Indonesia Lamps & Lighting Market Outlook to 2030

Region:Indonesia

Author(s):Yogita Sahu

Product Code:KROD3861

Region:Indonesia

Author(s):Yogita Sahu

Product Code:KROD3861

October 2024

88

By Product Type: The market is segmented by product type into LED lamps, fluorescent lamps, incandescent bulbs, solar lamps, and smart lighting systems. Recently, LED lamps hold a dominant market share in Indonesia under the product type segmentation. The main reason for the dominance of LED lighting is the Indonesian government's energy efficiency policies, which promote the transition from traditional lighting to more energy-efficient LED alternatives.

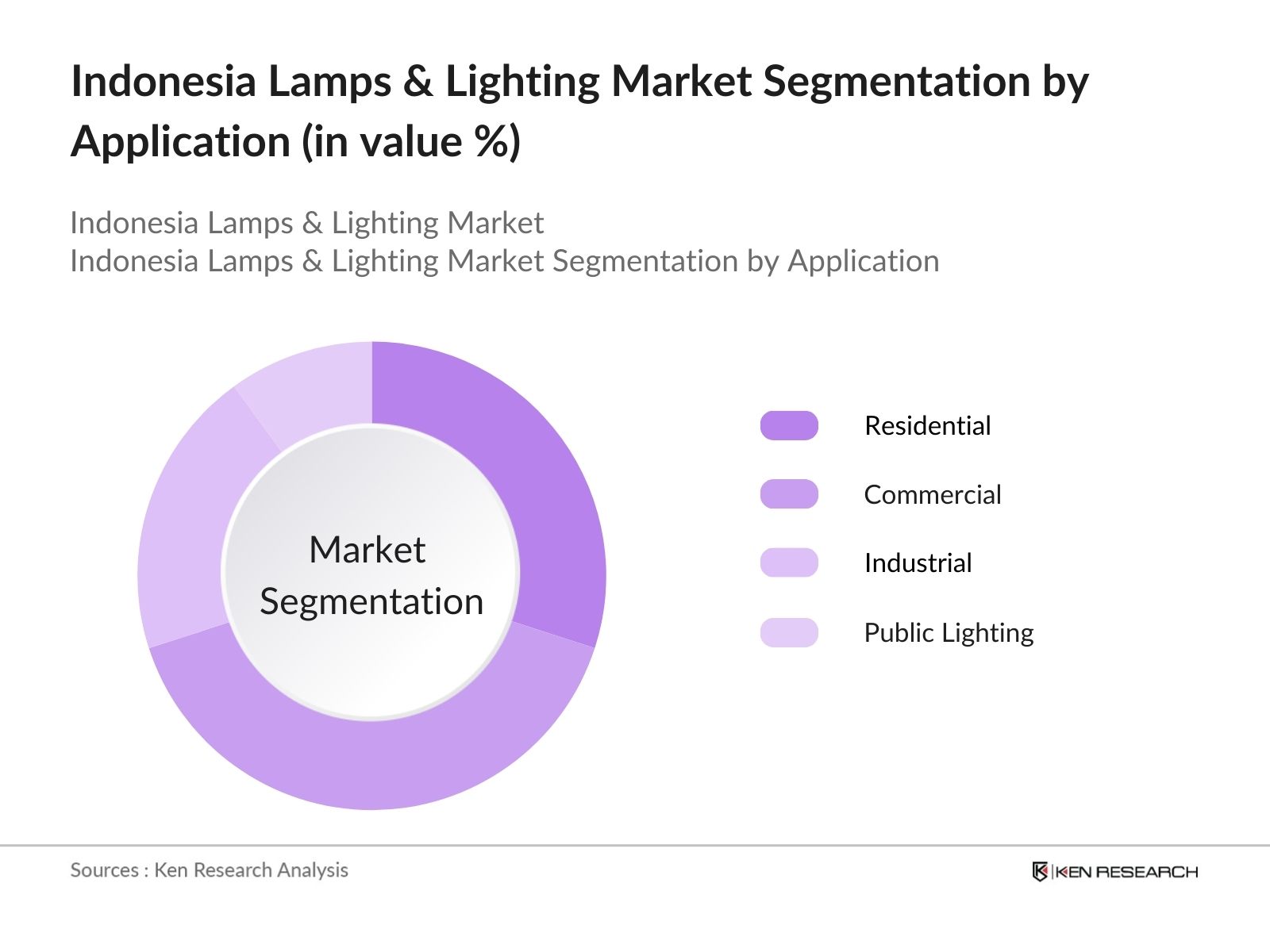

By Application: The market is also segmented by application into residential, commercial, industrial, and public lighting. The commercial sector currently leads the market under the application segmentation, accounting for a substantial portion of the demand. The rise in commercial projects, such as shopping malls, office spaces, and hotels, has escalated the need for innovative and energy-saving lighting solutions.

The market is dominated by several key players, both domestic and international. These companies have established their dominance through technological innovations, partnerships with the Indonesian government, and a wide product portfolio that caters to both energy efficiency and aesthetic design needs.

|

Company Name |

Establishment Year |

Headquarters |

