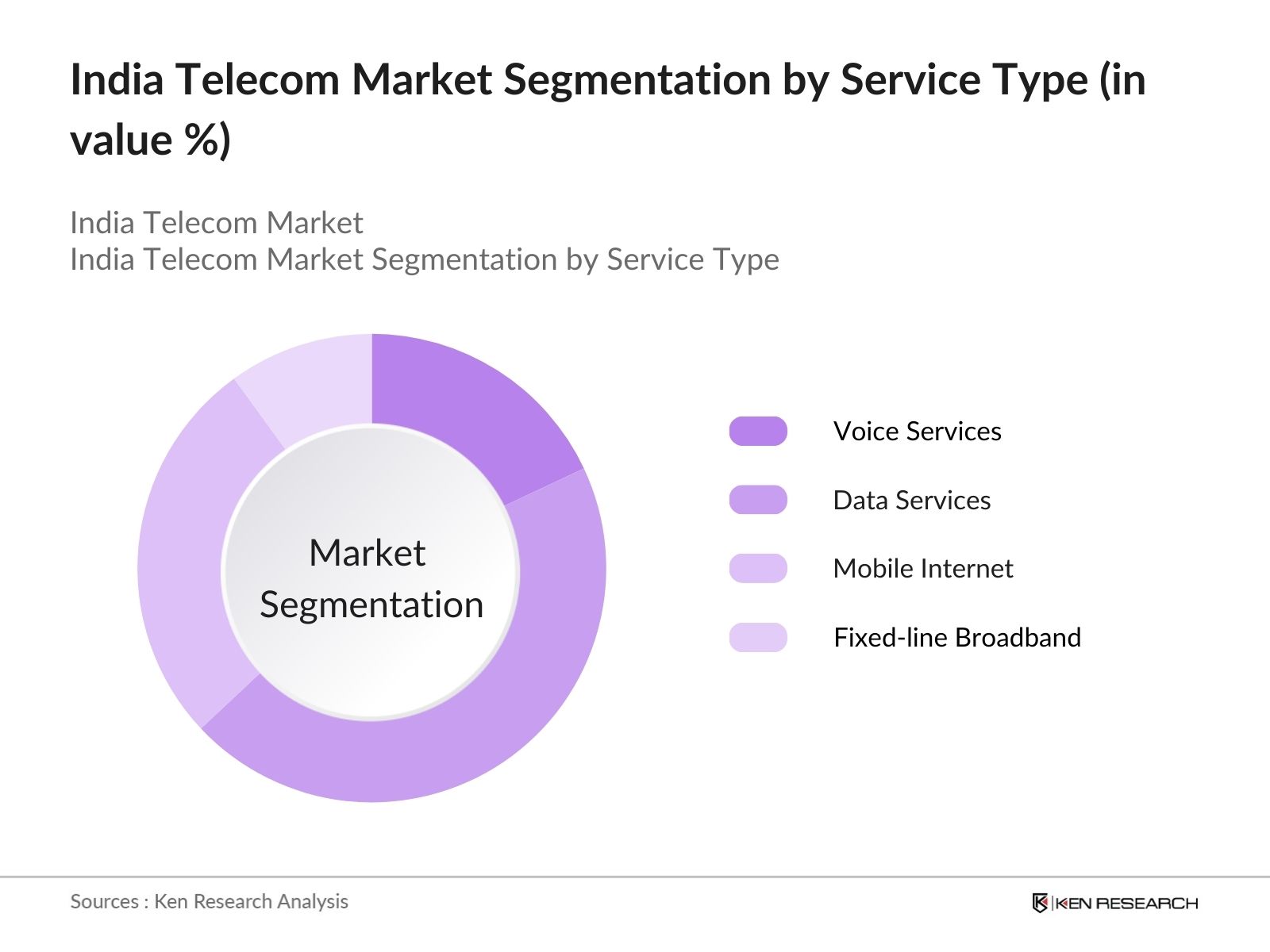

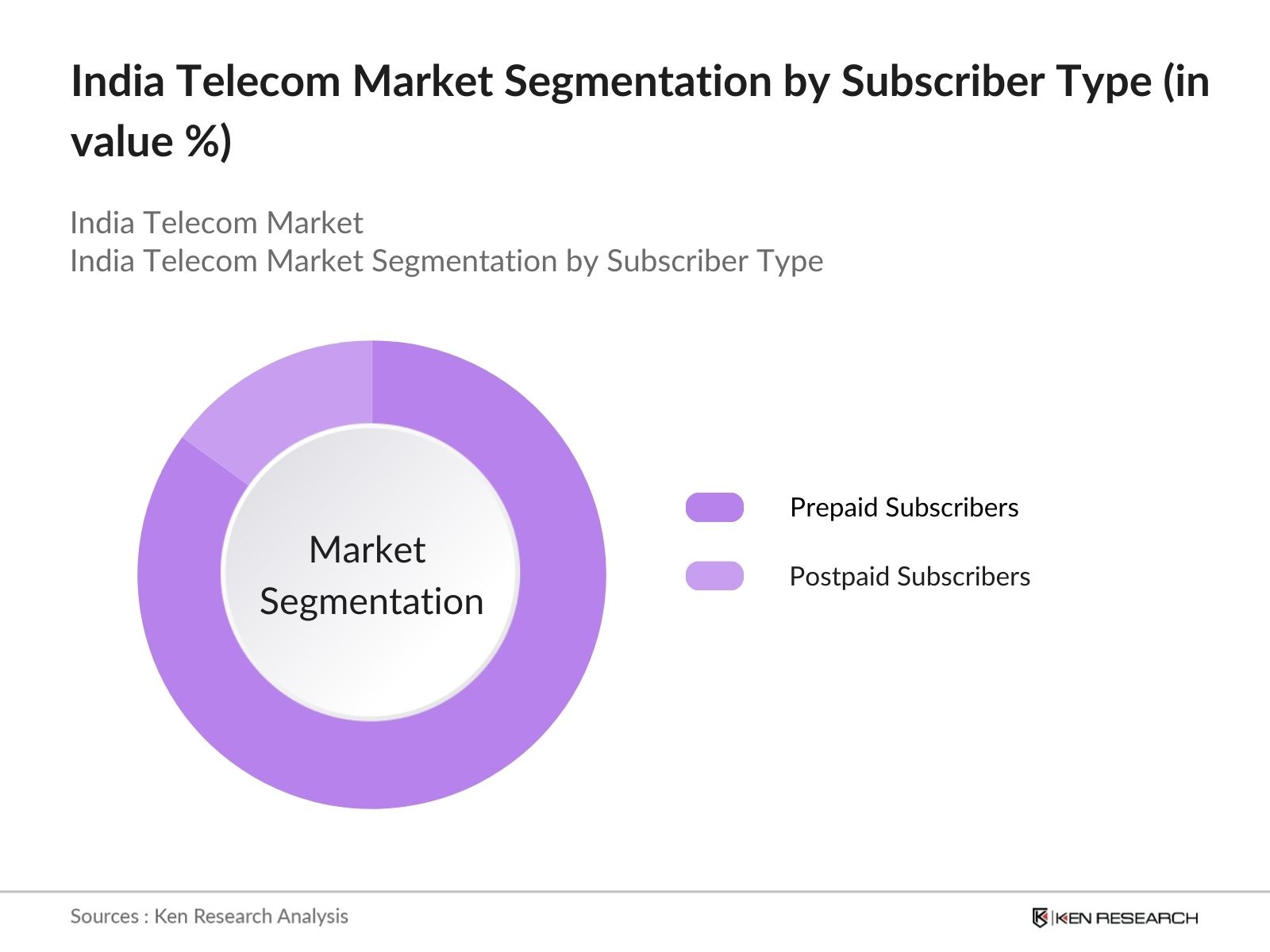

The India Telecom Market is segmented by service type, subscriber type, network type, end-user industry, and geographical region.

