Indonesia Cosmetics Market Outlook to 2030

Region:Indonesia

Author(s):Meenakshi

Product Code:KROD3772

Region:Indonesia

Author(s):Meenakshi

Product Code:KROD3772

October 2024

81

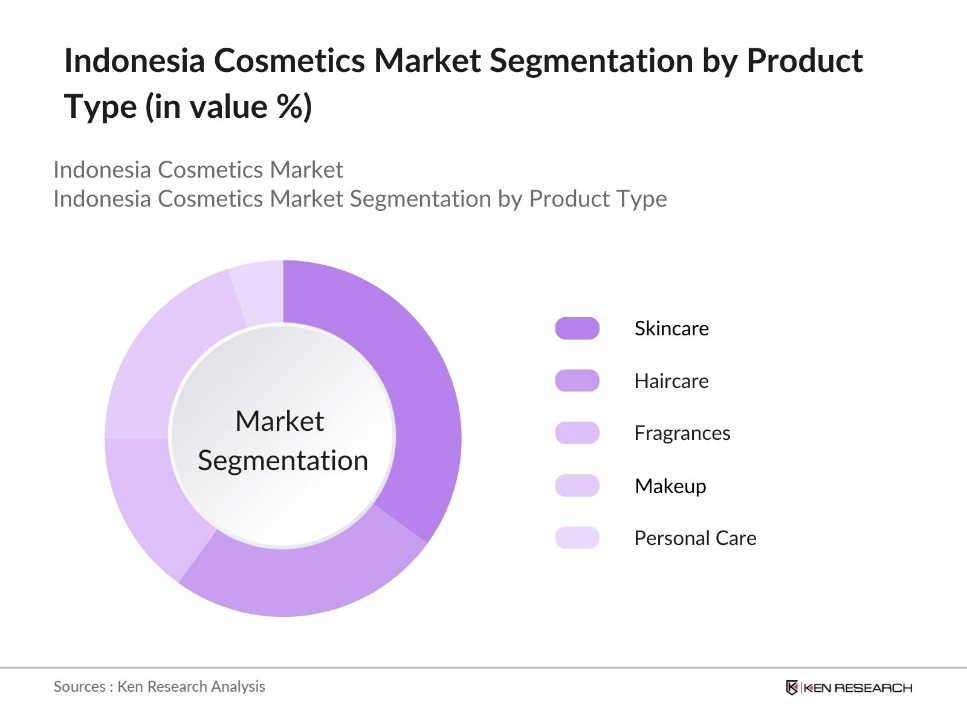

By Product Type: The Indonesia Cosmetics Market is segmented by product type into skincare, haircare, fragrances, makeup, and personal care products. Skincare products have a dominant market share in the Indonesia Cosmetics Market due to their increasing popularity among consumers concerned with health and personal care. This segment includes products such as moisturizers, anti-aging creams, and sunscreen lotions, which are widely used by both men and women. The rise of skincare routines and the influence of Korean beauty (K-beauty) trends also contribute to the dominance of this segment.

By Distribution Channel: The Indonesia Cosmetics Market is segmented by distribution channel into online retail, supermarkets/hypermarkets, specialty stores, department stores, and pharmacies. Online retail holds the largest market share within the distribution channel segment. This is driven by the increasing penetration of the internet and the growing popularity of e-commerce platforms like Tokopedia, Shopee, and Lazada. Consumers find it more convenient to purchase cosmetics online due to discounts, doorstep delivery, and a wide variety of choices. The pandemic has further accelerated this shift toward online shopping for beauty products.

The Indonesia Cosmetics Market is dominated by a few key players, including both domestic and international brands. Local brands like Wardah and Mustika Ratu have a stronghold in the halal beauty segment, while global giants like L'Oral and Unilever maintain a significant presence through their wide product portfolios and strong marketing strategies. This consolidation of power highlights the significant influence of these key players, with the competition largely focusing on innovation, pricing strategies, and product differentiation.

