Indonesia Buy Now Pay Later (BNPL) Market Outlook to 2030

Region:Indonesia

Author(s):Sanjeev

Product Code:KROD4614

Region:Indonesia

Author(s):Sanjeev

Product Code:KROD4614

October 2024

81

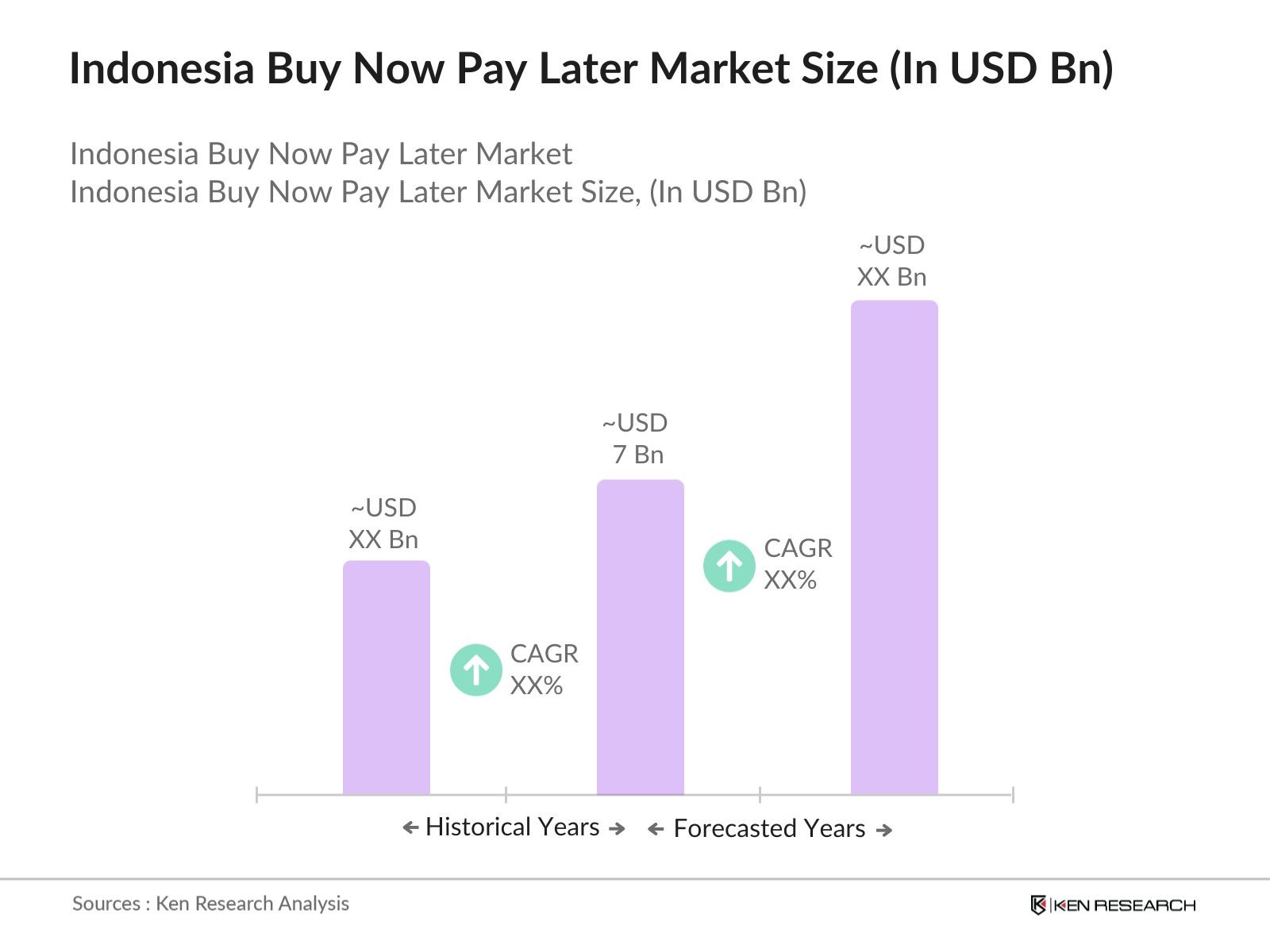

The Indonesia Buy Now Pay Later (BNPL) market is valued at USD 7 billion, driven by the rapid rise of e-commerce and fintech integrations. Key factors driving this growth include increasing smartphone penetration, particularly among young, tech-savvy consumers, and the demand for flexible payment options amid the rise of digital retail. The market is primarily supported by micro-lending platforms, fintech startups, and large-scale collaborations between BNPL providers and online retailers, which have fueled growth in digital transactions.

Jakarta, Bandung, and Surabaya dominate the BNPL market due to their high urbanization rates, established digital payment infrastructures, and robust e-commerce markets. The increasing integration of BNPL services within major e-commerce platforms and super apps, coupled with consumer demand for installment-based payment options, has made these cities prime locations for the adoption of BNPL services. Jakarta, in particular, serves as the country's financial hub, making it a key driver in Indonesia’s BNPL market.

The OJK has introduced comprehensive guidelines for BNPL providers in 2024, focusing on consumer protection and financial transparency. These regulations mandate that BNPL services disclose all fees and interest rates upfront, while also implementing stricter KYC procedures to prevent fraud. The guidelines also cap interest rates for certain categories of consumers, aiming to protect lower-income groups from excessive debt accumulation. Compliance with these guidelines is now a requirement for all licensed BNPL providers operating in Indonesia.

