Indonesia Used Automobiles Market Outlook to 2030

Region:Indonesia

Author(s):Shambhavi

Product Code:KROD7765

Region:Indonesia

Author(s):Shambhavi

Product Code:KROD7765

December 2024

87

Listen to the audio summary

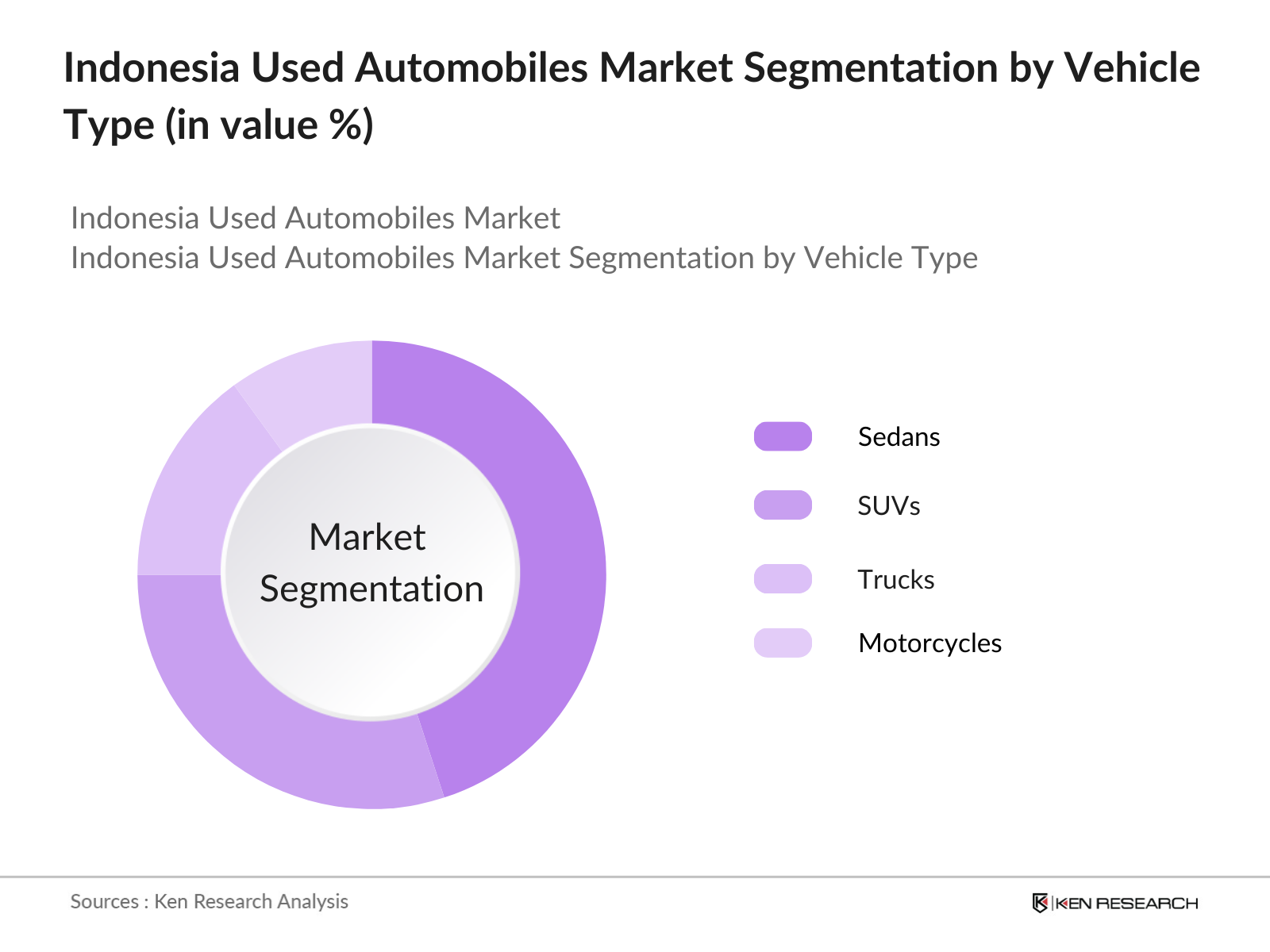

By Vehicle Type: The Indonesia Used Automobiles Market is segmented by vehicle type into sedans, SUVs, trucks, and motorcycles. Among these, SUVs currently hold a dominant market share due to Indonesias diverse terrain and a growing preference for vehicles that offer greater functionality and space. SUVs also appeal to consumers who view them as status symbols, and their versatility suits both urban and semi-urban settings. The high resale value of SUVs and the increasing availability of models in the used vehicle market have bolstered their popularity.

