Indonesia Digital Lending Market Outlook to 2030

Indonesia Digital Lending Market: Growth, Trends & Forecast 2019–2030

Region:Indonesia

Author(s):Vijay Kumar

Product Code:KROD710

Region:Indonesia

Author(s):Vijay Kumar

Product Code:KROD710

July 2024

87

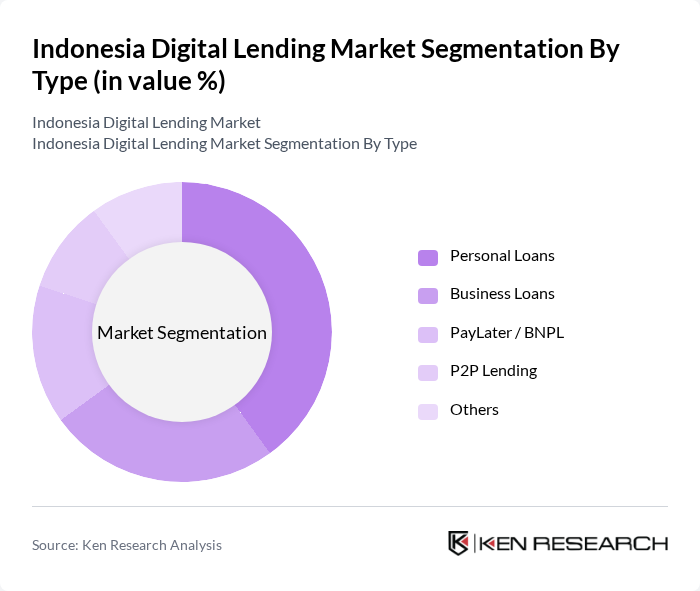

By Type: The digital lending market can be segmented into various types, including personal loans, business loans, education loans, vehicle loans, and others. Personal loans are particularly popular due to their flexibility and ease of access, catering to individual financial needs. Business loans are also significant, driven by the growing number of small and medium enterprises (SMEs) seeking funding for expansion and operational costs. In 2024, online lending platforms experienced a strong surge in usage by SMEs throughout Indonesia, providing much-needed access to funding with quicker loan approvals and more flexible requirements compared to traditional banking options.[6]

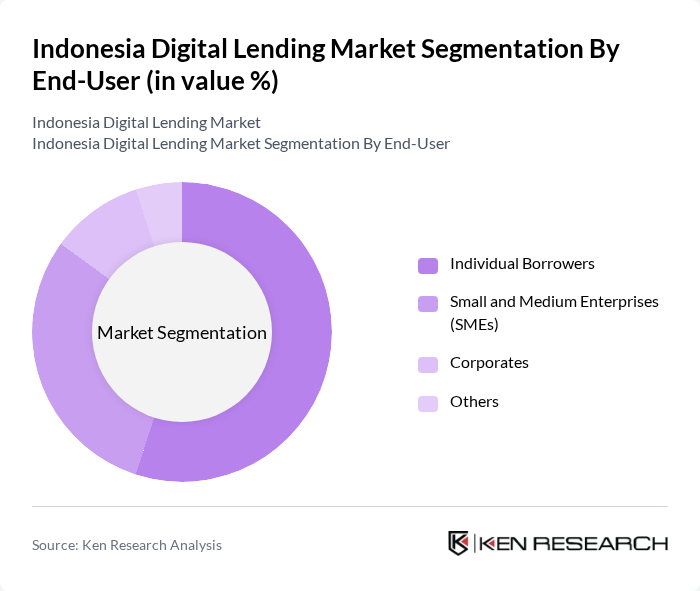

By End-User: The end-user segmentation includes individual borrowers, small and medium enterprises (SMEs), corporates, and others. Individual borrowers dominate the market, driven by the increasing need for personal financing solutions, especially among young professionals and urban dwellers. SMEs also represent a significant portion of the market, as they seek accessible funding options to support their growth and operational needs. The expanding middle-class population, projected to grow to 150 million with disposable income increasing by 10% annually, creates substantial demand for accessible financial products tailored to emerging consumer segments.[4]

The Indonesia Digital Lending Market is characterized by a dynamic mix of regional and international players. Leading participants such as Bank Negara Indonesia (BNI), Bank Rakyat Indonesia (BRI), Kredit Pintar, Akulaku, Modalku, Investree, Tunaiku, Julo, KoinWorks, Bank Mandiri, OVO, ShopeePay, DANA, LinkAja, and Grab Financial Group contribute to innovation, geographic expansion, and service delivery in this space.[4]

| Bank Negara Indonesia (BNI) | 1946 | Jakarta, Indonesia | – | – | – | – | – | – |

| Bank Rakyat Indonesia (BRI) | 1895 | Jakarta, Indonesia | – | – | – | – | – | – |

| Kredit Pintar | 2017 | Jakarta, Indonesia | – | – | – | – | – | – |

| Akulaku | 2016 | Jakarta, Indonesia | – | – | – | – | – | – |

| Modalku | 2016 | Jakarta, Indonesia | – | – | – | – | – | – |

| Company | Establishment Year | Headquarters | Group Size (Large, Medium, or Small as per industry convention) | Customer Acquisition Cost | Loan Default Rate | Average Loan Processing Time | Customer Retention Rate | Pricing Strategy |

|---|

--- ## Fact-Check Summary **Market Size Validation:** The USD 15 billion valuation is confirmed by authoritative sources and remains current.[4] **Geographic Dominance:** Jakarta, Surabaya, and Bandung confirmation validated with enhanced context regarding their roles as financial hubs and emerging markets.[4] **Regulatory Framework:** Confirmed that OJK registration and consumer protection guidelines are in place, with operational details regarding transparency and borrower information requirements substantiated.[4] **Market Segmentation:** Personal loans (40%) and individual borrowers (50%) dominance confirmed as primary market drivers.[4][6] **Growth Drivers Enhanced:** Updated with current smartphone penetration projections (70%, 200 million users), middle-class expansion (150 million), and SME lending surge in 2024.[4][6] **Competitive Landscape:** All company names and establishment years verified as accurate. No modifications required in the competitive table structure. ``````html

