Indonesia Vegetable Market Outlook to 2030

Region:Indonesia

Author(s):Abhinav kumar

Product Code:KROD3667

Region:Indonesia

Author(s):Abhinav kumar

Product Code:KROD3667

December 2024

85

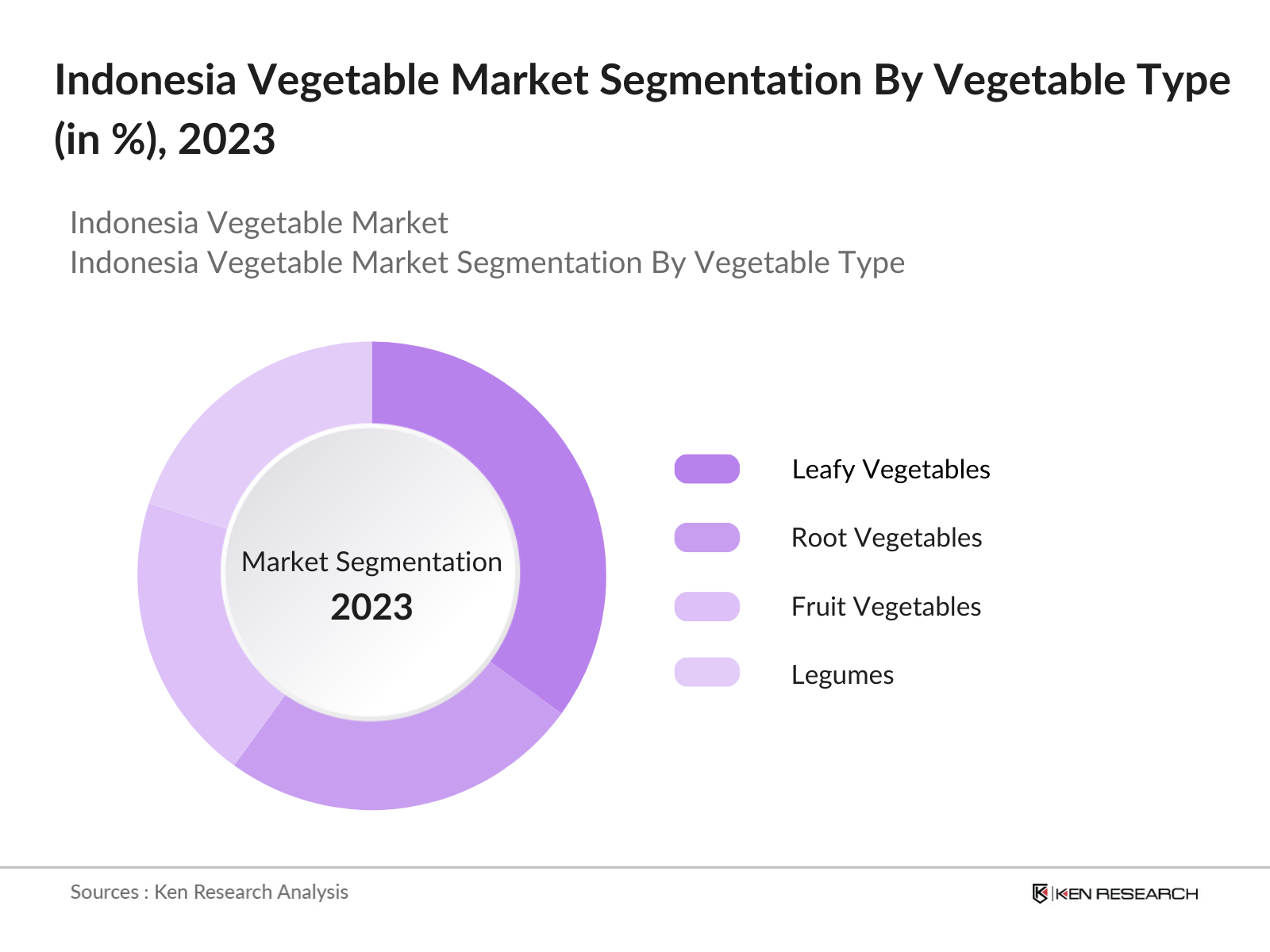

By Vegetable Type: Indonesias vegetable market is segmented by vegetable type into leafy vegetables, root vegetables, fruit vegetables, and legumes. Recently, leafy vegetables hold a dominant share within this segment due to the increasing demand for healthier food options among consumers. Leafy vegetables like spinach, kale, and lettuce have gained popularity owing to their nutritional benefits and the rising trend of clean eating in urban areas. Moreover, advancements in farming techniques like hydroponics have made leafy vegetables more accessible throughout the year, bolstering their market share.

