India Waste To Energy Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD4440

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD4440

October 2024

83

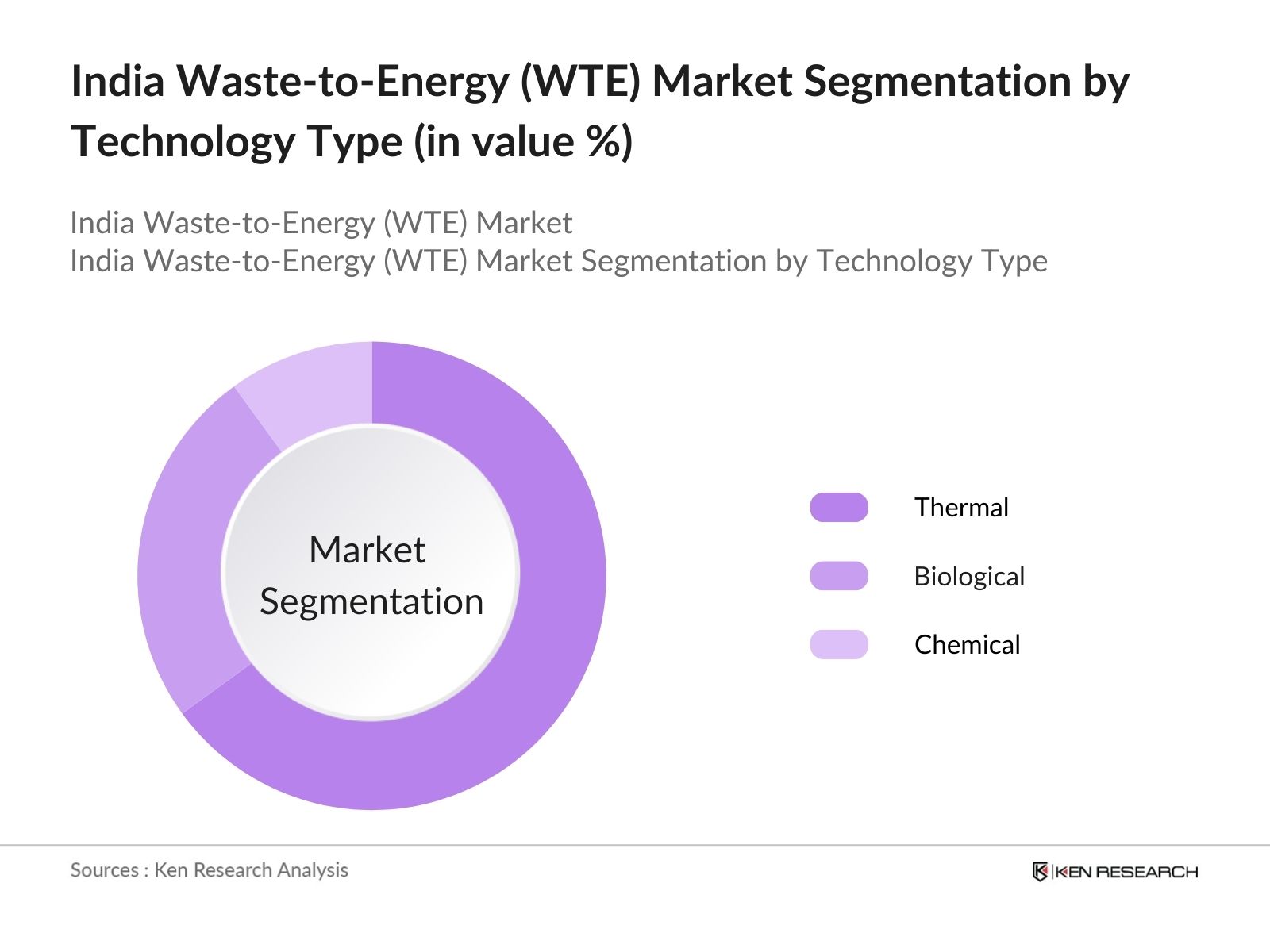

By Technology Type: The market is segmented by technology type into Thermal, Biological, and Chemical. The Thermal segment has dominated market share under the technology type segmentation. This is because thermal technologies like incineration and gasification are well-established, highly efficient, and capable of handling the large volume of waste generated in urban areas. These methods are preferred due to their ability to convert waste directly into energy, offering a high recovery rate of energy from waste materials.

