Indonesia Medical Imaging Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD6465

November 2024

93

About the Report

Indonesia Medical Imaging Market Overview

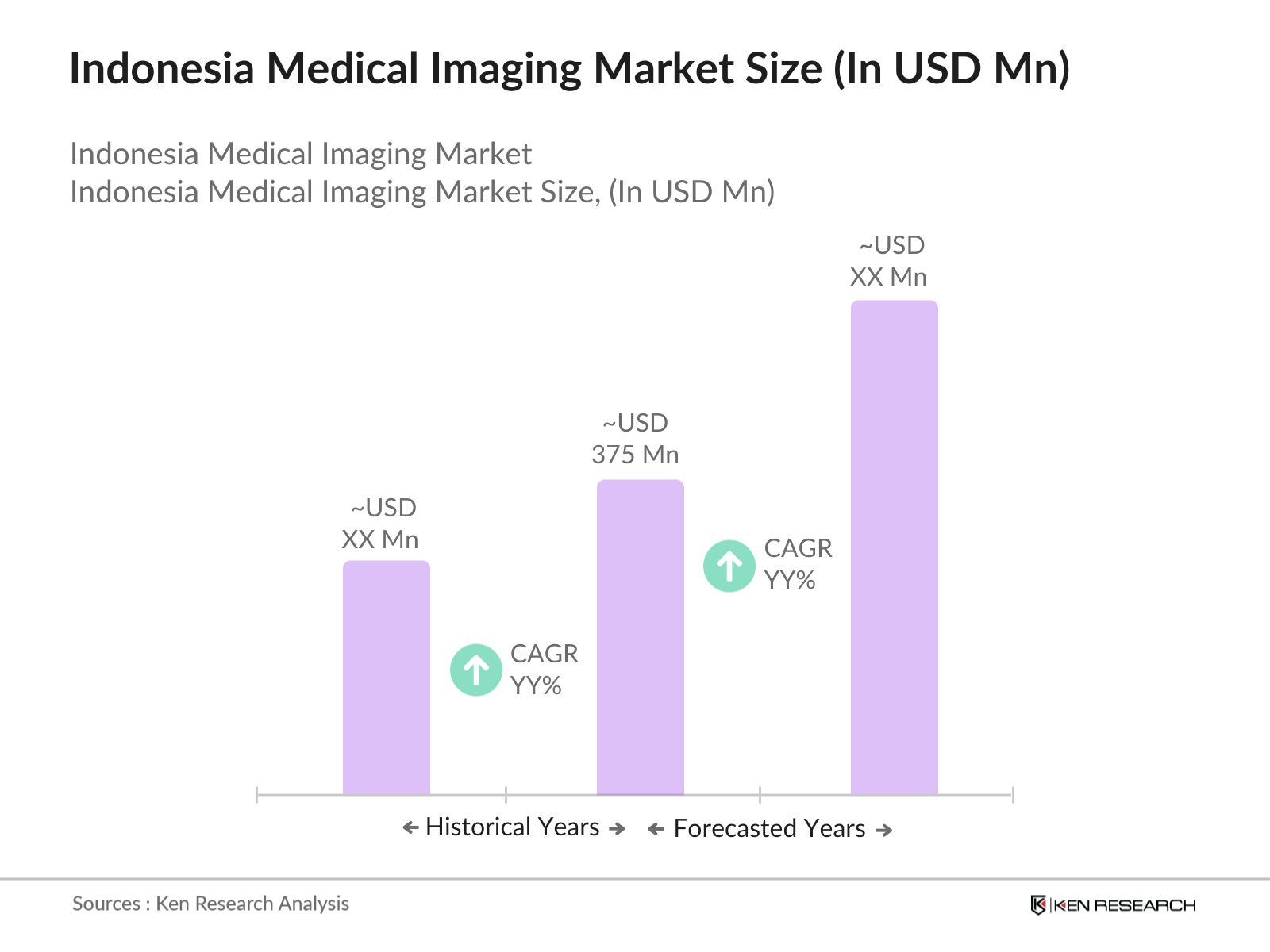

- The Indonesia Medical Imaging market, valued at USD 375 million, is primarily driven by the increasing prevalence of chronic diseases, including cardiovascular diseases and cancer, and a rapidly aging population. The adoption of advanced imaging technologies, such as MRI, CT scans, and ultrasound systems, is rising as healthcare facilities expand their diagnostic capabilities.

