Indonesia Automotive IoT Market Outlook to 2030

Region:Indonesia

Author(s):Sanjeev

Product Code:KROD3723

Region:Indonesia

Author(s):Sanjeev

Product Code:KROD3723

December 2024

81

The Indonesia Automotive IoT market is segmented by solution type and by application.

The Indonesia Automotive IoT market is dominated by a combination of local players and global automotive companies. The market is characterized by strategic partnerships and collaborations between automotive OEMs and IoT solution providers to enhance vehicle connectivity and data-driven applications. The competitive landscape indicates consolidation, with both local and global players dominating through technological innovations, partnerships, and IoT integrations.

|

Company Name |

Establishment Year |

Headquarters |

Key Markets |

Number of Employees |

Product Focus |

|

PT Astra Otoparts Tbk |

1976 |

Jakarta, Indonesia |

|||

|

PT Indomobil Sukses Int. Tbk |

1976 |

Jakarta, Indonesia |

|||

|

Telkomsel (PT Telekomunikasi) |

1995 |

Jakarta, Indonesia |

|||

|

Bosch Indonesia |

1917 |

Stuttgart, Germany |

|||

|

Denso Indonesia |

1949 |

Jakarta, Indonesia |

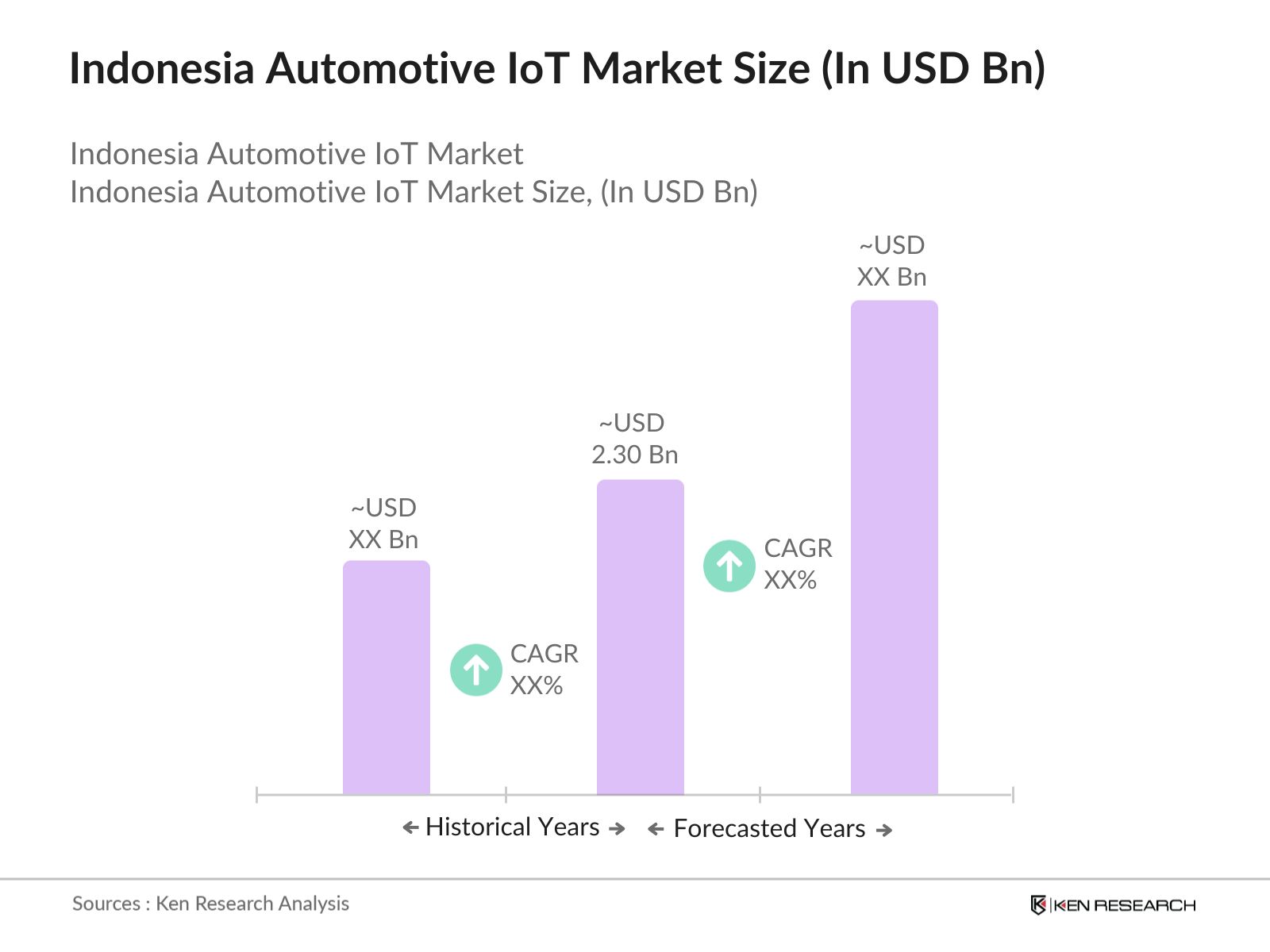

The Indonesia Automotive IoT market is expected to experience robust growth over the next five years, driven by the rising adoption of electric vehicles, advancements in autonomous driving technologies, and the expansion of 5G networks. Increasing demand for connected car features, such as vehicle diagnostics and real-time navigation, will play a significant role in this growth. Government policies supporting smart transportation and emission reduction efforts will further accelerate market adoption of IoT solutions in the automotive sector.

|

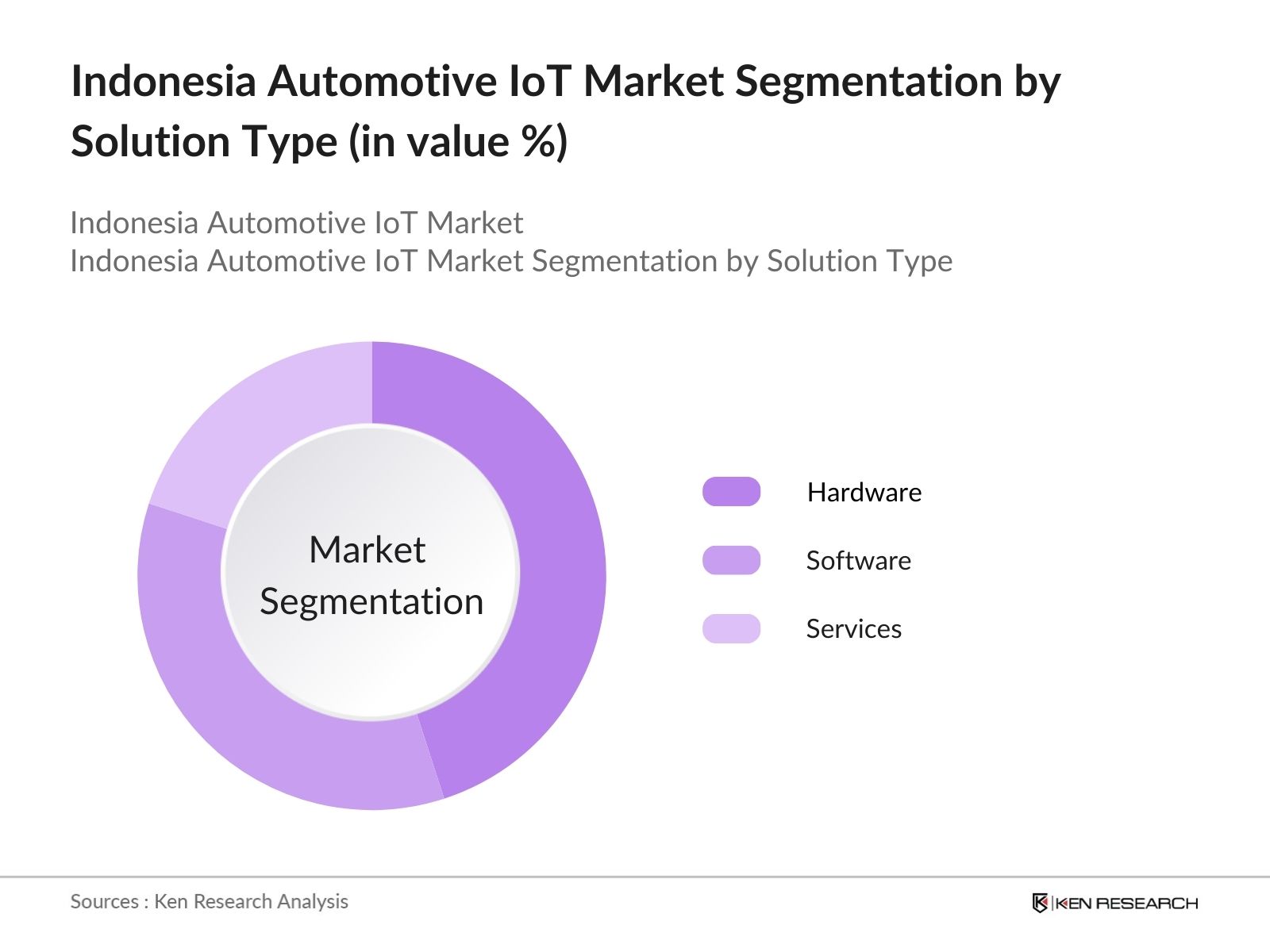

Hardware (Sensors, Actuators, Control Units) Software (Embedded, Cloud-Based Systems) Services (Consulting, Integration, Managed Services |

