Indonesia Software as a Service Market Outlook to 2030

Region:Indonesia

Author(s):Sanjna Verma

Product Code:KROD5858

Region:Indonesia

Author(s):Sanjna Verma

Product Code:KROD5858

December 2024

98

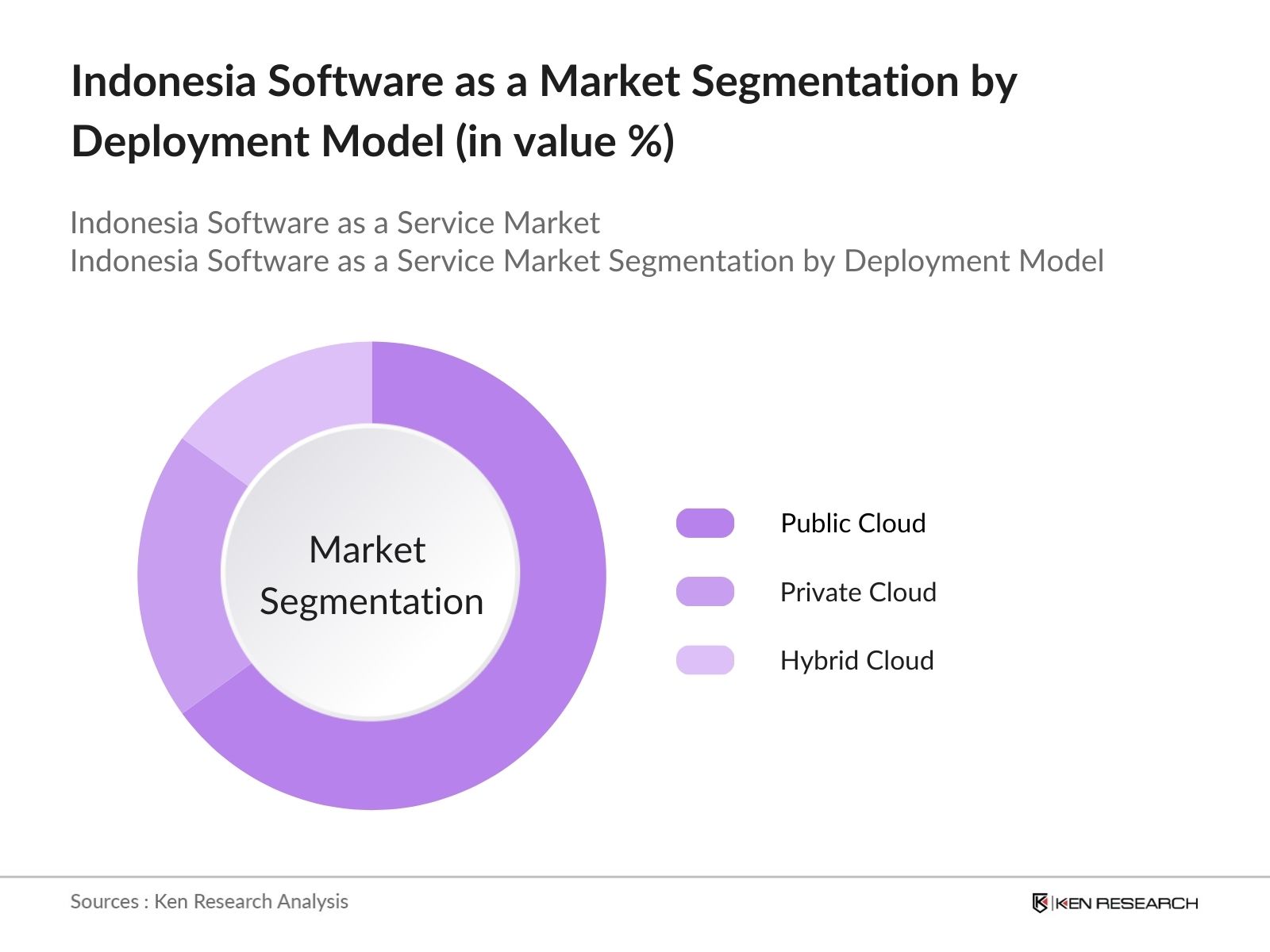

By Deployment Model: Indonesias SaaS market is segmented by deployment model into public cloud, private cloud, and hybrid cloud. Public cloud is the dominant segment due to its cost-effectiveness and scalability. In 2023, public cloud deployment models account for 65% of the market share. This dominance is attributed to businesses favoring public cloud due to lower initial costs, easier scalability, and flexibility in handling fluctuating workloads. Global providers like AWS and Google Cloud have established strong footholds, further driving public cloud adoption.

