Indonesia E-Health Market Outlook to 2030

Region:Global

Author(s):Shambhavi

Product Code:KROD4661

Region:Global

Author(s):Shambhavi

Product Code:KROD4661

December 2024

80

Listen to the audio summary

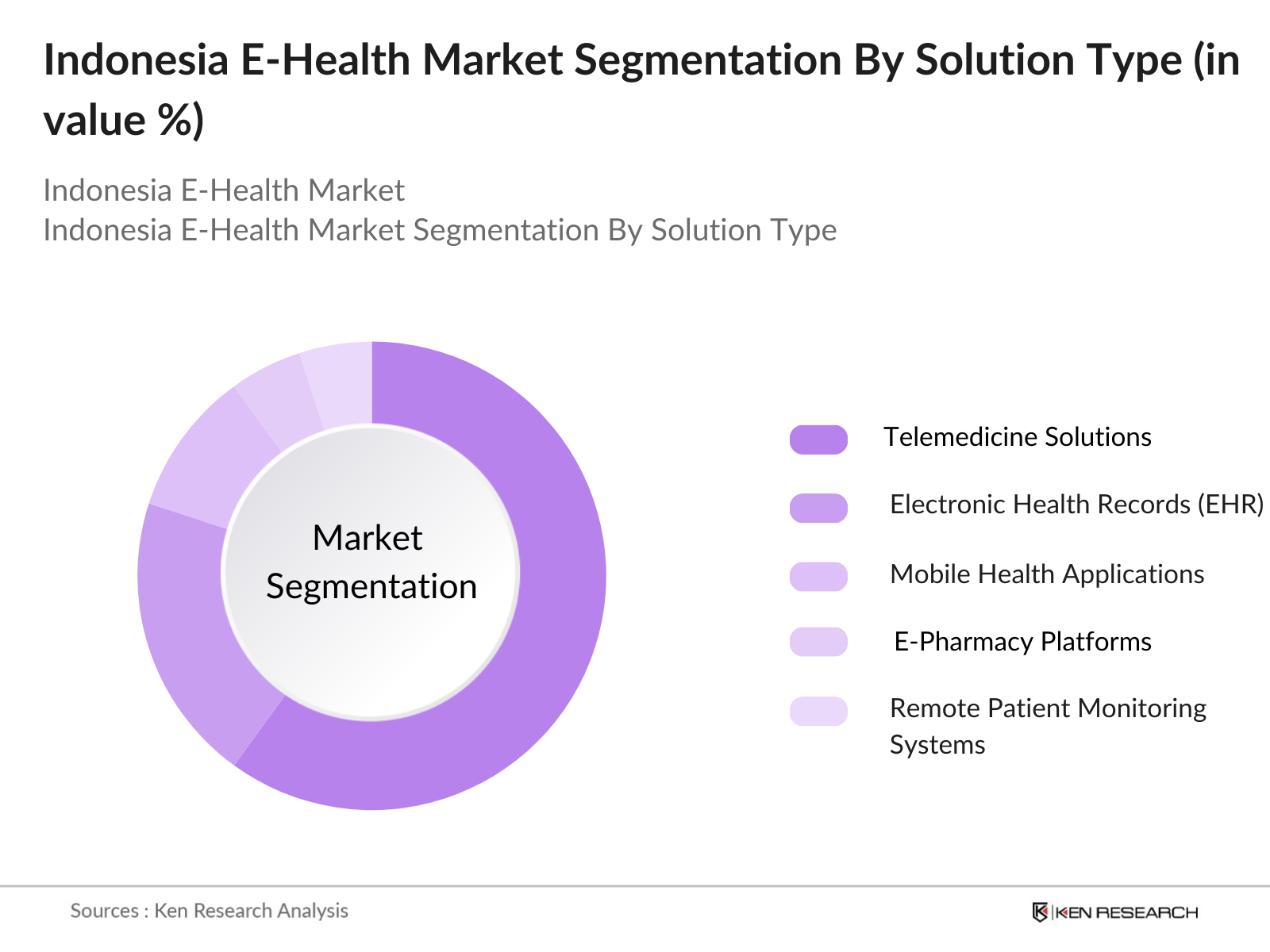

By Solution Type: The Indonesia E-Health market is segmented by solution type into Telemedicine Solutions, Electronic Health Records (EHR), Mobile Health Applications, E-Pharmacy Platforms, and Remote Patient Monitoring Systems. Among these, Telemedicine Solutions hold a dominant market share. This dominance is attributed to the country's geographical fragmentation, which makes remote healthcare solutions particularly valuable. Telemedicine platforms such as Halodoc and Alodokter have experienced rapid growth due to their convenience and cost-effectiveness, allowing patients to consult with healthcare professionals via video calls, minimizing travel time and costs, particularly in remote areas.

