India Tractor Market Outlook to 2030

Region:Asia

Author(s):Mukul

Product Code:KROD2616

October 2024

91

About the Report

India Tractor Market Overview

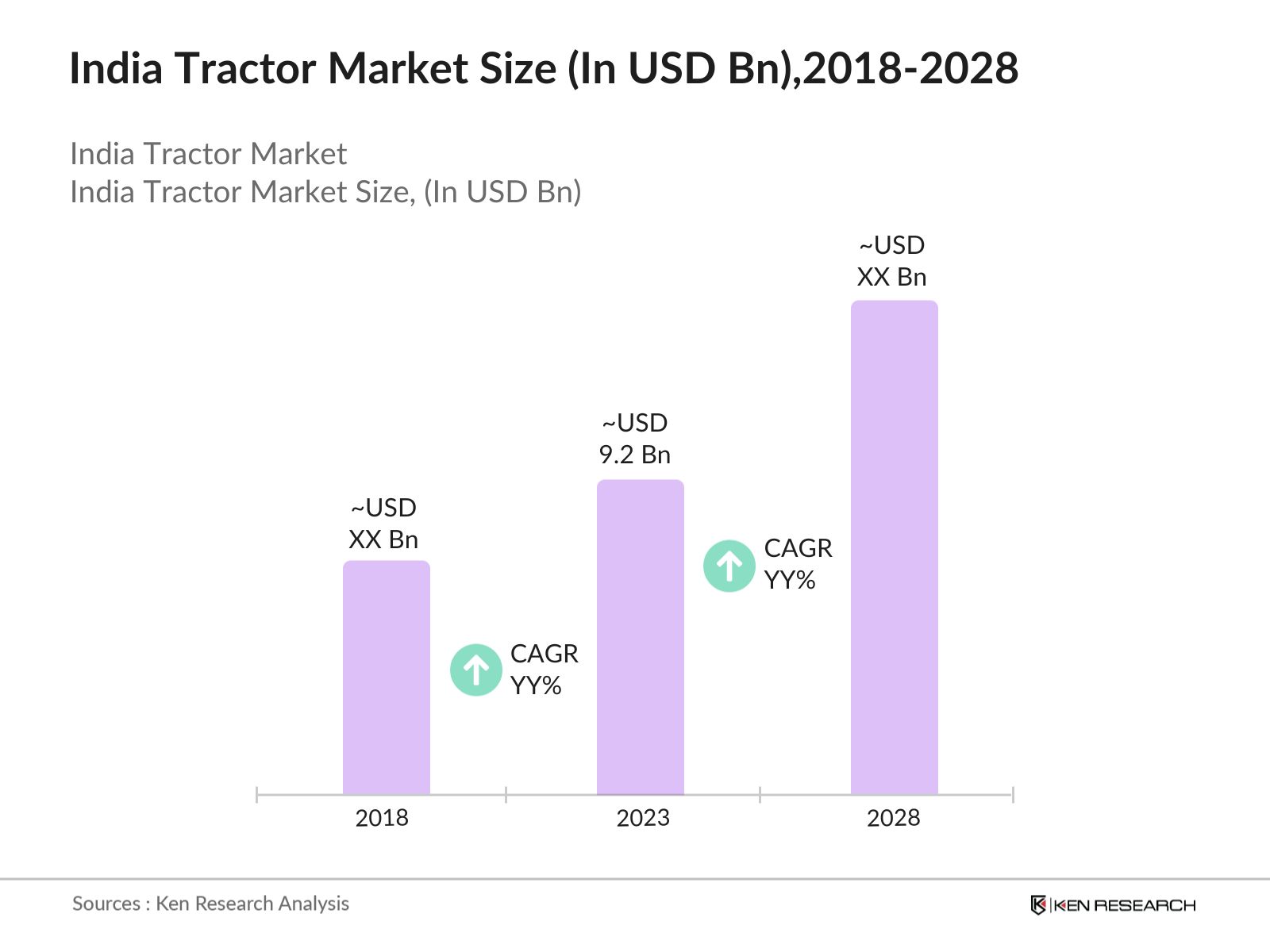

- The India tractor market reached a valuation of USD 9.2 billion in 2023, driven by increasing mechanization in agriculture, rising rural incomes, and government subsidies for farming equipment. The demand for tractors is particularly strong in the Northern and Western regions, where agricultural activities are most intense.