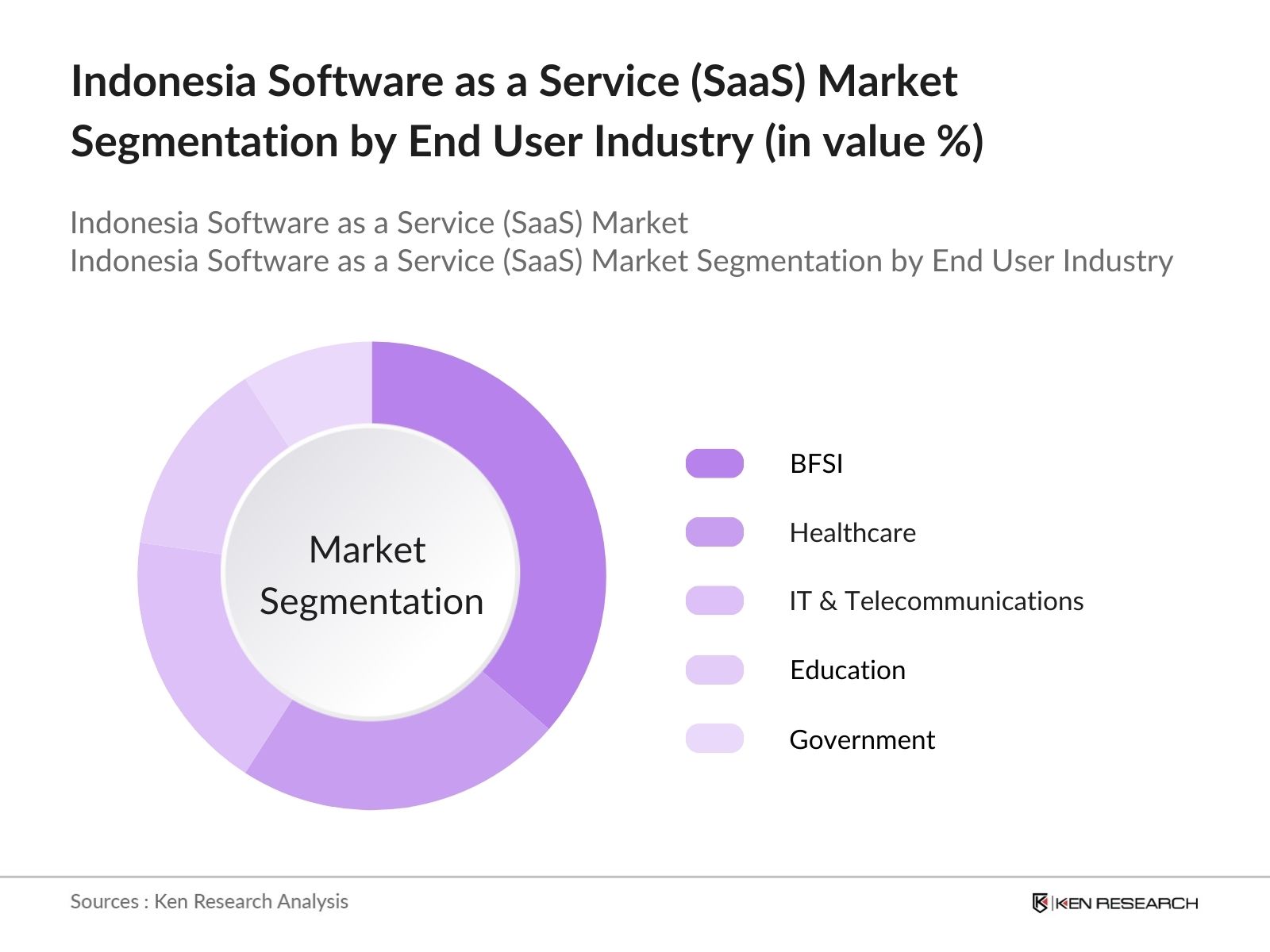

By End-User Industry: The SaaS market in Indonesia is also segmented by end-user industries, including BFSI, healthcare, IT and telecommunications, education, and government. The BFSI sector has emerged as the largest consumer of SaaS solutions, commanding 40% of the market share in 2023. This is primarily due to the sectors ongoing digital transformation initiatives aimed at improving customer experience and increasing operational efficiency. Cloud-based CRM and ERP systems are in high demand to manage large volumes of customer data and regulatory compliance requirements.

Indonesia Software as a Service (SaaS) Market Competitive Landscape

Indonesia Software as a Service (SaaS) Market Competitive LandscapeThe Indonesia SaaS market is dominated by a combination of global giants and local players, creating a competitive and consolidated environment. Major companies like Microsoft, Oracle, and Salesforce dominate the landscape due to their extensive product portfolios and widespread adoption of their platforms by enterprises. Local firms like Telkom Indonesias IndiCloud have a growing presence, catering to specific industries and sectors with localized offerings.

|

Company |

Establishment Year |

Headquarters |

Revenue |

Market Penetration |

Product Offering |

Cloud Platform |

