Indonesia Data Center Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD6435

December 2024

89

About the Report

Indonesia Data Center Market Overview

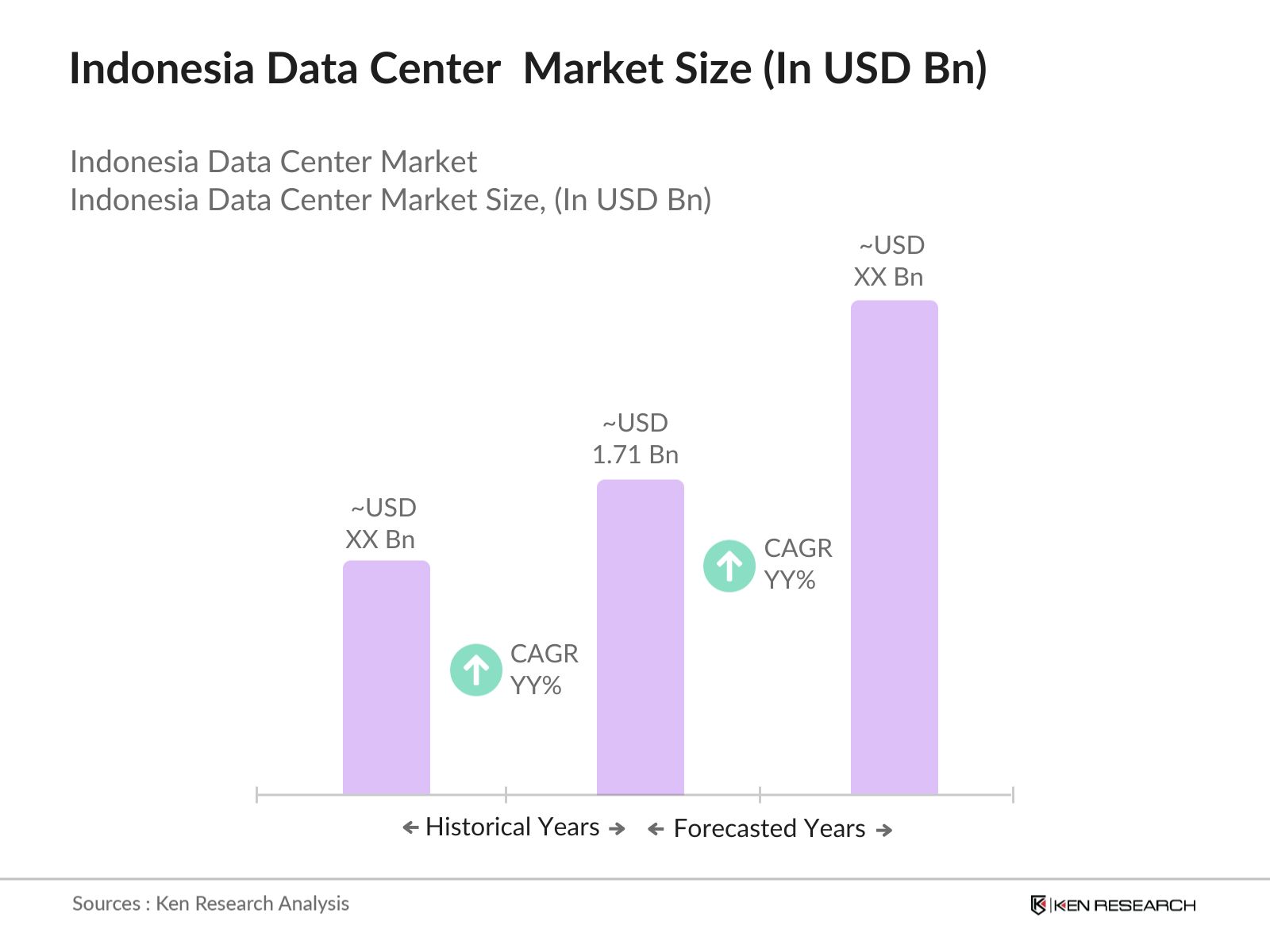

- The Indonesia data center market is valued at USD 1.71 billion, driven by the country's increasing digitalization, growing internet penetration, and expanding cloud computing services. Major infrastructural projects like the Palapa Ring and the government-backed Digital Indonesia Roadmap have played a role in advancing the digital infrastructure, contributing to the construction and expansion of data centers. Demand for data center services has surged due to the rapid adoption of cloud computing, big data, and AI-driven applications.

