Indonesia Video Game Market Outlook to 2030

Region:Indonesia

Author(s):Mukul

Product Code:KROD6347

Region:Indonesia

Author(s):Mukul

Product Code:KROD6347

October 2024

80

Listen to the audio summary

The competitive landscape in the Indonesia video game market is marked by the presence of international giants and local companies that focus on mobile platforms and localized content. Companies like Tencent dominate the mobile game sector with games such as PUBG Mobile, while local developers focus on culturally relevant content. The emergence of local e-sports events and collaborations between gaming companies and telecom operators have further strengthened market competition.

|

Company |

Establishment Year |

Headquarters |

Platform Focus |

Revenue (2023) |

No. of Employees |

Major Games |

Regional Focus |

Market Share |

|

Tencent Games |

1998 |

Shenzhen, China |

||||||

|

Garena |

2009 |

Singapore |

||||||

|

PT Lyto Datarindo Fortuna |

2003 |

Jakarta, Indonesia |

||||||

|

Moonton |

2014 |

Shanghai, China |

||||||

|

Gameloft SE |

1999 |

Paris, France |

MarketGrowth Drivers

Market Restraints

The Indonesia video game market is expected to witness significant growth over the coming years, driven by increasing smartphone adoption, government support for e-sports, and the rising number of local developers entering the scene. The integration of advanced technologies like cloud gaming and augmented reality will also fuel market expansion. As mobile data networks improve and more affordable gaming hardware becomes available, the market will continue to diversify across demographics and regions, leading to increased revenue streams from both domestic and international players.

