Indonesia Cheese Market Outlook to 2030

Region:Indonesia

Author(s):Paribhasha Tiwari

Product Code:KROD3570

Region:Indonesia

Author(s):Paribhasha Tiwari

Product Code:KROD3570

November 2024

88

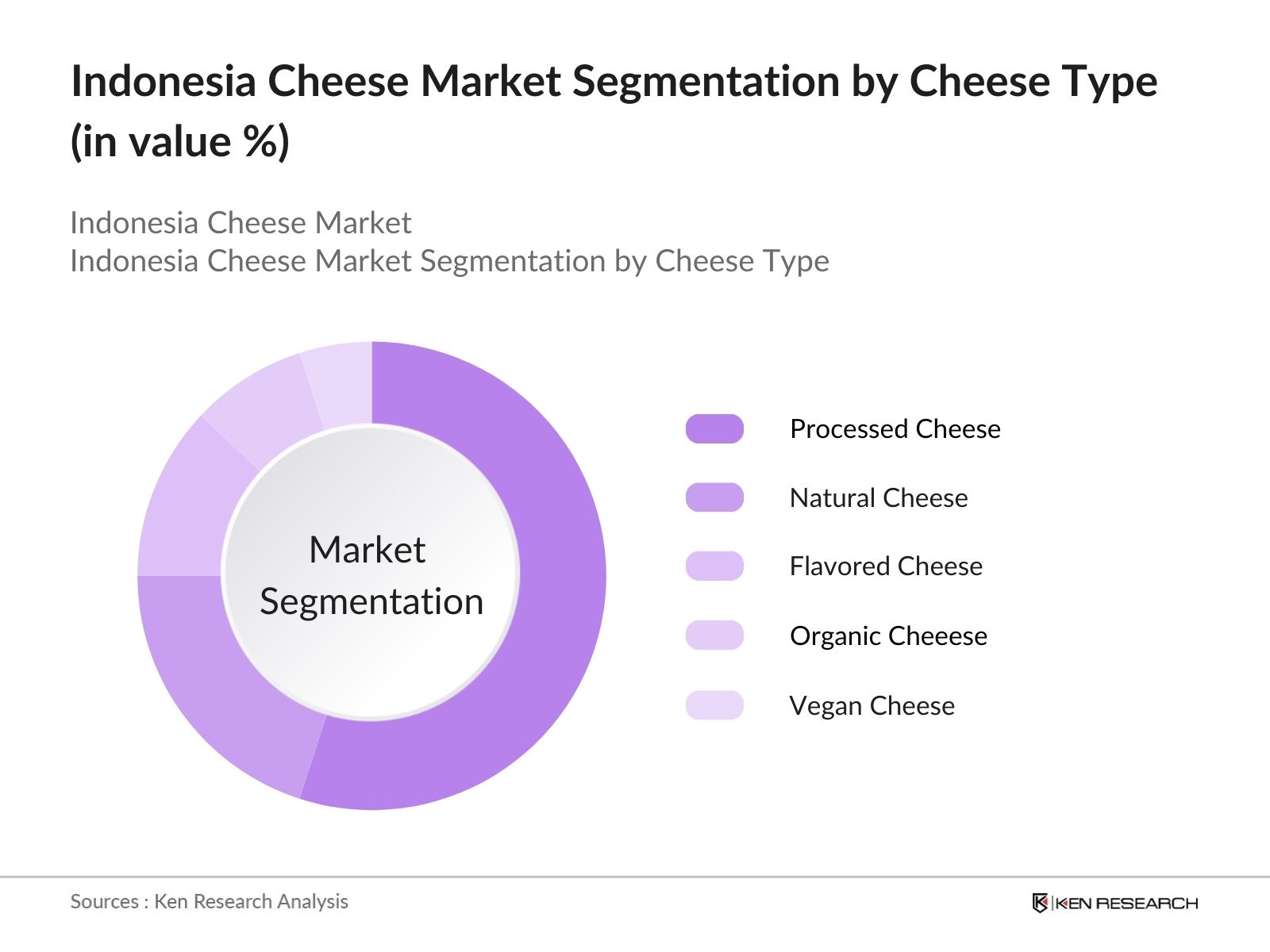

By Cheese Type: Indonesia's cheese market is segmented by cheese type into natural cheese, processed cheese, flavored cheese, organic cheese, and vegan cheese. Processed cheese held the dominant market share. This is primarily due to its versatility and long shelf life, making it a popular choice among consumers and foodservice operators alike. Processed cheese is widely used in fast food, snacks, and ready-to-eat meals, which have gained popularity as the urban lifestyle becomes more fast-paced. The availability of affordable processed cheese brands and its incorporation into traditional Indonesian dishes further fuel its growth.

