India Ventilator Market Outlook to 2030

Region:Asia

Author(s):Vijay Kumar

Product Code:KROD2365

December 2024

95

About the Report

India Ventilator Market Overview

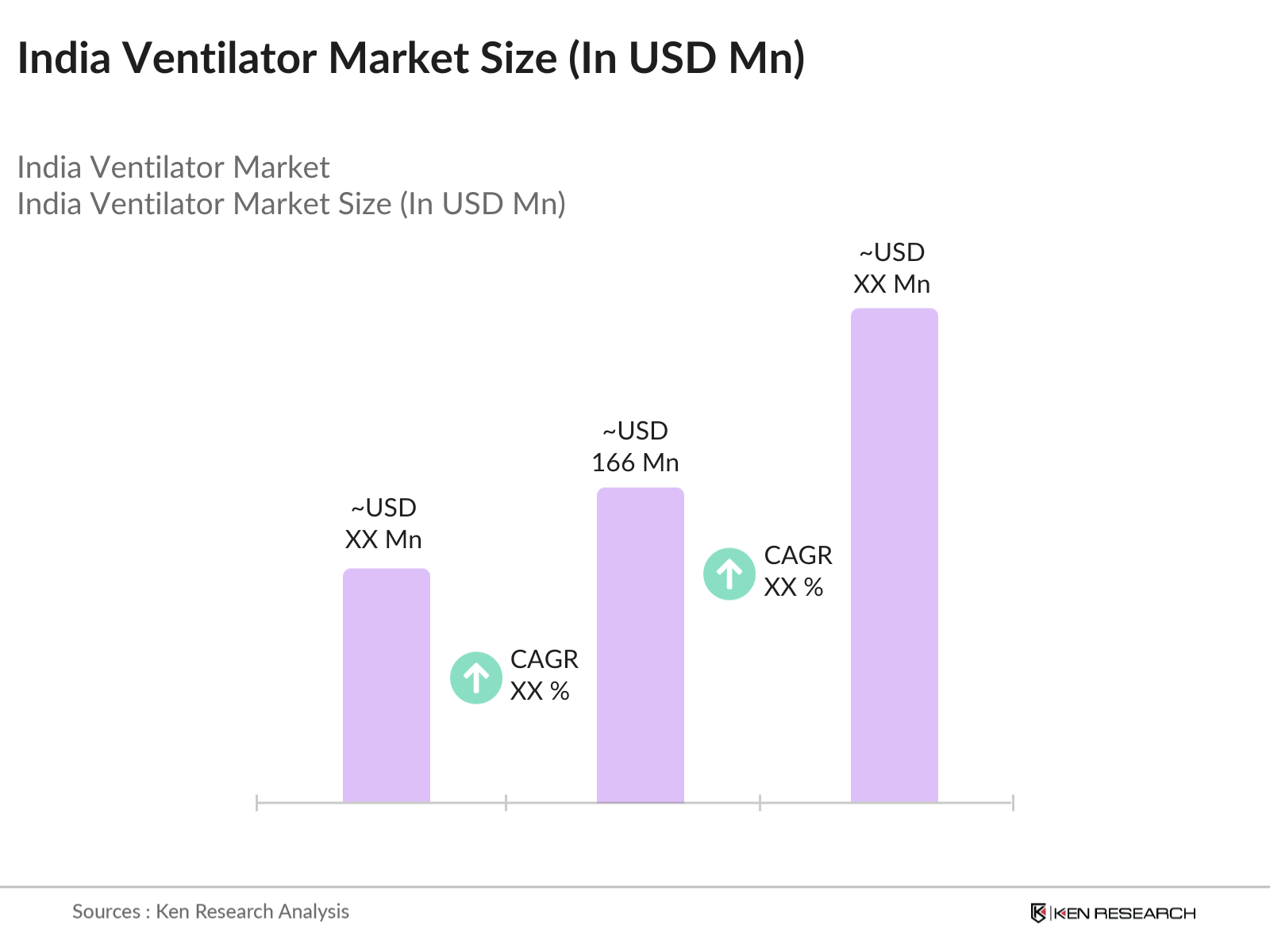

- The India ventilator market reached a valuation of USD 103 million in 2023, primarily driven by the increasing prevalence of respiratory diseases such as COPD and asthma, along with the rising demand for critical care units in hospitals. The market's growth is supported by the expansion of healthcare infrastructure across tier-2 and tier-3 cities and advancements in ventilator technology that cater to the specific needs of the Indian healthcare sector.