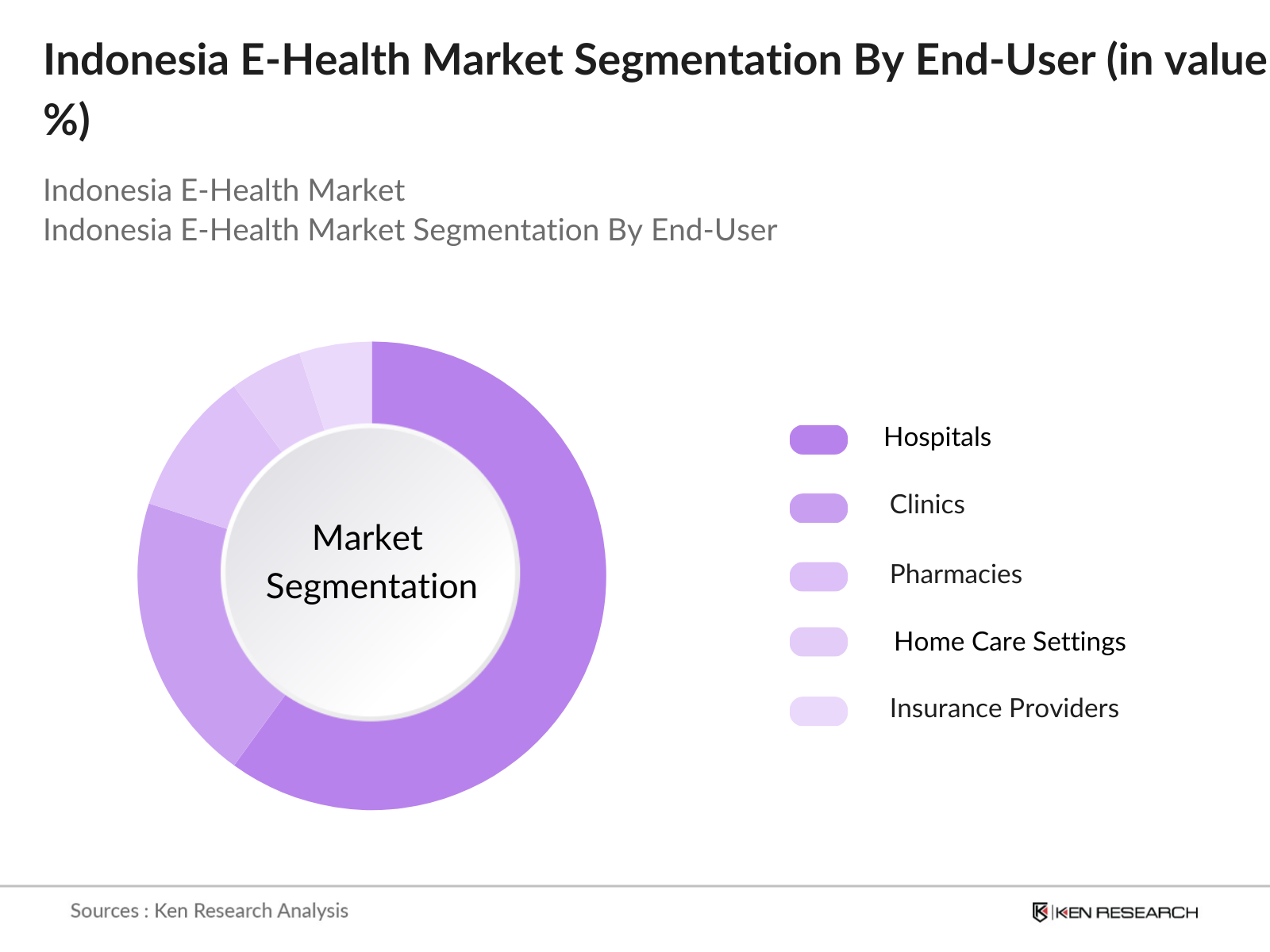

By End-User: The market is also segmented by end-users, which include Hospitals, Clinics, Pharmacies, Home Care Settings, and Insurance Providers. Hospitals currently dominate the end-user segment of the Indonesia E-Health market, largely due to their widespread adoption of comprehensive EHR systems and telemedicine platforms. Ma ny hospitals are integrating digital solutions to streamline patient data management, diagnostics, and treatment processes, contributing to improved efficiency and patient outcomes. The rising number of private hospitals adopting advanced digital tools further strengthens this segment's dominance.

The Indonesia E-Health market is dominated by both local and international players. Major companies like Halodoc and Alodokter have gained significant traction by providing telemedicine and mobile health services, while other players focus on EHR and remote monitoring technologies. The competitive landscape is shaped by technological innovations, partnerships with healthcare providers, and government backing.

The competitive landscape shows that the top players not only focus on digital health services but also leverage partnerships with hospitals, pharmacies, and the government to gain a competitive edge. Many players are increasing their regional footprints and are aggressively expanding their customer base.

Growth Drivers

Market Challenges

