Iraq Auto Accessories Market Outlook to 2030

Region:Iraq

Author(s):Samanyu

Product Code:KROD9630

Region:Iraq

Author(s):Samanyu

Product Code:KROD9630

October 2024

90

Listen to the audio summary

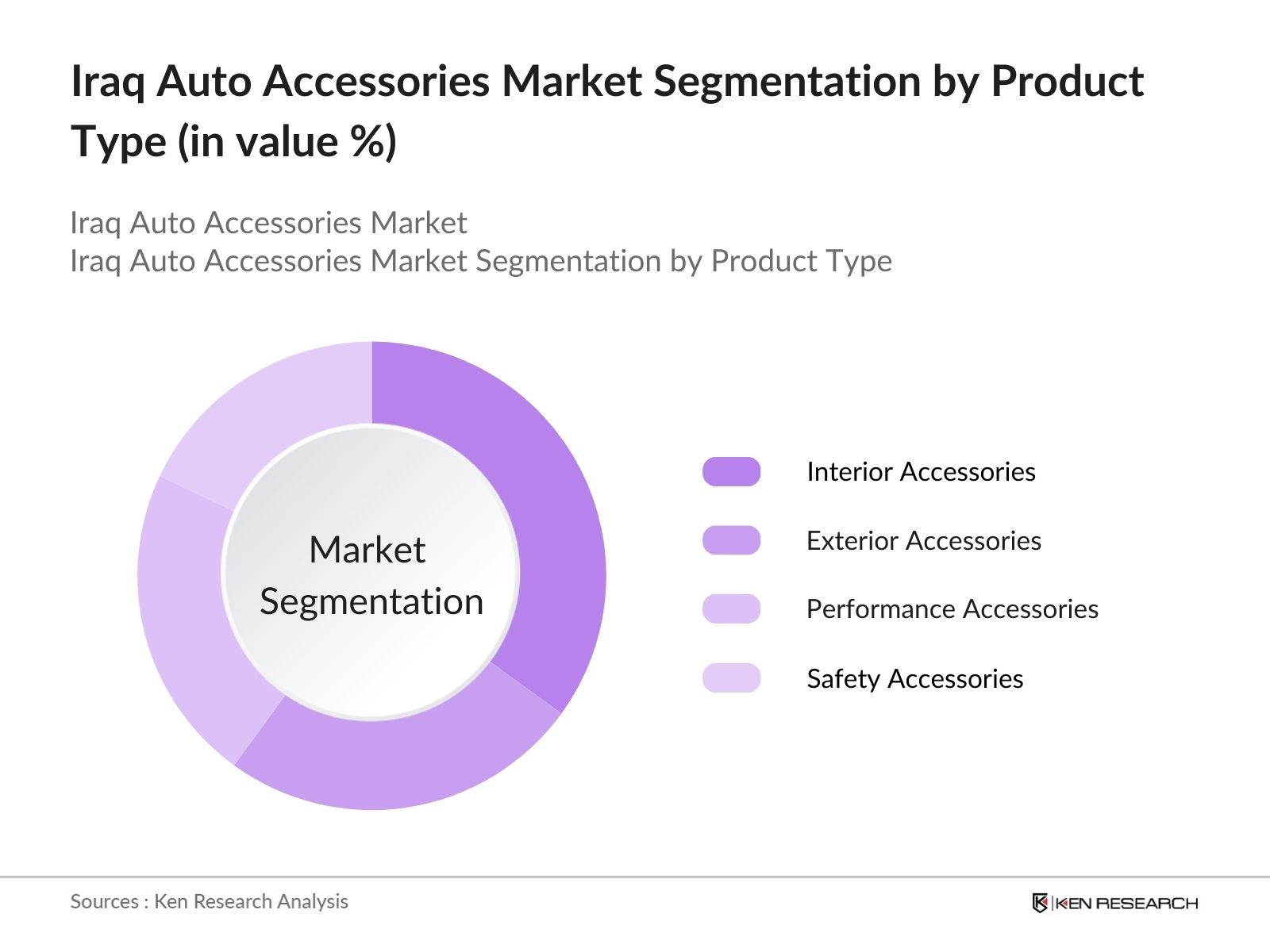

By Product Type: The market is segmented by product type into performance accessories, interior accessories, exterior accessories, and safety accessories. Interior accessories currently hold a dominant market share in this category. The demand for products such as seat covers, dash covers, and car mats has been high due to the extreme weather conditions in Iraq. These accessories not only offer comfort but also provide protection from the intense heat and dust. As many car owners in Iraq prioritize maintaining the interior aesthetics of their vehicles, this sub-segment is expected to continue its dominance.