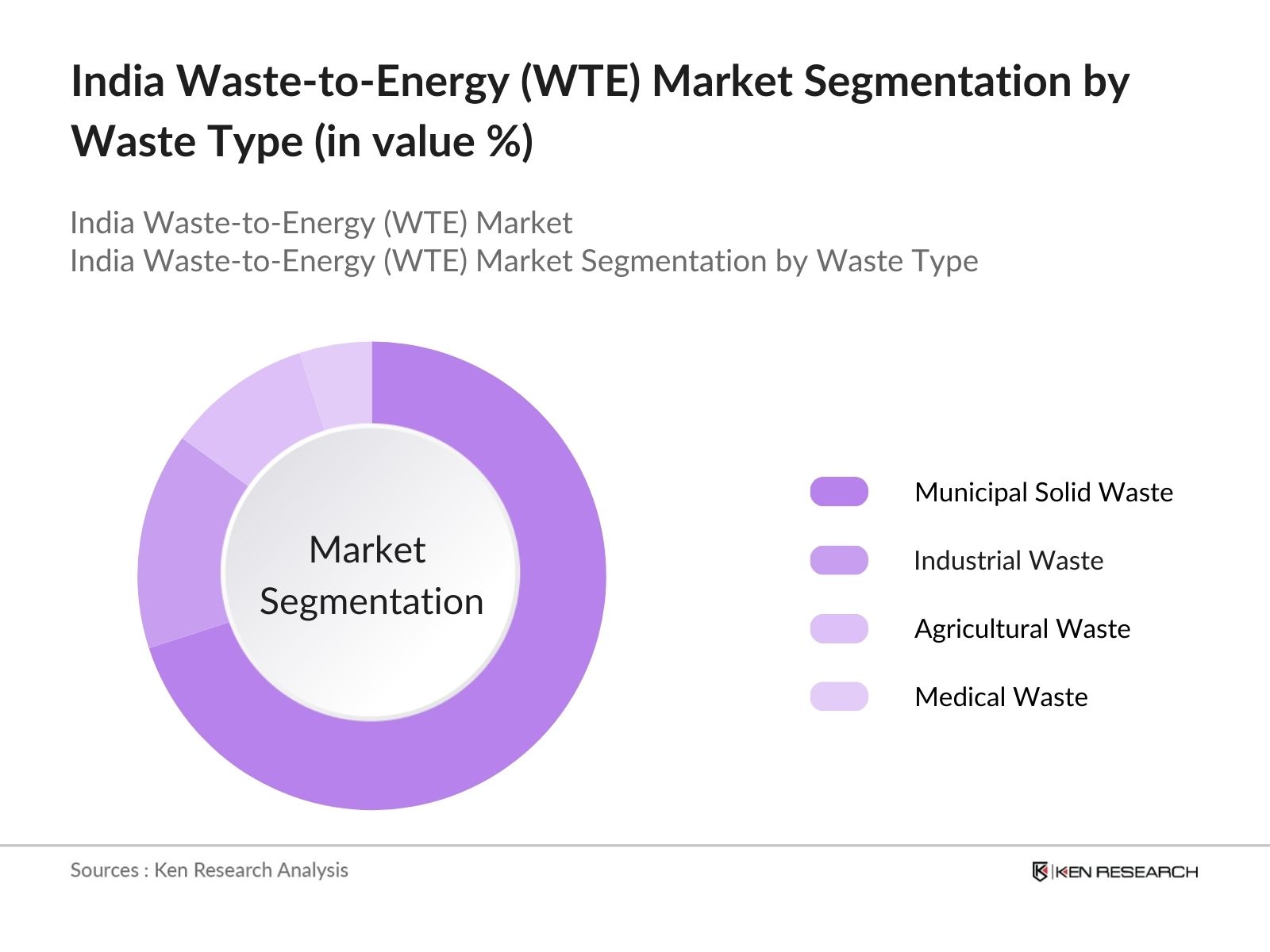

By Waste Type: The market is segmented by waste type into Municipal Solid Waste (MSW), Industrial Waste, Agricultural Waste, and Medical Waste. Municipal Solid Waste (MSW) holds the largest market share in this category. This dominance is driven by the massive volume of household and urban waste generated in Indias metropolitan regions. Government regulations requiring municipalities to handle waste more sustainably and the increasing reliance on WTE plants to manage this waste have made MSW the leading segment in this market.

The market is dominated by several key players, including domestic and international companies. The market is highly competitive due to government tenders and private sector investments, as companies vie to establish large-scale WTE projects across the country. Leading firms have leveraged technological innovations and strategic partnerships to strengthen their positions.

|

Company |

Year of Establishment |

Headquarters |

Installed Capacity (MW) |

Projects Completed |

Technology Type |

Revenue (USD Mn) |

Employees |

Market Share (%) |

|

Ramky Enviro Engineers Ltd. |

1994 |

Hyderabad, India |

||||||

|

Jindal Urban Waste Mgmt |

1997 |

New Delhi, India |

||||||

|

Hitachi Zosen India |

1982 |

Bengaluru, India |

||||||

|

Essel Infraprojects Ltd. |

1997 |

Mumbai, India |

||||||

|

Veolia India |

2000 |

Mumbai, India |

Over the next five years, the India Waste-to-Energy (WTE) industry is expected to witness growth driven by the increasing generation of municipal waste, technological advancements in waste conversion processes, and strong government backing for renewable energy projects. The National Clean Energy Mission and other waste management programs are expected to boost the WTE market as the country seeks to tackle urban waste while addressing energy deficits.