- Major players in the market include GE Healthcare, Philips Healthcare, Drgerwerk AG, Smiths Medical, and ResMed. These companies have strengthened their market positions through substantial investments in research and development, strategic collaborations, and a focus on expanding their distribution networks in India. Their commitment to innovation and introduction of advanced ventilators that cater to both hospital and home care settings have enabled them to maintain a competitive edge in the market.

- In 2023, a substantial development in the India ventilator market was the introduction of the advanced portable ventilator by ResMed, which features enhanced connectivity and user-friendly controls. The launch was aimed at meeting the increasing demand for portable and home care ventilators. This development aligns with the trend of remote patient monitoring and care, which has gained traction post-pandemic. The ventilator market is expected to witness further innovations and product launches in 2024 to cater to evolving healthcare needs.

- The Northern region of India dominates the ventilator market, primarily due to the presence of a large number of well-established hospitals and a high concentration of respiratory disease cases. The region's focus on improving healthcare accessibility and enhancing critical care facilities contributes to its leadership position. Government initiatives like the "National Health Infrastructure Mission" are also driving the adoption of ventilators across various healthcare settings.

India Ventilator Market Segmentation

The India Ventilator Market can be segmented based on Product Type, End-User, and Region.

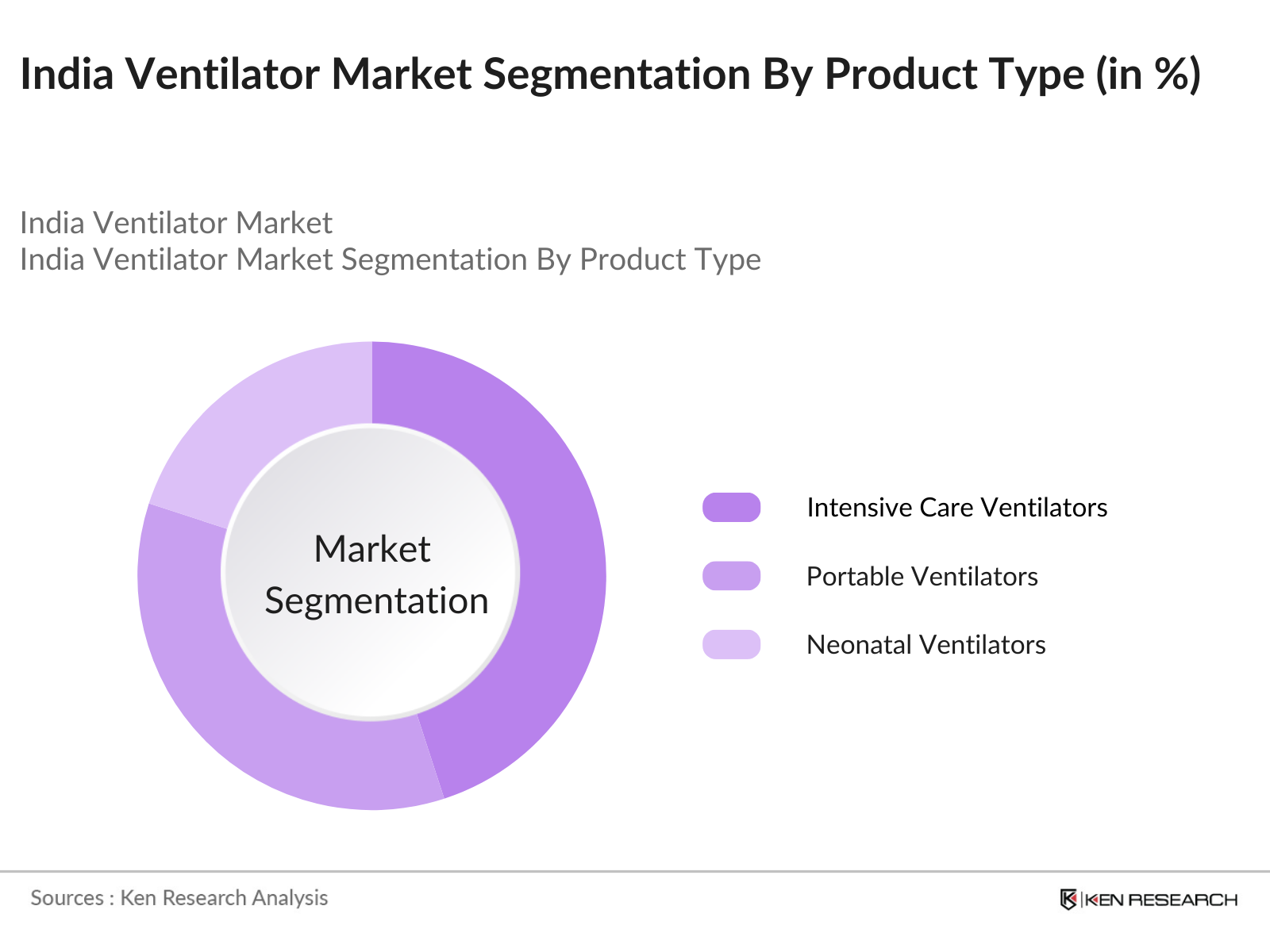

By Product Type: The market is segmented by product type into intensive care ventilators, portable ventilators, and neonatal ventilators. In 2023, intensive care ventilators held the dominant market share due to their widespread use in hospitals for managing severe respiratory conditions.