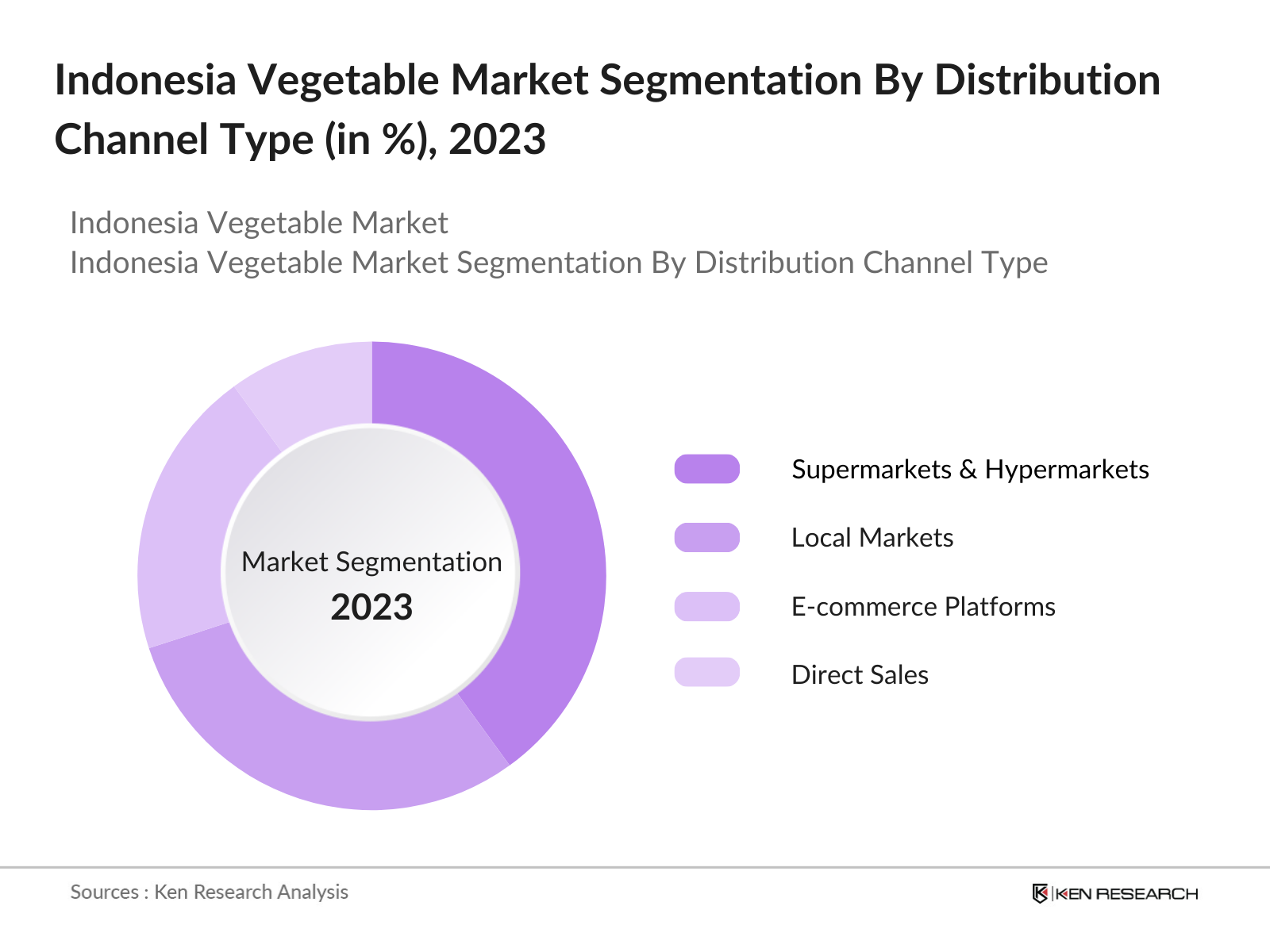

By Distribution Channel: In terms of distribution channels, the Indonesia vegetable market is segmented into supermarkets and hypermarkets, local markets, e-commerce platforms, and direct sales (farmers to consumers). Supermarkets and hypermarkets currently dominate this segment due to their extensive reach, growing urbanization, and consumer preference for one-stop shopping experiences. As more Indonesians move to cities, they increasingly rely on modern retail chains for access to fresh produce, which is why this channel holds a significant share of the distribution market.

The Indonesia vegetable market is dominated by a mix of local and international players, with companies like PT East West Seed Indonesia and PT TaniHub Group holding significant influence. The market is characterized by a robust competitive ecosystem, with both domestic and multinational firms vying for market share by leveraging their extensive distribution networks, strong brand presence, and diverse product portfolios. The consolidation of these players highlights their ability to meet the growing consumer demand while ensuring quality and scalability in production.

|

Company Name |

Establishment Year |

Headquarters |

No. of Employees |

Revenue (USD) |

Market Penetration |

Key Product Type |

Distribution Channel |

Sustainability Initiatives |

|

PT East West Seed Indonesia |

1982 |

Purwakarta, Indonesia |

- |

- |

- |

- |

- |

- |

|

PT TaniHub Group |

2016 |

Jakarta, Indonesia |

- |

- |

- |

- |

- |

- |

|

PT Sumber Tani Agung |

1971 |

Medan, Indonesia |

- |

- |

- |

- |

- |

- |

|

PT BISI International Tbk |

1983 |

Kediri, Indonesia |

- |

- |

- |

- |

- |

- |

|

PT Sewu Segar Nusantara |

1995 |

Jakarta, Indonesia |

- |

- |

- |

- |

- |

- |

Over the next five years, the Indonesia vegetable market is expected to witness significant growth, driven by increasing health awareness among consumers, continued government support for agricultural productivity, and the adoption of innovative farming techniques. Technological advancements such as precision farming and vertical agriculture are anticipated to improve yield and quality, while sustainability efforts such as organic farming practices will play a major role in meeting both domestic and export demand.