- Key players in the India tractor market include Mahindra & Mahindra, TAFE, Escorts Limited, John Deere, and Sonalika International. These companies dominate the market through extensive distribution networks, continuous innovation, and a strong presence across different price segments catering to small, medium, and large-scale farmers.

- Major tractor-consuming states in India include Punjab, Uttar Pradesh, and Maharashtra. Punjab leads the market with high farm mechanization levels, while Uttar Pradesh has the highest agricultural output. Maharashtra has seen growth due to state-led initiatives supporting farm mechanization.

- In 2023, Mahindra & Mahindra made significant strides in the Indian tractor market by launching a new range of tractors aimed at enhancing farm productivity. The company introduced theOJA, Target, and Naya Swarajtractors, which are designed to meet the diverse

needs of farmers, particularly focusing on affordability and efficiency.

needs of farmers, particularly focusing on affordability and efficiency.

India Tractor Market Segmentation

-

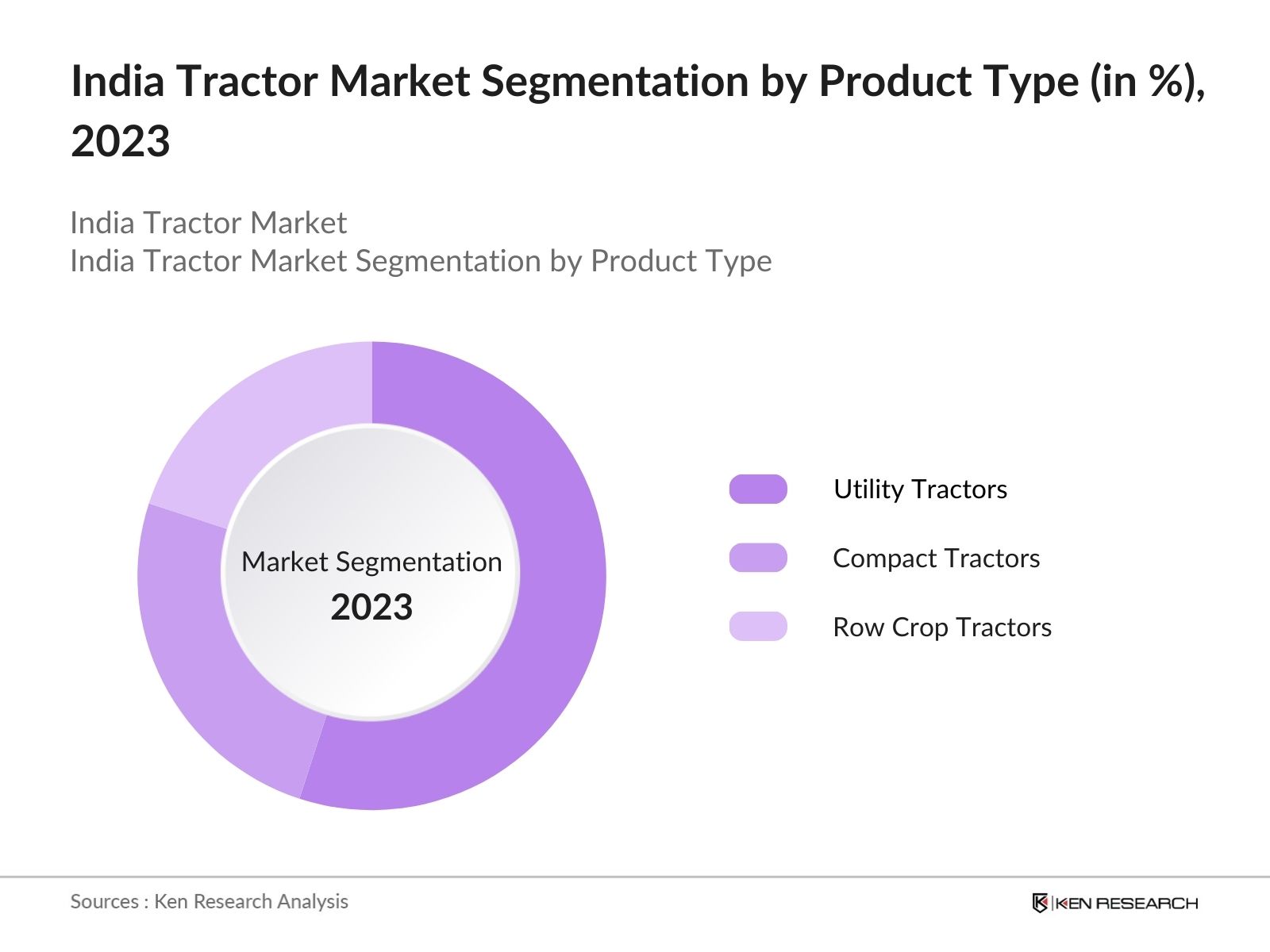

By Product Type: The India tractor market is segmented by product type into compact tractors, utility tractors, and row crop tractors. In 2023, utility tractors dominated the market due to their widespread use in agricultural and non-agricultural tasks such as hauling and plowing. Their versatility and durability make them a preferred choice for farmers across India.