- The market is dominated by key metropolitan cities such as Jakarta, Surabaya, and Bandung due to their advanced healthcare infrastructure, high concentration of hospitals, and the presence of major diagnostic centers. These cities lead the market as they attract more investment in healthcare, benefit from higher disposable income among the population, and exhibit a greater demand for advanced medical technologies.

- The governments universal healthcare program (JKN) has expanded its coverage, providing over 220 million Indonesians access to basic healthcare services in 2024. Under the expanded coverage, the program now includes specific diagnostic services such as X-rays and ultrasounds. This is expected to drive the adoption of imaging technologies across public hospitals and clinics as the government strives to meet the increased demand for diagnostic services.

Indonesia Medical Imaging Market Segmentation

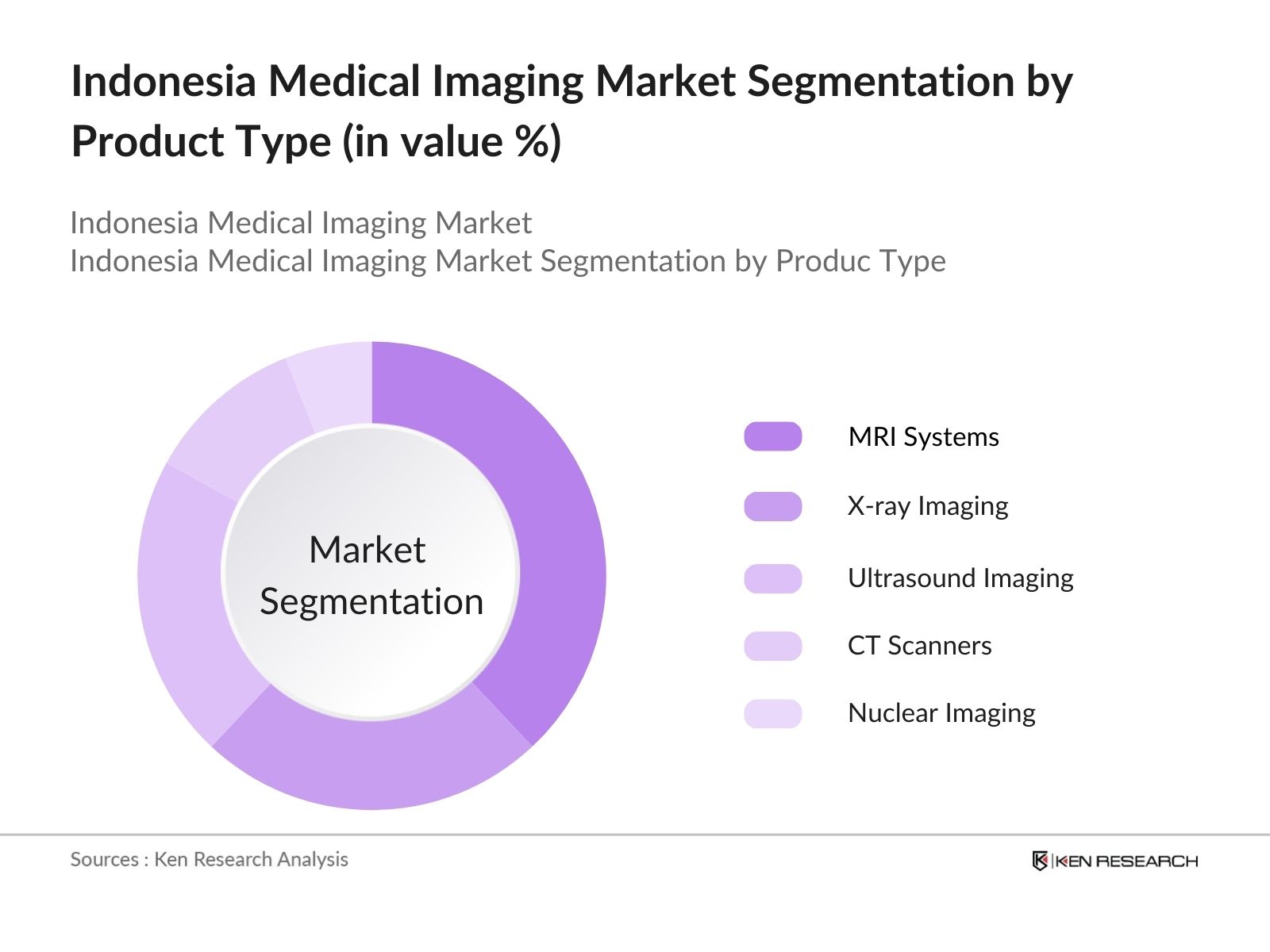

By Product Type: The market is segmented by product type into X-ray Imaging, Ultrasound Imaging, MRI Systems, CT Scanners, and Nuclear Imaging. MRI systems hold a dominant market share in Indonesias medical imaging market, primarily due to their non-invasive diagnostic capabilities and the rising demand for detailed soft-tissue imaging. The growing prevalence of chronic diseases such as cardiovascular diseases and cancer necessitates the use of MRI for accurate diagnosis.