- Greater Jakarta remains the dominant region for data centers in Indonesia. This dominance stems from its superior infrastructure, strategic geographical location, and concentration of technology-driven companies. The availability of land, power, and network infrastructure in Greater Jakarta facilitates the establishment of Tier III and Tier IV data centers, making it the epicenter for data center growth in the country.

- The Indonesian government has laid out a comprehensive digital transformation roadmap aiming to accelerate data center development. As part of this initiative, by 2024, the government will allocate over $2 billion towards developing digital infrastructure, including data centers. The roadmap supports the growth of the tech ecosystem, including data storage, cloud services, and digital payment systems, fostering a favorable environment for data center expansion.

Indonesia Data Center Market Segmentation

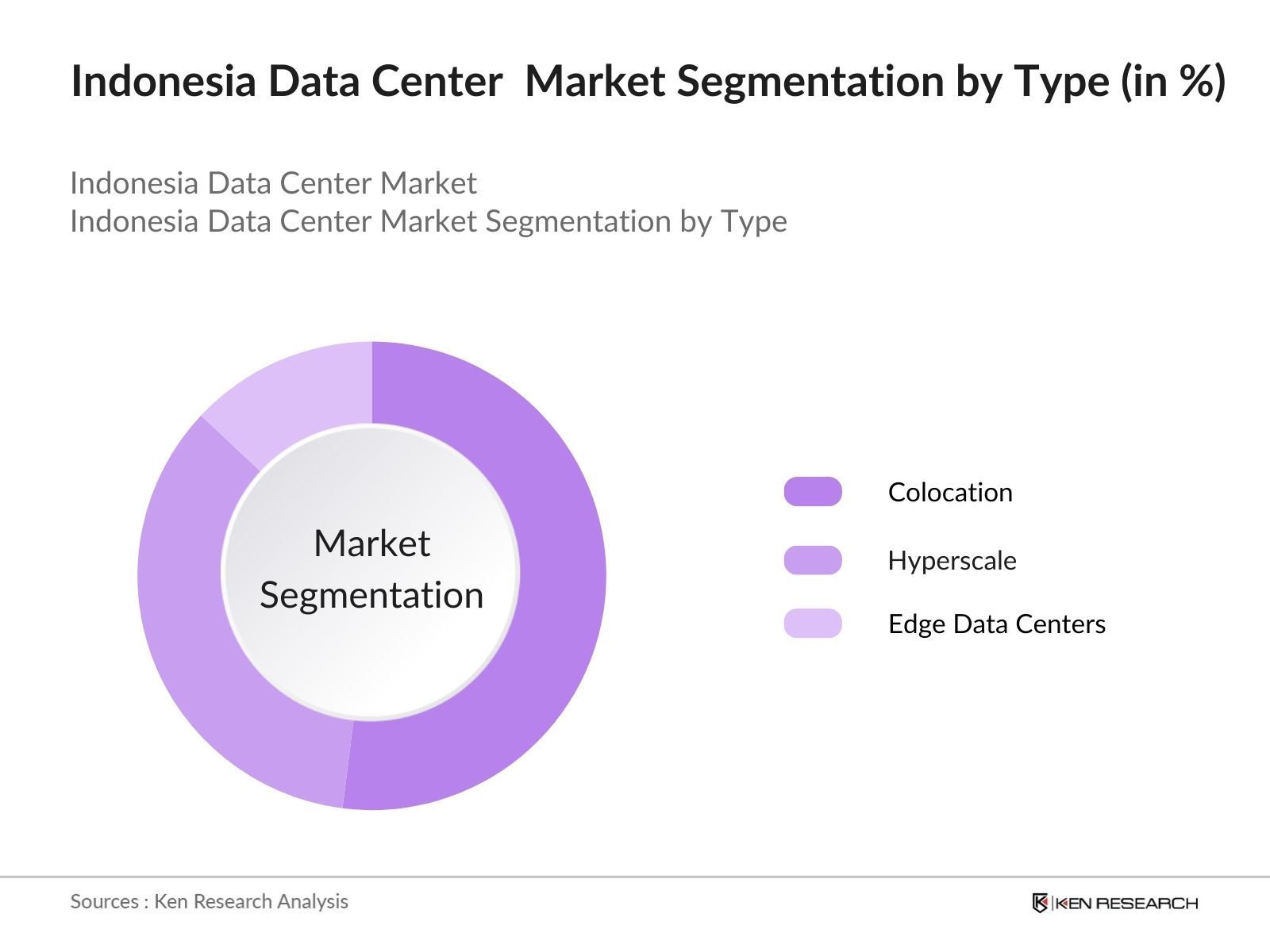

By Type: The market is segmented by type into Colocation, Hyperscale, and Edge Data Centers. Colocation services dominate the market due to the growing number of enterprises seeking cost-effective solutions for their IT infrastructure. Colocation facilities offer flexibility and scalability, attracting both local and international companies to outsource their data storage and processing needs. Hyperscale data centers are also gaining traction as cloud services and large-scale IT operations expand across the region.

