India Virtual Reality Market Outlook to 2030

Region:India

Author(s):Shambhavi

Product Code:KROD3156

Region:India

Author(s):Shambhavi

Product Code:KROD3156

November 2024

89

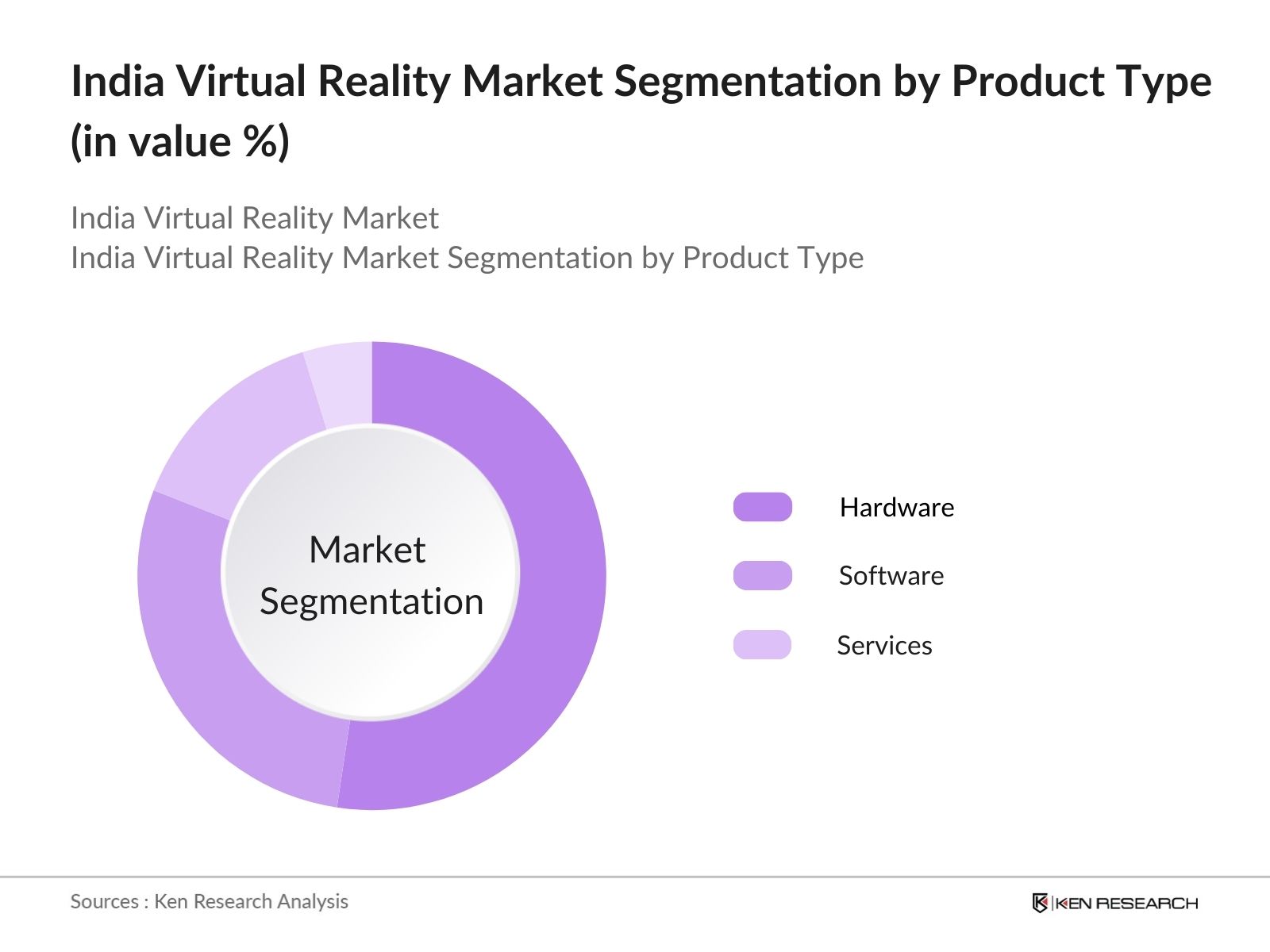

By Product Type: The India Virtual Reality market is segmented by product type into hardware, software, and services. Among these, hardware dominates the market due to the high demand for VR headsets and motion controllers in the gaming and enterprise sectors. The proliferation of standalone VR devices, which offer immersive experiences without requiring a PC, has further boosted hardware demand. Companies like Meta and HTC are leading the hardware sub-segment with their affordable and cutting-edge VR headsets that cater to both consumers and businesses.

