Indonesia Natural Gas Market Outlook to 2030

Region:Indonesia

Author(s):Shubham Kashyap

Product Code:KROD3444

Region:Indonesia

Author(s):Shubham Kashyap

Product Code:KROD3444

November 2024

85

The Indonesia natural gas market is competitive, with major players including state-owned enterprises and multinational corporations. Pertamina, Indonesias state-owned oil and gas company, dominates the upstream and downstream sectors, including gas production, processing, and distribution. The entry of global energy giants such as Chevron and TotalEnergies has increased competition, particularly in exploration and production activities.

|

Company Name |

Establishment Year |

Headquarters |

Gas Production (Million Cubic Feet) |

LNG Export Capacity (Million Tonnes) |

Employees |

Revenue (2023) |

Investment in R&D (2023) |

Key Operations |

|

Pertamina |

1957 |

Indonesia |

||||||

|

Chevron |

1879 |

USA |

||||||

|

ExxonMobil |

1882 |

USA |

||||||

|

TotalEnergies |

1924 |

France |

||||||

|

Medco Energi |

1980 |

Indonesia |

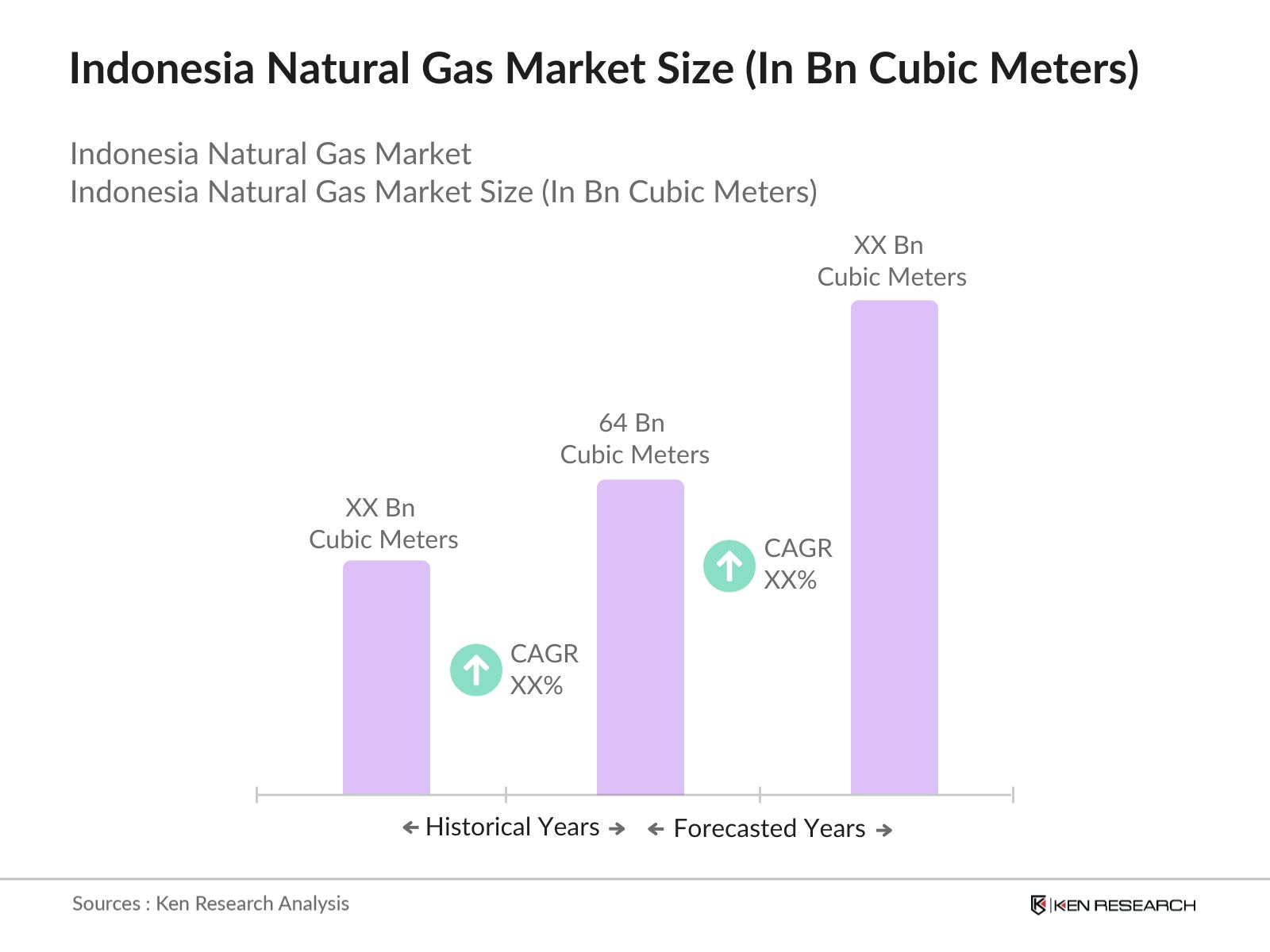

The Indonesia natural gas market is expected to continue its growth trajectory through 2028, driven by rising domestic demand, increased industrial usage, and ongoing government efforts to promote natural gas as a key energy source. The development of LNG facilities and expanded pipeline infrastructure will further support market expansion. The governments commitment to transitioning to cleaner energy sources is expected to bolster the natural gas market in the coming years.