|

Technology Type |

Thermal Biological Chemical |

|

Application |

Power Generation Heat Generation Fuel Conversion |

|

Waste Type |

Municipal Solid Waste Industrial Waste Agricultural Waste Medical Waste |

|

End-User |

Urban Municipalities Industrial Facilities Agriculture Sector |

|

Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy (Technology Type, Application, Waste Type)

1.3. Market Growth Rate (CAGR)

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis (Capacity Installed, Power Generation)

2.3. Key Market Developments and Milestones (Projects, Investments)

3.1. Growth Drivers

3.1.1. Urban Waste Generation

3.1.2. Government Regulations and Initiatives

3.1.3. Environmental Sustainability Goals

3.1.4. Power Deficit Management

3.2. Market Challenges

3.2.1. High Capital Investment

3.2.2. Operational Efficiency Issues

3.2.3. Public Acceptance and Environmental Concerns

3.3. Opportunities

3.3.1. Expansion in Tier 2 & Tier 3 Cities

3.3.2. Technological Advancements in Conversion Efficiency

3.3.3. Circular Economy Integration

3.4. Trends

3.4.1. Adoption of Plasma Gasification Technology

3.4.2. Hybrid Renewable Energy Solutions

3.4.3. Rise of Public-Private Partnerships (PPP)

3.5. Government Regulation

3.5.1. Waste Management Rules (Solid Waste Management, Hazardous Waste Management)

3.5.2. Renewable Energy Certificates (RECs) and Tariff Regulations

3.5.3. National Mission on Waste-to-Energy

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Municipal Corporations, Waste Management Firms, Energy Producers)