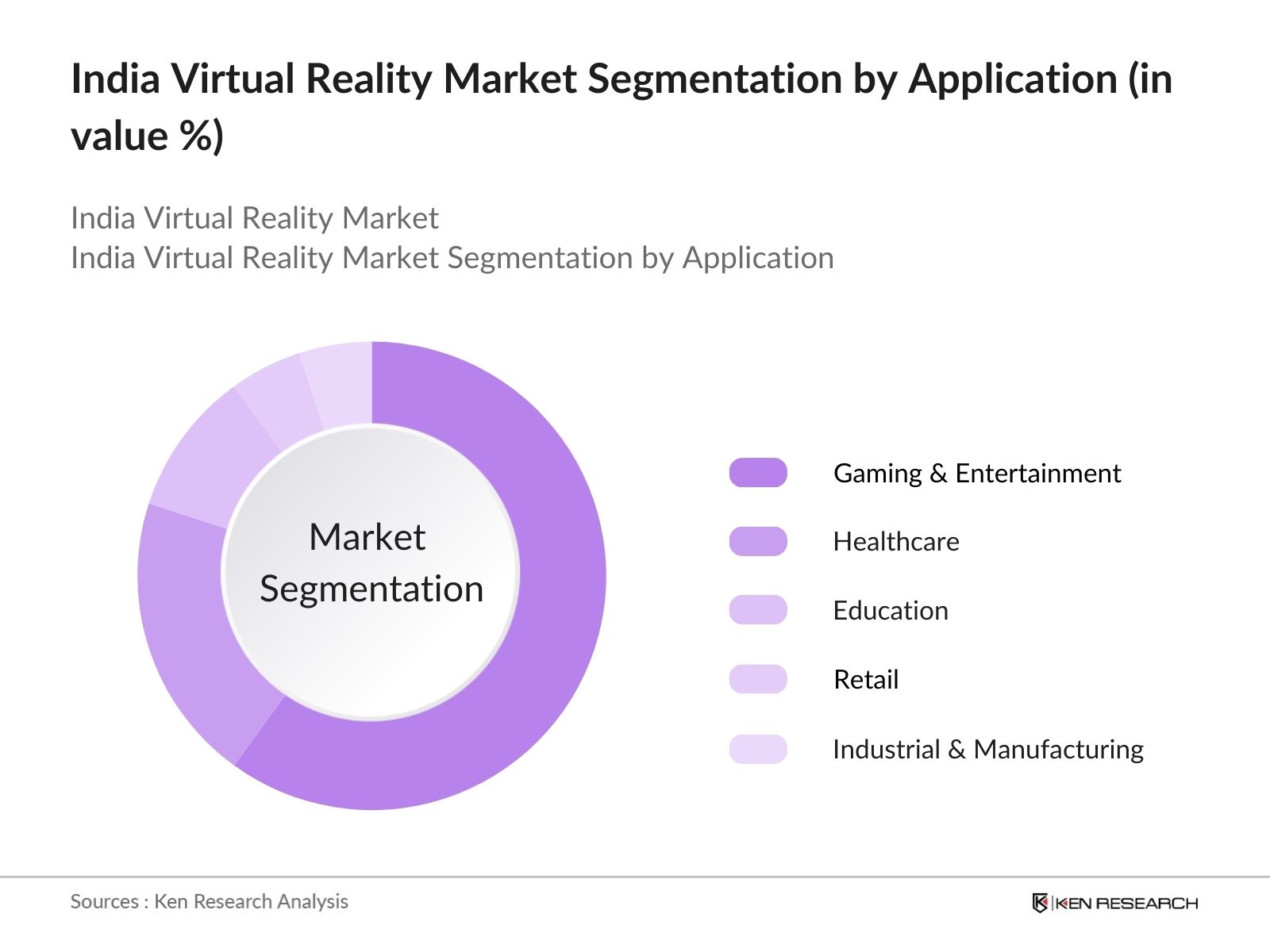

By Application: The market is also segmented by application into gaming and entertainment, healthcare, and education. The gaming and entertainment sector leads the market, driven by the increasing demand for immersive gaming experiences. India's large youth population, coupled with the rise of mobile gaming and the popularity of VR arcades, further supports this segment. Developers are creating VR content tailored for Indian gamers, which enhances local engagement and drives market growth.

The India VR market is characterized by the presence of both global and local players. The competitive landscape is highly consolidated, with key companies dominating due to their strong brand presence, extensive R&D investments, and robust product portfolios. These companies are leveraging partnerships and collaborations to enhance their market position. Global leaders such as Meta and HTC are establishing strong footholds in the Indian market through localized strategies, while domestic firms are focusing on affordable VR solutions tailored to local demand.

|

Company |

Establishment Year |

Headquarters |

Revenue |

Market Share |

Key VR Products |

R&D Expenditure |

Strategic Partnerships |

|

Meta (Facebook Reality Labs) |

2004 |

Menlo Park, CA |

|||||

|

HTC Corporation |

1997 |

Taipei, Taiwan |

|||||

|

Sony Interactive Entertainment |

1993 |

Tokyo, Japan |

|||||

|

Google (Alphabet Inc.) |

1998 |

Mountain View, CA |

|||||

|

Samsung Electronics |

1969 |

Suwon, South Korea |

Growth Drivers

Market Challenges

Over the next five years, the India Virtual Reality market is expected to experience significant growth, driven by technological advancements in VR devices, the expansion of 5G networks, and increasing applications across multiple industries. Government initiatives such as Digital India and the development of smart cities will create favorable conditions for VR adoption in sectors like education, healthcare, and entertainment. The rising demand for immersive experiences and the continued evolution of affordable hardware will further drive market growth.

