Indonesia Wine Market Outlook to 2030

Region:Indonesia

Author(s):Yogita Sahu

Product Code:KROD9471

Region:Indonesia

Author(s):Yogita Sahu

Product Code:KROD9471

December 2024

95

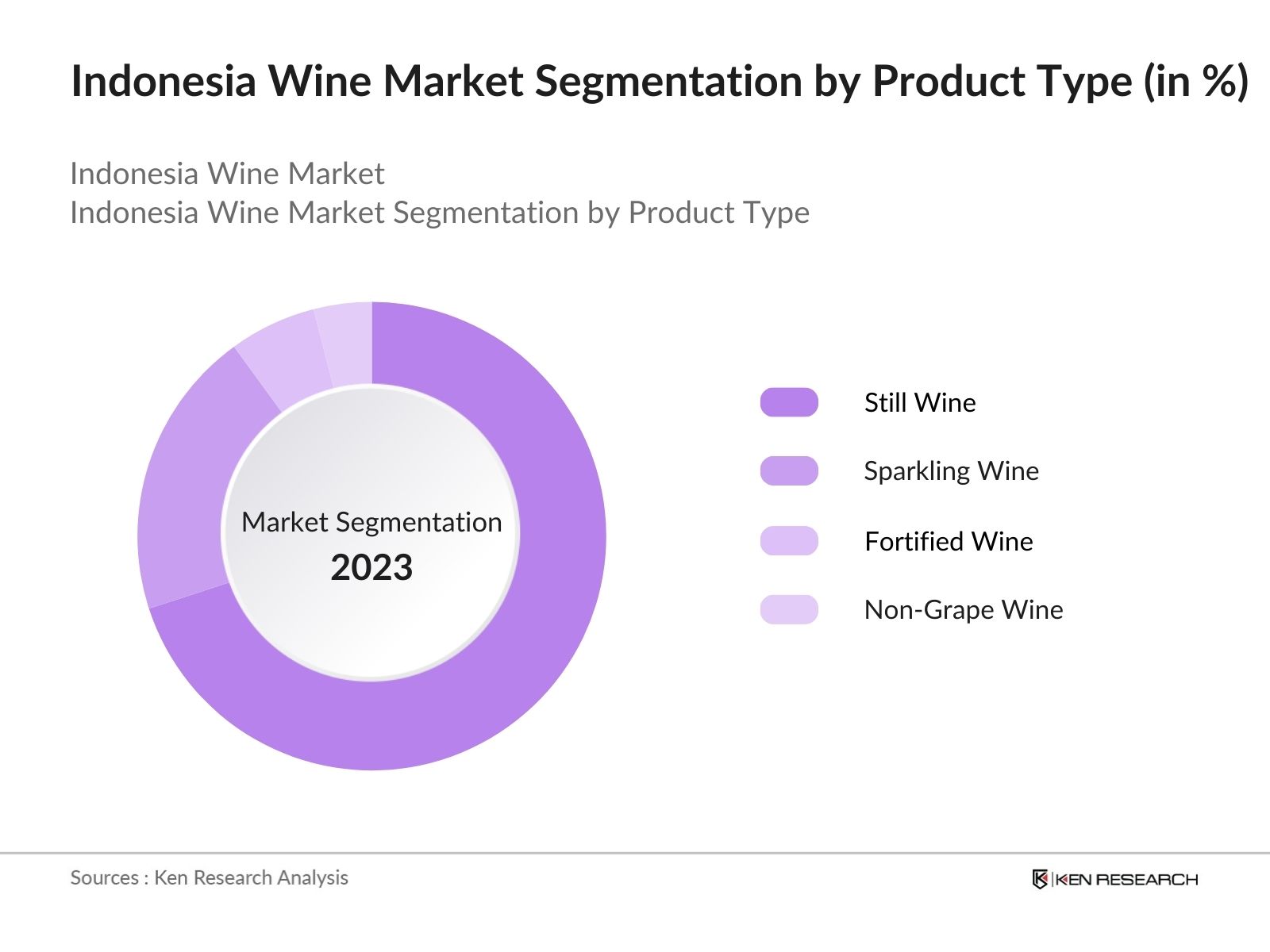

By Product Type: The market is segmented by product type into still wine, sparkling wine, fortified wine, and non-grape wine. Recently, still wine has dominated the market, driven by its popularity among locals and expatriates. Still wine's affordability and wide range of options, from local to imported varieties, make it a favorite for both casual consumption and formal gatherings.