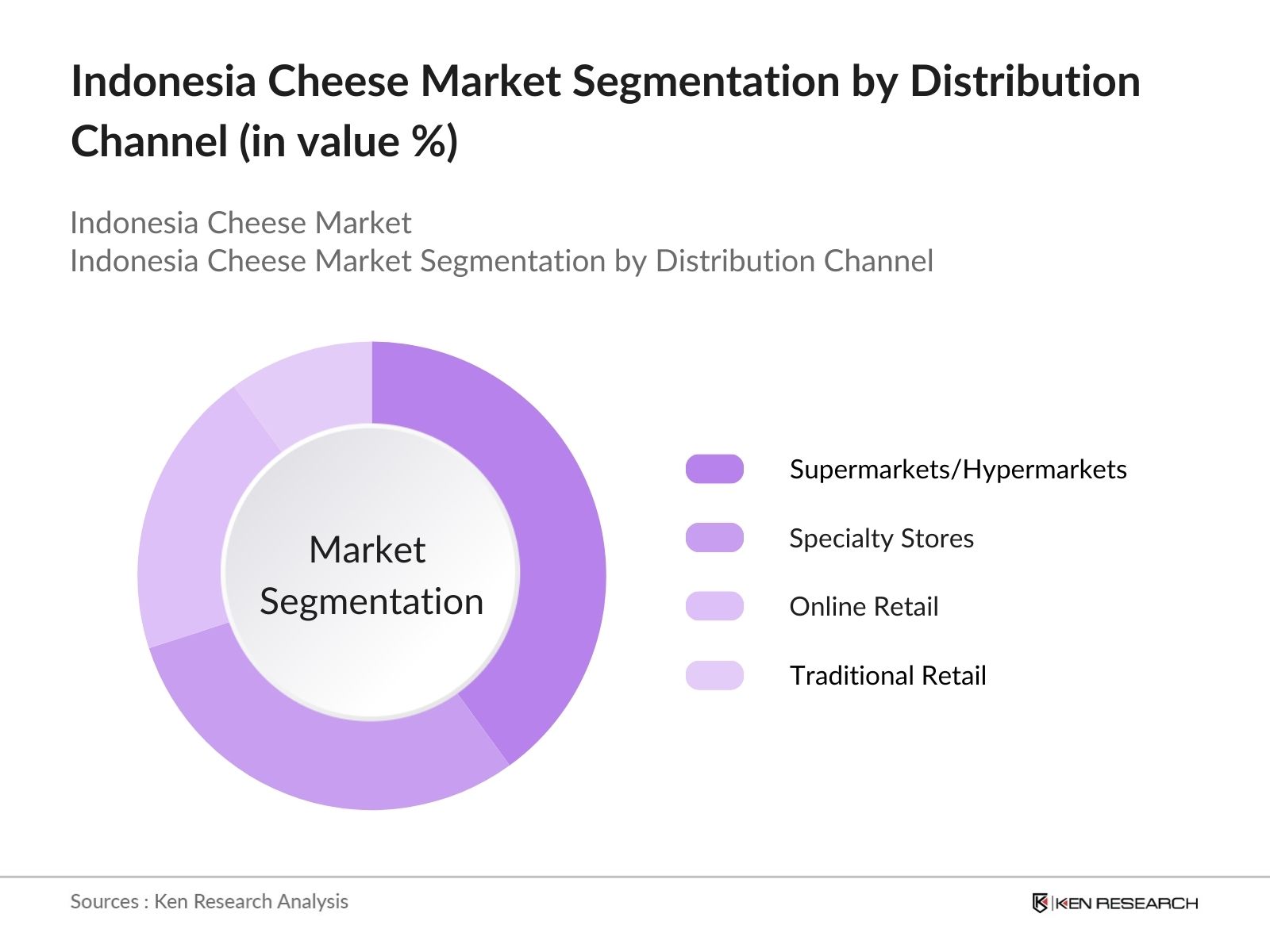

By Distribution Channel: The cheese market in Indonesia is also segmented by distribution channel into supermarkets/hypermarkets, specialty stores, online retail, and traditional retail. Supermarkets and hypermarkets hold the largest market share in the market. This dominance can be attributed to their widespread presence in urban areas and their ability to offer a wide variety of cheese products, catering to both local and international tastes. Additionally, the modern retail format provides better refrigeration facilities, ensuring product freshness, which is crucial for dairy items like cheese. The growing trend of modern shopping experiences and promotional activities by large retail chains also contribute to the popularity of this distribution channel.

The Indonesia cheese market is characterized by both domestic and international players. A few major players have a stronghold due to their established distribution networks, product innovation, and brand recognition. The competitive landscape in Indonesia's cheese market is led by large global players such as Kraft Heinz and FrieslandCampina, alongside local companies like PT Mulia Boga Raya Tbk, which has capitalized on its local production and distribution channels.

|

Company |

Year Established |

Headquarters |

Cheese Types |

Revenue |

Distribution Network |

Local Production |

Brand Recognition |

Innovation |

Customer Loyalty |

|

PT Mulia Boga Raya Tbk |

2006 |

Jakarta, Indonesia |

|||||||

|

Kraft Heinz Indonesia |

2005 |

Jakarta, Indonesia |

|||||||

|

Greenfields Indonesia |

1997 |

East Java, Indonesia |

|||||||

|

FrieslandCampina Indonesia |

1927 |

Jakarta, Indonesia |

|||||||

|

Indolakto (Indofood) |

1994 |

Jakarta, Indonesia |