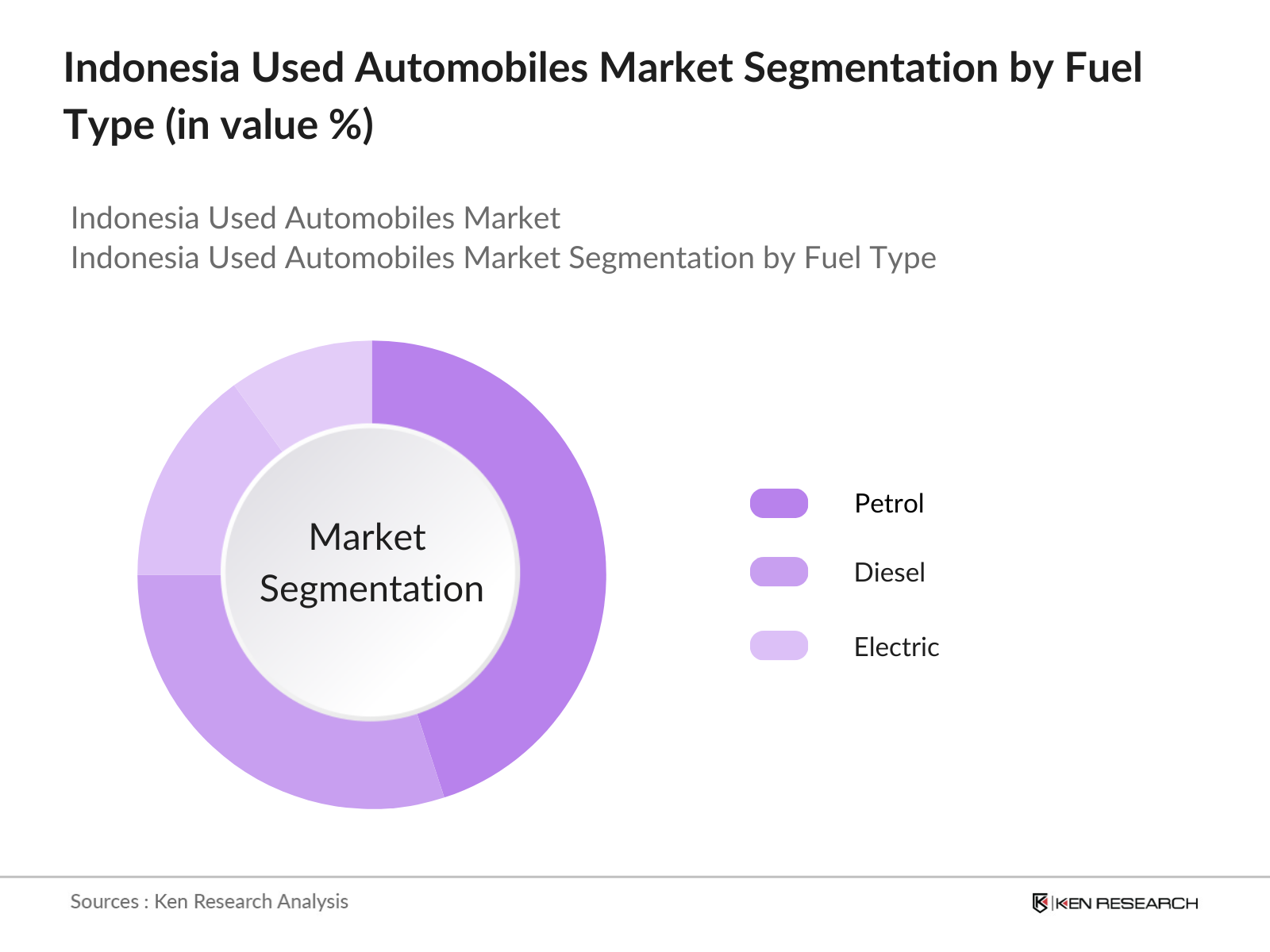

By Fuel Type: The market is segmented by fuel type into petrol, diesel, and electric vehicles. Petrol vehicles have a dominant share, mainly due to their widespread availability, lower upfront costs, and familiarity among consumers. Despite a gradual shift towards alternative energy sources, electric vehicle infrastructure remains limited, making petrol vehicles the most practical choice for used automobile buyers in Indonesia. Furthermore, maintenance costs and fuel availability favor petrol vehicles over others, reinforcing their position in the market.

The Indonesia Used Automobiles Market is dominated by a combination of local and international players who leverage strong dealership networks, digital platforms, and robust customer service models to maintain competitive edges. Market leaders such as OLX Autos and Carmudi Indonesia benefit from established brand recognition and extensive market knowledge, which enables them to attract a steady consumer base.