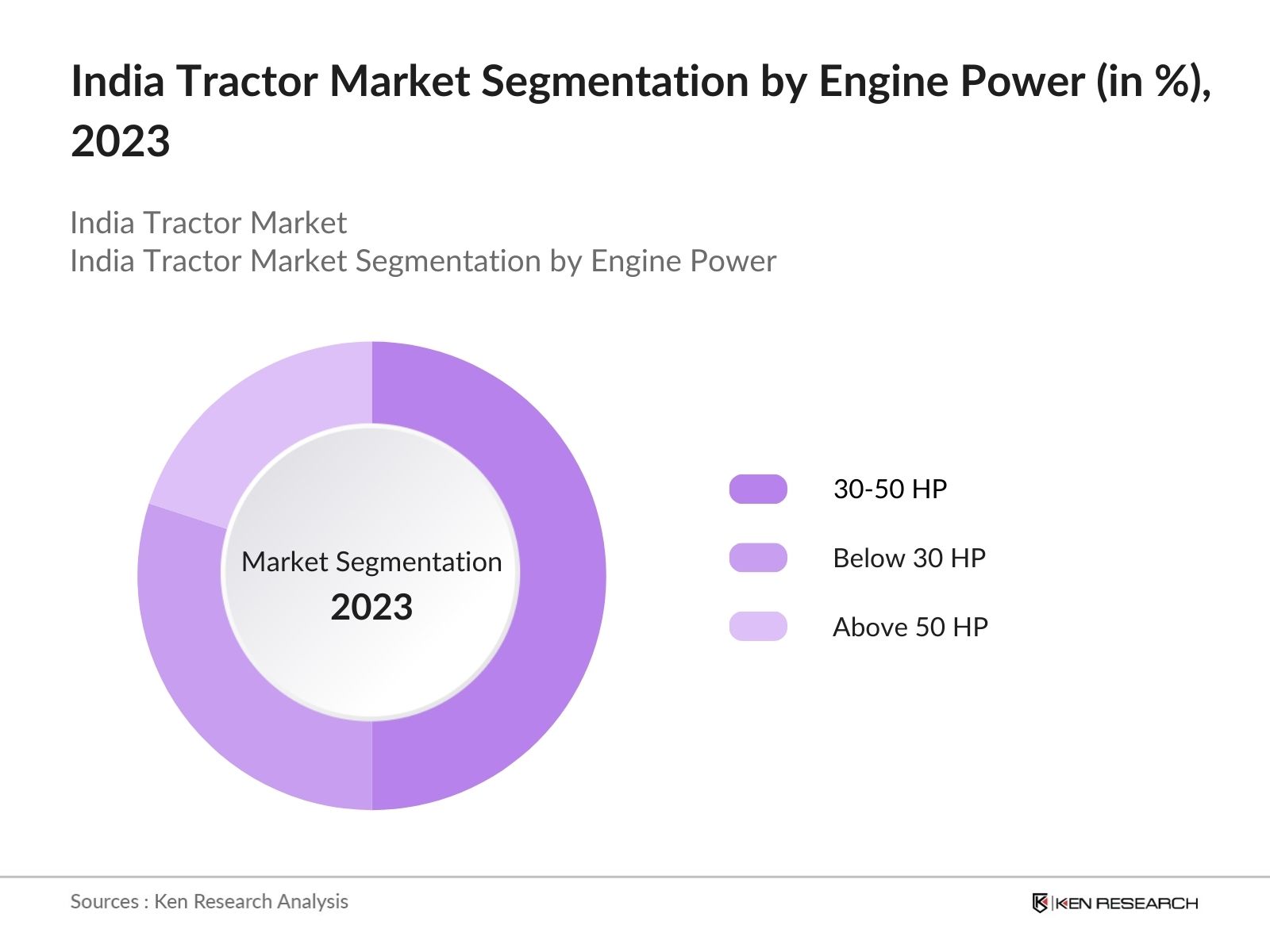

- By Engine Power: The market is segmented by engine power into below 30 HP, 30-50 HP, and above 50 HP. Tractors in the 30-50 HP dominated the market in 2023, driven by the demand from medium-sized farms. These tractors strike a balance between affordability and functionality, making them popular among farmers in various regions.

- By Region: Geographically, the India tractor market is segmented into North, South, East, and West. The Northern region dominated the market in 2023, with states like Punjab, Haryana, and Uttar Pradesh leading tractor sales due to their extensive agricultural activities and government support for mechanization.

India Tractor Market Competitive Landscape

|

Company Name |

Established Year |

Headquarters |

|

Mahindra & Mahindra |

1945 |

Mumbai |

|

TAFE (Tractors and Farm Equipment Ltd.) |

1960 |

Chennai |

|

Escorts Limited |

1944 |

Faridabad |

|

John Deere India |

1998 |

Pune |

|

Sonalika International |

1969 |

Hoshiarpur |

- Escorts Limited: In 2023, Escorts Kubota Limited, formerly known as Escorts Limited, made notable advancements in the Indian tractor market. The company recorded8,587 tractor salesin March 2024, reflecting a16.7% declinecompared to10,305 tractorssold in March 2023. This decrease was attributed to factors such as the shift of the Chaitra Navratri festival to April and erratic monsoon patterns affecting agricultural activities in central and southern regions.

- John Deere India: In 2023, John Deere India made significant advancements in the Indian tractor market, focusing on innovation and technological enhancements to improve farm productivity. The company introduced the5M series tractor, which features higher horsepower and advanced precision technology aimed at reducing farming operational costs and enhancing income levels for farmers.

India Tractor Industry Analysis

India Tractor Market Growth Drivers

- Rising Demand for Mechanization: The need for increased productivity and efficiency in farming practices has led to a growing demand for tractors. InJune 2024, domestic tractor sales reached101,981 units, marking a3.86% increasefrom98,195 unitssold in June 2023.This trend indicates a consistent demand for mechanization in agriculture.

- Positive Agricultural Sentiment: Improved agricultural sentiment due to favorable weather conditions has contributed to the growth of the tractor market. The early arrival of the monsoon in 2024 led to increased Kharif acreage by over30%, positively impacting tractor demand. The overall tractor production in June 2024 was95,010 units, showcasing a robust supply response to the growing demand.