The Indonesia cheese market is expected to experience substantial growth over the next five years, driven by increasing urbanization, the rise of the middle class, and the growing demand for western-style food products. The country's expanding foodservice sector, particularly fast food and casual dining, is also expected to fuel the demand for processed and flavored cheese. Additionally, consumer awareness regarding the nutritional benefits of cheese and its protein content is likely to boost consumption across various demographics.

|

By Cheese Type |

Natural Cheese Processed Cheese Flavored Cheese Organic Cheese Vegan Cheese |

|

By Application |

Household Consumption Foodservice Industry Retail Sector Industrial Use |

|

By Distribution Channel |

Supermarkets/Hypermarkets Specialty Stores Online Retail Traditional Retail |

|

By Source |

Cow Milk Cheese Goat Milk Cheese Sheep Milk Cheese Plant-Based Cheese |

|

By Region |

Jakarta Bali Java Sumatra Sulawesi |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Western Food Preferences (Cheese Consumption Patterns)

3.1.2. Increasing Disposable Income (Per Capita Income)

3.1.3. Expanding Food Service Industry (Restaurants & Cafes)

3.1.4. Urbanization (Cheese Demand in Urban Areas)

3.2. Market Challenges

3.2.1. Limited Cold Chain Infrastructure (Cheese Storage Challenges)

3.2.2. High Import Dependency (Import vs. Domestic Production)

3.2.3. High Price Sensitivity (Price Elasticity of Cheese)

3.3. Opportunities

3.3.1. Growth in Cheese-based Products (Innovation in Cheese Products)

3.3.2. Growing Modern Retail Formats (Cheese Availability in Supermarkets)

3.3.3. Local Cheese Production Initiatives (Expansion of Domestic Production)

3.4. Trends

3.4.1. Shift Towards Organic Cheese (Organic and Natural Cheese Trends)

3.4.2. Rising Demand for Processed Cheese (Cheddar, Mozzarella, and Other Varieties)

3.4.3. Vegan Cheese Alternatives (Alternative Dairy Products)

3.5. Government Regulations

3.5.1. Import Tariffs on Cheese

3.5.2. Dairy Safety and Quality Standards

3.5.3. Policies to Encourage Domestic Dairy Industry

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Cheese Type (In Value %)