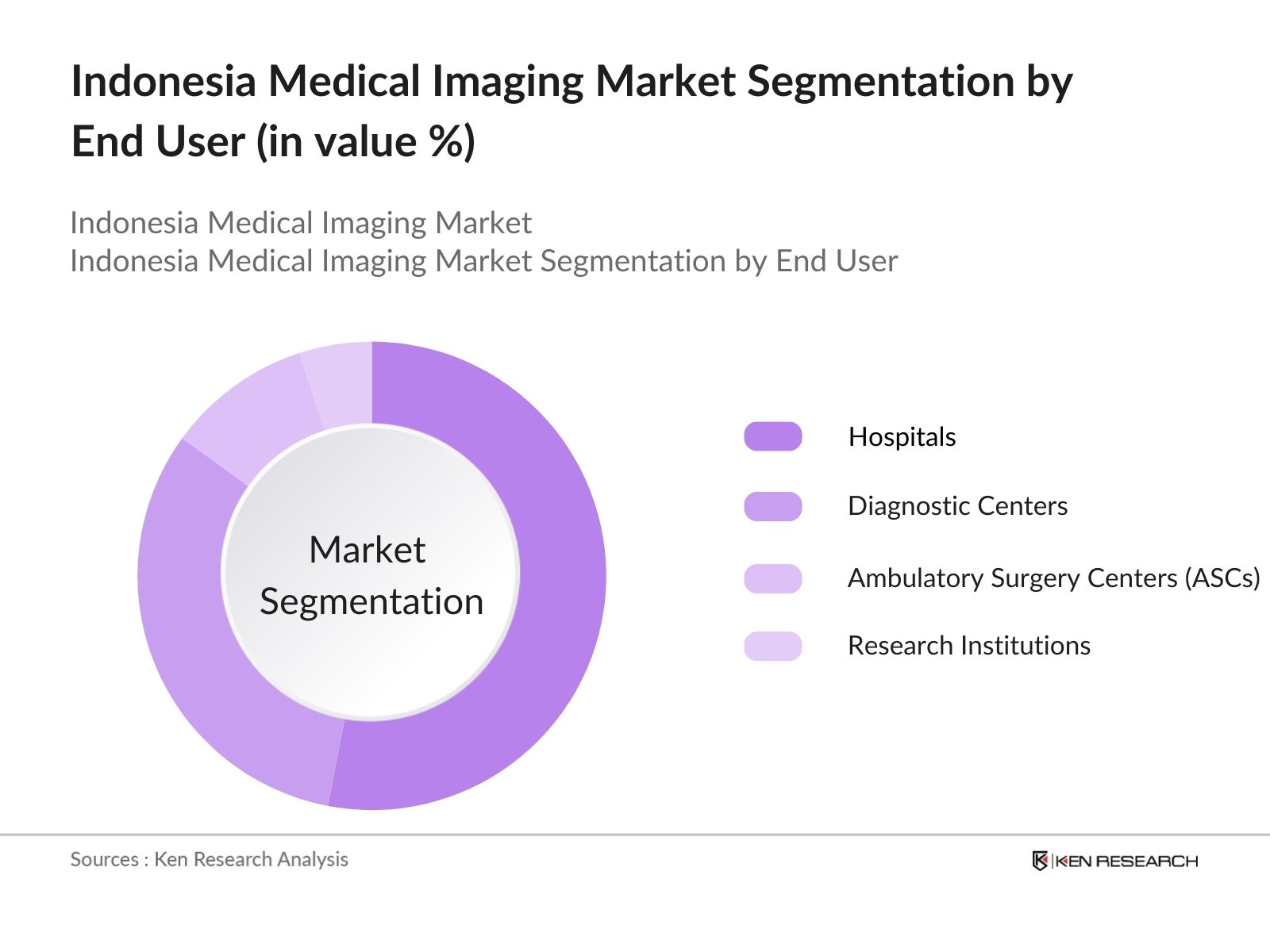

By End User: The market is segmented by end user into Hospitals, Diagnostic Centers, Ambulatory Surgery Centers (ASCs), and Research Institutions. Hospitals dominate the market share within this segment, primarily due to the wide adoption of advanced imaging technologies, which are essential for both diagnosis and treatment planning. Most large hospitals are equipped with a variety of imaging devices, including MRI, CT scanners, and ultrasound systems, to handle a diverse range of medical conditions.

Indonesia Medical Imaging Market Competitive Landscape

The market is characterized by the presence of both global and local players. Major companies have consolidated their position by offering a broad portfolio of imaging solutions tailored to different medical needs. The competitive landscape is dominated by global giants like GE Healthcare and Siemens Healthineers, alongside local players contributing to niche areas.

|

Company |

Established Year |

Headquarters |

Global Reach |

Revenue (USD) |

Product Portfolio |

Key Clients |

R&D Investments |

Strategic Partnerships |

Technological Advancements |

|

GE Healthcare |

1892 |

USA |

|||||||

|

Siemens Healthineers |

1847 |

Germany |

|||||||

|

Philips Healthcare |

1891 |

Netherlands |

|||||||

|

Canon Medical Systems |

1937 |

Japan |

|||||||

|

Fujifilm Holdings Corp |

1934 |

Japan |

Indonesia Medical Imaging Market Analysis

Market Growth Drivers

- Rising Prevalence of Chronic Diseases: The increasing burden of chronic diseases such as cardiovascular illnesses and cancer in Indonesia is driving demand for diagnostic tools, including medical imaging devices. In 2024, Indonesia recorded over 4 million cases of cardiovascular diseases and nearly 350,000 cases of cancer. This surge in non-communicable diseases requires advanced imaging technologies for accurate and early diagnosis, leading to an increase in the procurement of medical imaging equipment in hospitals and diagnostic centers nationwide.