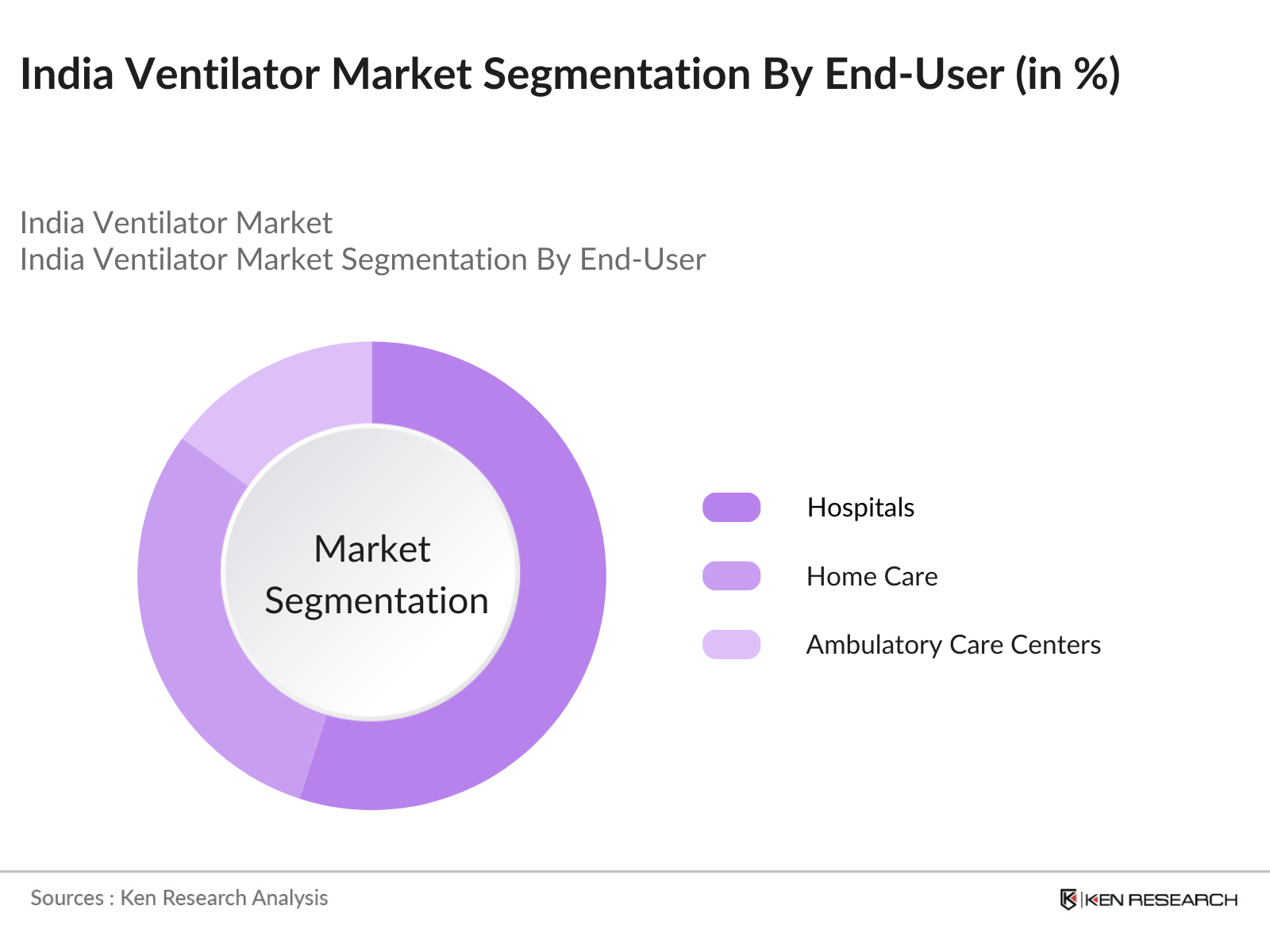

By End-User: The market is further segmented by end-user into hospitals, home care, and ambulatory care centers. The hospital segment accounted for the largest market share in 2023, driven by the high demand for ventilators in critical care settings. Hospitals remain the primary providers of acute respiratory care, with a growing focus on upgrading ICU facilities to enhance patient outcomes.

By Region: Geographically, the market is segmented into North, South, East, and West India. The Northern region dominated the market in 2023, driven by the high concentration of key healthcare providers and advanced medical research centers.

India Ventilator Market Competitive Landscape

|

Company Name |

Headquarters |

Establishment Year |

|

GE Healthcare |

Chicago, USA |

1892 |

|

Philips Healthcare |

Amsterdam, Netherlands |

1891 |

|

Drgerwerk AG |

Lbeck, Germany |

1889 |

|

Smiths Medical |

London, UK |

1940 |

|

ResMed |

San Diego, USA |

1989 |

- GE Healthcare: In 2023, GE Healthcare announced a significant expansion in its ventilator manufacturing capabilities in India, aiming to produce 20,000 ventilators annually by 2024. This move is part of their strategy to cater to the increasing demand in the Asian market, particularly in India, where the healthcare infrastructure is rapidly evolving. The company also introduced a new range of ventilators featuring advanced monitoring systems to enhance patient care.

- Philips Healthcare: In 2024, Philips Healthcare set up a new R&D center in Pune, Maharashtra, focusing on innovation in healthcare technologies, including ventilators. The facility is designed to house 1,900 employees and underscores Philips' dedication to developing advanced healthcare solutions tailored to the Indian market and expanding its global reach.