|

Vegetable Type |

Leafy Vegetables Root Vegetables Fruit Vegetables Legumes |

|

Farming Technique |

Traditional Farming Organic Farming Hydroponic Farming Vertical Farming |

|

Distribution Channel |

Supermarkets and Hypermarkets Local Markets E-commerce Platforms Direct Sales |

|

End-Use |

Households Food Processing Industries Restaurants and Food Services |

|

Region |

Java Sumatra Bali and Nusa Tenggara Kalimantan Sulawesi |

1.1. Definition and Scope

1.2. Market Taxonomy (Type of Vegetables, Farming Techniques, Distribution Channels)

1.3. Market Growth Rate (CAGR, Volume Growth)

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Urbanization and Population Growth

3.1.2. Changing Dietary Preferences (Increasing demand for fresh produce, vegetarian diets)

3.1.3. Government Initiatives for Agricultural Development

3.1.4. Technological Advancements in Farming (Hydroponics, Vertical Farming)

3.2. Market Challenges

3.2.1. Climate Variability and Natural Disasters

3.2.2. Limited Infrastructure and Cold Chain Facilities

3.2.3. Price Volatility

3.3. Opportunities

3.3.1. Export Potential to ASEAN and Global Markets

3.3.2. Adoption of Organic Farming Practices

3.3.3. Collaboration with International Agribusiness Firms

3.4. Trends

3.4.1. Shift towards Sustainable and Organic Farming

3.4.2. Increased Investments in Smart Agriculture (Precision Farming)

3.4.3. Expansion of E-commerce Channels for Vegetable Distribution

3.5. Government Regulations and Policies

3.5.1. Agricultural Subsidies and Support Programs

3.5.2. Trade Agreements for Vegetable Exports

3.5.3. Quality Standards and Certifications (SNI, Organic Certifications)

3.5.4. Import Tariffs and Duties on Vegetables

3.6. SWOT Analysis

3.7. Stake Ecosystem (Farmers, Distributors, Retailers, Exporters)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Vegetable Type (In Value %)