- Expanding Middle-Class Population Demanding Better Healthcare Services: Indonesias middle-class population is to grow, contributing to an increased demand for advanced medical services, including diagnostic imaging. As the middle class continues to prioritize quality healthcare, the demand for services such as MRI, CT scans, and ultrasound is expected to see growth, as patients now prefer modern diagnostics over traditional methods.

- Rise in Healthcare Expenditure by the Private Sector: Indonesias private healthcare expenditure is forecasted to surpass by 2024. Private hospital chains are investing heavily in upgrading diagnostic and imaging technologies to meet the growing patient demand for accurate diagnostics. Several prominent private healthcare providers in the country have announced investments in new diagnostic centers that are equipped with advanced medical imaging devices, significantly contributing to market growth.

Market Challenges

- High Cost of Medical Imaging Devices: Advanced medical imaging technologies such as MRI machines and PET scanners remain costly, with a single MRI machine costing upwards of IDR 20 billion. For many healthcare providers in rural and remote areas, this cost is prohibitive, limiting the adoption of advanced diagnostic technologies. The lack of affordable financing solutions for hospitals to procure this equipment further exacerbates the challenge.

- Limited Availability of Skilled Professionals: Indonesia faces a shortage of radiologists and skilled technicians required to operate advanced medical imaging equipment. As of 2024, Indonesia has less than 3,000 certified radiologists for a population exceeding 270 million, a ratio far below global standard. The lack of trained professionals hampers the optimal use of medical imaging technologies, particularly in rural regions.