Market Opportunities

|

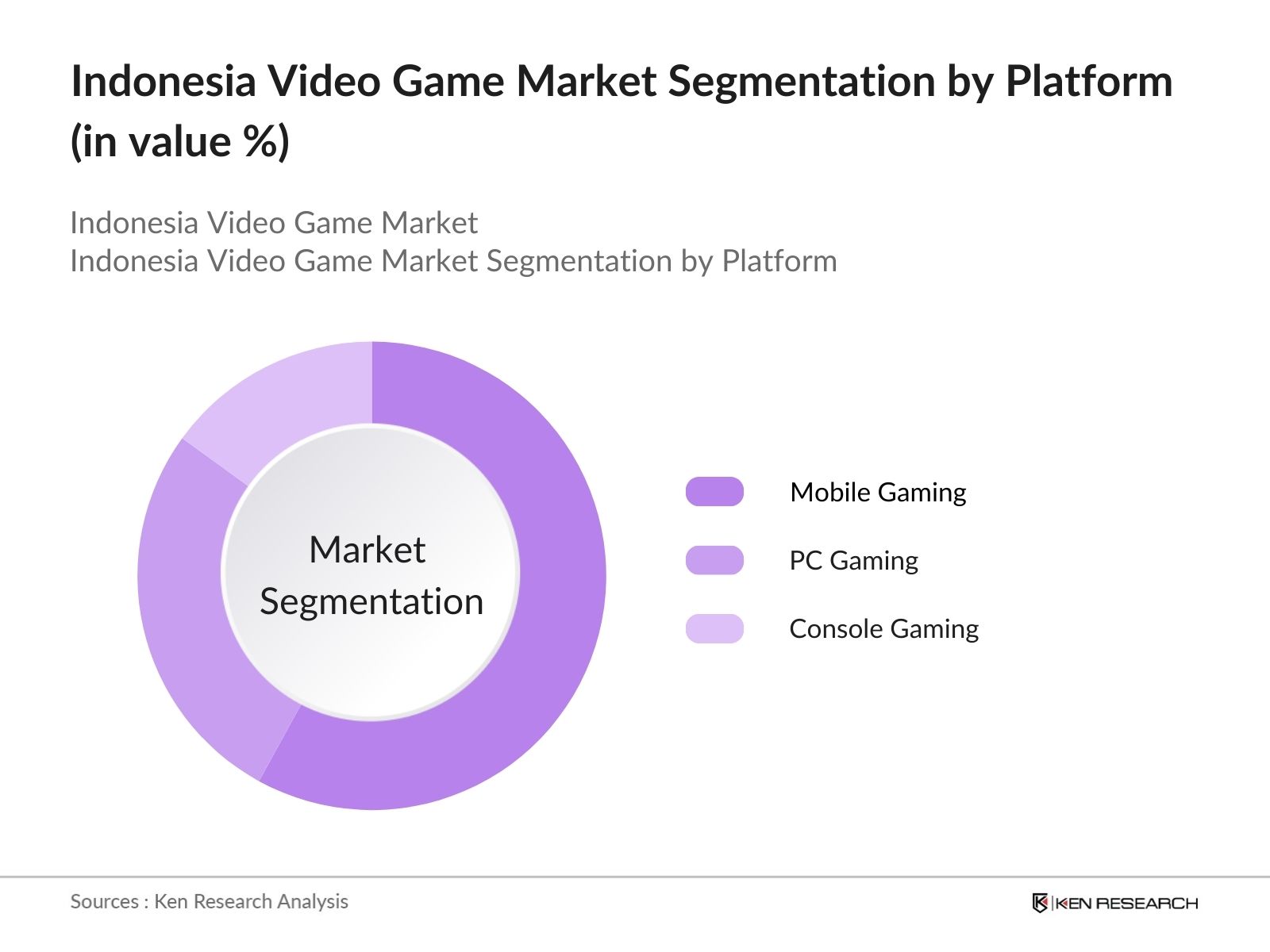

Platform |

Mobile Gaming, PC Gaming, Console Gaming |

|

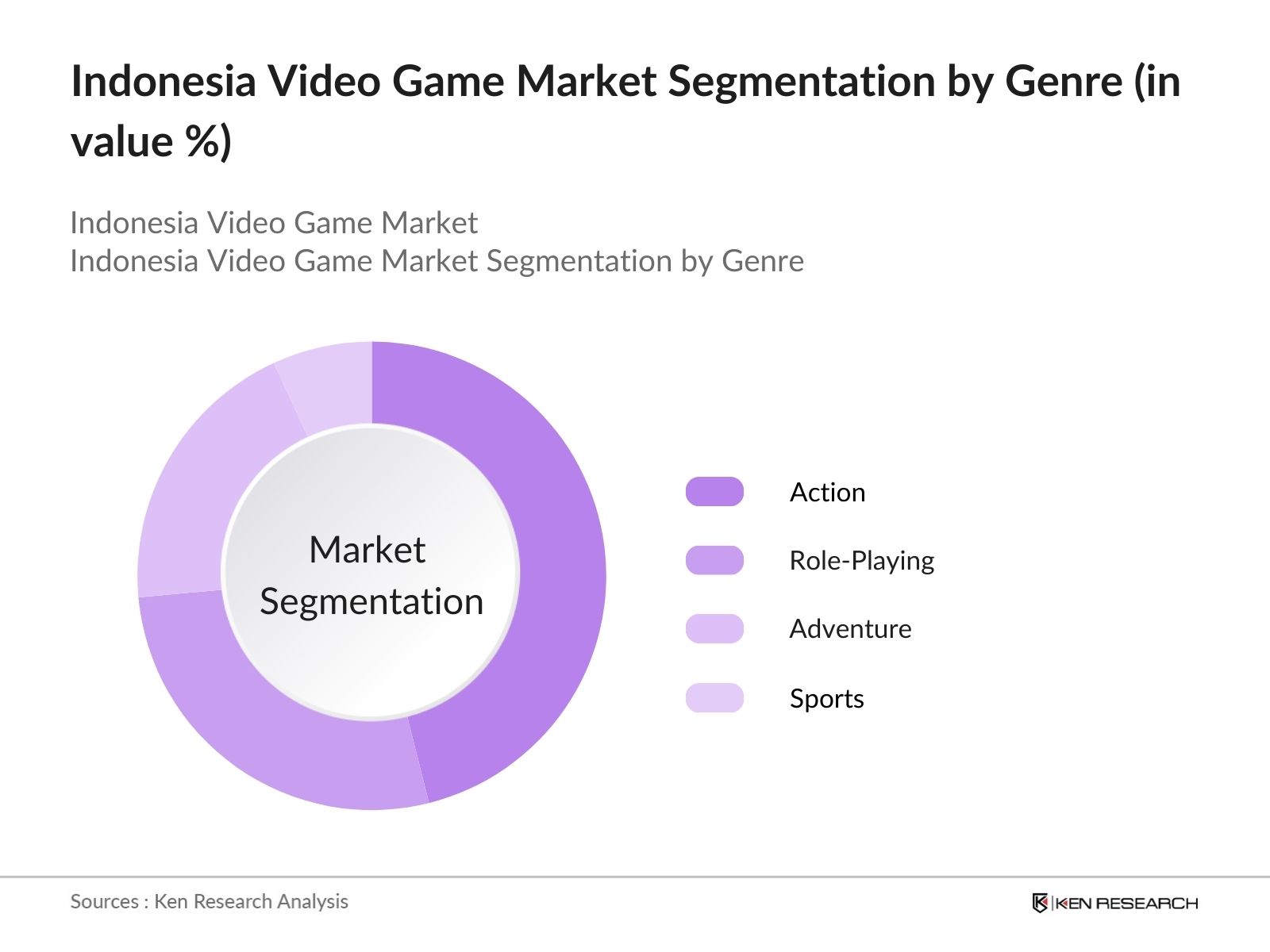

Genre |

Action, Adventure, Role-Playing, Sports, Simulation |

|

Business Model |

Free-to-Play (F2P), Pay-to-Play (P2P), Subscription-Based |

|

Distribution Channel |

Digital Stores (Google Play, Apple Store, Steam), Physical Retail |

|

Region |

Java, Sumatra, Bali & Nusa Tenggara, Kalimantan, Sulawesi |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (Digital Infrastructure, Mobile Penetration, E-Sports Expansion, In-Game Monetization)