India Ventilator Market Analysis

Market Growth Drivers

- Rising Incidence of Respiratory Diseases: In 2024, the prevalence of respiratory diseases like Chronic Obstructive Pulmonary Disease (COPD) and asthma in India continues to drive the demand for ventilators. According to the Ministry of Health and Family Welfare, COPD affected over 65 million people in India, leading to an increased requirement for respiratory support in hospitals and home care settings. Additionally, the increase in air pollution levels, particularly in urban areas, has exacerbated respiratory conditions, thereby boosting the need for ventilators in both public and private healthcare facilities.

- Expansion of Healthcare Infrastructure: The Government of India's ongoing efforts to improve healthcare infrastructure are a significant growth driver for the ventilator market. The "Ayushman Bharat Pradhan Mantri Jan Arogya Yojana" (AB-PMJAY) initiative aims to enhance healthcare accessibility across the country, with a specific focus on tier-2 and tier-3 cities. By 2024, the government had allocated INR 64,000 crore for the development of hospitals and clinics under this program, which directly correlates with the increased procurement of ventilators to equip these facilities adequately.

- Increasing Geriatric Population: India's aging population is another critical driver for the ventilator market. As of 2024, over 138 million people in India are aged 60 and above, according to the National Statistical Office (NSO). This demographic shift is leading to a higher prevalence of age-related respiratory illnesses, thus increasing the demand for advanced ventilatory support systems. Hospitals and home care settings are expanding their capacities to cater to the needs of elderly patients, necessitating the procurement of more ventilators.