Indonesia Medical Imaging Market Future Outlook

Over the next five years, the Indonesia Medical Imaging industry is expected to experience robust growth due to the expanding healthcare infrastructure, increasing demand for diagnostic imaging services, and advancements in medical imaging technology.

Future Market Opportunities

- Growth of Tele-radiology Services in Remote Areas: By 2029, the expansion of telemedicine will drive the growth of tele-radiology services in Indonesia, allowing radiologists to remotely analyze medical images and provide diagnoses for patients in rural areas. The government and private healthcare providers are expected to collaborate in establishing a network of tele-radiology centers that link urban hospitals with rural clinics.

- Increasing Localization of Medical Imaging Manufacturing: Over the next five years, the governments initiative to boost domestic production of medical equipment will result in the local manufacturing of high-quality imaging technologies. As domestic manufacturers ramp up production, Indonesia will see reduced reliance on imported imaging devices, making advanced diagnostic technologies more affordable and accessible.

Scope of the Report

|

Product Type |

X-ray Imaging Ultrasound Imaging MRI Systems CT Scanners Nuclear Imaging |

|

Application |

Oncology Cardiology Neurology Orthopedics Obstetrics and Gynecology |

|

Technology |

2D Imaging 3D Imaging 4D Imaging |

|

End User |

Hospitals Diagnostic Centers Ambulatory Surgery Centers Research Institutions |

|

Region |

North East West South |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Banks and Financial institution

Medical Device Manufacturers

Healthcare Service Providers

Government and Regulatory Bodies (Ministry of Health, Indonesia)

Investor and Venture Capitalist Firms

Telemedicine Providers

Healthcare IT and Software Solution Providers

Companies

Players Mentioned in the Report:

GE Healthcare

Siemens Healthineers

Philips Healthcare

Canon Medical Systems

Fujifilm Holdings Corporation

Hitachi Medical Systems

Samsung Medison

Carestream Health

Esaote SpA

Mindray Medical International

Table of Contents

1. Indonesia Medical Imaging Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Indonesia Medical Imaging Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Indonesia Medical Imaging Market Analysis