|

Company Name |

Year of Establishment |

Headquarters |

Product Range |

Market Focus |

Halal Certified |

Distribution Network |

Revenue (2023) |

Sustainability Initiatives |

|

Wardah |

1985 |

Jakarta |

||||||

|

Mustika Ratu |

1975 |

Jakarta |

||||||

|

L'Oral Indonesia |

1979 |

Jakarta |

||||||

|

Unilever Indonesia |

1933 |

Jakarta |

||||||

|

PZ Cussons Indonesia |

1975 |

Jakarta |

Over the next five years, the Indonesia Cosmetics Market is expected to experience significant growth, driven by increasing consumer demand for premium, natural, and halal-certified cosmetics. The rise of e-commerce platforms will continue to fuel market expansion as more consumers prefer the convenience of online shopping. Moreover, the growing male grooming segment and increasing awareness of anti-aging and skincare routines are anticipated to provide new growth opportunities for market players.

|

Product Type |

Skincare Haircare Fragrances Makeup Personal Care |

|

Distribution Channel |

Online Retail Supermarkets Specialty Stores |

|

Consumer Group |

Women Men Children |

|

Price Range |

Premium Mass |

|

Region |

Java Bali Sumatra Kalimantan Sulawesi |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Disposable Income

3.1.2. Expansion of E-Commerce

3.1.3. Urbanization and Changing Lifestyles

3.1.4. Influence of Social Media (Instagram, YouTube, etc.)

3.2. Market Challenges

3.2.1. High Competition from Local Brands

3.2.2. Stringent Government Regulations (BPOM Indonesia)

3.2.3. High Cost of Raw Materials (Natural Ingredients)

3.3. Opportunities

3.3.1. Growing Male Grooming Segment

3.3.2. Increasing Demand for Organic & Natural Cosmetics

3.3.3. Rising Awareness on Anti-aging Products

3.4. Trends

3.4.1. Personalization and Customization of Beauty Products

3.4.2. Surge in K-Beauty and J-Beauty Products

3.4.3. Shift Toward Sustainable and Eco-friendly Packaging

3.5. Government Regulation

3.5.1. Indonesian National Agency of Drug and Food Control (BPOM) Regulations

3.5.2. Import Tariff Policies

3.5.3. Product Labeling and Certification Standards

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Skincare

4.1.2. Haircare

4.1.3. Fragrances

4.1.4. Makeup

4.1.5. Personal Care Products

4.2. By Distribution Channel (In Value %)

4.2.1. Online Retail

4.2.2. Supermarkets/Hypermarkets

4.2.3. Specialty Stores

4.2.4. Department Stores

4.2.5. Pharmacy/Drug Stores

4.3. By Consumer Group (In Value %)

4.3.1. Women

4.3.2. Men

4.3.3. Children

4.4. By Price Range (In Value %)

4.4.1. Premium Segment

4.4.2. Mass Segment

4.5. By Region (In Value %)

4.5.1. Java

4.5.2. Bali

4.5.3. Sumatra

4.5.4. Kalimantan

4.5.5. Sulawesi

5.1. Detailed Profiles of Major Companies

5.1.1. PT Martina Berto Tbk

5.1.2. Wardah

5.1.3. Mustika Ratu

5.1.4. PZ Cussons Indonesia

5.1.5. L'Oral Indonesia

5.1.6. Unilever Indonesia

5.1.7. Procter & Gamble Indonesia

5.1.8. The Body Shop Indonesia

5.1.9. Shiseido Indonesia

5.1.10. Estee Lauder Indonesia

5.1.11. Oriflame Indonesia

5.1.12. Kao Corporation Indonesia

5.1.13. Revlon Indonesia

5.1.14. PT Kino Indonesia Tbk

5.1.15. Innisfree Indonesia

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Product Range, Revenue, Distribution Channels, Market Share, Growth Strategies, Sustainability Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. BPOM Regulatory Standards

6.2. Import Restrictions and Certifications

6.3. Certification Process for Natural and Organic Cosmetics

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By Consumer Group (In Value %)

8.4. By Price Range (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase involves mapping out all key stakeholders in the Indonesia Cosmetics Market, utilizing a combination of desk research and secondary sources such as government databases, market reports, and proprietary research. This phase is crucial in identifying the key variables that drive market dynamics, such as consumer behavior, regulatory environment, and distribution channels.

In this phase, historical data from various sources is compiled to assess market penetration, product segments, and revenue generation. The focus is on analyzing the performance of different product types and distribution channels, with an emphasis on identifying growth trends and potential areas for market expansion.