The Indonesia Buy Now Pay Later market is dominated by both local and global players, each bringing innovative solutions to the table. Key players are leveraging partnerships with e-commerce platforms and fintech companies to offer seamless user experiences. Local startups like Kredivo and Akulaku have gained significant traction through their user-friendly interfaces and micro-lending services. Global entrants such as Atome and Splitit have also captured market share by focusing on cross-border e-commerce opportunities.

|

Company |

Established |

Headquarters |

Key Partnerships |

Funding Rounds |

Technology Platform |

User Base |

Revenue Model |

Target Market |

Growth Strategy |

|

Kredivo |

2015 |

Jakarta |

- |

- |

- |

- |

- |

- |

- |

|

Akulaku |

2016 |

Jakarta |

- |

- |

- |

- |

- |

- |

- |

|

Atome |

2019 |

Singapore |

- |

- |

- |

- |

- |

- |

- |

|

GoPayLater |

2020 |

Jakarta |

- |

- |

- |

- |

- |

- |

- |

|

Indodana |

2017 |

Jakarta |

- |

- |

- |

- |

- |

- |

- |

Increasing Smartphone Penetration: Indonesia's smartphone penetration has reached 85.4% in 2024, driven by affordable data packages and the widespread availability of budget smartphones. This is critical for the Buy Now Pay Later (BNPL) market, as smartphones are the primary access points for digital payment solutions. With 237 million internet users, the country's mobile-first economy enables more consumers to adopt BNPL services, particularly in urban areas where mobile connectivity is near universal. The expanding 5G network is expected to further bolster this adoption, especially in metropolitan areas like Jakarta and Surabaya.

Rising E-commerce Adoption: Indonesia's e-commerce sector reached $53.2 billion in revenue in 2024, contributing significantly to the rise of BNPL services. With the increased consumer demand for online shopping, BNPL options are becoming a popular payment alternative, especially among younger consumers who prefer flexible payment terms. Data from the Ministry of Trade highlights that over 74% of Indonesians aged 18-35 now make at least one online purchase per month, spurring demand for payment flexibility that BNPL services provide.