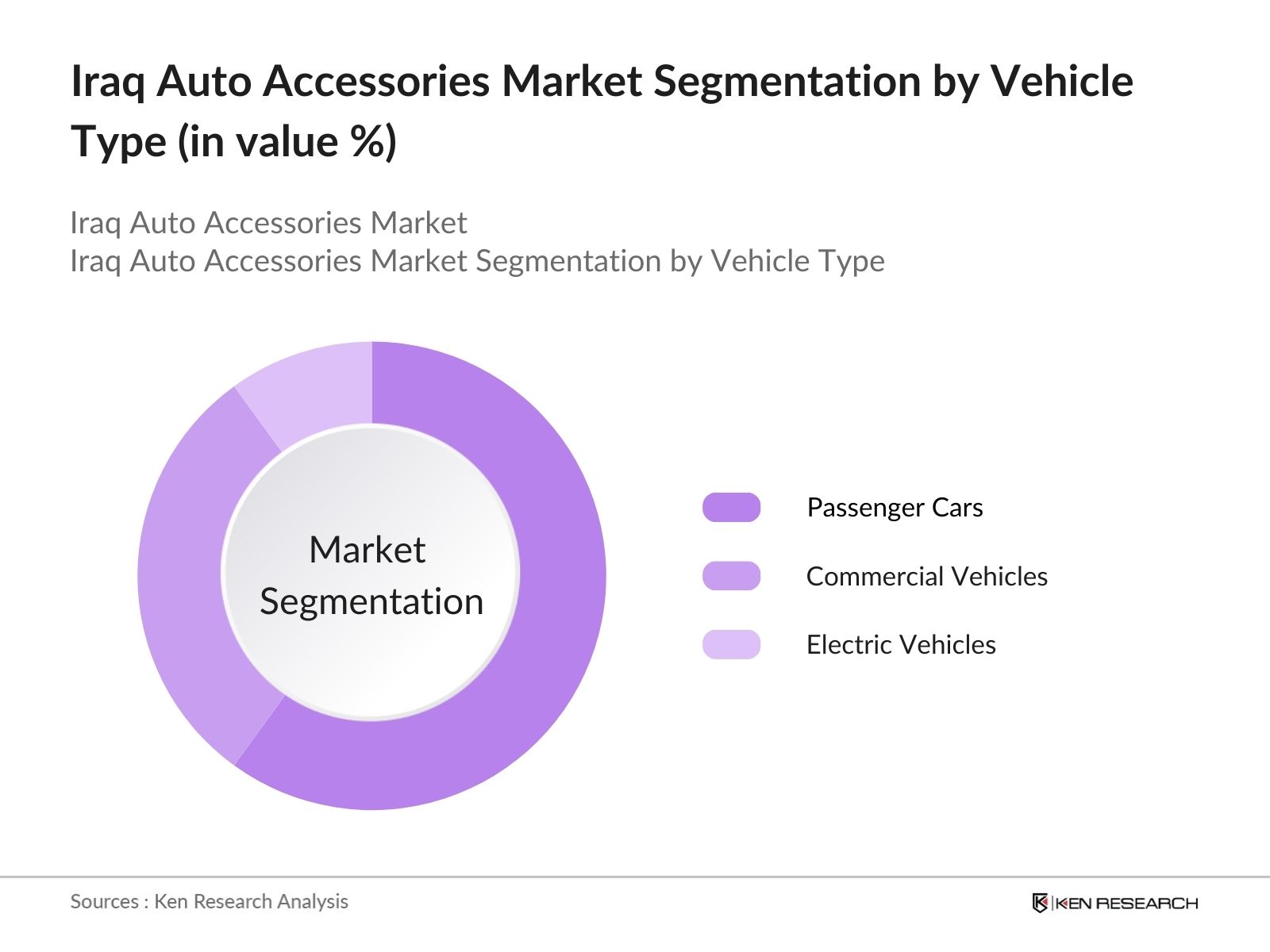

By Vehicle Type: The market is segmented by vehicle type into passenger cars, commercial vehicles, and electric vehicles. Passenger cars hold the dominant share in this segment due to the rising trend of car ownership in urban centers, with a focus on customization and comfort. The growth of the urban population and their preference for personal mobility, especially in cities like Baghdad and Erbil, has led to the increased sale of auto accessories for passenger cars. Furthermore, consumer preference for sedan and SUV models, which often require more accessories, is driving demand in this sub-segment.