Industry experts are consulted through structured interviews to validate market hypotheses and gain firsthand insights into market trends, challenges, and opportunities. These consultations also provide valuable information on industry best practices and emerging trends, which are crucial for refining market projections.

The final step involves synthesizing all collected data into a comprehensive report. This includes analyzing the market performance of major players, consumer preferences, and product segments to ensure that the report offers a detailed and accurate representation of the Indonesia Cosmetics Market.

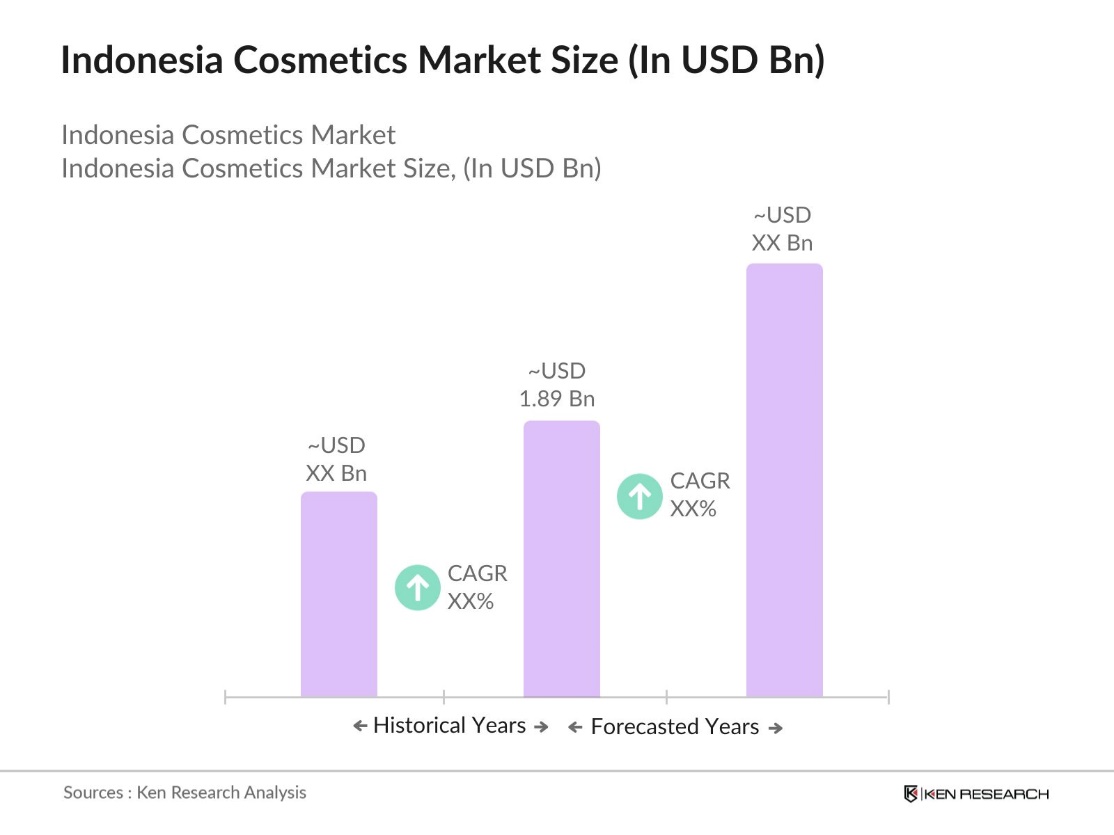

The Indonesia Cosmetics Market is valued at USD 1.89 billion, driven by increasing disposable income, a growing middle-class population, and the popularity of halal-certified products among the predominantly Muslim population.

Challenges in Indonesia Cosmetics Market include high competition from both local and international brands, regulatory hurdles related to halal certification and product registration, and the increasing cost of natural raw materials.

Key players in Indonesia Cosmetics Market include Wardah, Mustika Ratu, L'Oral Indonesia, Unilever Indonesia, and PZ Cussons Indonesia. These companies dominate due to their strong brand presence, wide distribution networks, and product innovation.

The Indonesia Cosmetics Market is driven by rising disposable incomes, increasing consumer awareness of personal care, the growth of e-commerce, and the demand for halal-certified and natural cosmetic products.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.