Financial Inclusion Initiatives: Government-backed financial inclusion initiatives have connected over 140 million Indonesians to formal banking services by 2024. Programs like “Gerakan Nasional Non-Tunai” (GNNT) and the expansion of the QRIS (Quick Response Code Indonesian Standard) system are crucial in fostering the growth of BNPL, especially among previously unbanked or underbanked populations. As more Indonesians gain access to digital financial services, the BNPL market has a fertile environment to grow, driven by both regulatory support and increasing consumer access to digital payment methods.

Regulatory Uncertainty (OJK Oversight, Financial Consumer Protection): Indonesia's Financial Services Authority (OJK) is tightening oversight of the BNPL sector in 2024, introducing new rules on financial consumer protection and risk management. These regulations, while aimed at preventing market abuse, have created uncertainty for BNPL providers, many of whom must re-align their practices to meet stricter compliance standards. The lack of clear guidelines on interest rates and consumer data protection is a significant challenge for new entrants and small providers. The OJK is expected to issue further clarification, but this regulatory ambiguity can slow market expansion.

Rising Consumer Debt Concerns: In 2024, household debt in Indonesia climbed to over IDR 1,600 trillion, raising concerns about the rising consumer debt burden. BNPL services, with their easy access to credit, contribute to this issue, as many consumers lack financial literacy regarding the risks of deferred payments. Although default rates are low compared to traditional loans, increasing debt accumulation among lower-income groups could affect market growth. OJK has also indicated that stricter debt-to-income ratio regulations may be introduced, which could further constrain BNPL service providers.

Over the next five years, the Indonesia Buy Now Pay Later market is expected to experience exponential growth driven by expanding fintech ecosystems, increased adoption of mobile wallets, and the rising popularity of e-commerce. This growth will also be spurred by Indonesia’s young, digitally engaged population and a surge in online retail transactions. The future of the market will likely include further innovation in payment technologies, deeper fintech and e-commerce integrations, and improved regulation to protect consumer interests.