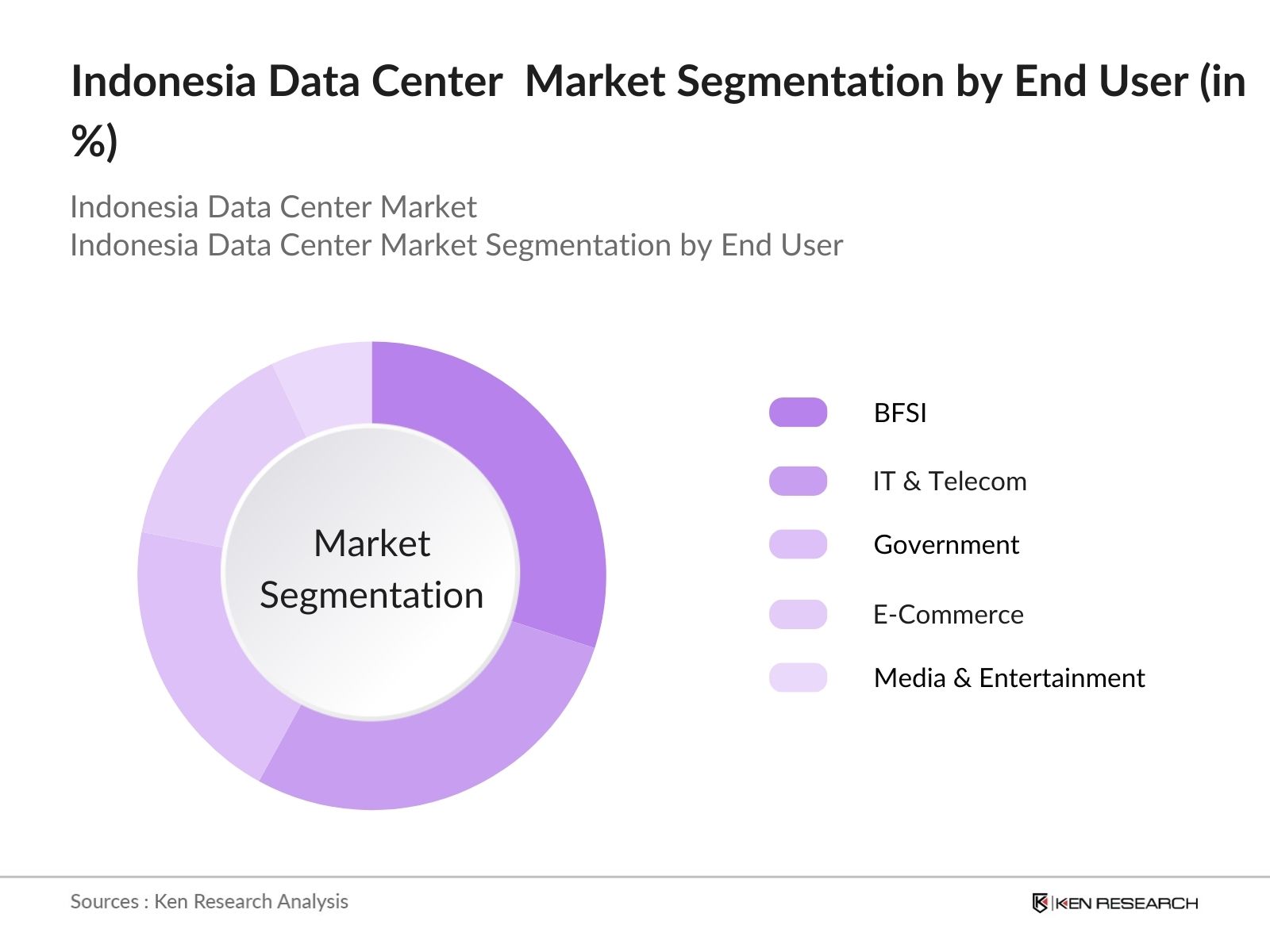

By End-User: The market is also segmented by end-user into BFSI, IT & Telecom, Government, E-Commerce, and Media & Entertainment. The BFSI sector holds the largest share, as financial institutions increasingly require secure and scalable data storage solutions for digital banking services. The IT & Telecom sector follows closely due to the rapid expansion of cloud computing and AI technologies, making Indonesia a growing hub for data processing.

Indonesia Data Center Market Competitive Landscape

The market is dominated by a mix of global and local players. The presence of multinational companies like Amazon Web Services and Alibaba Cloud has bolstered competition, driving innovation in infrastructure development.

Indonesia Data Center Market Analysis

Market Growth Drivers

- Rising Demand for Cloud Services and Data Storage: Indonesia is witnessing an increase in demand for cloud services and data storage due to the rapid expansion of its digital economy. As more businesses adopt digital platforms, the demand for data centers to support cloud services has surged. By 2024, over 200 million internet users are expected to generate enormous data flows, requiring expanded data storage capacities across the country.