The Indonesia Used Automobiles Market is set for steady growth driven by increasing digitalization in car sales, the proliferation of e-commerce platforms, and flexible financing options. With consumer preference shifting toward cost-effective and convenient car-buying processes, companies are focusing on enhancing online platforms to offer seamless, transparent, and reliable vehicle transactions. Additionally, as government incentives support the growth of electric vehicles, the used car market is expected to gradually integrate more eco-friendly vehicle options.

|

By Vehicle Type |

Sedans SUVs Hatchbacks Pick-ups Others |

|

By Age of Vehicle |

0-3 Years 3-5 Years 5-10 Years 10+ Years |

|

By Engine Type |

Petrol Diesel Hybrid Electric |

|

By Distribution Channel |

Dealerships Private Sellers Online Platforms |

|

By Region |

Java Sumatra Kalimantan Sulawesi Papua |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Middle-Class Population (Population growth, disposable income increase)

3.1.2. Urbanization Trends (Urban population growth, infrastructure development)

3.1.3. Shift to Affordable Transport Solutions (Increased demand for cost-effective mobility)

3.1.4. Environmental Concerns (Government initiatives for eco-friendly vehicles)

3.2. Market Challenges

3.2.1. Regulatory Compliance (Government regulations on emissions)

3.2.2. Quality Assurance Issues (Market concerns over vehicle safety and maintenance)

3.2.3. Competition from New Vehicles (Aggressive pricing from manufacturers)

3.3. Opportunities

3.3.1. Growth of E-commerce Platforms (Online sales channels for used automobiles)

3.3.2. Enhanced Financing Options (Increased access to loans and credit)

3.3.3. Integration of Technology (Adoption of mobile applications for vehicle purchase)

3.4. Trends

3.4.1. Increasing Popularity of Electric Vehicles (Government incentives for EV adoption)

3.4.2. Rise of Online Marketplaces (Shifting consumer preferences towards digital platforms)

3.4.3. Growing Demand for Certified Pre-Owned Vehicles (Consumer preference for reliable purchases)

3.5. Government Regulation

3.5.1. Emission Standards (Implementation of stricter pollution control measures)

3.5.2. Taxation Policies (Impact of tax incentives on used vehicle sales)

3.5.3. Licensing Requirements (Changes in vehicle registration processes)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Vehicle Type (In Value %)

4.1.1. Sedans

4.1.2. SUVs

4.1.3. Hatchbacks

4.1.4. Pick-ups

4.1.5. Others

4.2. By Age of Vehicle (In Value %)

4.2.1. 0-3 Years

4.2.2. 3-5 Years

4.2.3. 5-10 Years

4.2.4. 10+ Years

4.3. By Engine Type (In Value %)

4.3.1. Petrol

4.3.2. Diesel

4.3.3. Hybrid

4.3.4. Electric

4.4. By Distribution Channel (In Value %)

4.4.1. Dealerships

4.4.2. Private Sellers

4.4.3. Online Platforms

4.5. By Region (In Value %)

4.5.1. Java

4.5.2. Sumatra

4.5.3. Kalimantan

4.5.4. Sulawesi

4.5.5. Papua

5.1 Detailed Profiles of Major Companies

5.1.1. Toyota Astra Motor

5.1.2. Honda Prospect Motor

5.1.3. Nissan Motor Indonesia

5.1.4. Mitsubishi Motors Krama Yudha Indonesia

5.1.5. Daihatsu Indonesia

5.1.6. Suzuki Indomobil Sales

5.1.7. Hyundai Motor Manufacturing Indonesia

5.1.8. Isuzu Astra Motor Indonesia

5.1.9. Hino Motors Sales Indonesia

5.1.10. BMW Indonesia

5.1.11. Mercedes-Benz Indonesia

5.1.12. Kia Motors Indonesia

5.1.13. Ford Motor Indonesia

5.1.14. Great Wall Motors Indonesia

5.1.15. Wuling Motors

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Vehicle Type (In Value %)

8.2. By Age of Vehicle (In Value %)

8.3. By Engine Type (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact Us

The process begins with constructing a detailed ecosystem map, identifying all significant stakeholders within the Indonesia Used Automobiles Market. This stage involves in-depth secondary research utilizing credible sources, including industry reports and proprietary databases, to define the critical market variables.

In this stage, historical data related to the Indonesia Used Automobiles Market is compiled and analyzed. This involves a review of market penetration, the ratio of online to offline sales, and assessment of vehicle turnover rates to ensure accurate revenue projections.

Hypotheses are formulated based on preliminary data analysis and then validated through expert consultations with industry leaders and dealership representatives. These insights help refine data accuracy and provide a market-specific perspective.

The final phase entails synthesizing data from various sources, ensuring a comprehensive and validated analysis of the market. Interactions with key stakeholders help consolidate data points, thereby delivering a reliable and robust market analysis report.