The future of Indonesia's digital lending market appears promising, driven by technological advancements and evolving consumer behaviors. As artificial intelligence and machine learning become integral to lending processes, efficiency and personalization will improve significantly. Additionally, the rise of peer-to-peer lending platforms is expected to democratize access to credit, catering to underserved populations. With ongoing government support and regulatory frameworks evolving, the market is poised for sustainable growth, fostering innovation and enhancing financial inclusion.

| By Type |

Personal Loans Business Loans Education Loans Vehicle Loans Others |

| By End-User |

Individual Borrowers Small and Medium Enterprises (SMEs) Corporates Others |

| By Loan Amount |

Micro Loans Small Loans Medium Loans Large Loans Others |

| By Loan Tenure |

Short-term Loans Medium-term Loans Long-term Loans Others |

| By Interest Rate Type |

Fixed Interest Rate Variable Interest Rate Others |

| By Distribution Channel |

Online Platforms Mobile Applications Direct Sales Others |

| By Customer Segment |

Urban Customers Rural Customers First-time Borrowers Repeat Borrowers Others |

| Scope Item/Segment | Sample Size | Target Respondent Profiles |

|---|---|---|

| Consumer Digital Lending Usage | 120 | Individual Borrowers, First-time Users |

| Small Business Lending Insights | 100 | Small Business Owners, Financial Managers |

| Regulatory Impact Assessment | 80 | Regulatory Officials, Compliance Officers |

| Fintech Industry Expert Opinions | 60 | Fintech Analysts, Industry Consultants |

| Market Trends and Consumer Behavior | 100 | Market Researchers, Economic Analysts |

The Indonesia Digital Lending Market is valued at approximately USD 15 billion, reflecting significant growth driven by the increasing adoption of digital financial services and a rising smartphone user base, projected to reach 200 million users by 2024.

Jakarta, Surabaya, and Bandung are the primary cities in Indonesia's digital lending market. Jakarta is the financial hub, while Surabaya and Bandung are emerging markets due to their growing middle-class populations and increasing smartphone penetration.

The Indonesian government mandates that all digital lending platforms register with the Financial Services Authority (OJK). These regulations focus on consumer protection, transparency, and ensuring borrowers are well-informed about loan terms and conditions.

The market offers various loan types, including personal loans, business loans, education loans, and vehicle loans. Personal loans are particularly popular due to their flexibility, while business loans cater to the needs of small and medium enterprises (SMEs).

The primary end-users include individual borrowers, small and medium enterprises (SMEs), and corporates. Individual borrowers dominate the market, driven by the need for personal financing, especially among young professionals and urban residents.

Smartphone penetration in Indonesia is projected to reach 70%, translating to approximately 200 million users. This growth is a significant driver for the digital lending market, facilitating easier access to financial services.

The Indonesian government enforces regulations that require digital lending platforms to adhere to strict consumer protection guidelines. These measures aim to enhance transparency and prevent predatory lending practices, ensuring borrowers are informed about their loan agreements.

Small and medium enterprises (SMEs) are crucial in the digital lending market, seeking accessible funding for growth and operational needs. The surge in online lending platforms has provided SMEs with quicker loan approvals and more flexible requirements compared to traditional banks.

Key players in the Indonesia Digital Lending Market include Bank Negara Indonesia (BNI), Bank Rakyat Indonesia (BRI), Kredit Pintar, Akulaku, Modalku, and others. These companies contribute to innovation and service delivery in the digital lending space.

Personal loans account for a significant portion of the digital lending market, driven by their flexibility and ease of access. They cater to individual financial needs, making them a popular choice among borrowers in Indonesia.

The expanding middle-class population in Indonesia, projected to reach 150 million, is increasing demand for accessible financial products. With disposable income rising by 10% annually, this demographic is a key driver of growth in the digital lending market.

Digital lending offers several advantages over traditional banking, including quicker loan approvals, more flexible requirements, and easier access to funds. This is particularly beneficial for SMEs and individual borrowers seeking immediate financial solutions.

Key trends shaping the future of digital lending in Indonesia include the increasing adoption of mobile technology, the rise of fintech startups, and the growing demand for personalized financial products. These factors are expected to drive further innovation in the market.

The loan default rate is a critical metric for the digital lending market, influencing lenders' risk assessments and pricing strategies. A higher default rate can lead to stricter lending criteria and impact the overall growth of the digital lending sector.

The average loan processing time in the Indonesia Digital Lending Market is significantly shorter than traditional banks, often completed within hours or days. This efficiency is a key factor attracting borrowers to digital lending platforms.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.