The Indonesia E-Health market is expected to experience sustained growth over the next five years, driven by continuous investments in digital health infrastructure, the expansion of 4G/5G networks, and the growing demand for remote healthcare services. The governments push for universal healthcare through initiatives such as Jaminan Kesehatan Nasional (JKN) is also expected to boost the adoption of E-health solutions, as more citizens become aware of and gain access to telemedicine and EHR platforms. The rise of AI and machine learning in healthcare diagnostics, alongside the integration of IoT devices, will further enhance the capabilities of digital health solutions, allowing for real-time patient monitoring and predictive diagnostics. Additionally, e-pharmacy platforms are likely to see increased adoption as digital literacy improves and e-commerce continues to thrive in the region.

Market Opportunities

|

By Solution Type |

E-Prescriptions |

|

Telemedicine Solutions |

|

|

EHR/EMR Solutions |

|

|

Mobile Health Apps |

|

|

E-Pharmacy Platforms |

|

|

By End-User |

Hospitals |

|

Clinics |

|

|

Home Care Settings |

|

|

Pharmacies |

|

|

By Deployment Mode |

On-Premise Solutions |

|

Cloud-Based Solutions |

|

|

By Technology |

AI and Machine Learning |

|

Blockchain |

|

|

Internet of Medical Things (IoMT) |

|

|

Big Data Analytics |

|

|

By Region |

Java |

|

Sumatra |

|

|

Sulawesi |

|

|

Kalimantan |

|

|

Bali and Nusa Tenggara |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Government Initiatives (Indonesia's National Health Insurance Program)