3.8. Porters Five Forces (Supplier Bargaining Power, Buyer Power, etc.)

3.9. Competitive Ecosystem

4.1. By Technology Type (In Value %)

4.1.1. Thermal (Incineration, Pyrolysis, Gasification)

4.1.2. Biological (Anaerobic Digestion, Fermentation)

4.1.3. Chemical (Refuse-Derived Fuel, Plasma Arc Gasification)

4.2. By Application (In Value %)

4.2.1. Power Generation

4.2.2. Heat Generation

4.2.3. Fuel Conversion

4.3. By Waste Type (In Value %)

4.3.1. Municipal Solid Waste (MSW)

4.3.2. Industrial Waste

4.3.3. Agricultural Waste

4.3.4. Medical Waste

4.4. By End-User (In Value %)

4.4.1. Urban Municipalities

4.4.2. Industrial Facilities

4.4.3. Agriculture Sector

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. West India

4.5.4. East India

5.1. Detailed Profiles of Major Companies

5.1.1. Ramky Enviro Engineers Ltd.

5.1.2. Jindal Urban Waste Management

5.1.3. Essel Infraprojects Ltd.

5.1.4. Hitachi Zosen India Pvt. Ltd.

5.1.5. IL&FS Environmental Infrastructure & Services Ltd.

5.1.6. Thermax Limited

5.1.7. Veolia India

5.1.8. Nepra Resource Management Pvt. Ltd.

5.1.9. Organic Recycling Systems Pvt. Ltd.

5.1.10. Timarpur Okhla Waste Management Pvt. Ltd.

5.1.11. Suez India

5.1.12. Ramky Enviro Group

5.1.13. Hitachi Zosen India

5.1.14. ClearChem Development Pvt. Ltd.

5.1.15. GEPIL

5.2. Cross Comparison Parameters (No. of Employees, Installed Capacity, Projects Undertaken, Revenue, Investment, Technology Type, Market Share, Power Generated)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government and Private Funding

6.1. Waste Segregation and Disposal Guidelines

6.2. Compliance with National Green Tribunal (NGT) Rules

6.3. Carbon Credit Mechanism

6.4. Certification and Standards

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Government Policies, Waste Generation Projections, Technological Innovations)

8.1. By Technology Type (In Value %)

8.2. By Application (In Value %)

8.3. By Waste Type (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Key Entry Barriers and Success Factors

9.3. Strategic Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase involves mapping out key stakeholders in the India Waste-to-Energy market. Extensive desk research is conducted using both secondary sources and proprietary databases to identify critical variables such as waste generation trends, technological advancements, and regulatory developments.

In this phase, historical data related to the WTE market, including waste treatment capacities, energy production rates, and revenue generation, are analyzed. This analysis provides insights into the existing market size, dominant technology types, and application areas.

To validate market hypotheses, interviews with industry experts from waste management firms, WTE technology providers, and government agencies are conducted. These consultations offer practical insights into the markets operational landscape.

The final phase consolidates findings from various stakeholders, including manufacturers, technology providers, and municipal bodies, ensuring the accuracy and completeness of the report. Data is synthesized into a comprehensive market report that includes forecasts and strategic recommendations.