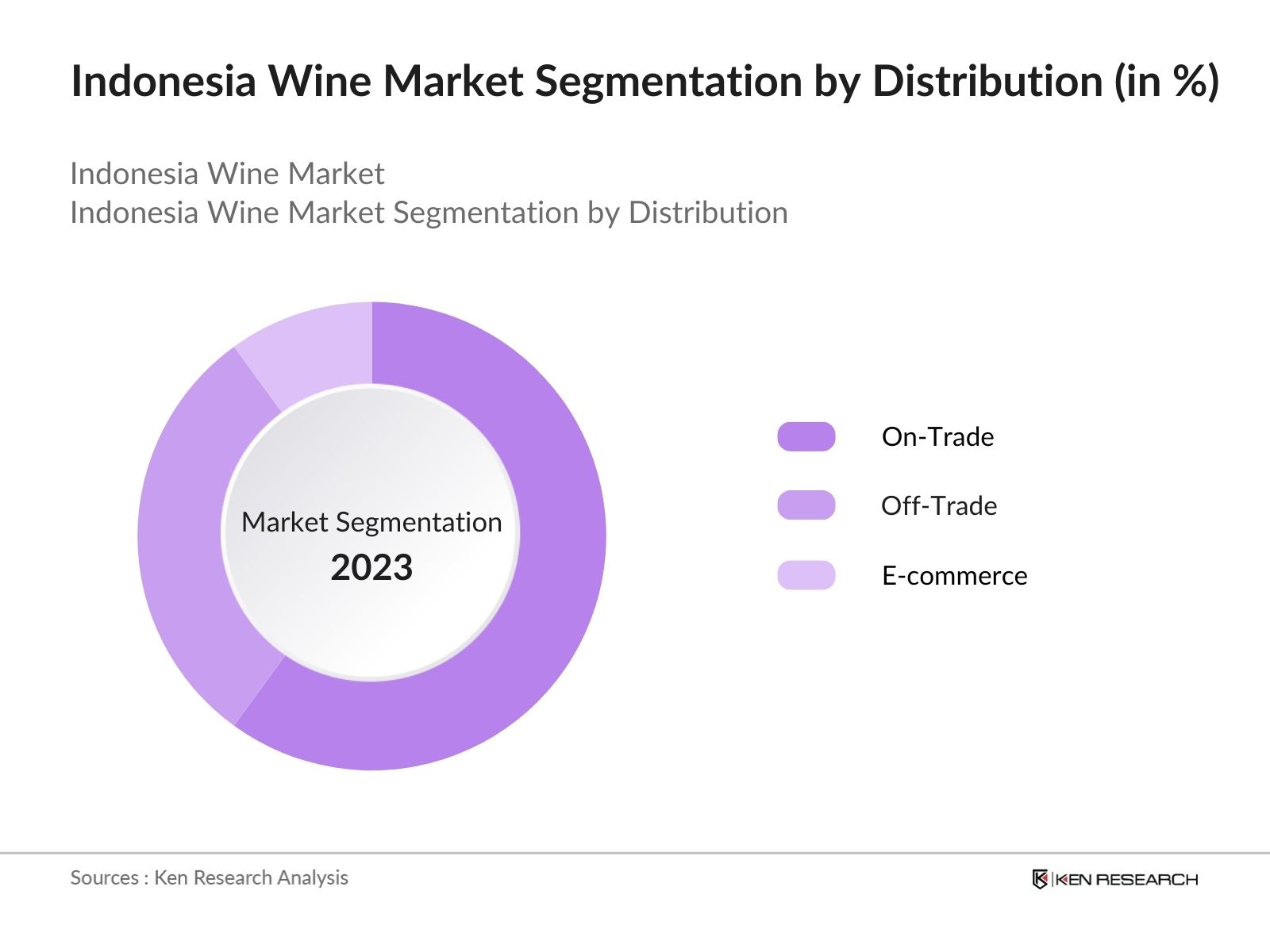

By Distribution Channel: The market is also segmented by distribution channels into on-trade (restaurants, hotels, bars), off-trade (supermarkets, hypermarkets, and specialty stores), and e-commerce. On-trade dominates the distribution, especially in tourist-heavy areas like Bali, where wine is a key offering in high-end restaurants and resorts. Off-trade, while less dominant, has grown steadily due to wine retailing in urban supermarkets.

The market is characterized by a blend of local and international players. Local brands such as Hatten Wines have a strong presence in the domestic market, especially in regions like Bali, leveraging local production and cultural integration.

|

Company Name |

Establishment Year |

Headquarters |

No. of Employees |

Revenue |

Product Type |

Market Presence |

Global Reach |

Brand Strength |

Strategic Initiatives |

|

Hatten Wines |

1994 |

Bali, Indonesia |

|||||||

|

Orang Tua Group |

1948 |

Jakarta, Indonesia |

|||||||

|

Diageo |

1997 |

London, UK |

|||||||

|

Pernod Ricard |

1975 |

Paris, France |

|||||||

|

Treasury Wine Estates |

2011 |

Melbourne, Australia |

Over the next five years, the Indonesia wine industry is expected to witness growth driven by tourism recovery, increasing consumer interest in premium and organic wines, and rising adoption of wine in urban social settings.