The Iraq Auto Accessories market is characterized by the presence of a mix of global giants and regional players. The market is dominated by companies offering a wide range of products, from performance accessories to safety upgrades. These companies have strong distribution networks across the country, particularly in urban centers like Baghdad and Basra, allowing them to cater to a wide customer base. The competitive landscape is shaped by collaborations between manufacturers and local distributors, which helps in strengthening market presence and increasing product availability.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (2023) |

Employees |

Key Product |

Distribution Channels |

Key Clients |

Global Presence |

|

Denso Corporation |

1949 |

Japan |

||||||

|

Bosch Auto Parts |

1886 |

Germany |

||||||

|

Toyota Tsusho Corporation |

1948 |

Japan |

||||||

|

Valeo S.A. |

1923 |

France |

||||||

|

Continental AG |

1871 |

Germany |

Growth Drivers

Market Challenges

Over the next five years, the Iraq Auto Accessories market is expected to witness significant growth, driven by the increasing adoption of smart accessories, government initiatives supporting local manufacturing, and a growing focus on vehicle safety. The rise of e-commerce and digital platforms is likely to further boost the sale of auto accessories, as consumers seek more convenient ways to purchase these products. Additionally, advancements in vehicle technology, such as electric vehicles and connected car systems, are likely to create new opportunities for accessory manufacturers.

Future Market Opportunities

|

By Product Type |

Performance Accessories Interior Accessories Exterior Accessories Safety Accessories |

|

By Vehicle Type |

Passenger Cars Commercial Vehicles Electric Vehicles |

|

By Technology |

Smart Accessories Conventional Accessories |

|

By Sales Channel |

Offline Online |

|

By Region |

Baghdad Basra Erbil Mosul Sulaymaniyah |

1.1. Definition and Scope (Auto Accessories: Performance, Interior, Exterior, Safety)

1.2. Market Taxonomy (Product, Distribution Channel, End User)

1.3. Market Growth Rate (CAGR, Demand Forecasts, Revenue Projections)

1.4. Market Segmentation Overview (Product Type, Vehicle Type, Technology, Sales Channel, Region)

2.1. Historical Market Size (Market Trends, GDP Impact, Consumer Preferences)

2.2. Year-On-Year Growth Analysis (Growth Rates, Sector-wise Contribution)

2.3. Key Market Developments and Milestones (Investment Announcements, Policy Changes)

3.1. Growth Drivers

3.1.1. Increasing Vehicle Ownership (Rising Middle Class, Urbanization)

3.1.2. Consumer Preferences for Vehicle Customization (Exterior & Interior)

3.1.3. Expansion of Aftermarket Services (Repair, Maintenance, Parts)

3.1.4. Demand for Improved Vehicle Safety (Airbags, Braking Systems)

3.2. Restraints

3.2.1. Price Sensitivity (Economic Fluctuations, Consumer Budgeting)

3.2.2. Low Adoption of Premium Accessories (Brand Loyalty, Awareness)

3.2.3. Unorganized Distribution Channels (Local Market Dependency)

3.2.4. Regulatory Restrictions (Import Duties, Local Production Mandates)

3.3. Opportunities

3.3.1. Growth in Online Retail (E-commerce, Digital Marketing)

3.3.2. Expansion into Rural and Semi-Urban Areas (Service Penetration)

3.3.3. Government Initiatives (Local Manufacturing, Auto Sector Incentives)

3.3.4. Rising Popularity of Electric Vehicles (EV Accessories, Battery Market)

3.4. Trends

3.4.1. Integration of Smart Accessories (IoT-enabled Accessories, Smart Dashcams)

3.4.2. Focus on Sustainable Accessories (Eco-friendly, Recycled Materials)

3.4.3. Customization and Aesthetic Enhancements (Car Wrapping, Chrome Parts)

3.4.4. Increased Demand for Comfort Accessories (Seat Covers, In-car Entertainment)

3.5. Government Regulation

3.5.1. Local Production Policies (Tariff Structures, Auto Accessory Regulations)

3.5.2. Trade Agreements (Import Restrictions, Bilateral Trade Pacts)

3.5.3. Emission Standards (Pollution Control, Vehicle Compliance)

3.5.4. Vehicle Safety Regulations (Mandatory Accessories, Safety Audits)

3.6. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7. Stakeholder Ecosystem (Manufacturers, Distributors, Retailers, Consumers)