|

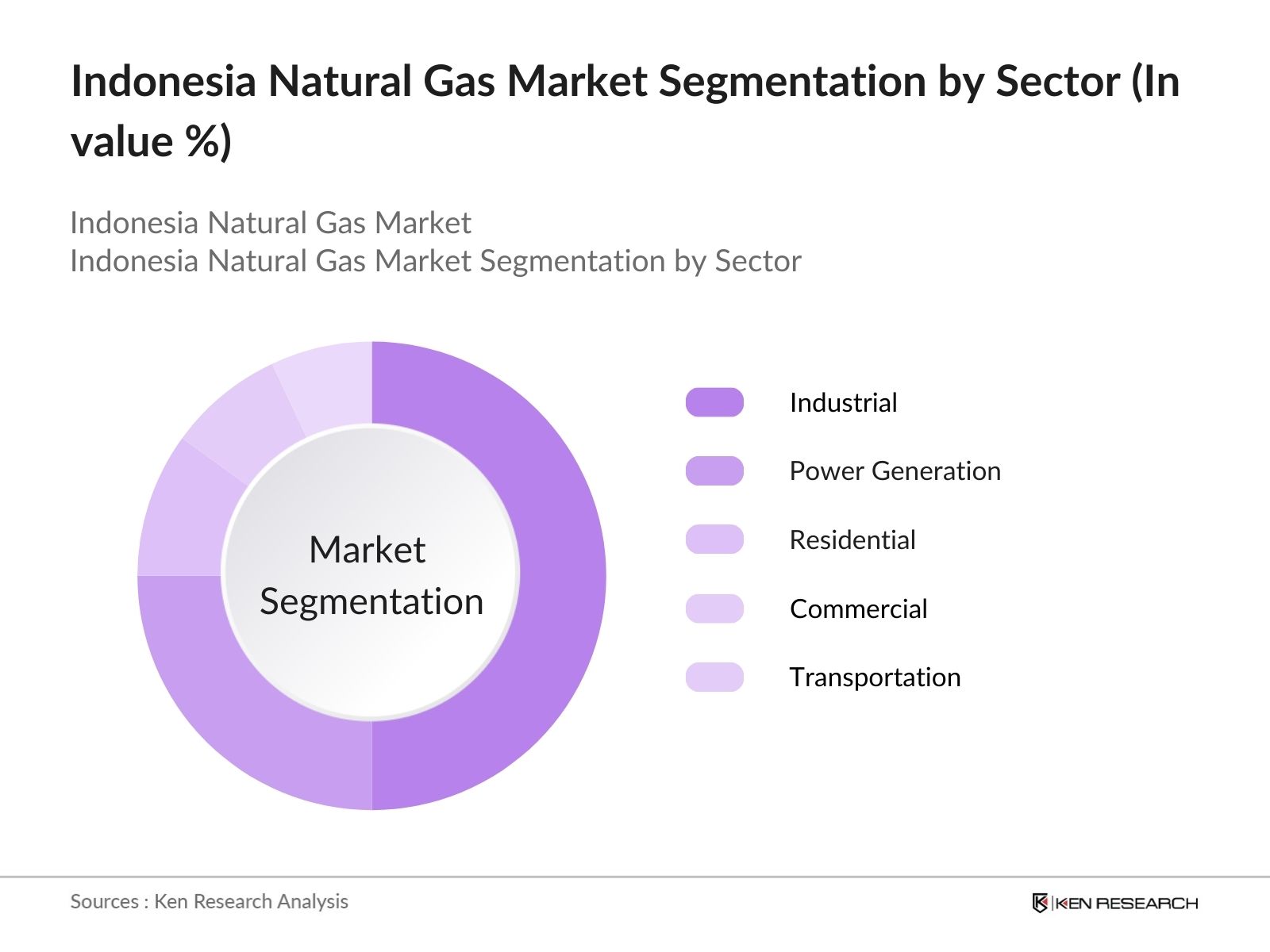

By Sector |

Industrial Power Generation Residential Transportation Commercial |

|

By Distribution Method |

Pipeline Gas Liquefied Natural Gas (LNG) |

|

By Technology |

Conventional Gas Unconventional Gas (Shale, CBM) |

|

By Region |

Sumatra Kalimantan Java Papua Sulawesi |

1.1. Definition and Scope

1.2. Natural Gas Supply Chain Analysis (Production, Processing, Transportation, Distribution)

1.3. Market Taxonomy (By Sector, By Distribution Method, By Technology)

1.4. Natural Gas Market Structure and Ecosystem

1.5. Gas Infrastructure Overview (LNG Terminals, Pipelines, Storage Facilities)

2.1. Historical Market Size (Domestic Consumption, Export Volumes)

2.2. Key Market Developments and Milestones (Policy Shifts, Infrastructure Growth)

2.3. Year-On-Year Growth Analysis (Production, Consumption, Trade)

3.1. Growth Drivers

3.1.1. Abundant Reserves and Increased Exploration Activities

3.1.2. Government Policies Favoring Natural Gas Utilization

3.1.3. Rising Industrial and Power Sector Demand

3.1.4. LNG Export Potential to Regional Markets

3.2. Market Challenges

3.2.1. Inadequate Gas Distribution Infrastructure in Remote Areas

3.2.2. Global Price Volatility and Export Dependency

3.2.3. Regulatory Bottlenecks and Licensing Delays

3.2.4. Competition from Renewable Energy Alternatives

3.3. Opportunities

3.3.1. Expansion of LNG Export Facilities

3.3.2. Development of Gas-to-Power Projects

3.3.3. Partnerships for Infrastructure Modernization

3.3.4. Investment in Downstream Processing Facilities

3.4. Trends

3.4.1. Adoption of Digital Technologies in Gas Operations

3.4.2. Growing Focus on Decarbonization and Low-Emission Gas Solutions

3.4.3. Shift Towards Small-Scale LNG for Remote Areas

3.4.4. Integration of Natural Gas with Hydrogen Projects

3.5. Government Regulation

3.5.1. National Energy Policy (RUEN) and Gas Role

3.5.2. Gas Distribution and Pricing Regulations

3.5.3. Incentives for Private Sector Investments in Gas Infrastructure