|

Product Type |

Still Wine Sparkling Wine Fortified Wine Non-Grape Wine |

|

Distribution Channel |

On-Trade (Restaurants, Hotels, Bars) Off-Trade (Supermarkets, Hypermarkets, Specialty Stores) E-commerce |

|

Consumer Group |

Tourists and Expats Domestic Urban Consumers Millennials and Young Professionals |

|

Packaging Type |

Glass Bottles Boxed Wine Canned Wine |

|

Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Growing Domestic Wine Consumption (local production focus)

3.1.2. Tourism and Expatriate Demand (impact of tourism on wine consumption)

3.1.3. Rise of E-commerce Channels (shift to online wine sales)

3.1.4. Cultural Integration of Wine (wine in celebrations and social events)

3.2. Market Challenges

3.2.1. High Import Duties (government tariffs and taxes on imports)

3.2.2. Regulatory Restrictions on Alcoholic Beverages

3.2.3. Lack of Local Raw Materials (grape scarcity and climate limitations)

3.3. Opportunities

3.3.1. Expansion of Local Wine Brands (Hatten Wines and others)

3.3.2. Growth in On-Trade Channels (restaurants, hotels, bars)

3.3.3. Introduction of Organic and Low-Alcohol Wines (consumer health trends)

3.4. Trends

3.4.1. Preference for Premium and Imported Wines (shift to high-quality products)

3.4.2. Increased Consumption in Urban Areas (urban demographics driving demand)

3.4.3. Rise of non-Grape Wines (fruit and herbal wines)

3.5. Government Regulation

3.5.1. Alcohol Taxation Policies (import duties and local taxes)

3.5.2. Legal Restrictions on Sales and Advertising

3.5.3. Changes in Licensing Requirements for On-Trade Sales

3.6. SWOT Analysis

3.7. Porters Five Forces

3.8. Competition Ecosystem

4.1. By Product Type (In Value)

4.1.1. Still Wine

4.1.2. Sparkling Wine

4.1.3. Fortified Wine

4.1.4. Non-Grape Wine

4.2. By Distribution Channel (In Value)

4.2.1. On-Trade (Restaurants, Hotels, Bars)

4.2.2. Off-Trade (Supermarkets, Hypermarkets, Specialty Stores)

4.2.3. E-commerce

4.3. By Consumer Group (In Value)

4.3.1. Tourists and Expats

4.3.2. Domestic Urban Consumers

4.3.3. Millennials and Young Professionals

4.4. By Packaging Type (In Value)

4.4.1. Glass Bottles

4.4.2. Boxed Wine

4.4.3. Canned Wine

4.5. By Region (In Value)

4.5.1. North

4.5.2. East

4.5.3. West

4.5.4. South

5.1. Detailed Profiles of Major Companies

5.1.1. Hatten Wines

5.1.2. Orang Tua Group

5.1.3. LVMH Mot Hennessy

5.1.4. Diageo

5.1.5. Pernod Ricard

5.1.6. Treasury Wine Estates

5.1.7. Constellation Brands

5.1.8. Castel Group

5.1.9. Accolade Wines

5.1.10. The Wine Group

5.1.11. E&J Gallo Winery

5.1.12. Bacardi Limited

5.1.13. Campari Group

5.1.14. Brown-Forman

5.1.15. Bronco Wine Company

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Distribution Channels, Market Penetration, Brand Positioning, Local vs. Imported Share)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

6.1. Alcohol Taxation Policies

6.2. Compliance and Certification Requirements

6.3. Regulatory Changes in Import/Export Laws

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value)

8.2. By Distribution Channel (In Value)

8.3. By Consumer Group (In Value)

8.4. By Packaging Type (In Value)

8.5. By Region (In Value)

9.1. TAM/SAM/SOM Analysis

9.2. White Space Opportunity Analysis

9.3. Marketing and Promotional Strategies

The research began with mapping key stakeholders within the Indonesia wine market. Extensive desk research was conducted using proprietary databases and verified secondary sources to gather relevant industry-level data. This process helped in defining the core variables that influence market dynamics, such as consumer trends, distribution networks, and regulatory factors.

Historical data related to market penetration, revenue growth, and market size were compiled and analyzed. This phase also included segmentation analysis to identify key trends in on-trade and off-trade channels. Multiple data points were cross-verified to ensure accuracy.

Market hypotheses were tested through structured interviews with industry professionals, including wine producers, distributors, and retail chains. These consultations provided insights into operational challenges and future market trends, helping validate initial research findings.

The final step involved synthesizing data from multiple sources and interviews to produce a comprehensive market report. The findings were further refined through interaction with local stakeholders to ensure relevance and accuracy for the Indonesia wine market.