|

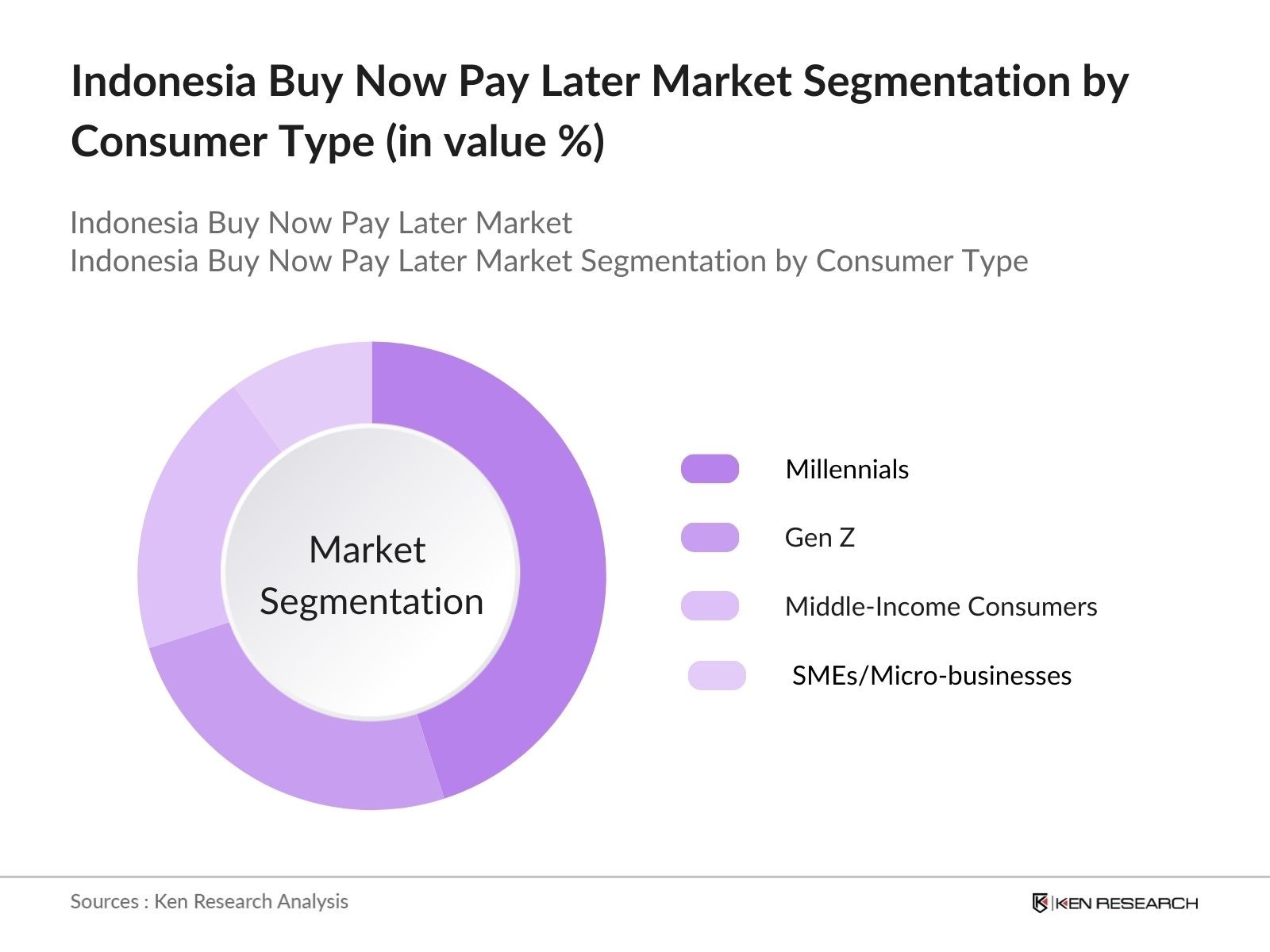

By Consumer Type |

Millennials Gen Z Middle-Income Consumers SMEs and Micro-businesses |

|

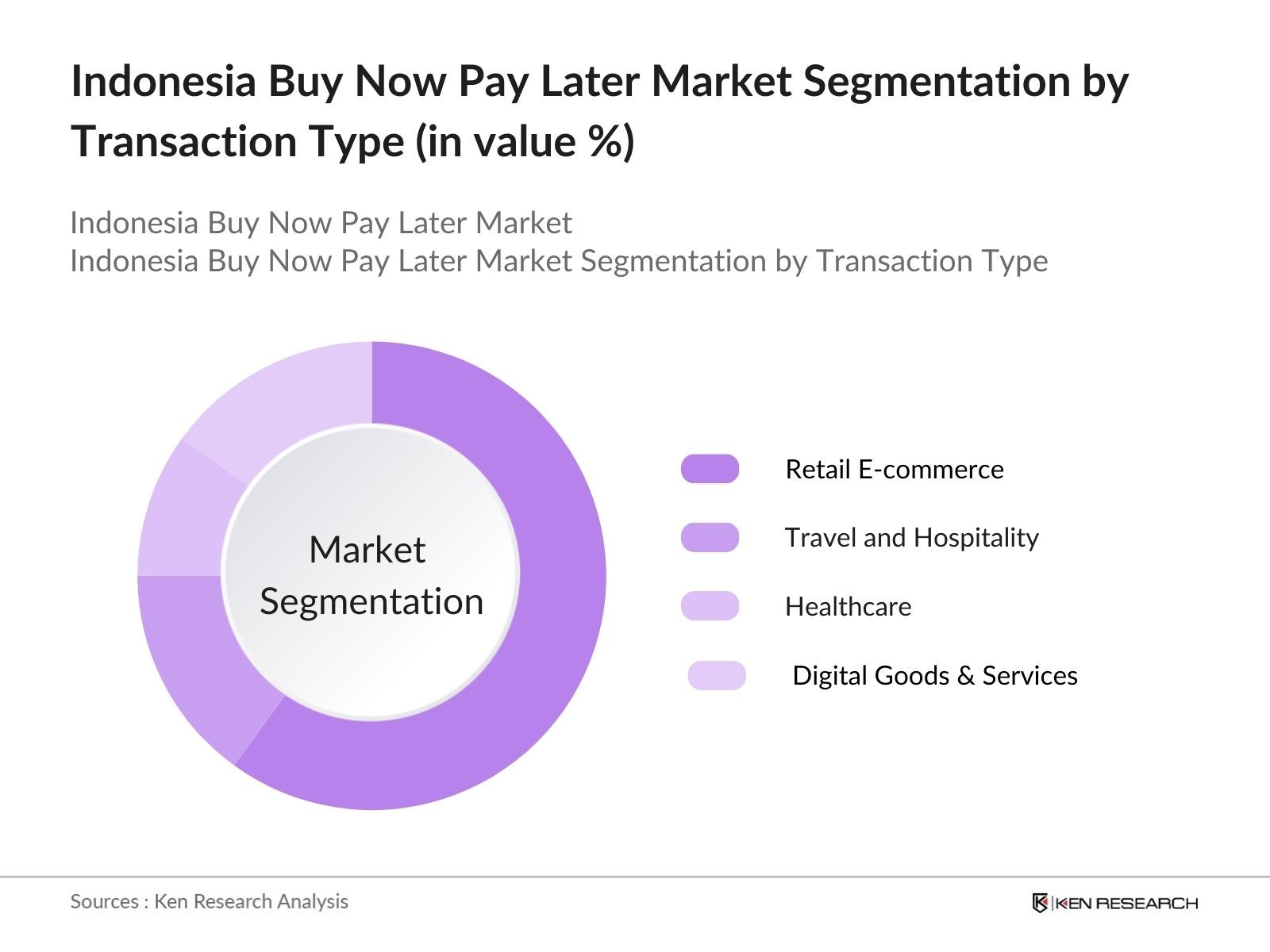

By Transaction Type |

Retail E-commerce Travel and Hospitality Healthcare Digital Goods and Services |

|

By Platform Type |

E-commerce Platforms BNPL Aggregators Fintech Apps Retail POS Solutions |

|

By Payment Model |

Installment Plans Pay-in-4 Models Interest-free Payments Deferred Payments |

|

By Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Growth in Digital Financial Services Adoption)

1.4. Market Segmentation Overview (Consumer Segments, Transaction Types, Platforms)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis (Transaction Volume, Active Users)

2.3. Key Market Developments and Milestones (E-commerce Partnerships, Fintech Integration)

3.1. Growth Drivers

3.1.1. Increasing Smartphone Penetration

3.1.2. Rising E-commerce Adoption

3.1.3. Financial Inclusion Initiatives

3.1.4. Consumer Demand for Flexible Payment Solutions

3.2. Market Challenges

3.2.1. Regulatory Uncertainty (OJK Oversight, Financial Consumer Protection)

3.2.2. Rising Consumer Debt Concerns

3.2.3. Fraud and Security Risks (Transaction Authentication)

3.3. Opportunities

3.3.1. Growth in Micro and Small Retailer Adoption

3.3.2. Expansion into Untapped Rural Markets

3.3.3. Cross-border E-commerce Facilitation

3.4. Trends

3.4.1. Integration with E-wallets and Super Apps

3.4.2. Increasing Usage in In-store Payments

3.4.3. Rise of Interest-free Payment Models

3.5. Government Regulation

3.5.1. Financial Services Authority (OJK) Guidelines

3.5.2. Digital Payment Licensing (Bank Indonesia)

3.5.3. E-commerce Transaction Regulations (Ministry of Trade)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (BNPL Providers, Fintech Platforms, Banks, E-commerce Players)