- By Service Type: The India Telecom market is segmented by service type into voice services, data services, mobile internet, and fixed-line broadband. Data services dominate the service type segment due to the increasing consumption of data driven by the proliferation of smartphones, video streaming platforms, and social media usage. Additionally, the surge in demand for remote work and online education post-2020 has further solidified the prominence of data services as a key revenue generator for telecom operators.

- By Subscriber Type: The market is also segmented by subscriber type into prepaid and postpaid subscribers. Prepaid subscribers account for a significant portion of the market share due to the affordability and flexibility of prepaid plans. Prepaid plans are popular across a wide demographic, particularly among the lower-income segments and rural areas, as they offer a low entry barrier and pay-as-you-go convenience, making them accessible to a large population.

India Telecom Market Competitive Landscape

The India Telecom market is dominated by a few key players, including Bharti Airtel, Reliance Jio, Vodafone Idea, and Bharat Sanchar Nigam Limited (BSNL). This market consolidation highlights the significant influence of these companies in terms of pricing power, service delivery, and technological advancements. Global technology providers such as Cisco Systems and Ericsson also play a key role by supplying the critical infrastructure required for the deployment of next-generation networks like 5G.

|

Company |

Establishment Year |

Headquarters |

Market Penetration |

Subscriber Base (Mn) |

Revenue (USD Bn) |

ARPU (USD) |

5G Rollout |

Spectrum Holdings (MHz) |

|

Bharti Airtel |

1995 |

New Delhi, India |

- |

- |

- |

- |

- |

- |

|

Reliance Jio |

2007 |

Mumbai, India |

- |

- |

- |

- |

- |

- |

|

Vodafone Idea |

2018 |

Mumbai, India |

- |

- |

- |

- |

- |

- |

|

Bharat Sanchar Nigam Ltd |

2000 |

New Delhi, India |

- |

- |

- |

- |

- |

- |

|

Cisco Systems |

1984 |

San Jose, USA |

- |

- |

- |

- |

- |

- |

India Telecom Market Analysis

India Telecom Market Growth Drivers

- Increasing Smartphone Penetration: India's smartphone user base is projected to exceed900 millionby 2025, supported by affordable devices and initiatives aimed at enhancing connectivity in both urban and rural areas. As of 2024, over70%of mobile users in India are indeed smartphone users. The government's "Digital India" initiative is crucial in promoting internet access and digital literacy, further accelerating smartphone adoption, especially in rural regions. This trend significantly impacts data consumption and mobile application usage within the telecom sector.

- Affordable Data Pricing: India continues to have some of thelowest mobile data pricesglobally, with average rates aroundINR 7 per GBas of 2023, down from INR 50 per GB in 2018. This significant reduction has led to increased data consumption, with over12 billion GBconsumed monthly. Major telecom operators like Reliance Jio have implemented aggressive pricing strategies that enhance accessibility across various socioeconomic classes, thereby boosting the adoption of digital services.

- Expanding 4G/5G Infrastructure: The4G networkin India has reached over95%of the population, with substantial investments in5G infrastructure. As of mid-2024, telecom companies have deployed more than150,000 5G base stations, making these services available in key urban areas. Investments in network upgrades reached approximatelyINR 2.2 trillionin 2023. This expansion supports industries reliant on high-speed internet, such as cloud computing and mobile streaming services, while also benefiting education and healthcare sectors in rural areas.

India Telecom Market Challenges

- Spectrum Scarcity: Indias telecom industry does facespectrum scarcity, with approximately680 MHzavailable for mobile communication, which is notably lower than the global average. As of 2024, telecom operators have requested an additional1,000 MHzacross various bands to support5Gand improve service quality. High spectrum prices during auctions have indeed strained operators finances, with spectrum acquisition costs exceedingINR 4.4 trillionin 2023. These factors hinder telecom providers from effectively expanding capacity and enhancing network efficiency.