Key Products |

Technology Focus |

No. of Employees |

Revenue |

Distribution Channels |

|

Philips Lighting Indonesia |

1891 |

Jakarta, Indonesia |

|||||

|

Osram Indonesia |

1919 |

Surabaya, Indonesia |

|||||

|

Panasonic Lighting Indonesia |

1935 |

Bandung, Indonesia |

|||||

|

Schneider Electric Indonesia |

1836 |

Jakarta, Indonesia |

|||||

|

GE Lighting Indonesia |

1878 |

Jakarta, Indonesia |

Over the next five years, the Indonesia lamps and lighting industry is expected to grow, driven by continuous government support for energy efficiency and the growing adoption of smart lighting solutions. The shift toward renewable energy sources, such as solar-powered lighting systems, will further drive market expansion, particularly in the public lighting and industrial segments.

|

Product Type |

LED Lamps |

|

Fluorescent Lamps |

|

|

Incandescent Bulbs |

|

|

Solar Lamps |

|

|

Smart Lighting Systems |

|

|

Application |

Residential |

|

Commercial |

|

|

Industrial |

|

|

Public Lighting |

|

|

Technology |

Smart Lighting |

|

Conventional Lighting |

|

|

Sensor-based Lighting |

|

|

Sales Channel |

Offline Distribution Channels (Retailers, Wholesalers) |

|

Online Distribution Channels (E-commerce, Marketplaces) |

|

|

Region |

North |

|

East |

|

|

West |

|

|

South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Government Investment in Infrastructure (Public Works and Housing Ministry's Initiatives)