3.8. Porter’s Five Forces Analysis (Competitive Rivalry, Threat of New Entrants)

3.9. Competition Ecosystem

4.1. By Consumer Type (In Value %)

4.1.1. Millennials

4.1.2. Gen Z

4.1.3. Middle-Income Consumers

4.1.4. SMEs and Micro-businesses

4.2. By Transaction Type (In Value %)

4.2.1. Retail E-commerce

4.2.2. Travel and Hospitality

4.2.3. Healthcare

4.2.4. Digital Goods and Services

4.3. By Platform Type (In Value %)

4.3.1. E-commerce Platforms

4.3.2. BNPL Aggregators

4.3.3. Fintech Apps

4.3.4. Retail POS Solutions

4.4. By Payment Model (In Value %)

4.4.1. Installment Plans

4.4.2. Pay-in-4 Models

4.4.3. Interest-free Payments

4.4.4. Deferred Payments

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. West

4.5.4. South

5.1. Detailed Profiles of Major Companies

5.1.1. Kredivo

5.1.2. Akulaku

5.1.3. Atome

5.1.4. Shopee PayLater

5.1.5. GoPayLater

5.1.6. Indodana

5.1.7. Brankas

5.1.8. FinAccel

5.1.9. Splitit

5.1.10. Traveloka PayLater

5.1.11. Julo

5.1.12. SPayLater (Shopback)

5.1.13. UangMe

5.1.14. Investree

5.1.15. Cicil

5.2. Cross Comparison Parameters (Funding Rounds, Key Partnerships, Technology Integration, User Base, Business Model, Loan Disbursement Size, Revenue Model, Credit Scoring Technology)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Product Innovations, Market Entry Strategies)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Initiatives

5.9. Private Equity Investments

6.1. BNPL Licensing Requirements (Bank Indonesia)

6.2. Consumer Protection Laws (OJK)

6.3. Compliance with Digital Payment Standards

6.4. Data Privacy and Security Regulations

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Consumer Type (In Value %)

8.2. By Transaction Type (In Value %)

8.3. By Platform Type (In Value %)

8.4. By Payment Model (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Behavior Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The research begins with a comprehensive mapping of the ecosystem surrounding the Indonesia BNPL Market. This involves understanding the key stakeholders such as consumers, BNPL platforms, fintech providers, and government regulators. The process includes extensive desk research using proprietary databases and government publications to gather critical industry insights.

In this step, historical data on consumer credit, e-commerce growth, and digital payment penetration is collected and analyzed. This helps assess the BNPL market’s size, transaction volume, and user adoption. Further, the revenue generation potential of BNPL services in various consumer and retail segments is evaluated.

Market experts from fintech companies, BNPL providers, and financial institutions are consulted through interviews and discussions. These insights offer real-world perspectives on market trends, challenges, and opportunities, which help validate the market hypotheses.

The final phase involves combining quantitative data and expert opinions to generate an accurate market analysis. This synthesis ensures that the Indonesia BNPL Market report is comprehensive and provides an actionable outlook for stakeholders in the fintech ecosystem.

The Indonesia Buy Now Pay Later market is valued at USD 7 billion, driven by the rapid rise in e-commerce, fintech adoption, and demand for flexible payment options.

Challenges in Indonesia Buy Now Pay Later Market include regulatory uncertainties, rising consumer debt concerns, and the risk of fraud in online transactions. Regulatory oversight from the OJK and Bank Indonesia is critical in maintaining consumer trust.

Key players in Indonesia Buy Now Pay Later Market include Kredivo, Akulaku, Atome, GoPayLater, and Indodana. These companies dominate the market due to their strong partnerships with leading e-commerce platforms and innovative mobile-first solutions.

The Indonesia Buy Now Pay Later Market is driven by increasing smartphone penetration, expanding e-commerce activity, and consumer demand for more flexible, interest-free payment solutions. Collaborations between BNPL providers and online retailers have also accelerated growth.

Trends include the integration of Indonesia Buy Now Pay Later Market with e-wallets and super apps, growing adoption for in-store payments, and the increasing use of installment-based payment models across various consumer segments.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.