3.1.1. Internet and Mobile Penetration

3.1.2. Rising Popularity of E-Sports

3.1.3. Increased Spending on Digital Entertainment

3.1.4. Emergence of Local Game Developers

3.2. Market Challenges (Gaming Addiction, Regulatory Challenges, Digital Divide, Data Privacy Issues)

3.2.1. Government Regulations on Game Content

3.2.2. Concerns over Data Privacy and Security

3.2.3. Competition from Global Platforms

3.2.4. Gaming Addiction among Youth

3.3. Opportunities (Cloud Gaming, VR/AR Integration, E-Sports Sponsorships, Localization of Games)

3.3.1. Integration of Virtual Reality and Augmented Reality

3.3.2. Rising Opportunities in Cloud-Based Gaming

3.3.3. Expansion of E-Sports Tournaments and Sponsorships

3.3.4. Opportunities in Game Localization and Cultural Relevance

3.4. Trends (Mobile Gaming, Indie Game Development, Subscription-Based Gaming, Streaming)

3.4.1. Increasing Mobile Gaming Popularity

3.4.2. Indie Game Development and Crowdfunding

3.4.3. Streaming Platforms Integration

3.4.4. Subscription-Based Gaming Models

3.5. Government Regulation (Digital Rights Management, Age Ratings, Intellectual Property, E-Sports Regulations)

3.5.1. Content Moderation and Digital Rights Management

3.5.2. Regulatory Landscape for E-Sports and Online Gaming

3.5.3. Intellectual Property Challenges in Game Development

3.5.4. Age-Based Content Ratings and Compliance

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces (Competitive Rivalry, Bargaining Power of Suppliers, Bargaining Power of Consumers, Threat of Substitutes, Threat of New Entrants)

3.9. Competitive Landscape Analysis

4.1. By Platform (In Value %)

4.1.1. Mobile Gaming

4.1.2. PC Gaming

4.1.3. Console Gaming

4.2. By Genre (In Value %)

4.2.1. Action

4.2.2. Adventure

4.2.3. Role-Playing

4.2.4. Sports

4.2.5. Simulation

4.3. By Business Model (In Value %)

4.3.1. Free-to-Play (F2P)

4.3.2. Pay-to-Play (P2P)

4.3.3. Subscription-Based

4.4. By Distribution Channel (In Value %)

4.4.1. Digital Stores (Google Play, Apple Store, Steam)

4.4.2. Physical Retail

4.5. By Region (In Value %)

4.5.1. Java

4.5.2. Sumatra

4.5.3. Bali & Nusa Tenggara

4.5.4. Kalimantan

4.5.5. Sulawesi

5.1. Detailed Profiles of Major Competitors (Revenue, Market Share, Key Products, Strategies)

5.1.1. Garena

5.1.2. Tencent Games

5.1.3. NetEase

5.1.4. PT Lyto Datarindo Fortuna

5.1.5. Gameloft SE

5.1.6. Moonton

5.1.7. Electronic Arts

5.1.8. Ubisoft

5.1.9. GungHo Online Entertainment

5.1.10. MiHoYo

5.1.11. Valve Corporation

5.1.12. Sony Interactive Entertainment

5.1.13. Microsoft Studios

5.1.14. Activision Blizzard

5.1.15. Rovio Entertainment

5.2. Cross Comparison Parameters (Headquarters, Inception Year, No. of Employees, Revenue, Game Library, Genre Focus, Platform Focus, Regional Market Focus)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Sponsorships, Game Launches)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Content Regulations and Age Restrictions

6.2. Intellectual Property Protections

6.3. Online Gambling Laws

6.4. Consumer Data Protection Laws

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Platform (In Value %)

8.2. By Genre (In Value %)

8.3. By Business Model (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Segment Insights

9.3. Marketing Initiatives

9.4. White Space Opportunities

In this phase, we construct a comprehensive map of the Indonesia video game market, identifying all major players including developers, publishers, and distributors. Extensive desk research is conducted using industry databases to identify key market variables such as mobile penetration rates, consumer spending, and gaming demographics.

This step involves collecting and analyzing historical data on the Indonesia video game market, with a particular focus on mobile and PC gaming penetration, average revenue per user (ARPU), and e-sports participation. Both qualitative and quantitative methods are employed to ensure the reliability of revenue and growth estimates.

Market hypotheses are developed based on the initial data collection and are validated through in-depth interviews with industry experts from leading game development firms. These consultations provide insights into operational strategies, game launches, and market entry challenges.