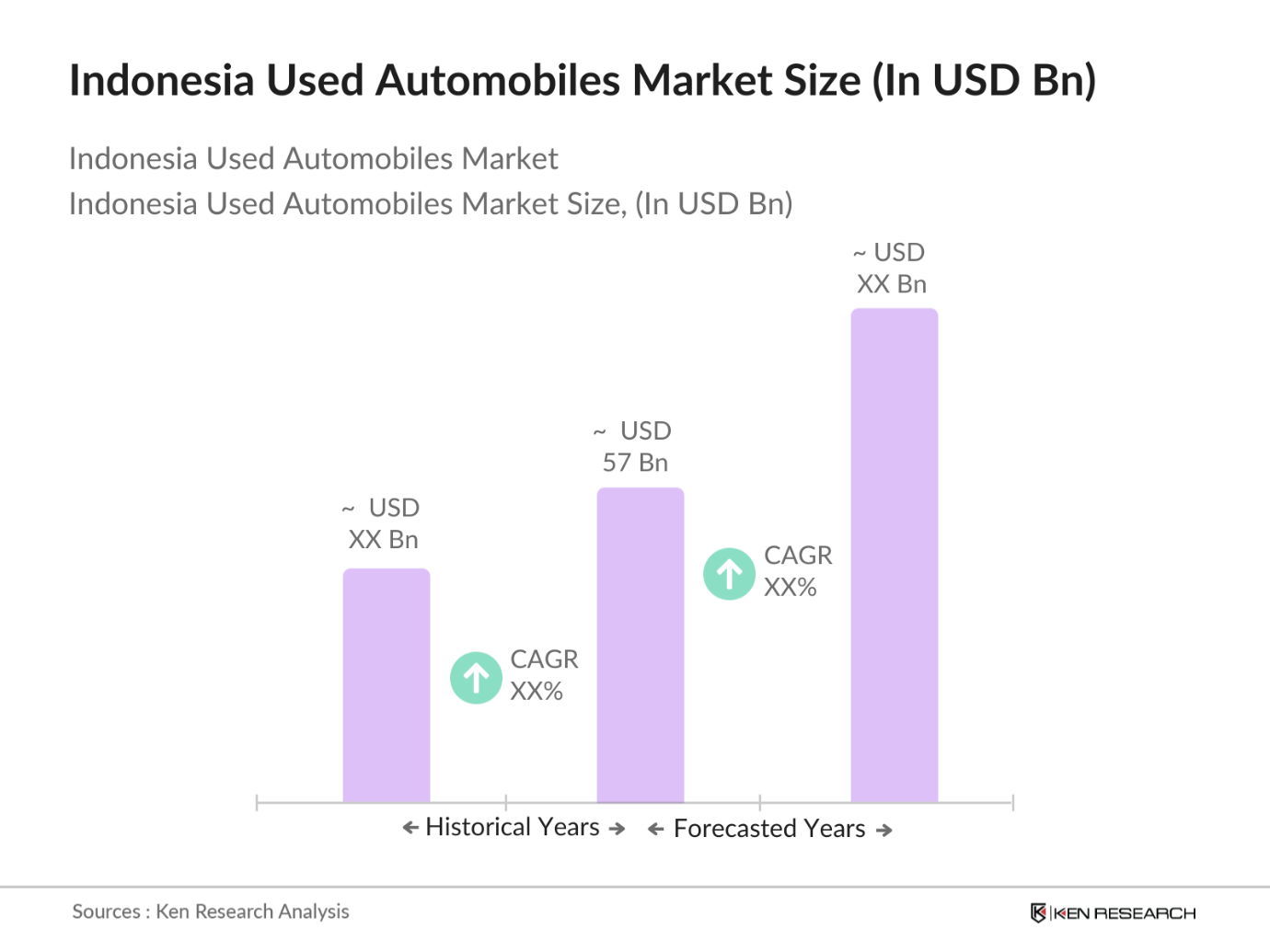

The Indonesia Used Automobiles Market is valued at USD 57 billion, driven by consumer demand for affordable vehicles, a growing middle class, and the expanding availability of online platforms for used vehicle sales.

Challenges include a lack of transparency in transactions, regulatory hurdles, and competition from the new car market, which may affect consumer confidence and impact the growth of used vehicle sales.

Major players include OLX Autos, Mobil88, Carmudi Indonesia, BeliMobilGue, and Carsome, who leverage established networks, online platforms, and customer service excellence to maintain market dominance.

SUVs are favored due to their versatility, suitability for Indonesias diverse terrain, and status as aspirational vehicles. Their robust presence in the used car market is bolstered by high resale values and strong consumer demand.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.