- Increased Foreign Direct Investment (FDI) in Data Center Infrastructure: Indonesia's data center market is benefiting from increased foreign investments due to favorable regulations encouraging global players to enter the market. With the Indonesian government actively encouraging FDI, the country has attracted billions in investments from major players. In 2024 alone, it is estimated that foreign investments in the data center sector will exceed $2 billion.

- Regulatory Push for Data Localization: Indonesias government mandates local data storage regulations, requiring critical data to be stored within the country. This regulatory push, formalized under Government Regulation No. 71/2019, has accelerated the demand for localized data centers. In 2024, the strict enforcement of this regulation is expected to prompt businesses, including global tech firms, to build or lease local data storage facilities, driving market growth.

Market Challenges

- High Energy Costs and Sustainability Issues: Data centers are highly energy-intensive, and in Indonesia, electricity prices are among the highest in the region. In 2024, the average commercial electricity cost in Indonesia is expected to reach around IDR 1,500 per kWh, posing a significant operational challenge for data center operators.

- Limited Connectivity in Remote Areas: While major cities like Jakarta and Surabaya have well-developed digital infrastructure, other regions still suffer from limited connectivity. By 2024, more than 40% of Indonesia's population in rural areas will continue to face internet access issues, constraining the potential growth of data centers beyond urban regions.