- Technological Advancements: The introduction of advanced tractor models with better fuel efficiency and precision farming technologies has also contributed to market growth.John Deeresold8,023 tractorsin June 2024, marking a4.55% increasefrom7,674 unitssold in June 2023. The focus on innovation is helping farmers adopt more efficient practices, further driving the demand for tractors.

India Tractor Market Challenges

- Fragmented Land Holdings: India's agricultural land is highly fragmented, which limits the use of large-scale machinery like tractors. Many farms are too small to justify the investment in tractors, leading to uneven demand distribution across different regions of the country.

- Inadequate Rural Infrastructure: Poor rural infrastructure remains a challenge for the growth of the tractor market. Inadequate road conditions and lack of connectivity in rural areas make it difficult for farmers to transport produce and machinery, limiting the utility of tractors in certain regions.

India Tractor Market Government Initiatives

- Minimum Support Price (MSP) Revisions: The government periodically revises the Minimum Support Prices for various crops, which helps increase farmers' income and purchasing power. This policy has led to sustained demand for tractors, as farmers are more likely to invest in mechanization when they have guaranteed returns on their crops. For instance, the MSP for Kharif crops was revised in 2023, positively impacting farmer sentiment.

- Public Awareness Campaigns and Demonstration Projects: The government has initiated public awareness campaigns and demonstration projects to educate farmers about the benefits of electric tractors and available incentives. These initiatives allow farmers to experience the advantages of electric technology firsthand, often through subsidized trials. This has been crucial in building confidence in electric tractors among farmers.

India Tractor Market Future Outlook

The India tractor market is expected to witness robust growth over the next five years, driven by increasing agricultural mechanization, rising rural incomes, and government support. By 2028, the market will experience a shift toward more technologically advanced tractors, including electric and AI-powered models.

Future Market Trends

- Adoption of Electric Tractors: Over the next five years, electric tractors will become more prevalent in Indias agricultural landscape. Companies like Mahindra and Escorts are already investing in electric tractor technology, and by 2028, electric models are expected to gain significant market share due to rising environmental concerns and government incentives for sustainable farming.

- Integration of Precision Farming Technologies: Over the next five years, Precision farming technologies, such as GPS-based systems and AI-powered tractors, will become more common by 2028. These technologies will help farmers optimize input costs and increase productivity, making them an essential part of India's agricultural modernization efforts.

Scope of the Report

|

By Product |

Compact Tractors Utility Tractors Row Crop Tractors |

|

By Engine Power |

Below 30 HP 30-50 HP Above 50 HP |

|

By Region |

North South East West |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

Tractor Manufacturers

Government and Regulatory Bodies (Ministry of Agriculture and Farmers' Welfare, NITI Aayog)

Agricultural Cooperatives

Agro-Based Industries

Large Farm Owners

Agricultural Machinery Distributors

Small and Medium Enterprises (SMEs)

Financial Institutions and Banks

Investment and Venture Capitalist Firms

Rural Development Agencies

Time Period Captured in the Report

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report

Mahindra & Mahindra

TAFE (Tractors and Farm Equipment Limited)

Escorts Limited

John Deere

Sonalika International Tractors

New Holland Agriculture

VST Tillers Tractors Ltd

Swaraj Tractors

Preet Tractors

ACE Tractors

Force Motors

Kubota Agricultural Machinery India Pvt. Ltd

Indo Farm Equipment Limited

Captain Tractors

Standard Tractors

Table of Contents

1.India Tractor Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.India Tractor Market Size (in USD Bn), 2018-2023

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.India Tractor Market Analysis