3.1.2. Increasing Adoption of Telemedicine (Regulations on Telemedicine Usage)

3.1.3. Growing Internet Penetration (ICT Infrastructure Improvements)

3.1.4. Rising Demand for Remote Patient Monitoring (Increased Chronic Disease Burden)

3.2. Market Challenges

3.2.1. Data Privacy Concerns (Compliance with Data Protection Regulations)

3.2.2. Limited Digital Literacy (Challenges in Adoption of Digital Health Solutions)

3.2.3. Infrastructure Gaps in Rural Areas (Limited Access to High-Speed Internet)

3.3. Opportunities

3.3.1. Integration with AI and Machine Learning (AI-driven Diagnostic Tools)

3.3.2. Expansion of E-Pharmacy Platforms (Ease of Access to Medications)

3.3.3. Development of Mobile Health Apps (Increased Smartphone Usage)

3.4. Trends

3.4.1. Adoption of Cloud-Based E-Health Solutions (Cloud-Based Health Records Management)

3.4.2. Rise in Wearable Health Devices (IoT Integration in Wearables)

3.4.3. Increase in Digital Therapeutics (Regulatory Push for Digital Health Solutions)

3.5. Government Regulation

3.5.1. National E-Health Strategy (Indonesia's Digital Health Roadmap)

3.5.2. Telemedicine Regulation (MOH's Telemedicine Guidelines)

3.5.3. Patient Data Protection Law (Regulations on Health Data Security)

3.5.4. E-Pharmacy Legal Framework (E-Pharmacy Licensing Requirements)

3.6. SWOT Analysis

3.7. Stake Ecosystem (Role of Hospitals, Insurers, Tech Firms in the E-Health Ecosystem)

3.8. Porters Five Forces (Impact of Suppliers, Buyers, New Entrants, Substitutes, Rivalry)

3.9. Competition Ecosystem

4.1. By Solution Type (In Value %)

4.1.1. E-Prescriptions

4.1.2. Telemedicine Solutions

4.1.3. EHR/EMR Solutions

4.1.4. Mobile Health Apps

4.1.5. E-Pharmacy Platforms

4.2. By End-User (In Value %)

4.2.1. Hospitals

4.2.2. Clinics

4.2.3. Home Care Settings

4.2.4. Pharmacies

4.3. By Deployment Mode (In Value %)

4.3.1. On-Premise Solutions

4.3.2. Cloud-Based Solutions

4.4. By Technology (In Value %)

4.4.1. AI and Machine Learning

4.4.2. Blockchain

4.4.3. Internet of Medical Things (IoMT)

4.4.4. Big Data Analytics

4.5. By Region (In Value %)

4.5.1. Java

4.5.2. Sumatra

4.5.3. Sulawesi

4.5.4. Kalimantan

4.5.5. Bali and Nusa Tenggara

5.1. Detailed Profiles of Major Companies

5.1.1. Telkom Indonesia

5.1.2. Halodoc

5.1.3. Alodokter

5.1.4. GrabHealth

5.1.5. GoDok

5.1.6. Good Doctor Technology

5.1.7. Siloam Hospitals

5.1.8. Omni Hospitals

5.1.9. SehatQ

5.1.10. KlikDokter

5.1.11. Konsula

5.1.12. Zenius Health

5.1.13. ProSehat

5.1.14. Indonesia Medika

5.1.15. DokterSehat

5.2. Cross Comparison Parameters (Market Share, Technology Stack, Services Offered, Revenue Models, Regional Presence, Customer Base, Digital Maturity, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Mergers & Acquisitions, New Product Launches, Collaborations)

5.5. Investment Analysis (Venture Capital Investments, Private Equity Investments)

5.6. Government Grants and Funding

6.1. Health Data Privacy Standards (Personal Data Protection Act)

6.2. Compliance Requirements (Ministry of Health's Guidelines)

6.3. Certification Processes (Medical Device Licensing for E-Health Platforms)

7.1. TAM/SAM/SOM Analysis

7.2. Go-to-Market Strategies

7.3. Customer Targeting Strategies

7.4. Innovation White Spaces

In this stage, we map the ecosystem of the Indonesia E-Health market, identifying major stakeholders, including health service providers, digital platforms, and regulatory bodies. Extensive desk research is conducted to gather relevant data from secondary sources such as industry reports and governmental databases.

We analyze historical data and compile market insights related to e-health platform penetration, user adoption, and service provider data. This involves an examination of service usage patterns and the overall efficiency of digital health solutions in Indonesia.

Market hypotheses are validated through expert consultations, including interviews with key players in the E-health and telemedicine fields. This feedback refines our market forecasts and provides operational insights into digital health services.

We finalize the report by cross-referencing the gathered data with industry feedback. Detailed insights on product segments, consumer behavior, and future market trends are provided to offer a comprehensive analysis of the Indonesia E-Health market.