India Ventilator Market Challenges

- High Cost of Advanced Ventilators: One of the primary challenges facing the India ventilator market is the high cost associated with advanced ventilators. These devices, which are crucial for critical care, can range from INR 5 lakh to INR 15 lakh per unit. The high price makes it difficult for smaller hospitals, especially in rural areas, to afford these essential devices. Despite government subsidies, many healthcare providers struggle to meet the cost, hindering the overall market growth.

- Shortage of Trained Healthcare Professionals: Another significant challenge in the India ventilator market is the shortage of trained healthcare professionals to operate and maintain ventilators. The Ministry of Health and Family Welfare reported in 2024 that there is a deficit of nearly 1.5 million healthcare professionals, including doctors and nurses, proficient in using advanced medical devices like ventilators. This shortage impedes the optimal utilization of ventilators, particularly in rural and semi-urban areas, where training facilities and skilled manpower are limited.

India Ventilator Market Government Initiatives

- Pradhan Mantri Bhartiya Janaushadhi Pariyojana (PMBJP): The Indian government launched the Pradhan Mantri Bhartiya Janaushadhi Pariyojana (PMBJP) to provide affordable and quality generic medicines and medical devices, including ventilators. By 2024, over 8,000 PMBJP centers had been established across the country, supplying affordable ventilators to government hospitals and clinics. This initiative aims to make essential medical equipment accessible to underserved areas, thus supporting the expansion of the ventilator market in India.

- Production Linked Incentive (PLI) Scheme for Medical Devices: In 2024, the Government of India continued its focus on boosting domestic manufacturing through the Production Linked Incentive (PLI) scheme for medical devices. Under this scheme, an allocation of INR 3,420 crore was made to encourage the local production of critical medical devices, including ventilators. The PLI scheme aims to reduce dependency on imports, enhance domestic capabilities, and ensure a steady supply of ventilators, especially during health crises.

India Ventilator Market Future Outlook

The India ventilator market is poised for significant growth, driven by advancements in technology, increased demand in emerging regions, and a stronger focus on healthcare infrastructure and accessibility.

Future Market Trends

- Market Outlook 2028 Driven by Digital Health Integration: By 2028, the India ventilator market is expected to be significantly influenced by the integration of digital health technologies. The adoption of telemedicine and AI-driven ventilator monitoring systems will become more prevalent, enabling remote management and personalized patient care. As healthcare providers increasingly embrace digital solutions, the demand for smart ventilators with advanced connectivity and data analytics features will likely surge, driving market growth.

- Growth in Demand for Home-Based Ventilator Solutions: Over the next five years, the demand for home-based ventilator solutions is anticipated to grow substantially. With an increasing number of patients opting for home care and the aging population requiring long-term respiratory support, manufacturers are expected to focus on developing portable, user-friendly ventilators. The expansion of home healthcare services and government incentives for home-based treatments will further boost this segment, contributing to the overall growth of the ventilator market in India.

Scope of the Report

|

By Product |

Intensive Care Ventilators Portable Ventilators Neonatal Ventilators |

|

By End-User |

Hospitals Home Care Ambulatory Care Centers |

|

By Region |

North South East West |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Hospitals and Healthcare Providers

Medical Device Distributors

Government and Regulatory Bodies (e.g., Ministry of Health and Family Welfare)

Investments and Venture Capitalist Firms

Home Healthcare Service Providers

Emergency Medical Services

Time Period Captured in the Report

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

GE Healthcare

Philips Healthcare

Drgerwerk AG

Smiths Medical

ResMed

Hamilton Medical

Medtronic

BPL Medical Technologies

Mindray Medical International Limited

Fisher & Paykel Healthcare

Table of Contents

1. India Ventilator Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. India Ventilator Market Size (in INR Crore), 2018-2023

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. India Ventilator Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Prevalence of Respiratory Diseases