Market Opportunities

|

By Product Type |

Hardware Software Services |

|

By Application |

Gaming & Entertainment Education Healthcare Retail Industrial & Manufacturing |

|

By End-User |

Individual Consumers Enterprises Government & Defense |

|

By Component |

Headsets Motion Controllers Software Accessories |

|

By Region |

North India South India East India West India |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Advancements in VR Technology (Immersive Display, Motion Tracking)

3.1.2. Increased Adoption in Gaming & Entertainment (Gaming, AR/VR Content Creation)

3.1.3. Government Support for Digital India (Policy Incentives, Digital Ecosystem)

3.1.4. Growth in Enterprise Adoption (Corporate Training, Remote Collaboration)

3.2. Market Challenges

3.2.1. High Cost of VR Hardware (Headsets, Sensors)

3.2.2. Limited Content Availability (Localized Content, VR Content Creation)

3.2.3. Low Consumer Awareness and Accessibility (Penetration in Tier-2/3 Cities)

3.3. Opportunities

3.3.1. Expanding VR Applications in Healthcare (Surgery Simulation, Therapy)

3.3.2. Integration with 5G Technology (Low Latency Streaming, Immersive Experiences)

3.3.3. Growth of E-Commerce and Retail (Virtual Shopping, VR Showrooms)

3.4. Trends

3.4.1. Rising Demand for Social VR Platforms (Virtual Events, Collaborative Spaces)

3.4.2. Development of Lightweight and Affordable VR Devices (Standalone Headsets)

3.4.3. Increasing Adoption in Education (Virtual Classrooms, Immersive Learning)

3.5. Government Regulation

3.5.1. Digital India Initiative (Digital Infrastructure, Innovation Hubs)

3.5.2. Policy Support for AR/VR Startups (Incubation Programs, Tax Benefits)

3.5.3. Easing Import Restrictions on VR Hardware (Customs Policies, Incentives)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Hardware (Headsets, Controllers, Sensors)