The final synthesis phase involves integrating the qualitative insights gained from expert consultations with the quantitative market data. This ensures the report provides a holistic, validated view of the Indonesia video game market, identifying both current trends and future opportunities.

01. How big is the Indonesia Video Game Market?

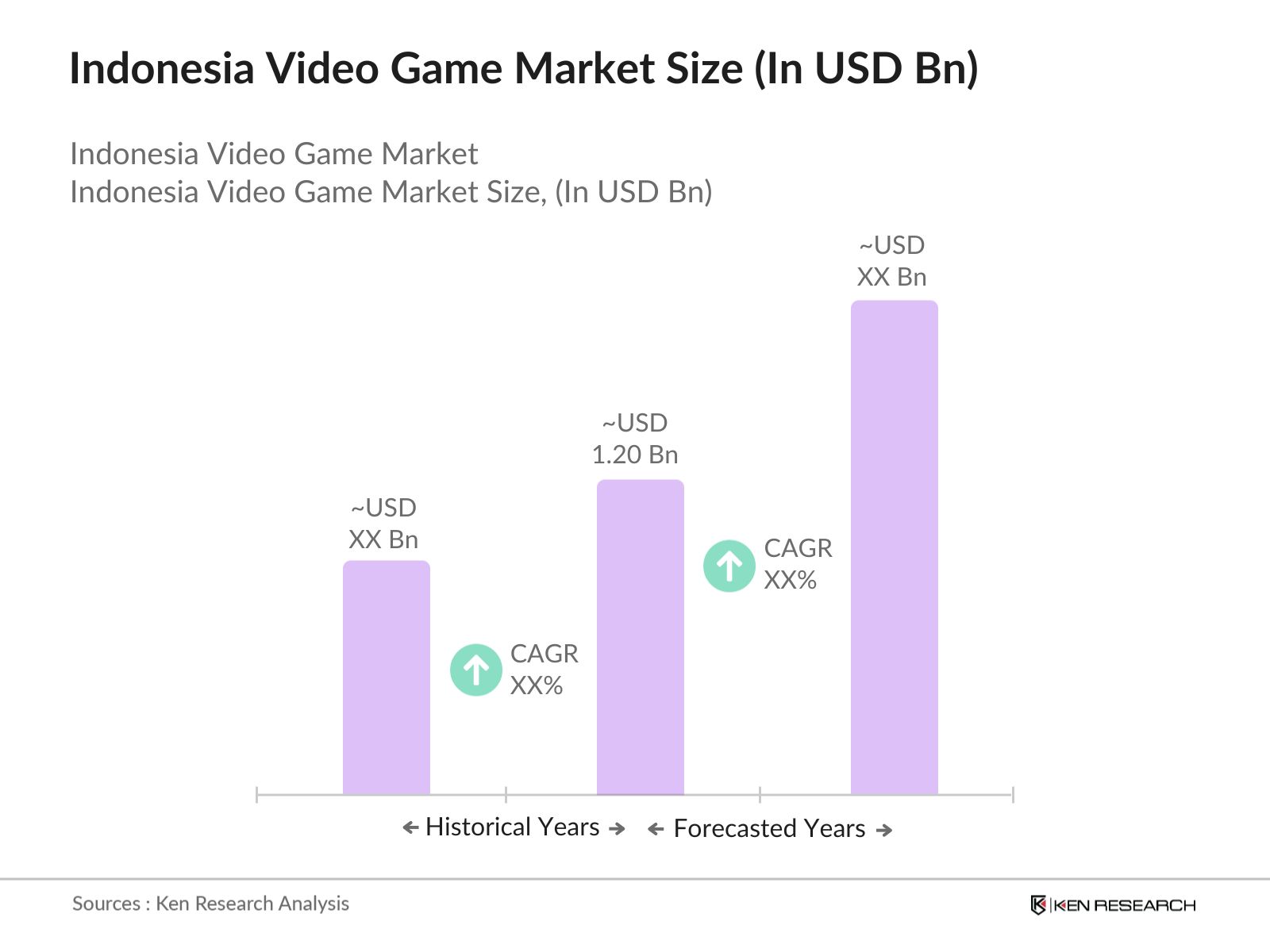

The Indonesia video game market is valued at USD 1.20 billion, driven by a large mobile gaming population and the growing influence of e-sports.

Challenges include government regulations on game content, data privacy concerns, and the digital divide, which limits access to high-speed internet in rural areas.

Major players in the market include Tencent Games, Garena, PT Lyto Datarindo Fortuna, Moonton, and Gameloft SE, all of which have a strong focus on mobile gaming.

The market is driven by mobile gaming, increasing smartphone penetration, rising popularity of e-sports, and strong consumer interest in digital entertainment and in-game purchases.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.