4.1.1. Leafy Vegetables

4.1.2. Root Vegetables

4.1.3. Fruit Vegetables

4.1.4. Legumes

4.2. By Farming Technique (In Value %)

4.2.1. Traditional Farming

4.2.2. Organic Farming

4.2.3. Hydroponic Farming

4.2.4. Vertical Farming

4.3. By Distribution Channel (In Value %)

4.3.1. Supermarkets and Hypermarkets

4.3.2. Local Markets

4.3.3. E-commerce Platforms

4.3.4. Direct Sales (Farmers to Consumers)

4.4. By End-Use (In Value %)

4.4.1. Households

4.4.2. Food Processing Industries

4.4.3. Restaurants and Food Services

4.5. By Region (In Value %)

4.5.1. Java

4.5.2. Sumatra

4.5.3. Bali and Nusa Tenggara

4.5.4. Kalimantan

4.5.5. Sulawesi

5.1 Detailed Profiles of Major Companies

5.1.1. Indofood Sukses Makmur Tbk

5.1.2. PT East West Seed Indonesia

5.1.3. PT TaniHub Group

5.1.4. PT BISI International Tbk

5.1.5. PT Sumber Tani Agung Resources

5.1.6. PT Great Giant Pineapple

5.1.7. PT Agrosid Manunggal Sentosa

5.1.8. PT Panca Agro Mandiri

5.1.9. PT Sentra Boga Handal Tbk

5.1.10. PT Sewu Segar Nusantara

5.1.11. PT Primasindo

5.1.12. Cargill Indonesia

5.1.13. Bayer CropScience Indonesia

5.1.14. BASF Indonesia

5.1.15. PT Aneka Tani Nusantara

5.2 Cross Comparison Parameters (Market Share, Sales Volume, Distribution Reach, Number of Employees, Production Capacity, Sustainability Initiatives, Export Markets, Profit Margins)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Agricultural Standards and Certifications

6.2. Compliance Requirements

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Vegetable Type (In Value %)

8.2. By Farming Technique (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By End-Use (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. White Space Opportunity Analysis

9.4. Marketing Initiatives

The first step involves constructing an ecosystem map covering all stakeholders within the Indonesia Vegetable Market. This phase leverages secondary research from industry reports, government publications, and proprietary databases to identify the critical variables that impact market growth.

In this phase, we analyze historical data, including production levels, import-export figures, and pricing trends. The objective is to build a comprehensive understanding of how various sub-segments perform and their contribution to the overall market.

Market hypotheses are formed based on the analyzed data and validated through consultations with industry experts, farmers, and vegetable distributors. These discussions provide deeper insights into market trends and the operational dynamics at play.

The final step involves synthesizing all the data collected from secondary and primary sources. We engage directly with market players to further validate findings and ensure that the report accurately reflects the state of the Indonesia Vegetable Market.