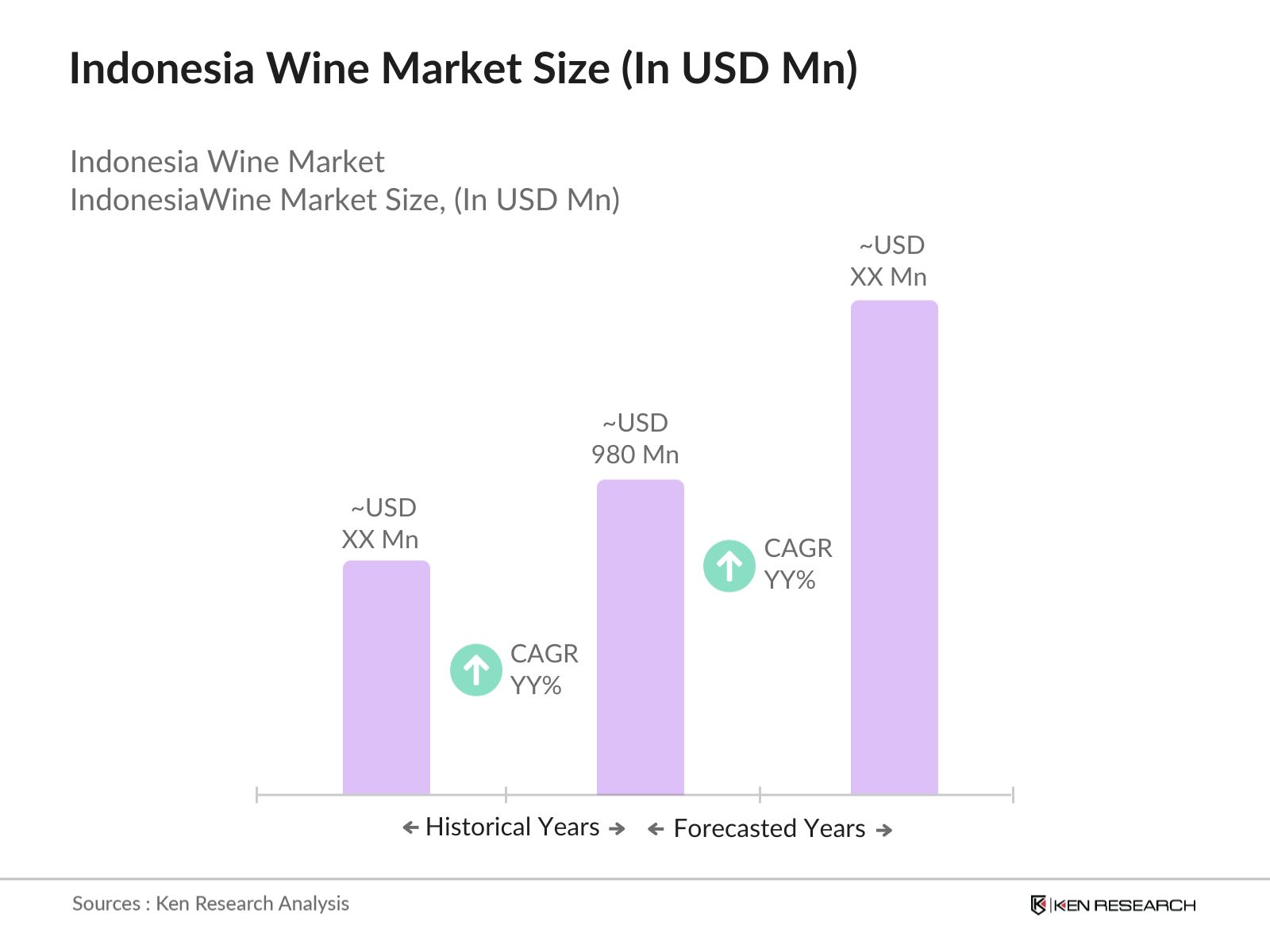

The Indonesia wine market is valued at USD 980 million, reflecting its slow but steady recovery, driven by a combination of tourism and local wine culture integration.

Key challenges in the Indonesia wine market include high import duties, regulatory restrictions on alcohol sales, and limited local production capacity due to climate limitations affecting grape cultivation.

Major players in the Indonesia wine market include local brands like Hatten Wines and Orang Tua, as well as international companies such as Diageo, Pernod Ricard, and Treasury Wine Estates.

Tourism recovery, increasing consumer interest in premium and organic wines, and the rise of e-commerce platforms are key drivers of Indonesia wine market growth.

Future trends in the Indonesia wine market include the growing popularity of non-grape wines, expansion of e-commerce wine sales, and an increasing shift towards premium and organic wine products among affluent consumers.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.