Indonesia Data Center Market Future Outlook

The Indonesia data center industry is expected to experience robust growth over the next five years, driven by factors such as increased cloud adoption, the deployment of 5G networks, and ongoing digital transformation initiatives.

Future Market Opportunities

- Expansion of Edge Data Centers to Support 5G Rollout: Indonesia is set to experience rapid expansion in edge data centers to complement the ongoing 5G rollout, expected to be completed by 2026. By 2027, it is estimated that over 75 edge data centers will be operating across Indonesia, reducing latency and enhancing connectivity for users in both urban and rural areas. This trend will support industries such as gaming, financial services, and e-commerce, which rely heavily on low-latency services.

- Increased Focus on Green Data Centers: Over the next five years, sustainability will be a focus in Indonesia's data center market. By 2029, it is projected that 50% of new data center projects will be powered by renewable energy sources, supported by the government's initiatives to promote green energy. This shift is expected to reduce the carbon footprint of the industry by over 10 million tons annually by the end of the decade.

Scope of the Report

|

By Type |

Colocation Hyperscale Edge |

|

By Deployment Model |

On-Premise Cloud Hybrid |

|

By Enterprise Size |

Large Enterprises SMEs |

|

By End-User |

BFSI IT & Telecom Government E-Commerce Others |

|

By Region |

North East West South |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Cloud Service Providers

Data Center Operators

BFSI Industry Stakeholders

Telecommunication Companies

Government and Regulatory Bodies (Ministry of Communication and Informatics, Indonesia)

Investor and Venture Capitalist Firms

IT and Software Development Companies

Renewable Energy Solution Providers

Companies

Players Mentioned in the Report:

PT DCI Indonesia Tbk

NTT Ltd

Amazon Web Services (AWS)

Alibaba Cloud

EdgeConneX Inc.

Digital Edge (Singapore) Holdings

Space DC Pte Ltd

BDx Data Center Pte Ltd

Equinix Inc.

Princeton Digital Group

Table of Contents

Indonesia Data Center Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Key Market Trends (Cloud Adoption, AI Integration, 5G Expansion)

1.4. Market Segmentation Overview

Indonesia Data Center Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Major Market Milestones (Digital Indonesia Roadmap, Palapa Ring Project)

Indonesia Data Center Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Cloud Adoption

3.1.2. Digital Transformation Initiatives

3.1.3. AI and 5G Integration

3.1.4. Government Incentives (Digital Indonesia Roadmap)

3.2. Market Challenges

3.2.1. Power Supply Constraints

3.2.2. High Construction Costs

3.2.3. Data Privacy Regulations

3.2.4. Geographical Connectivity Issues (East Indonesia Connectivity)

3.3. Opportunities

3.3.1. Expansion into Tier-II Cities

3.3.2. Green Data Centers

3.3.3. Increased Colocation Demand

3.4. Market Trends

3.4.1. Hyperscale Data Centers Growth

3.4.2. Increased Use of Renewable Energy

3.4.3. Rising Edge Data Centers Development

3.5. Regulatory Framework

3.5.1. Data Sovereignty Laws

3.5.2. Compliance with Uptime Institute Standards

3.5.3. Government Incentives for Infrastructure Development

3.6. Stake Ecosystem

3.7. Porters Five Forces Analysis (Bargaining Power, Competitive Rivalry, New Entrants Threats)

3.8. Competition Ecosystem

Indonesia Data Center Market Segmentation

4.1. By Type (In Value %)

4.1.1. Colocation

4.1.2. Hyperscale

4.1.3. Edge Data Centers

4.2. By Deployment Model (In Value %)

4.2.1. On-Premise

4.2.2. Cloud-Based

4.2.3. Hybrid

4.3. By Enterprise Size (In Value %)

4.3.1. Large Enterprises

4.3.2. Small & Medium Enterprises (SMEs)

4.4. By End-User (In Value %)

4.4.1. BFSI

4.4.2. IT & Telecom

4.4.3. Government

4.4.4. E-Commerce

4.4.5. Others (Manufacturing, Media & Entertainment)

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. West

4.5.4. South

Indonesia Data Center Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. NTT Ltd