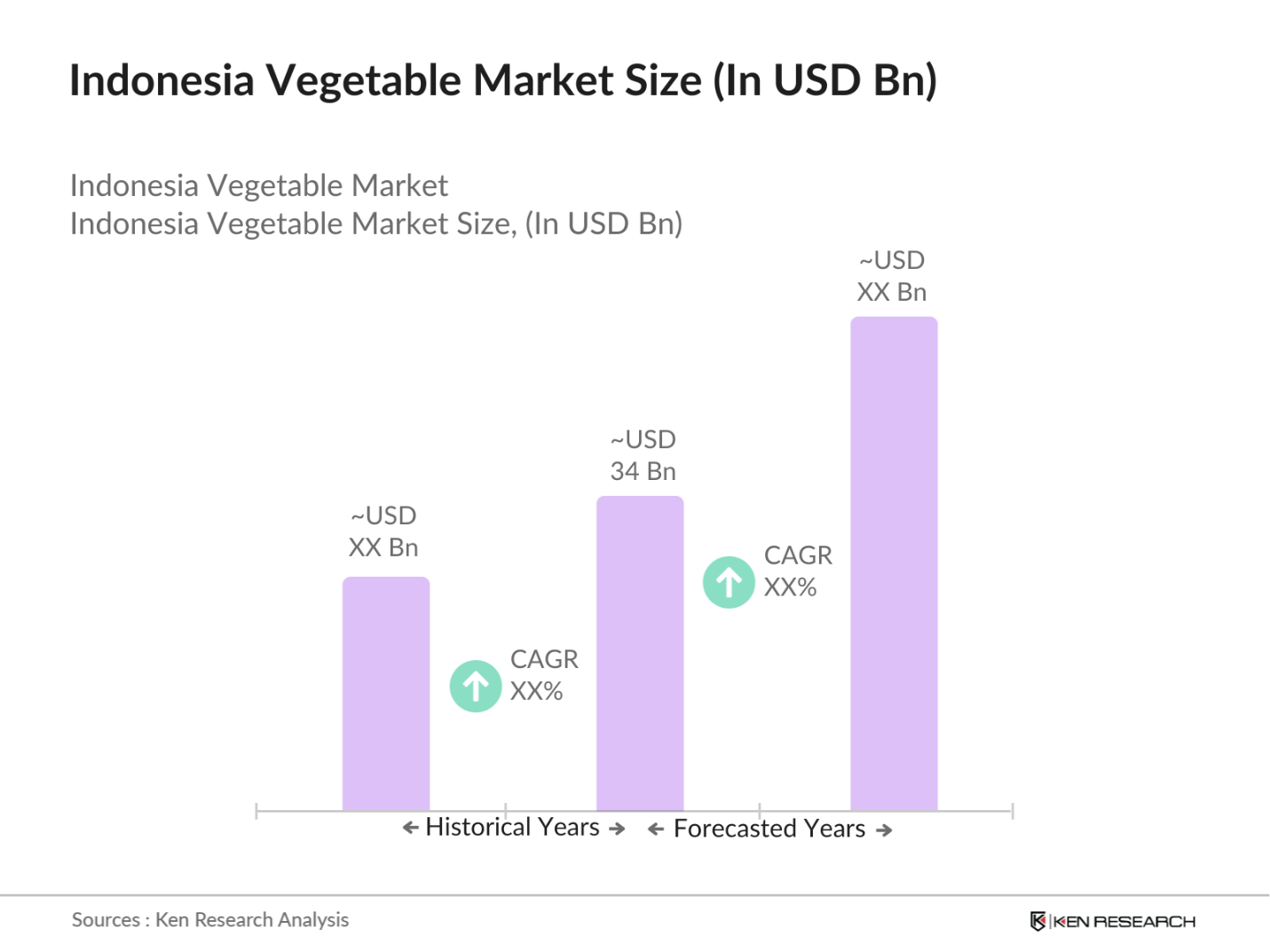

The Indonesia vegetable market is valued at USD 34 billion, driven by rising consumer demand for fresh, organic produce and an expanding export market within Southeast Asia.

Challenges include climate variability, inadequate cold chain infrastructure, and price volatility, which can affect both domestic sales and export volumes.

Major players include PT East West Seed Indonesia, PT TaniHub Group, PT Sumber Tani Agung Resources, PT BISI International Tbk, and PT Sewu Segar Nusantara, each with a strong foothold in different vegetable segments.

Key drivers include rising health consciousness, urbanization, government support for agriculture, and technological advancements such as vertical farming and hydroponics.

Trends include a shift towards organic farming, increased investment in sustainable practices, and the expansion of e-commerce as a distribution channel for fresh produce.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.