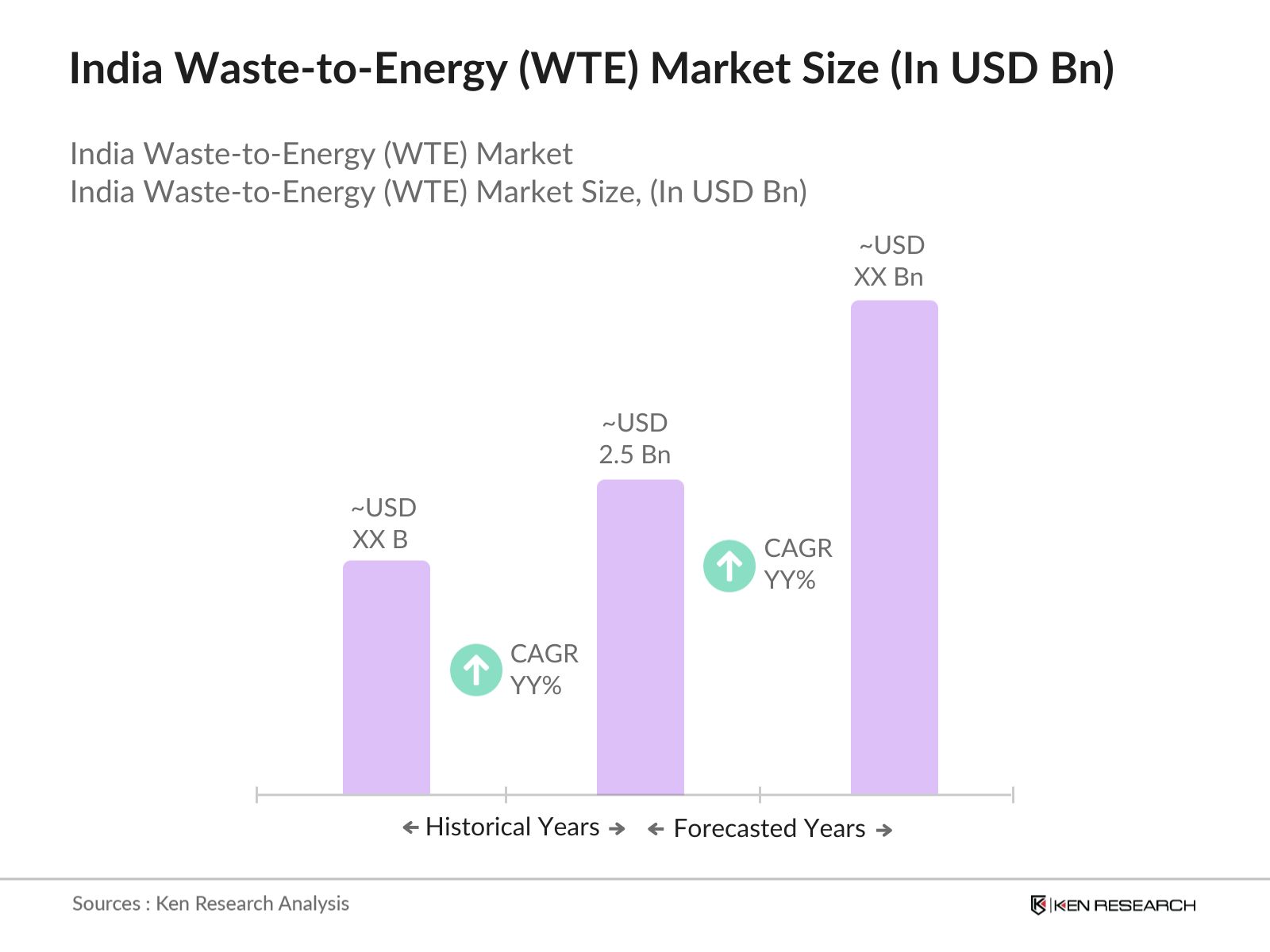

The India Waste-to-Energy market is valued at USD 2.5 billion, driven by the increasing generation of urban waste and government initiatives promoting renewable energy.

Challenges in the India Waste-to-Energy market include high capital investment requirements, operational efficiency issues, and public concerns regarding environmental safety.

Key players in the India Waste-to-Energy market include Ramky Enviro Engineers Ltd., Jindal Urban Waste Management, Hitachi Zosen India, Essel Infraprojects Ltd., and Veolia India.

The India Waste-to-Energy market is driven by increasing waste generation, government regulations on waste management, and the focus on reducing reliance on non-renewable energy sources.

Thermal technologies, such as incineration and gasification, dominate the India Waste-to-Energy market due to their ability to process large volumes of waste and recover energy efficiently.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.