- High Capital Expenditure: The telecom sector in India has seencapital expendituressurpassingINR 2.5 trillionannually due to ongoing needs for network expansion, infrastructure upgrades, and spectrum purchases. As of 2024, major players continue to invest heavily in5G infrastructureand fiber networks. The rapid growth in data demand necessitates continuous investment, placing significant pressure on operators balance sheets. Additionally, projects aimed at improving rural connectivity and compliance with regulatory environmental standards contribute to the financial burden, which can limit profitability for smaller telecom operators.

India Telecom Market Future Outlook

Over the next few years, the India Telecom market is expected to witness substantial growth driven by government initiatives to expand digital connectivity, rising consumer demand for high-speed internet, and the continued rollout of 5G technology. Telecom operators are likely to invest heavily in fiber networks, enhance data center infrastructure, and offer innovative digital services such as OTT platforms, IoT solutions, and AI-powered services, positioning themselves to meet the growing demand for data and advanced telecom solutions.

India Telecom Market Opportunities

- 5G Rollout and Adoption: As of 2024, India has launched commercial 5G services in over 200 cities, with over 40 million subscribers actively using 5G networks. The governments target is to cover the entire country by 2025, driving opportunities for industries such as manufacturing, healthcare, and smart cities. Telecom operators have allocated more than INR 1.5 trillion towards the deployment of 5G infrastructure, with initial results indicating faster internet speeds and low latency. This technological shift opens doors for new revenue streams, including industrial automation, smart devices, and immersive AR/VR experiences.

- Internet of Things (IoT) Deployment: Indias IoT market is expected to grow rapidly, with over 2 billion connected devices by 2025. As of 2024, the country has over 300 million IoT connections, primarily in smart cities, agriculture, and industrial applications. Telecom operators are investing in narrowband IoT (NB-IoT) networks to meet the demand for connected devices, with INR 100 billion earmarked for network expansion. This shift towards IoT adoption offers telecom companies opportunities to offer value-added services, enabling them to diversify revenue streams beyond traditional mobile connectivity.

Scope of the Report

|

Products

Key Target Audience

Telecom Service Providers

Infrastructure Providers

Government and Regulatory Bodies (Telecom Regulatory Authority of India (TRAI), Department of Telecommunications)

Telecom Equipment Manufacturers

Investors and Venture Capital Firms

Mobile Network Operators

Cloud Service Providers

IoT Solution Provider

Time Period Captured in the Report

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Major Players in India Telecom Market

Bharti Airtel

Reliance Jio

Vodafone Idea

Bharat Sanchar Nigam Limited (BSNL)

Tata Communications

Mahanagar Telephone Nigam Limited (MTNL)

Cisco Systems India

Ericsson India

Nokia India

Samsung Electronics

Huawei Technologies India

ZTE Corporation India

Sterlite Technologies

HFCL (Himachal Futuristic Communications Limited)

Tejas Networks

Table of Contents

1. India Telecom Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. India Telecom Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. India Telecom Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Smartphone Penetration

3.1.2. Affordable Data Pricing

3.1.3. Expanding 4G/5G Infrastructure

3.1.4. Government Initiatives (e.g., Digital India, BharatNet)

3.2. Market Challenges

3.2.1. Spectrum Scarcity

3.2.2. High Capital Expenditure

3.2.3. Regulatory Uncertainty

3.2.4. Intense Price Competition

3.3. Opportunities

3.3.1. 5G Rollout and Adoption

3.3.2. Rural Market Expansion

3.3.3. Internet of Things (IoT) Deployment

3.3.4. Cloud Services and Data Centers

3.4. Trends

3.4.1. Increasing OTT (Over-the-Top) Content Consumption

3.4.2. Rise of Digital Payment Platforms

3.4.3. Adoption of AI and Automation in Telecom

3.4.4. Telecom Tower Sharing & Fiber Network Expansion

3.5. Government Regulations

3.5.1. Spectrum Auctions

3.5.2. Net Neutrality Regulations

3.5.3. Telecom Regulatory Authority of India (TRAI) Guidelines

3.5.4. National Digital Communications Policy (NDCP)

3.6. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7. Stakeholder Ecosystem (Service Providers, Infrastructure Providers, Device Manufacturers, Regulatory Bodies)