3.1. Growth Drivers

3.1.1. Rising Demand for Mechanization

3.1.2. Positive Agricultural Sentiment

3.1.3. Technological Advancements

3.2. Restraints

3.2.1. High Tractor Costs

3.2.2. Fragmented Land Holdings

3.2.3. Inadequate Rural Infrastructure

3.3. Opportunities

3.3.1. Expansion of Agricultural Credit Facilities

3.3.2. Innovations in Compact Tractors

3.3.3. Electric Tractor Adoption

3.4. Trends

3.4.1. Integration of Precision Farming Technologies

3.4.2. Shift to Sustainable and Electric Tractors

3.4.3. Government Incentives for Mechanization

3.5. Government Regulation

3.5.1. Pradhan Mantri Kisan Tractor Yojana (2021)

3.5.2. Agriculture Infrastructure Fund (2023)

3.5.3. Atma Nirbhar Bharat Abhiyan (2022)

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Competition Ecosystem

4.India Tractor Market Segmentation, 2023

4.1. By Product Type (in Value %)

4.1.1. Compact Tractors

4.1.2. Utility Tractors

4.1.3. Row Crop Tractors

4.2. By Engine Power (in Value %)

4.2.1. Below 30 HP

4.2.2. 30-50 HP

4.2.3. Above 50 HP

4.3. By Region (in Value %)

4.3.1. North India

4.3.2. South India

4.3.3. East India

4.3.4. West India

5.India Tractor Market Cross Comparison

5.1 Detailed Profiles of Major Companies

5.1.1. Mahindra & Mahindra

5.1.2. TAFE (Tractors and Farm Equipment Ltd.)

5.1.3. Escorts Limited

5.1.4. John Deere India

5.1.5. Sonalika International

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6.India Tractor Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7.India Tractor Market Regulatory Framework

7.1. Agricultural Mechanization Policies

7.2. Compliance Requirements

7.3. Certification Processes

8.India Tractor Market Future Size (in USD Bn), 2023-2028

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9.India Tractor Market Future Segmentation, 2028

9.1. By Product Type (in Value %)

9.2. By Engine Power (in Value %)

9.3. By Region (in Value %)

10.India Tractor Market Analysts Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

11.Disclaimer

12.Contact Us

Research Methodology

Step 1: Identifying Key Variables

Ecosystem creation for all major entities within the India Tractor Market by referencing multiple secondary and proprietary databases. This includes desk research to gather detailed information on market dynamics, key players, product types, regional distribution, government initiatives, and technological advancements in the tractor industry.

Step 2: Market Building

Compiling statistics on the India Tractor Market over recent years, focusing on production volumes, sales, and market share data. Data from credible sources such as government reports, agricultural ministries, and trade associations on mechanization rates, infrastructure investments, and market trends are incorporated to compute the revenue generated in the sector.

Step 3: Validating and Finalizing

Building market hypotheses and conducting Computer-Assisted Telephonic Interviews (CATIs) with industry experts, tractor manufacturers, and agricultural sector representatives. This step ensures that gathered data is validated, and market insights are refined, offering a deeper understanding of industry trends and consumer behavior.

Step 4: Research Output

Our team engages with tractor manufacturers, distributors, and government agencies in India to understand supply chain dynamics, market drivers, and recent technological innovations. This bottom-up approach ensures the comprehensive validation of data, providing an accurate and thorough market analysis for the India Tractor Market.

Frequently Asked Questions

1.How big is the India Tractor Market?

The India tractor market was valued at USD 9.2 billion in 2023, fueled by the growing adoption of agricultural mechanization, rising rural incomes, and government subsidies for farming equipment. Demand is especially high in the Northern and Western regions, where agricultural activities are most concentrated.

2.What are the challenges in the India Tractor Market?

Challenges in the India tractor market include high costs of tractors and maintenance, fragmented land holdings, and inadequate rural infrastructure. These factors limit the adoption of tractors, particularly among small-scale farmers and in regions with poor connectivity.

3.Who are the major players in the India Tractor Market?

Key players in the India tractor market include Mahindra & Mahindra, TAFE, Escorts Limited, John Deere, and Sonalika International. These companies dominate through innovation, extensive dealer networks, and a strong presence in rural and semi-urban markets.

4.What are the growth drivers of the India Tractor Market?

The India tractor market is driven by increased agricultural mechanization, government subsidy schemes like the Kisan Credit Card, and rising rural incomes. Financial support programs have made tractors more accessible to small and marginal farmers.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.