3.5.4. Environmental Standards and Emission Reduction Policies

4.1. By Sector (In Value % and Volume)

4.1.1. Industrial

4.1.2. Power Generation

4.1.3. Residential

4.1.4. Transportation (CNG Vehicles, Marine Fuel)

4.1.5. Commercial

4.2. By Distribution Method (In Value % and Volume)

4.2.1. Pipeline Gas

4.2.2. Liquefied Natural Gas (LNG)

4.3. By Technology (In Value % and Volume)

4.3.1. Conventional Gas

4.3.2. Unconventional Gas (Shale Gas, Coal Bed Methane)

4.4. By Region (In Value % and Volume)

4.4.1. Sumatra

4.4.2. Kalimantan

4.4.3. Java

4.4.4. Papua

4.4.5. Sulawesi

5.1. Detailed Profiles of Major Companies

5.1.1. Pertamina

5.1.2. Chevron

5.1.3. ExxonMobil

5.1.4. TotalEnergies

5.1.5. Shell

5.1.6. BP

5.1.7. Medco Energi

5.1.8. ConocoPhillips

5.1.9. Santos Limited

5.1.10. Premier Oil

5.1.11. Eni

5.1.12. Petronas

5.1.13. Talisman Energy

5.1.14. Mubadala Petroleum

5.1.15. INPEX Corporation

5.2. Cross Comparison Parameters (Production Capacity, LNG Export Capacity, Upstream Reserves, Market Share)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Joint Ventures, Expansions)

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

5.9. R&D Investment Analysis

6.1. Gas Supply Licensing Process

6.2. Export-Import Laws and Regulations

6.3. LNG Export Quotas and Regional Trade Agreements

6.4. Compliance with Environmental Laws

7.1. Future Market Size Projections (Domestic Consumption, Export Volumes)

7.2. Key Factors Driving Future Market Growth (Industrialization, Power Demand)

8.1. By Sector (Industrial, Power, Residential, Commercial, Transportation)

8.2. By Distribution Method (Pipeline, LNG)

8.3. By Region (Sumatra, Java, Kalimantan, Papua, Sulawesi)

8.4. By Technology (Conventional, Unconventional)

9.1. TAM/SAM/SOM Analysis

9.2. Strategic Investment Areas

9.3. Market Entry and Expansion Strategies

9.4. White Space Opportunities

Disclaimer Contact Us