3.8. Porter’s Five Forces (Supplier Power, Buyer Power, Competitive Rivalry, Threat of New Entrants, Threat of Substitutes)

3.9. Competitive Landscape

4.1. By Product Type (In Value %)

4.1.1. Performance Accessories (Exhaust Systems, Air Filters)

4.1.2. Interior Accessories (Seat Covers, Dash Covers, Car Mats)

4.1.3. Exterior Accessories (Bumpers, Spoilers, Chrome Accessories)

4.1.4. Safety Accessories (Airbags, Sensors, Alarms)

4.2. By Vehicle Type (In Value %)

4.2.1. Passenger Cars (Sedans, SUVs, Hatchbacks)

4.2.2. Commercial Vehicles (Trucks, Buses, Vans)

4.2.3. Electric Vehicles (EV-Specific Accessories)

4.3. By Technology (In Value %)

4.3.1. Smart Accessories (Bluetooth, Connected Devices)

4.3.2. Conventional Accessories (Standard Safety, Comfort)

4.4. By Sales Channel (In Value %)

4.4.1. Offline (Authorized Dealers, Retailers)

4.4.2. Online (E-commerce, Brand Websites)

4.5. By Region (In Value %)

4.5.1. Baghdad

4.5.2. Basra

4.5.3. Erbil

4.5.4. Mosul

4.5.5. Sulaymaniyah

5.1. Detailed Profiles of Major Companies

5.1.1. Denso Corporation

5.1.2. Bosch Auto Parts

5.1.3. Toyota Tsusho Corporation

5.1.4. Magna International

5.1.5. Minda Corporation

5.1.6. Lear Corporation

5.1.7. Valeo S.A.

5.1.8. Panasonic Automotive Systems

5.1.9. Yazaki Corporation

5.1.10. Hella GmbH

5.1.11. Sumitomo Electric Industries

5.1.12. Pioneer Corporation

5.1.13. Delphi Technologies

5.1.14. Autoliv Inc.

5.1.15. Continental AG

5.2. Cross Comparison Parameters (Revenue, Global Presence, Market Share, Production Facilities, Technology Partnerships)

5.3. Market Share Analysis (Top Players, Market Fragmentation)

5.4. Strategic Initiatives (Product Launches, Regional Expansions, R&D Investments)

5.5. Mergers and Acquisitions (Recent Deals, Industry Impact)

5.6. Investment Analysis (Funding, Capital Expenditure)

5.7. Venture Capital and Private Equity Funding (Startups, Innovation Hubs)

5.8. Government Grants (Subsidies, Local Development Projects)

6.1. Industry Standards (Compliance with International Regulations, Quality Certifications)

6.2. Environmental Standards (Waste Management, Sustainable Manufacturing Practices)

6.3. Import/Export Regulations (Tariffs, Import Licensing)

7.1. Future Market Size Projections (Growth Trends, Innovation Potential)

7.2. Key Factors Driving Future Market Growth (Technology, Consumer Trends)

8.1. By Product Type (In Value %)

8.2. By Vehicle Type (In Value %)

8.3. By Technology (In Value %)

8.4. By Sales Channel (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Market Entry Strategies

9.3. Product Differentiation Strategies

9.4. Consumer Insight Analysis

9.5. Emerging Opportunities

The first phase involves the construction of an ecosystem map that includes all major stakeholders within the Iraq Auto Accessories Market. Extensive desk research, supported by secondary and proprietary databases, will be used to collect industry-level information. The primary goal of this phase is to identify and define critical market dynamics.

In this step, we analyze historical data related to the Iraq Auto Accessories Market, evaluating market penetration, market share of key companies, and revenue generation. An assessment of the quality-of-service providers will also be conducted to ensure the reliability of revenue estimates.

Market hypotheses will be formulated and validated through interviews with industry experts using computer-assisted telephone interviews (CATIs). These insights from industry practitioners will help refine and verify the data collected during previous steps.

The final phase involves synthesizing research through direct engagement with key automotive accessory manufacturers. This engagement will provide insights into product sales, consumer preferences, and market trends, ensuring a comprehensive and accurate analysis of the Iraq Auto Accessories Market.