Customer Base |

Local Partnerships |

|

Microsoft Indonesia |

1995 |

Jakarta |

- |

- |

- |

- |

- |

- |

|

Oracle Indonesia |

1997 |

Jakarta |

- |

- |

- |

- |

- |

- |

|

Salesforce Indonesia |

2005 |

Jakarta |

- |

- |

- |

- |

- |

- |

|

Google Cloud Indonesia |

2012 |

Jakarta |

- |

- |

- |

- |

- |

- |

|

Telkom Indonesia (IndiCloud) |

2010 |

Jakarta |

- |

- |

- |

- |

- |

- |

Indonesia SaaS market is expected to experience accelerated growth driven by increasing digital transformation across multiple industries. Continuous government support for cloud adoption, advancements in data analytics, and a growing demand for scalable software solutions will be key drivers of market expansion. Additionally, the emergence of artificial intelligence (AI) and machine learning (ML) technologies is expected to bolster SaaS applications, allowing companies to offer more personalized and automated solutions to their customers.

|

By Deployment Model |

Public Cloud |

|

By End-User Industry |

Banking, Financial Services, and Insurance (BFSI) |

|

By Application Type |

Customer Relationship Management (CRM) |

|

By Enterprise Size |

Small and Medium Enterprises (SMEs) |

|

By Region |

Greater Jakarta |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Cloud Adoption Across Industries