3.1.2. Expansion of Healthcare Infrastructure

3.1.3. Rising Geriatric Population

3.2. Restraints

3.2.1. High Cost of Advanced Ventilators

3.2.2. Shortage of Trained Healthcare Professionals

3.2.3. Import Dependency for Ventilator Components

3.3. Opportunities

3.3.1. Government Initiatives to Boost Healthcare

3.3.2. Advances in Ventilator Technology

3.3.3. Expansion in Home Healthcare Segment

3.4. Trends

3.4.1. Shift Towards Portable and Home Care Ventilators

3.4.2. Integration of AI and IoT in Ventilator Systems

3.4.3. Focus on Energy-Efficient Ventilators

3.5. Government Regulation

3.5.1. Pradhan Mantri Bhartiya Janaushadhi Pariyojana (PMBJP)

3.5.2. Production Linked Incentive (PLI) Scheme for Medical Devices

3.5.3. National Health Digital Mission (NHDM)

3.5.4. Compliance with Medical Device Regulations

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Competition Ecosystem

4. India Ventilator Market Segmentation, 2023

4.1. By Product Type (in Value %)

4.1.1. Intensive Care Ventilators

4.1.2. Portable Ventilators

4.1.3. Neonatal Ventilators

4.2. By End-User (in Value %)

4.2.1. Hospitals

4.2.2. Home Care

4.2.3. Ambulatory Care Centers

4.3. By Region (in Value %)

4.3.1. North India

4.3.2. South India

4.3.3. East India

4.3.4. West India

5. India Ventilator Market Cross Comparison

5.1. Detailed Profiles of Major Companies

5.1.1. GE Healthcare

5.1.2. Philips Healthcare

5.1.3. Drgerwerk AG

5.1.4. Smiths Medical

5.1.5. ResMed

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6. India Ventilator Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7. India Ventilator Market Regulatory Framework

7.1. Compliance Requirements for Medical Devices

7.2. Certification Processes

7.3. Data Protection and Cybersecurity Regulations

8. India Ventilator Future Market Size (in INR Crore), 2023-2028

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9. India Ventilator Future Market Segmentation, 2028

9.1. By Product Type (in Value %)

9.2. By End-User (in Value %)

9.3. By Region (in Value %)

10. India Ventilator Market Analysts Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identifying Key Variables

Creating an ecosystem for all major entities within the India Ventilator Market and referencing a combination of secondary and proprietary databases to conduct desk research. This step involves gathering industry-level information, identifying market trends, and understanding the competitive landscape to ensure a comprehensive analysis.

Step 2: Market Building

Collating statistics on the India Ventilator Market over the years, analyzing market penetration across various segments, and evaluating the performance of key market players. This includes reviewing production capacities, market shares, and sales data to accurately compute the revenue generated within the Indian ventilator market. Quality checks are conducted to ensure the accuracy and reliability of the data points shared.

Step 3: Validating and Finalizing

Developing market hypotheses and conducting Computer Assisted Telephone Interviews (CATIs) with industry experts and stakeholders from leading companies in the ventilator market. These interviews are crucial for validating the collected data, refining market forecasts, and obtaining operational and financial insights directly from industry representatives.

Step 4: Research Output

Engaging with multiple key players in the ventilator industry to understand the dynamics of product segments, customer needs, sales patterns, and market challenges. This step involves using a bottom-up approach to validate the data, ensuring that the final statistics and insights accurately reflect market conditions and support strategic decision-making.

Frequently Asked Questions

1. How big is the India Ventilator Market?

The India ventilator market reached a valuation of USD 103 million in 2023, primarily driven by the increasing prevalence of respiratory diseases such as COPD and asthma, along with the rising demand for critical care units in hospitals.

2. What are the challenges in the India Ventilator Market?

Challenges in the India ventilator market include the high cost of advanced ventilators, a shortage of trained healthcare professionals, and a heavy reliance on imported components, which can limit market growth and accessibility.

3. Who are the major players in the India Ventilator Market?

Key players in the India ventilator market include GE Healthcare, Philips Healthcare, Drgerwerk AG, Smiths Medical, and ResMed. These companies lead the market due to their innovative product offerings and strong distribution networks.

4. What are the growth drivers of the India Ventilator Market?

The market is driven by the increasing prevalence of respiratory diseases, expansion of healthcare infrastructure, and the rising geriatric population, contributing to the growing demand for ventilators in hospitals and home care settings.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.