4.1.1. Natural Cheese

4.1.2. Processed Cheese

4.1.3. Flavored Cheese

4.1.4. Organic Cheese

4.1.5. Vegan Cheese

4.2. By Application (In Value %)

4.2.1. Household Consumption

4.2.2. Foodservice Industry (Restaurants, Cafes)

4.2.3. Retail Sector (Supermarkets, Hypermarkets)

4.2.4. Industrial Use (Food Processing Companies)

4.3. By Distribution Channel (In Value %)

4.3.1. Supermarkets/Hypermarkets

4.3.2. Specialty Stores

4.3.3. Online Retail

4.3.4. Traditional Retail

4.4. By Source (In Value %)

4.4.1. Cow Milk Cheese

4.4.2. Goat Milk Cheese

4.4.3. Sheep Milk Cheese

4.4.4. Plant-Based Cheese

4.5. By Region (In Value %)

4.5.1. Jakarta

4.5.2. Bali

4.5.3. Java

4.5.4. Sumatra

4.5.5. Sulawesi

5.1. Detailed Profiles of Major Companies

5.1.1. PT Mulia Boga Raya Tbk

5.1.2. Kraft Heinz Indonesia

5.1.3. Greenfields Indonesia

5.1.4. Cisarua Mountain Dairy (Cimory)

5.1.5. Bongrain Indonesia

5.1.6. Indolakto (Indofood)

5.1.7. PT Tetra Pak Indonesia

5.1.8. Bega Cheese Limited

5.1.9. Arla Foods Indonesia

5.1.10. Fromageries Bel Indonesia

5.1.11. FrieslandCampina Indonesia

5.1.12. Fonterra Brands Indonesia

5.1.13. Parag Milk Foods

5.1.14. Saputo Inc.

5.1.15. Lactalis Indonesia

5.2. Cross Comparison Parameters (Production Volume, Local Distribution Network, Import Dependency, Market Penetration, Brand Loyalty, Product Innovation, Marketing Strategy, Consumer Perception)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants and Subsidies

5.8. Private Equity Investments

6.1. Dairy Product Certification

6.2. Import Licensing Requirements

6.3. Food Safety Standards for Cheese Products

6.4. Labeling Regulations

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Cheese Type (In Value %)

8.2. By Application (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By Source (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe first step involved mapping out the key stakeholders in the Indonesia cheese market. This included identifying major cheese producers, distributors, retailers, and end consumers. Secondary research through industry databases and reports was utilized to define the major variables influencing the market, such as cheese demand, production capacity, and market penetration.

In this phase, historical data was analyzed to determine the market's growth trajectory and current size. Parameters such as cheese production volumes, distribution networks, and consumer consumption patterns were assessed to create a reliable market forecast.

Key market assumptions were tested through consultations with industry experts, including representatives from leading dairy companies. These interviews helped validate our data on market drivers, challenges, and future growth prospects.

After gathering insights from industry stakeholders, the final market analysis was constructed. This synthesis included a bottom-up approach to ensure data accuracy and reliability, culminating in a detailed report on the Indonesia cheese market.