4.1.2. Software (VR Platforms, Development Tools, Content)

4.1.3. Services (Consultation, Integration, Training)

4.2. By Application (In Value %)

4.2.1. Gaming & Entertainment

4.2.2. Education

4.2.3. Healthcare

4.2.4. Retail

4.2.5. Industrial & Manufacturing

4.3. By End-User (In Value %)

4.3.1. Individual Consumers

4.3.2. Enterprises (Corporate, SMEs, Startups)

4.3.3. Government & Defense

4.4. By Component (In Value %)

4.4.1. Headsets

4.4.2. Motion Controllers

4.4.3. Software and Apps

4.4.4. Accessories (Sensors, Gloves)

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West India

5.1 Detailed Profiles of Major Competitors

5.1.1. Facebook Reality Labs (Meta)

5.1.2. HTC Corporation

5.1.3. Sony Interactive Entertainment

5.1.4. Google (Alphabet Inc.)

5.1.5. Samsung Electronics

5.1.6. Microsoft Corporation

5.1.7. Valve Corporation

5.1.8. Oculus (Meta Platforms)

5.1.9. Magic Leap Inc.

5.1.10. Lenovo Group

5.1.11. Immersion Corporation

5.1.12. HP Development Company

5.1.13. Qualcomm Technologies

5.1.14. NVIDIA Corporation

5.1.15. Unity Technologies

5.2 Cross Comparison Parameters (Product Portfolio, Revenue, R&D Investments, Global Presence, VR Market Share, Partnerships, Technological Capabilities, Customer Base)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Digital Infrastructure Standards

6.2. Data Privacy and Security Regulations

6.3. Import/Export Regulations for VR Hardware

6.4. Licensing and Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-User (In Value %)

8.4. By Component (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Segmentation and Persona Analysis

9.3. Market Entry Strategies

9.4. White Space Opportunity Analysis

The initial phase involves mapping the ecosystem of stakeholders in the India Virtual Reality market. This process includes desk research to identify key market variables such as product adoption rates, industry penetration, and growth drivers using proprietary databases and government reports.

In this phase, we gather and analyze historical market data to understand the trends and developments within the India Virtual Reality market. This includes evaluating the ratio of hardware sales to software deployment and the resultant revenue generation across different sectors.

Hypotheses around market dynamics are validated through interviews with industry professionals, using CATIS techniques to gather qualitative insights. These interviews help refine data accuracy and provide operational perspectives on VR usage in India.

In this final phase, data from various market stakeholders is synthesized to create a detailed and validated market report. This process includes interviews with key players in the VR space and cross-referencing findings with market trends, consumer preferences, and technological innovations.