5.1.2. PT DCI Indonesia Tbk

5.1.3. EdgeConneX Inc.

5.1.4. PT Sigma Tata Sadaya

5.1.5. Digital Edge (Singapore) Holdings

5.1.6. Princeton Digital Group

5.1.7. Space DC Pte Ltd

5.1.8. Amazon Web Services (AWS)

5.1.9. Alibaba Cloud

5.1.10. Telkomsigma

5.1.11. PT Faasri Utama Sakti

5.1.12. BDx Data Center Pte Ltd

5.1.13. Indosat Ooredoo Hutchison

5.1.14. Google Cloud

5.1.15. Equinix

5.2. Cross Comparison Parameters (Employee Count, Revenue, Headquarters, Year of Inception)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Acquisitions, Partnerships)

5.5. Investment Analysis (Private Equity, Venture Capital)

5.6. Mergers & Acquisitions

5.7. Government Grants and Incentives

Indonesia Data Center Future Market Size (In USD Bn)

6.1. Future Market Size Projections

6.2. Key Drivers of Future Growth

Indonesia Data Center Future Market Segmentation

7.1. By Type (In Value %)

7.2. By Deployment Model (In Value %)

7.3. By Enterprise Size (In Value %)

7.4. By End-User (In Value %)

7.5. By Region (In Value %)

Indonesia Data Center Market Analyst Recommendations

8.1. TAM/SAM/SOM Analysis

8.2. Customer Cohort Analysis

8.3. Go-to-Market Strategy

8.4. White Space Opportunities

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first phase involves mapping key stakeholders in the Indonesia data center market, identifying critical components like data center operators, energy providers, and IT service companies. This process includes a thorough analysis of existing market conditions using secondary data from legitimate sources and proprietary databases.

Step 2: Market Analysis and Construction

In this stage, historical data and market penetration levels are analyzed. The process includes reviewing data center capacities, service levels, and revenue generation across different regions in Indonesia. This analysis helps in understanding market dynamics and overall growth patterns.

Step 3: Hypothesis Validation and Expert Consultation

This phase involves validating hypotheses with insights from industry experts. Key professionals from major data center operators and technology companies are consulted to gain practical insights into operational efficiencies, infrastructure challenges, and future growth projections.

Step 4: Research Synthesis and Final Output

In the final phase, comprehensive data from both primary and secondary sources are synthesized. Detailed insights are drawn from consultations with experts and industry stakeholders, ensuring the final output is accurate and reflects the real-time market landscape.

Frequently Asked Questions

01. How big is the Indonesia Data Center Market?

The Indonesia data center market is valued at USD 1.71 billion, driven by the growing need for digital infrastructure and the rise of cloud services.

02. What are the challenges in the Indonesia Data Center Market?

Challenges in the Indonesia data center market include power supply constraints, high construction costs, and regulatory hurdles regarding data privacy and sovereignty, impacting the scalability of data centers.

03. Who are the major players in the Indonesia Data Center Market?

Major players in the Indonesia data center market include PT DCI Indonesia Tbk, NTT Ltd, Amazon Web Services (AWS), Alibaba Cloud, and EdgeConneX Inc., all of which have made significant investments in the region's infrastructure.

04. What are the growth drivers of the Indonesia Data Center Market?

Growth drivers in the Indonesia data center market include increased cloud adoption, government-backed digital transformation projects, and advancements in AI and 5G technologies.

05. Which regions dominate the Indonesia Data Center Market?

Greater Jakarta dominates the Indonesia data center market due to its advanced infrastructure, availability of power, and concentration of tech companies, making it the prime location for data center expansion.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.