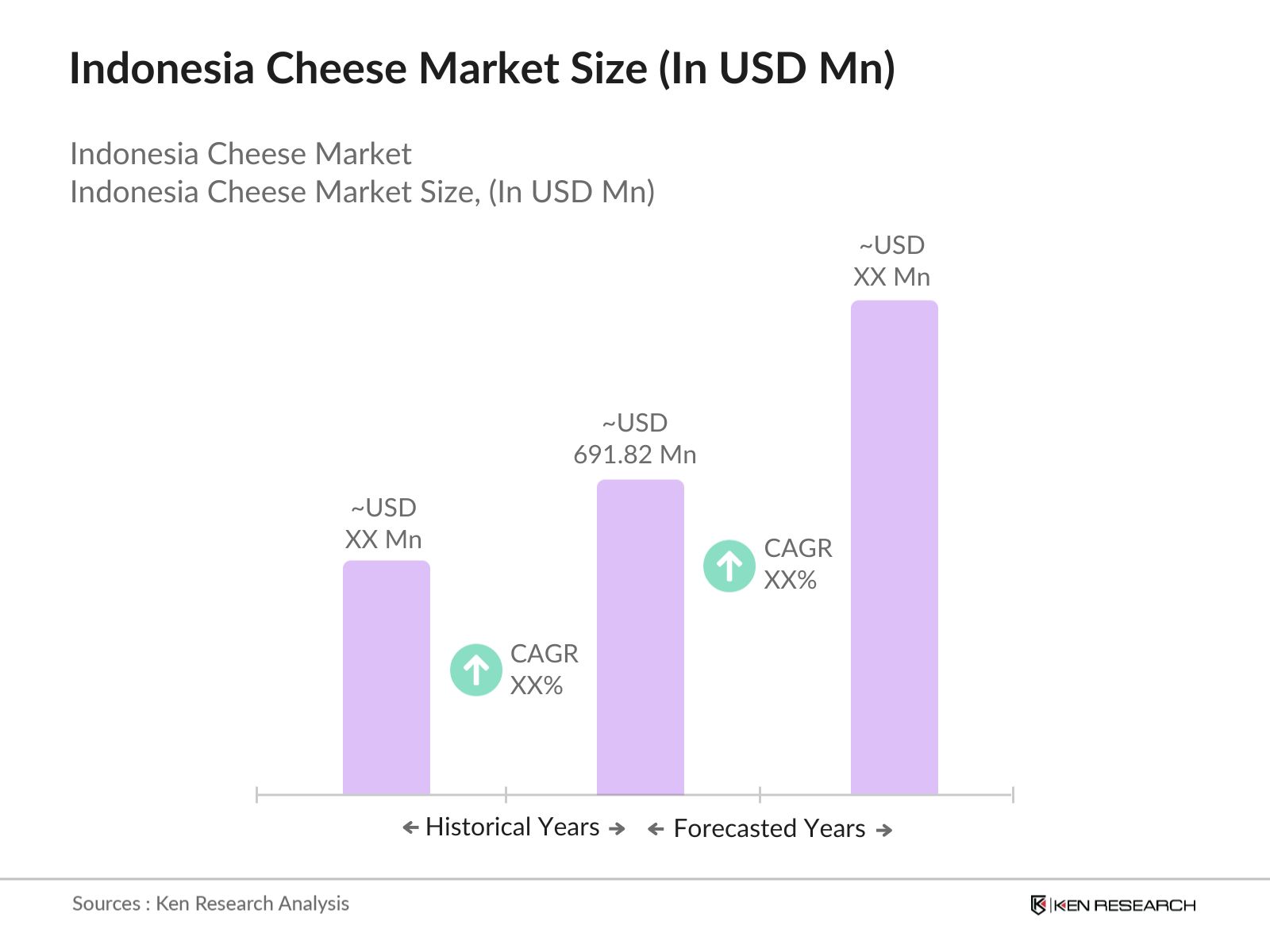

The Indonesia cheese market is valued at USD 691.82 million in 2023, driven by rising demand for western-style foods, especially in urban centers like Jakarta and Bali.

Challenges in the Indonesia cheese market include limited cold chain infrastructure, high dependency on imports, and price sensitivity among consumers.

Key players include PT Mulia Boga Raya Tbk, Kraft Heinz Indonesia, Greenfields Indonesia, and FrieslandCampina Indonesia. These companies dominate due to their extensive distribution networks and strong brand presence.

Growth in the Indonesia cheese market is driven by increasing urbanization, the rise of modern retail formats, and a growing middle-class population that demands more dairy-based products.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.