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape Overview

4. India Telecom Market Segmentation (In Value %)

4.1. By Service Type

4.1.1. Voice Services

4.1.2. Data Services

4.1.3. Mobile Internet

4.1.4. Fixed-line Broadband

4.2. By Subscriber Type

4.2.1. Prepaid Subscribers

4.2.2. Postpaid Subscribers

4.3. By Network Type

4.3.1. 4G/LTE

4.3.2. 5G

4.3.3. Fiber to the Home (FTTH)

4.4. By End-User Industry

4.4.1. Consumer

4.4.2. Enterprise

4.4.3. Government

4.4.4. Small and Medium Enterprises (SMEs)

4.5. By Region

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West India

5. India Telecom Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Bharti Airtel

5.1.2. Reliance Jio

5.1.3. Vodafone Idea

5.1.4. Bharat Sanchar Nigam Limited (BSNL)

5.1.5. Tata Communications

5.1.6. Mahanagar Telephone Nigam Limited (MTNL)

5.1.7. Cisco Systems India

5.1.8. Ericsson India

5.1.9. Nokia India

5.1.10. Samsung Electronics

5.1.11. Huawei Technologies India

5.1.12. ZTE Corporation India

5.1.13. Sterlite Technologies

5.1.14. HFCL (Himachal Futuristic Communications Limited)

5.1.15. Tejas Networks

5.2 Cross Comparison Parameters

(Revenue, ARPU, Subscriber Base, Market Share, Infrastructure Capex, Service Penetration, Spectrum Holding, EBITDA Margins)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. India Telecom Market Regulatory Framework

6.1. Licensing Framework

6.2. Spectrum Allocation Policies

6.3. Tariff and Pricing Regulations

6.4. Interconnection Usage Charges (IUC)

6.5. Quality of Service Regulations

7. India Telecom Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. India Telecom Future Market Segmentation (In Value %)

8.1. By Service Type

8.2. By Subscriber Type

8.3. By Network Type

8.4. By End-User Industry

8.5. By Region

9. India Telecom Market Analyst's Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

This initial step involves mapping out all major stakeholders within the India Telecom Market ecosystem. Comprehensive desk research is carried out using secondary and proprietary databases to define the market's critical variables, such as service types, subscriber trends, and network rollouts.

Step 2: Market Analysis and Construction

In this phase, historical data related to subscriber growth, ARPU, and service penetration are compiled to provide a thorough analysis of the market. This is supplemented with detailed statistics on telecom infrastructure expansion and spectrum allocation to ensure an accurate assessment of market trends.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed based on the collected data and subsequently validated through interviews with industry experts. These consultations provide operational and strategic insights from telecom operators and equipment providers, further refining the analysis.

Step 4: Research Synthesis and Final Output

This step involves synthesizing the findings from primary and secondary research to create a comprehensive market report. Detailed insights on service segmentation, competitive landscape, and future growth prospects are incorporated, ensuring that the report presents a validated and robust market analysis.

Frequently Asked Questions

01. How big is the India Telecom Market?

The India Telecom market is valued at USD 46 billion, primarily driven by increasing data consumption and government-backed digital initiatives.

02. What are the challenges in the India Telecom Market?

Key challenges include spectrum scarcity, high capital expenditure on infrastructure, regulatory uncertainties, and intense price competition among major service providers.

03. Who are the major players in the India Telecom Market?

Prominent players include Bharti Airtel, Reliance Jio, Vodafone Idea, BSNL, and Tata Communications, with strong market presence across urban and rural India.

04. What are the growth drivers for the India Telecom Market?

Growth drivers include the expansion of 4G and 5G infrastructure, increased smartphone penetration, affordable data plans, and government initiatives aimed at improving digital connectivity.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.