|

|

By Application |

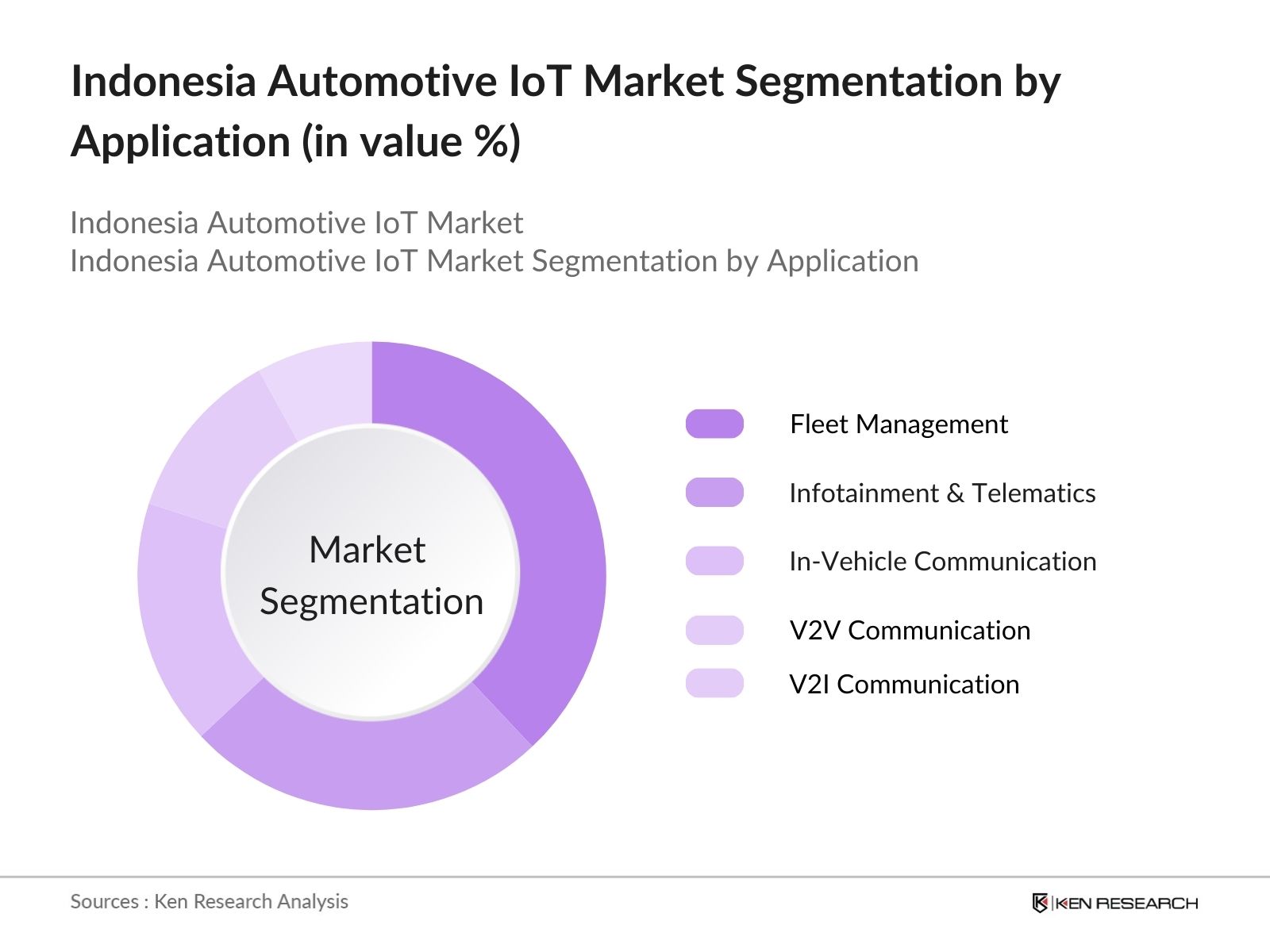

In-Vehicle Communication Vehicle-to-Vehicle (V2V) Communication Vehicle-to-Infrastructure (V2I) Communication Fleet Management Infotainment and Telematics |

|

By Connectivity |

Cellular Network (4G, 5G) Dedicated Short-Range Communication (DSRC) Wi-Fi and Bluetooth |

|

By End-User |

Passenger Vehicles Commercial Vehicles Heavy-Duty Vehicles |

|

By Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Demand for Connected Vehicles