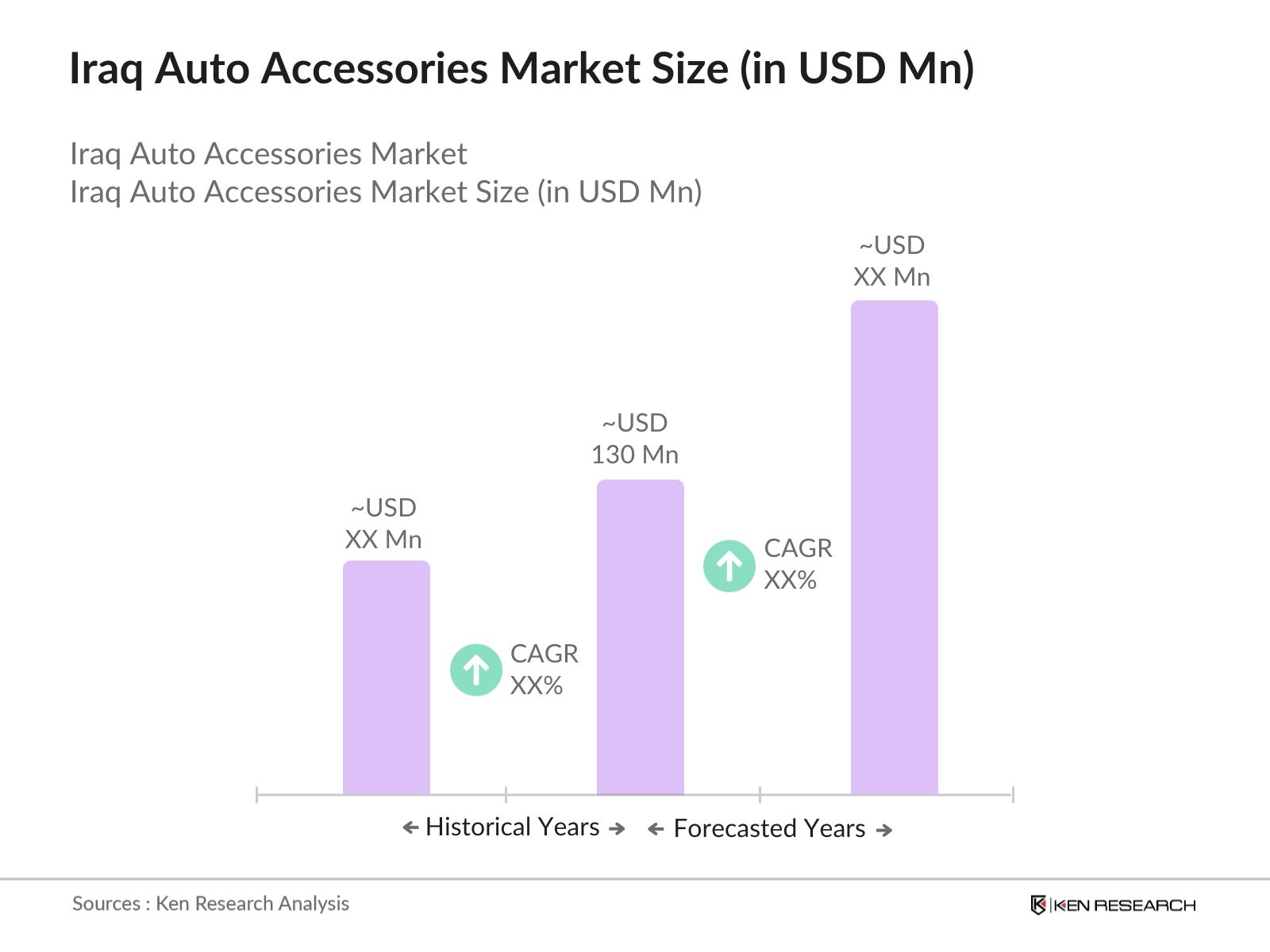

The Iraq Auto Accessories market is valued at USD 130 million, driven by increasing vehicle ownership, consumer preference for customization, and expanding aftermarket services.

Challenges in Iraq Auto Accessories market include unorganized distribution channels, high dependency on imports, and regulatory hurdles, especially around safety and environmental standards. Additionally, price sensitivity remains a significant issue for market growth.

Key players in Iraq Auto Accessories market include Denso Corporation, Bosch Auto Parts, Toyota Tsusho Corporation, Valeo S.A., and Continental AG, all of which have established strong distribution networks and brand presence in Iraq.

The Iraq Auto Accessories market is driven by rising vehicle ownership, increased demand for vehicle safety enhancements, and consumer preferences for interior and exterior customization.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.