In this step, a comprehensive ecosystem map is created for the Indonesia natural gas market, identifying all major stakeholders, including producers, consumers, and infrastructure developers. Desk research, coupled with proprietary databases, is utilized to gather relevant data on the markets key variables, including production, consumption, and export volumes.

Here, historical data on production, LNG exports, and gas consumption is analyzed. The ratio of gas infrastructure to demand centers is evaluated, ensuring accurate revenue estimates. Additionally, we assess the role of major infrastructure projects in shaping the market dynamics.

Industry experts are consulted through computer-assisted telephone interviews (CATIs) to validate market hypotheses. These experts provide insights into key operational challenges and opportunities, ensuring that the market data reflects current trends and conditions.

This step involves gathering data from multiple gas producers and infrastructure operators to verify the accuracy of market statistics. The data is cross-checked with industry reports to ensure a comprehensive and validated final analysis.

The Indonesia natural gas market is valued at 64 billion cubic meters, driven by increasing demand from the industrial and power sectors, along with rising exports of LNG.

Challenges in the Indonesia natural gas market include inadequate distribution infrastructure in remote areas, global gas price fluctuations, and regulatory hurdles. Additionally, competition from renewable energy sources presents a challenge to long-term growth.

Key players in the Indonesia natural gas market include Pertamina, Chevron, ExxonMobil, TotalEnergies, and Medco Energi. These companies dominate due to their extensive production capabilities and well-established LNG export operations.

Growth drivers in the Indonesia natural gas market - include abundant natural gas reserves, rising industrial demand, and government policies promoting the use of natural gas in power generation and exports. The expansion of LNG infrastructure also plays a role.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.