3.1.2. Growing Urbanization and Smart City Projects (National Urban Policy)

3.1.3. Rising Demand for Energy-Efficient Lighting (Energy-Saving Regulation No. 2)

3.1.4. Increased Adoption of LED Lighting (Peraturan Pemerintah No. 70 on Energy Efficiency)

3.2. Market Challenges

3.2.1. High Import Dependency on Lighting Components (Market Structure Challenges)

3.2.2. Lack of Local Manufacturing Capabilities (Supply Chain Constraints)

3.2.3. Regulatory and Certification Barriers (SNI Certification Requirements)

3.3. Opportunities

3.3.1. Expansion of Commercial Construction Projects (High-rise & Retail Developments)

3.3.2. Technological Innovation in Smart Lighting Systems (IoT Integration in Lighting)

3.3.3. Export Opportunities to Neighboring Southeast Asian Markets (AFTA Benefits)

3.4. Trends

3.4.1. Adoption of Smart City Lighting Solutions (Jakarta Smart City Initiatives)

3.4.2. Growing Popularity of Solar-Powered Outdoor Lighting (National Energy Strategy)

3.4.3. Integration of Sensor-Based Lighting in Buildings (Automated Control Systems)

3.5. Government Regulation

3.5.1. Energy Efficiency Standards for Lighting (Government Regulation No. 79/2014)

3.5.2. Import Tariffs and Duties on Lighting Components

3.5.3. SNI Certification and Compliance Requirements for LED Products

3.6. SWOT Analysis (Lamps & Lighting Market)

3.7. Stake Ecosystem

3.8. Porters Five Forces Analysis (Lighting Market in Indonesia)

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. LED Lamps

4.1.2. Fluorescent Lamps

4.1.3. Incandescent Bulbs

4.1.4. Solar Lamps

4.1.5. Smart Lighting Systems

4.2. By Application (In Value %)

4.2.1. Residential

4.2.2. Commercial

4.2.3. Industrial

4.2.4. Public Lighting

4.3. By Technology (In Value %)

4.3.1. Smart Lighting

4.3.2. Conventional Lighting

4.3.3. Sensor-based Lighting

4.4. By Sales Channel (In Value %)

4.4.1. Offline Distribution Channels (Retailers, Wholesalers)

4.4.2. Online Distribution Channels (E-commerce, Marketplaces)

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. West

4.5.4. South

5.1. Detailed Profiles of Major Companies

5.1.1. Philips Lighting Indonesia

5.1.2. Panasonic Lighting Indonesia

5.1.3. Osram Indonesia

5.1.4. Schneider Electric Indonesia

5.1.5. Panasonic Gobel Eco Solutions

5.1.6. PT Supreme Cable Manufacturing & Commerce

5.1.7. Lutron Electronics

5.1.8. Fagerhult Indonesia

5.1.9. GE Lighting Indonesia

5.1.10. Legrand Indonesia

5.1.11. Thorn Lighting

5.1.12. PT Surya Citra Teknologi

5.1.13. PT Sinar Angkasa Rungkut

5.1.14. PT Sarana Griya Optima

5.1.15. Havells Indonesia

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Product Portfolio, Revenue)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Product Launches)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Foreign Direct Investment, Local Investments)

5.7. Venture Capital Funding

5.8. Government Grants and Incentives

6.1. Energy-Efficiency Policies

6.2. Import Restrictions and Tariffs

6.3. Compliance and Certification Standards (SNI for Lighting Products)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Sales Channel (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Segmentation Analysis

9.3. Strategic Marketing Recommendations

9.4. White Space Opportunity Analysis

The first phase involves constructing an ecosystem map that includes all the major stakeholders within the Indonesia lamps and lighting market. This is done through extensive desk research, leveraging secondary sources and proprietary databases to collect comprehensive industry-level data. The goal here is to define and identify the critical variables influencing market growth.

During this stage, historical data related to the lamps and lighting market in Indonesia is compiled and analyzed. Factors like market penetration, ratio of suppliers to consumers, and revenue growth are thoroughly evaluated. This assessment ensures the accuracy of the revenue estimates and provides insight into service quality statistics.

In this phase, market hypotheses are formulated and validated through expert consultations. These insights are gathered through structured interviews with lighting industry specialists and representatives from major companies. The insights derived from these consultations serve to refine and confirm the market data.

The final stage involves synthesizing the data collected from various sources. By engaging directly with manufacturers and distributors, detailed information is gathered on product categories, consumer preferences, and sales performance. This ensures a thorough and validated analysis of the market.