3.1.2 Digital Transformation Initiatives

3.1.3 Government Regulations Promoting Cloud Solutions

3.1.4 Demand from SMEs for Scalable Solutions

3.2 Market Challenges

3.2.1 Data Privacy and Security Concerns

3.2.2 High Dependency on Internet Infrastructure

3.2.3 Limited Localized SaaS Offerings

3.3 Opportunities

3.3.1 Expansion into Untapped Sectors (e.g., Healthcare, Education)

3.3.2 Rising Demand for SaaS in Remote Workforce Management

3.3.3 Integration with AI and Machine Learning Technologies

3.4 Trends

3.4.1 Growth in SaaS Subscription Models

3.4.2 Increased Focus on Customizable SaaS Solutions

3.4.3 Higher Adoption of SaaS for ERP, CRM, and HR Management

3.5 Government Regulation

3.5.1 Digital Economy Framework

3.5.2 Data Protection and Cybersecurity Laws

3.5.3 National Cloud Computing Policies

3.6 Stakeholder Ecosystem

3.7 SWOT Analysis

3.8 Porters Five Forces

3.9 Competition Ecosystem

4.1 By Deployment Model (In Value %)

4.1.1 Public Cloud

4.1.2 Private Cloud

4.1.3 Hybrid Cloud

4.2 By End-User Industry (In Value %)

4.2.1 Banking, Financial Services, and Insurance (BFSI)

4.2.2 Healthcare

4.2.3 IT and Telecommunications

4.2.4 Education

4.2.5 Government

4.3 By Application Type (In Value %)

4.3.1 Customer Relationship Management (CRM)

4.3.2 Enterprise Resource Planning (ERP)

4.3.3 Human Resource Management (HRM)

4.3.4 Collaboration Tools

4.3.5 E-commerce Solutions

4.4 By Enterprise Size (In Value %)

4.4.1 Small and Medium Enterprises (SMEs)

4.4.2 Large Enterprises

4.5 By Region (In Value %)

4.5.1 Greater Jakarta

4.5.2 Java

4.5.3 Sumatra

4.5.4 Bali and Nusa Tenggara

4.5.5 Kalimantan

5.1 Detailed Profiles of Major Companies

5.1.1 PT Microsoft Indonesia

5.1.2 Oracle Indonesia

5.1.3 SAP Indonesia

5.1.4 Salesforce Indonesia

5.1.5 Zoho Corporation

5.1.6 Google Cloud Indonesia

5.1.7 Amazon Web Services (AWS) Indonesia

5.1.8 PT Telkom Indonesia (IndiCloud)

5.1.9 NetSuite Indonesia

5.1.10 Freshworks Indonesia

5.2 Cross Comparison Parameters (Revenue, Inception Year, Product Offering, Market Share, Partnerships)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Support and Incentives

6.1 Data Protection Laws (Personal Data Protection Act)

6.2 Compliance and Certification Standards (ISO 27001, SOC 2)

6.3 Cloud Computing Guidelines

6.4 Cybersecurity Framework

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Deployment Model (In Value %)

8.2 By End-User Industry (In Value %)

8.3 By Application Type (In Value %)

8.4 By Enterprise Size (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

The research process begins with constructing an ecosystem map that encompasses all key stakeholders in the Indonesia SaaS market. This includes extensive desk research using proprietary databases and secondary resources to capture market dynamics and trends. The objective is to define critical factors like cloud adoption rate, end-user demand, and software development challenges.

In this phase, we collect and analyze historical market data, including SaaS penetration, enterprise software adoption, and the growth of cloud infrastructure. We also assess market revenue generation and the impact of internet infrastructure quality on SaaS deployment in Indonesia.

Hypotheses related to the SaaS market are validated through consultations with industry professionals, cloud service providers, and system integrators. These interviews provide insights into market behavior, product offerings, and customer requirements, refining the research findings.

Finally, we engage with SaaS vendors to obtain detailed product segment data, market performance, and consumer trends. This bottom-up approach ensures that all statistical insights are validated and align with market conditions, leading to a comprehensive analysis of the Indonesia SaaS market.