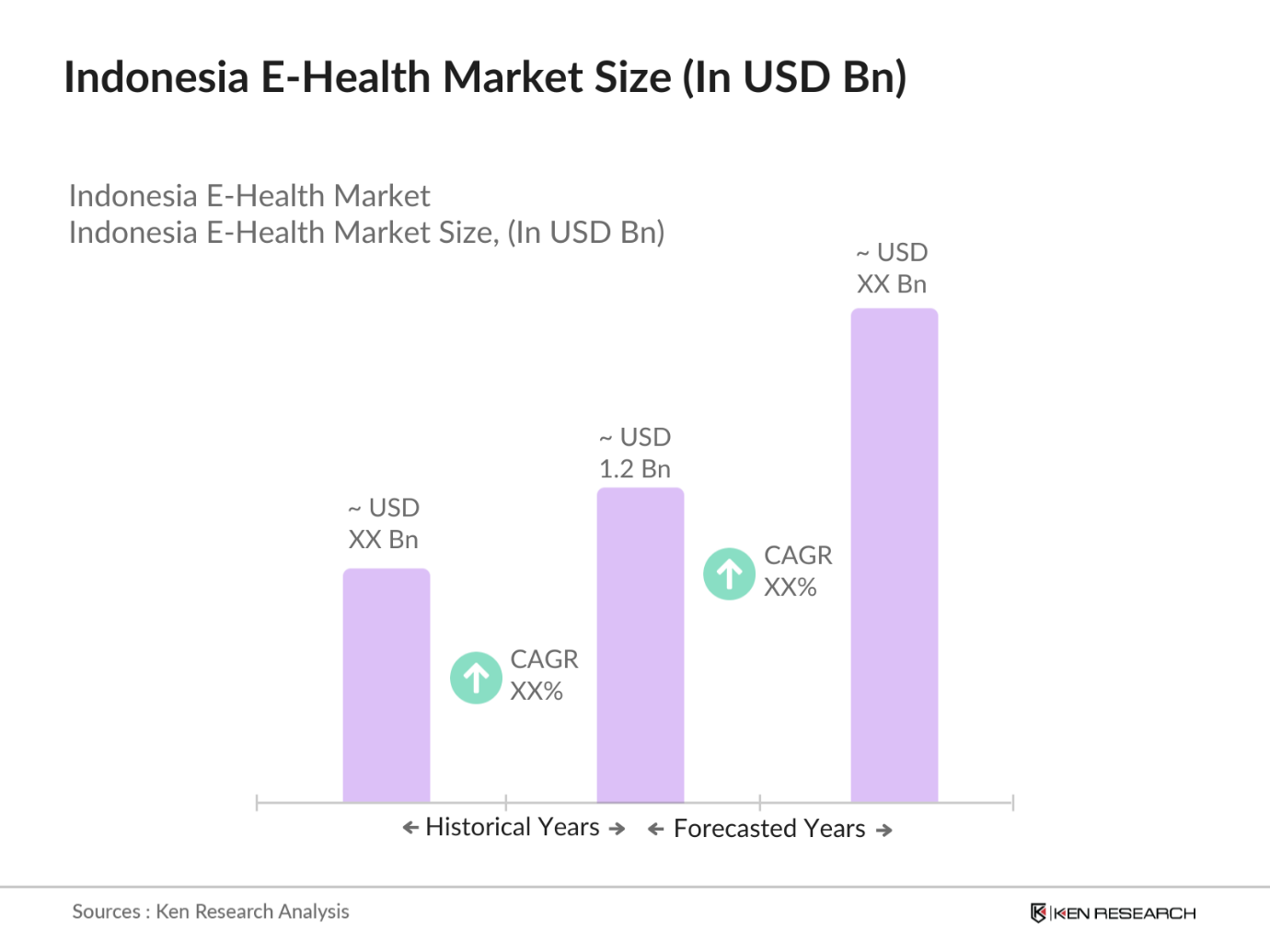

The Indonesia E-Health market was valued at USD 1.2 billion, driven by rising demand for telemedicine solutions, electronic health records, and mobile health applications.

Challenges in the market include limited digital literacy in rural areas, data privacy concerns, and infrastructure gaps that hinder the adoption of advanced digital health technologies.

Key players include Halodoc, Alodokter, Siloam Hospitals, ProSehat, and Good Doctor Technology, each leveraging technology and partnerships to lead the market.

Growth is driven by government initiatives such as JKN, the increasing penetration of smartphones, and the rising popularity of telemedicine platforms across the country.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.