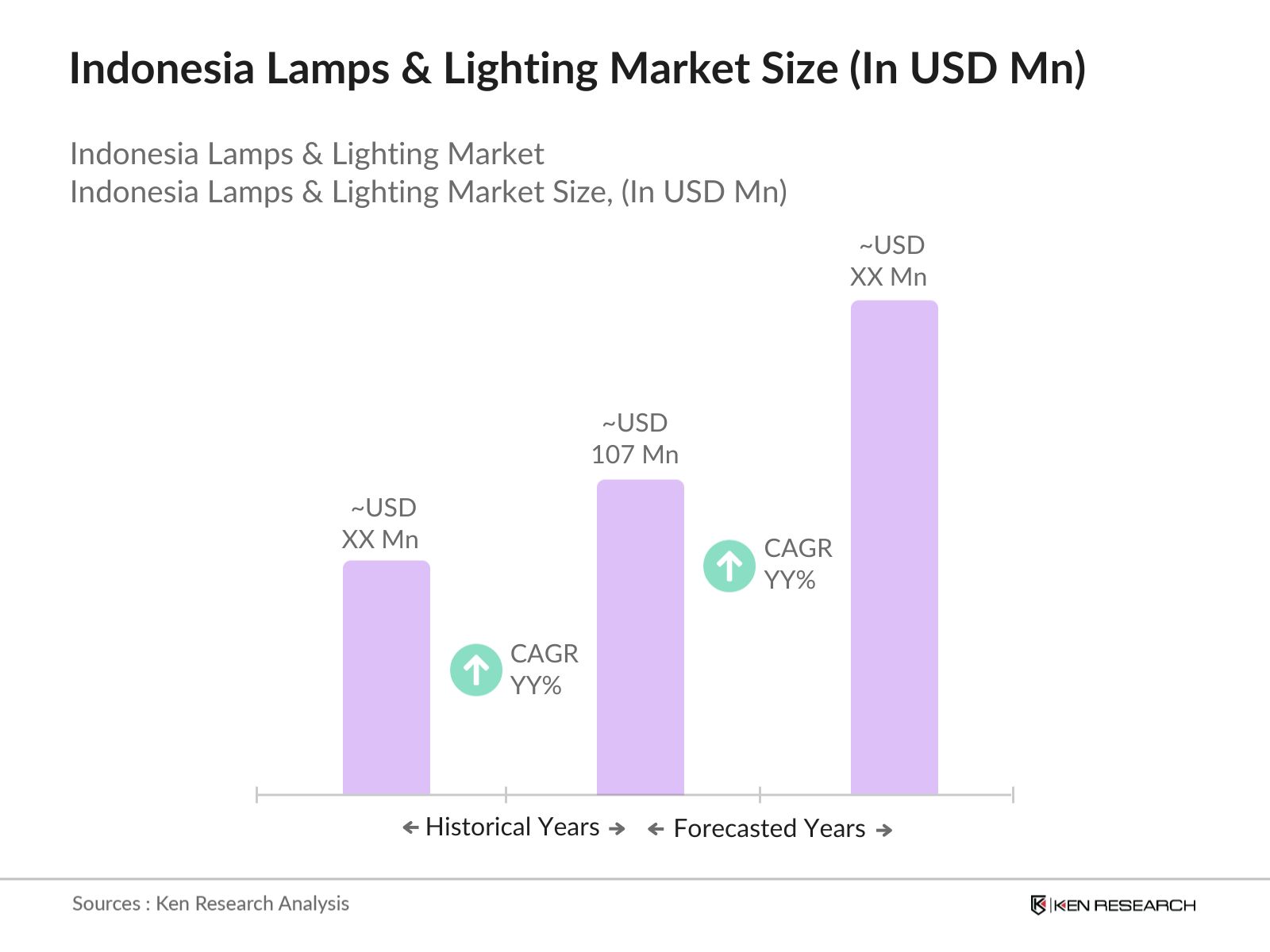

The Indonesia lamps and lighting market is valued at USD 107 million, driven by growing infrastructure projects and increased demand for energy-efficient solutions.

Challenges in the Indonesia lamps and lighting market include high import dependency on lighting components and a lack of local manufacturing capabilities, which hinders cost efficiency and increases supply chain risks.

Key players in the Indonesia lamps and lighting market include Philips Lighting Indonesia, Osram Indonesia, Panasonic Lighting Indonesia, Schneider Electric Indonesia, and GE Lighting Indonesia.

The Indonesia lamps and lighting market is driven by urbanization, government initiatives to promote energy efficiency, and the growing demand for smart city lighting solutions across major urban centers like Jakarta.

The future outlook of the Indonesia lamps and lighting market points to continued growth due to increasing adoption of LED technology, advancements in smart lighting, and expanded infrastructure projects throughout the country.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.