3.1. Growth Drivers

3.1.1. Aging Population and Rise in Chronic Diseases (Medical Device Penetration)

3.1.2. Increasing Healthcare Expenditure (Healthcare Infrastructure)

3.1.3. Government Healthcare Initiatives (Public Health Policy)

3.1.4. Technological Advancements in Imaging Modalities (Equipment Innovation)

3.2. Market Challenges

3.2.1. High Cost of Advanced Imaging Systems (Cost Barriers)

3.2.2. Lack of Skilled Workforce (Healthcare Workforce Gaps)

3.2.3. Limited Access in Remote Areas (Infrastructure Deficiency)

3.3. Opportunities

3.3.1. Integration of AI and Machine Learning in Imaging (AI in Diagnostics)

3.3.2. Expansion of Telemedicine for Remote Diagnosis (Tele-Imaging)

3.3.3. Investments in Healthcare Infrastructure (Government Funding)

3.4. Trends

3.4.1. Growing Adoption of Portable Imaging Devices (Portability Trends)

3.4.2. Rise of Hybrid Imaging Systems (Technology Convergence)

3.4.3. Emergence of 3D and 4D Imaging (Advanced Visualization)

3.5. Government Regulations

3.5.1. Regulatory Approval Process for Medical Imaging Devices (Device Certification)

3.5.2. Compliance with Radiation Safety Standards (Radiation Control)

3.5.3. Government Procurement Programs (Public Healthcare Projects)

3.5.4. Import Tariffs and Tax Incentives (Economic Policy)

3.6. SWOT Analysis

3.6.1. Strengths

3.6.2. Weaknesses

3.6.3. Opportunities

3.6.4. Threats

3.7. Stakeholder Ecosystem

3.7.1. Manufacturers

3.7.2. Distributors

3.7.3. Hospitals and Diagnostic Centers

3.7.4. Government Entities

3.8. Porters Five Forces Analysis

3.8.1. Supplier Power

3.8.2. Buyer Power

3.8.3. Competitive Rivalry

3.8.4. Threat of New Entrants

3.8.5. Threat of Substitutes

3.9. Competitive Ecosystem

3.9.1. Key Players and Market Share

3.9.2. New Market Entrants and Potential Disruptors

4. Indonesia Medical Imaging Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. X-ray Imaging

4.1.2. Ultrasound Imaging

4.1.3. MRI Systems

4.1.4. CT Scanners

4.1.5. Nuclear Imaging

4.2. By Application (In Value %)

4.2.1. Oncology

4.2.2. Cardiology

4.2.3. Neurology

4.2.4. Orthopedics

4.2.5. Obstetrics and Gynecology

4.3. By Technology (In Value %)

4.3.1. 2D Imaging

4.3.2. 3D Imaging

4.3.3. 4D Imaging

4.4. By End User (In Value %)

4.4.1. Hospitals

4.4.2. Diagnostic Centers

4.4.3. Ambulatory Surgery Centers (ASCs)

4.4.4. Research Institutions

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. West

4.5.4. South

5. Indonesia Medical Imaging Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. GE Healthcare

5.1.2. Siemens Healthineers

5.1.3. Philips Healthcare

5.1.4. Canon Medical Systems

5.1.5. Fujifilm Holdings Corporation

5.1.6. Hitachi Medical Systems

5.1.7. Samsung Medison

5.1.8. Carestream Health

5.1.9. Esaote SpA

5.1.10. Mindray Medical International

5.1.11. Agfa Healthcare

5.1.12. Shimadzu Corporation

5.1.13. Hologic Inc.

5.1.14. Medtronic

5.1.15. Toshiba Medical Systems

5.2. Cross Comparison Parameters (Product Portfolio, Global Market Presence, Key Clients, Strategic Partnerships, Technological Advancements, Revenue, Market Share, Innovation Rate)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Indonesia Medical Imaging Market Regulatory Framework

6.1. Radiology Equipment Standards

6.2. Certification and Compliance

6.3. Healthcare Facility Licensing

6.4. Public-Private Collaboration Regulations

7. Indonesia Medical Imaging Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Indonesia Medical Imaging Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

9. Indonesia Medical Imaging Market Analysts' Recommendations

9.1. Total Addressable Market (TAM) Analysis

9.2. Customer Cohort Analysis

9.3. Strategic Marketing Initiatives

9.4. Emerging Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first step involved mapping the medical imaging ecosystem in Indonesia, identifying all major stakeholders including manufacturers, healthcare providers, and regulatory bodies. We performed extensive desk research using secondary sources and proprietary databases to define key variables, such as product usage trends, technological adoption, and healthcare expenditures.

Step 2: Market Analysis and Construction

We then compiled historical data on medical imaging devices, analyzing their market penetration and usage within Indonesias healthcare system. This data was used to calculate revenue generation and identify significant market trends across product categories and geographic regions.

Step 3: Hypothesis Validation and Expert Consultation

To validate our hypotheses, we conducted interviews with medical professionals and industry experts. These consultations helped refine our understanding of market dynamics, particularly in terms of the challenges faced by different segments of the healthcare system.

Step 4: Research Synthesis and Final Output

Finally, we synthesized the findings into actionable insights, ensuring the data was both comprehensive and validated. Multiple touchpoints with industry stakeholders helped cross-verify key metrics, guaranteeing the reliability of the final report.

Frequently Asked Questions

How big is Indonesia's Medical Imaging Market?

The Indonesia medical imaging market is valued at USD 375 million, driven by increased healthcare spending and technological advancements in imaging equipment.

What are the challenges in Indonesia's Medical Imaging Market?

Challenges in the Indonesia medical imaging market include high costs of advanced imaging technologies, lack of skilled professionals in remote areas, and limited infrastructure for advanced diagnostics in rural regions.

Who are the major players in Indonesia's Medical Imaging Market?

Key players in the Indonesia medical imaging market include GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and Fujifilm Holdings, each known for their advanced diagnostic solutions and wide product portfolios.

What are the growth drivers of Indonesia's Medical Imaging Market?

Key drivers in the Indonesia medical imaging market include the rising prevalence of chronic diseases, increasing government investment in healthcare infrastructure, and advancements in diagnostic imaging technologies like AI-enabled systems.

Which product type dominates Indonesia's Medical Imaging Market?

MRI systems dominate the medical imaging market due to their superior diagnostic capabilities, especially in detecting complex medical conditions like cancer and neurological disorders.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.