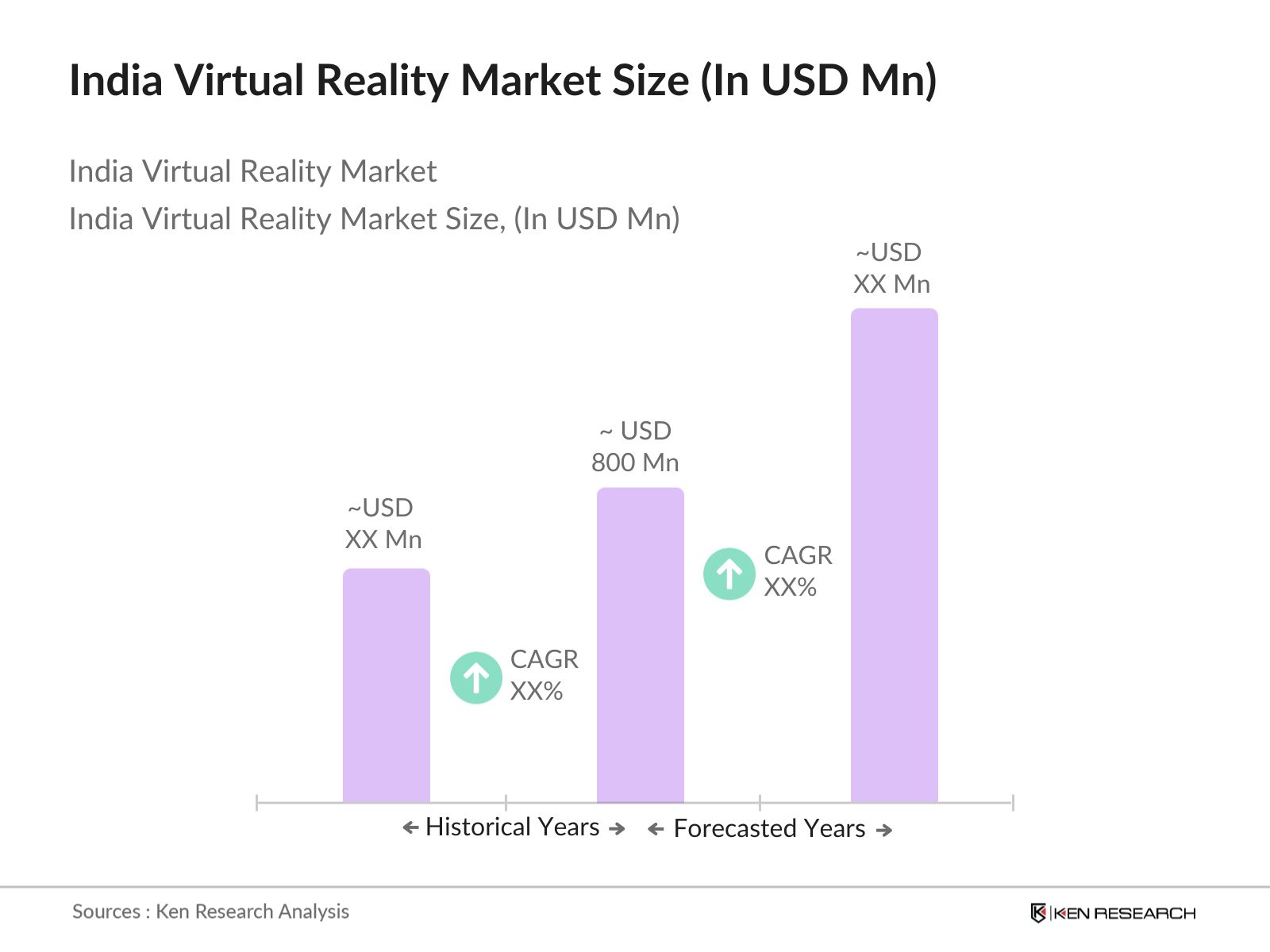

The India Virtual Reality market is valued at USD 800 million, driven by advancements in hardware and software, as well as growing demand from the gaming, healthcare, and education sectors.

Challenges in the India Virtual Reality market include the high cost of VR hardware, limited availability of localized content, and low consumer awareness in rural areas.

Key players in the India Virtual Reality market include Meta, HTC Corporation, Sony Interactive Entertainment, Google, and Samsung Electronics, driven by their advanced product portfolios and strong brand presence.

Growth in the India Virtual Reality market is propelled by technological advancements in VR devices, government support for digital infrastructure, and rising consumer demand for immersive experiences across various sectors.

South India, particularly cities like Bangalore and Hyderabad, dominate the market due to their strong tech ecosystems, R&D centers, and favorable government policies supporting innovation and technology adoption.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.