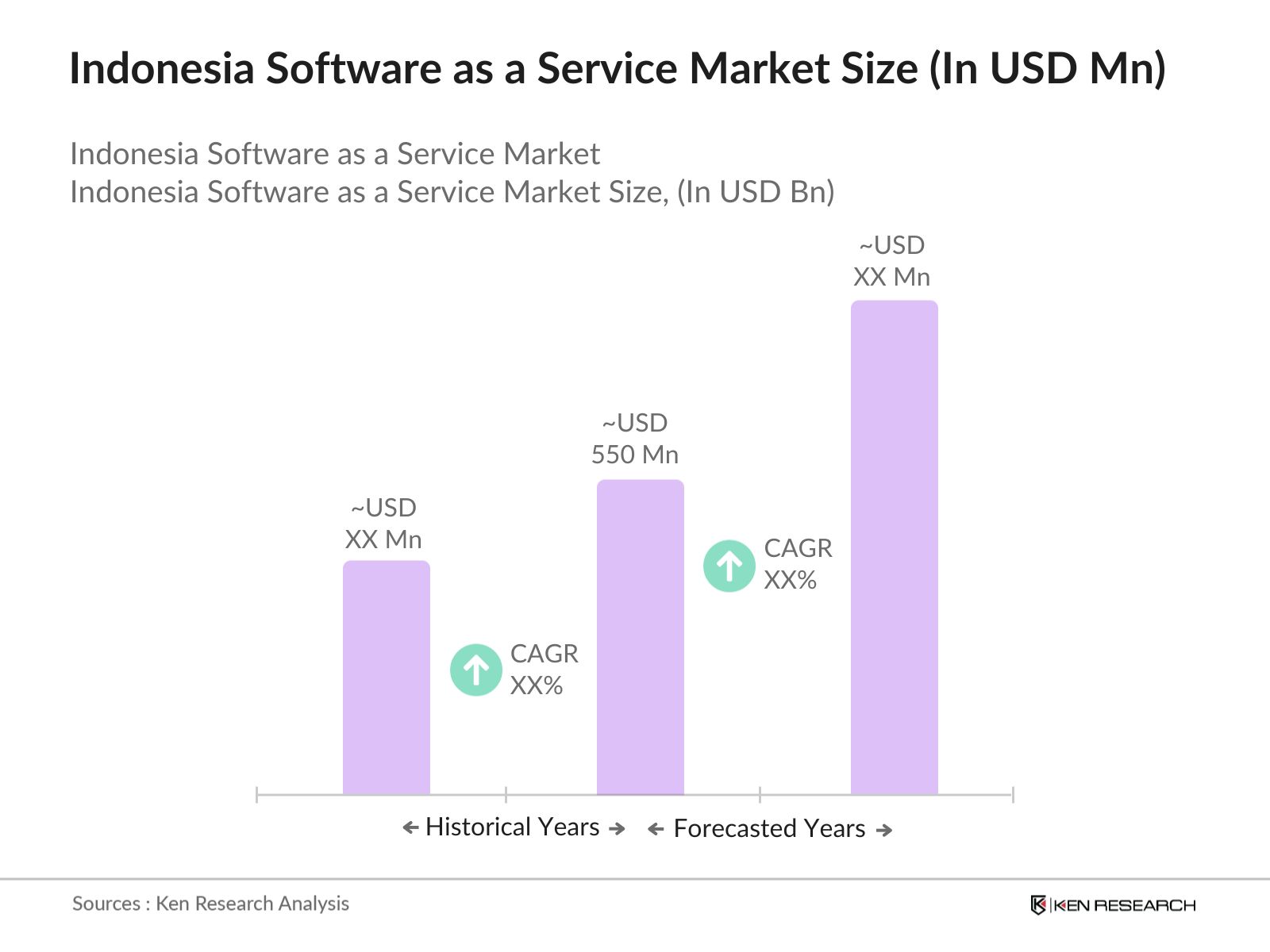

The Indonesia SaaS market is valued at USD 550 million, driven by digital transformation efforts and a growing demand for scalable cloud solutions among enterprises and SMEs.

Key challenges of Indonesia SaaS market include data privacy concerns, reliance on robust internet infrastructure, and limited availability of localized SaaS solutions. Additionally, regulatory compliance and security requirements pose hurdles for SaaS providers.

Major players of Indonesia SaaS market include global companies such as Microsoft, Oracle, Salesforce, and local entities like Telkom Indonesias IndiCloud. These firms dominate the market due to their comprehensive product offerings and strong client bases.

Growth drivers of Indonesia SaaS market include the increasing adoption of cloud technologies, digital transformation initiatives across industries, and the rising demand for cost-effective, scalable software solutions. The governments push for IT modernization and cloud adoption is also a key factor.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.