3.1.2. Government Smart Mobility Initiatives

3.1.3. Consumer Shift Toward In-Vehicle Automation

3.1.4. Adoption of Telematics in Logistics and Fleet Management

3.2. Market Challenges

3.2.1. High Cost of Implementation

3.2.2. Data Privacy and Security Concerns

3.2.3. Fragmented IoT Standards

3.3. Opportunities

3.3.1. Partnerships with Telecom Operators for 5G Integration

3.3.2. Increasing Use of Cloud Computing in IoT Infrastructure

3.3.3. Expansion of IoT Applications in Electric Vehicles

3.4. Trends

3.4.1. Adoption of Edge Computing in Vehicle IoT Systems

3.4.2. Integration of AI with IoT for Predictive Maintenance

3.4.3. Use of IoT for Autonomous Driving Solutions

3.5. Government Regulations

3.5.1. National Roadmap for Smart Transportation

3.5.2. IoT Data Security Policies

3.5.3. Regulatory Compliance for Automotive IoT Devices

3.5.4. Emission Reduction and Green Vehicle Promotion Policies

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem

4.1. By Solution Type (In Value %)

4.1.1. Hardware (Sensors, Actuators, Control Units)

4.1.2. Software (Embedded, Cloud-Based Systems)

4.1.3. Services (Consulting, Integration, Managed Services)

4.2. By Application (In Value %)

4.2.1. In-Vehicle Communication

4.2.2. Vehicle-to-Vehicle (V2V) Communication

4.2.3. Vehicle-to-Infrastructure (V2I) Communication

4.2.4. Fleet Management

4.2.5. Infotainment and Telematics

4.3. By Connectivity (In Value %)

4.3.1. Cellular Network (4G, 5G)

4.3.2. Dedicated Short-Range Communication (DSRC)

4.3.3. Wi-Fi and Bluetooth

4.4. By End-User (In Value %)

4.4.1. Passenger Vehicles

4.4.2. Commercial Vehicles

4.4.3. Heavy-Duty Vehicles

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. West

4.5.4. South

5.1. Detailed Profiles of Major Companies 5.1.1. PT Astra Otoparts Tbk

5.1.2. PT Indomobil Sukses Internasional Tbk

5.1.3. Telkomsel (PT Telekomunikasi Selular)

5.1.4. PT Gojek Indonesia

5.1.5. Bosch Indonesia

5.1.6. Denso Indonesia

5.1.7. PT Toyota Astra Motor

5.1.8. Harman Indonesia

5.1.9. PT Suzuki Indomobil Motor

5.1.10. PT Honda Prospect Motor

5.1.11. Continental Automotive Indonesia

5.1.12. PT United Tractors Tbk

5.1.13. PT Telekomunikasi Indonesia Tbk

5.1.14. ZF Group Indonesia

5.1.15. Hyundai Motors Indonesia

5.2. Cross Comparison Parameters

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Automotive Safety Standards

6.2. IoT Data Privacy Regulations

6.3. Vehicle Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Solution Type (In Value %)

8.2. By Application (In Value %)

8.3. By Connectivity (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial step focuses on constructing an ecosystem map encompassing all major stakeholders within the Indonesia Automotive IoT market. This step involves extensive desk research and the use of proprietary databases to gather comprehensive industry-level information, with the aim of identifying and defining the critical variables influencing market dynamics.

In this phase, historical data pertaining to the Indonesia Automotive IoT market is compiled and analyzed. This includes assessing market penetration, connectivity infrastructure, and IoT solution adoption rates. Additionally, we evaluate the operational efficiencies of vehicle IoT solutions, ensuring accurate market revenue estimates.

Market hypotheses are developed and validated through computer-assisted telephone interviews (CATIs) with industry experts representing companies involved in the automotive and IoT sectors. These consultations provide operational and financial insights, helping refine and validate the market data.

The final phase involves direct engagement with automotive manufacturers and IoT providers to gain detailed insights into product segments, sales performance, and customer preferences. This interaction verifies and complements the data derived from the bottom-up approach, ensuring a comprehensive analysis of the Indonesia Automotive IoT market.

The Indonesia Automotive IoT market was valued at USD 1.7 billion, driven by increasing demand for connected vehicles, in-vehicle communication systems, and telematics-based solutions.

Key challenges in Indonesia Automotive IoT market include the high cost of IoT hardware, concerns over data privacy and security, and the lack of standardized IoT protocols, all of which hinder rapid adoption.

Major players in the Indonesia Automotive IoT market include PT Astra Otoparts Tbk, Telkomsel, Bosch Indonesia, PT Toyota Astra Motor, and Hyundai Motors Indonesia. These companies dominate due to their technological innovations and strong market presence.

The Indonesia Automotive IoT market is propelled by factors such as the increasing adoption of telematics and connected car systems, government support for smart mobility initiatives, and advancements in 5G technology.

Java and Sumatra are the dominant regions in the Indonesia Automotive IoT market, owing to their highly developed infrastructure, large urban populations, and presence of leading automotive manufacturers.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.