KSA Ammonia Market Outlook to 2030

Region:Saudi Arabia

Author(s):Sanjna Verma

Product Code:KROD6614

Region:Saudi Arabia

Author(s):Sanjna Verma

Product Code:KROD6614

December 2024

82

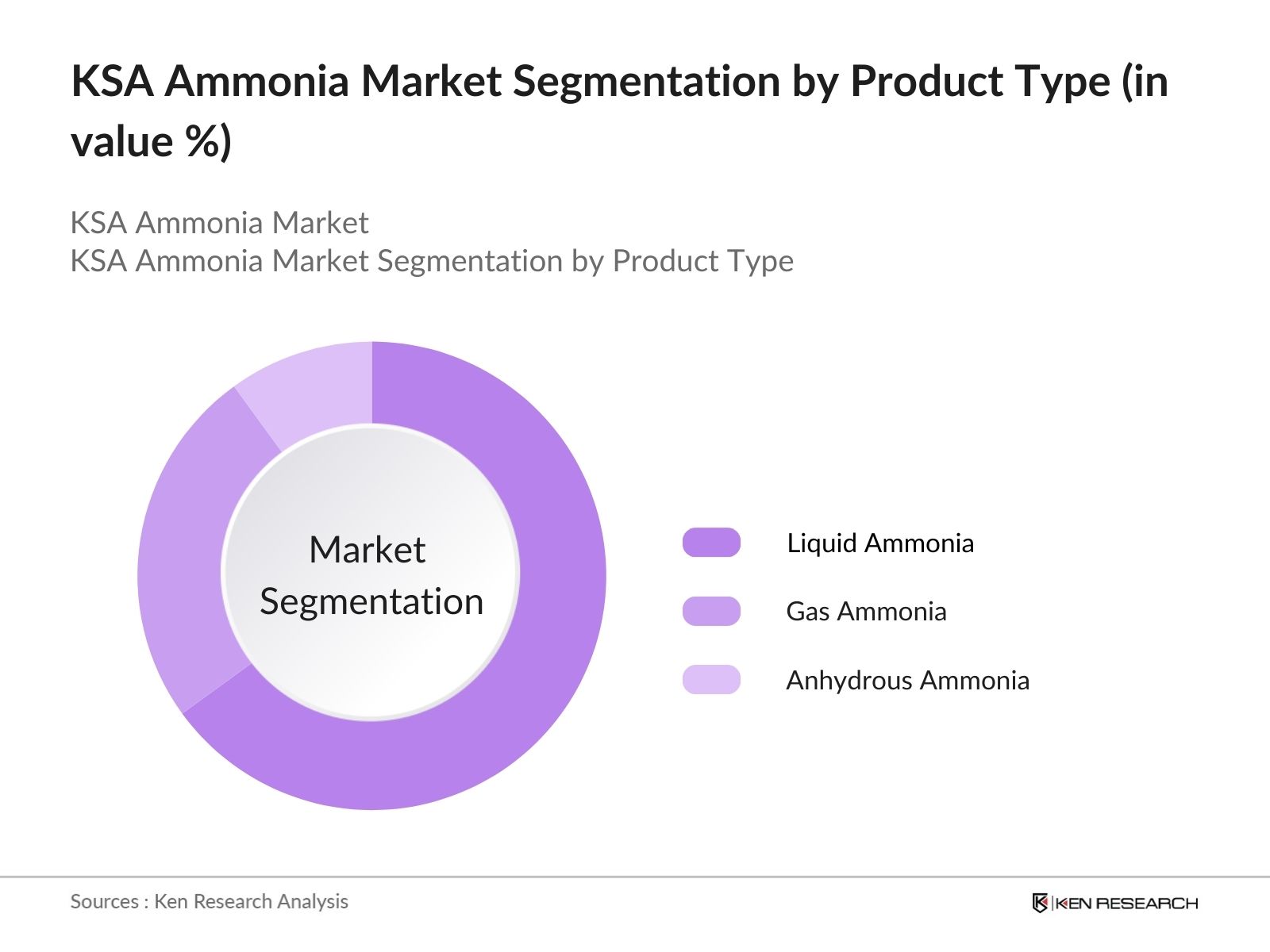

By Product Type: The KSA ammonia market is segmented by product type into liquid ammonia, gas ammonia, and anhydrous ammonia. Liquid ammonia dominates the market share due to its extensive use in the chemical and agricultural sectors. As an essential ingredient for fertilizers, liquid ammonia is favored for its ease of transport and storage, making it more suitable for large-scale applications. The industrial sector also utilizes liquid ammonia in refrigeration systems, contributing to its dominance in the market.

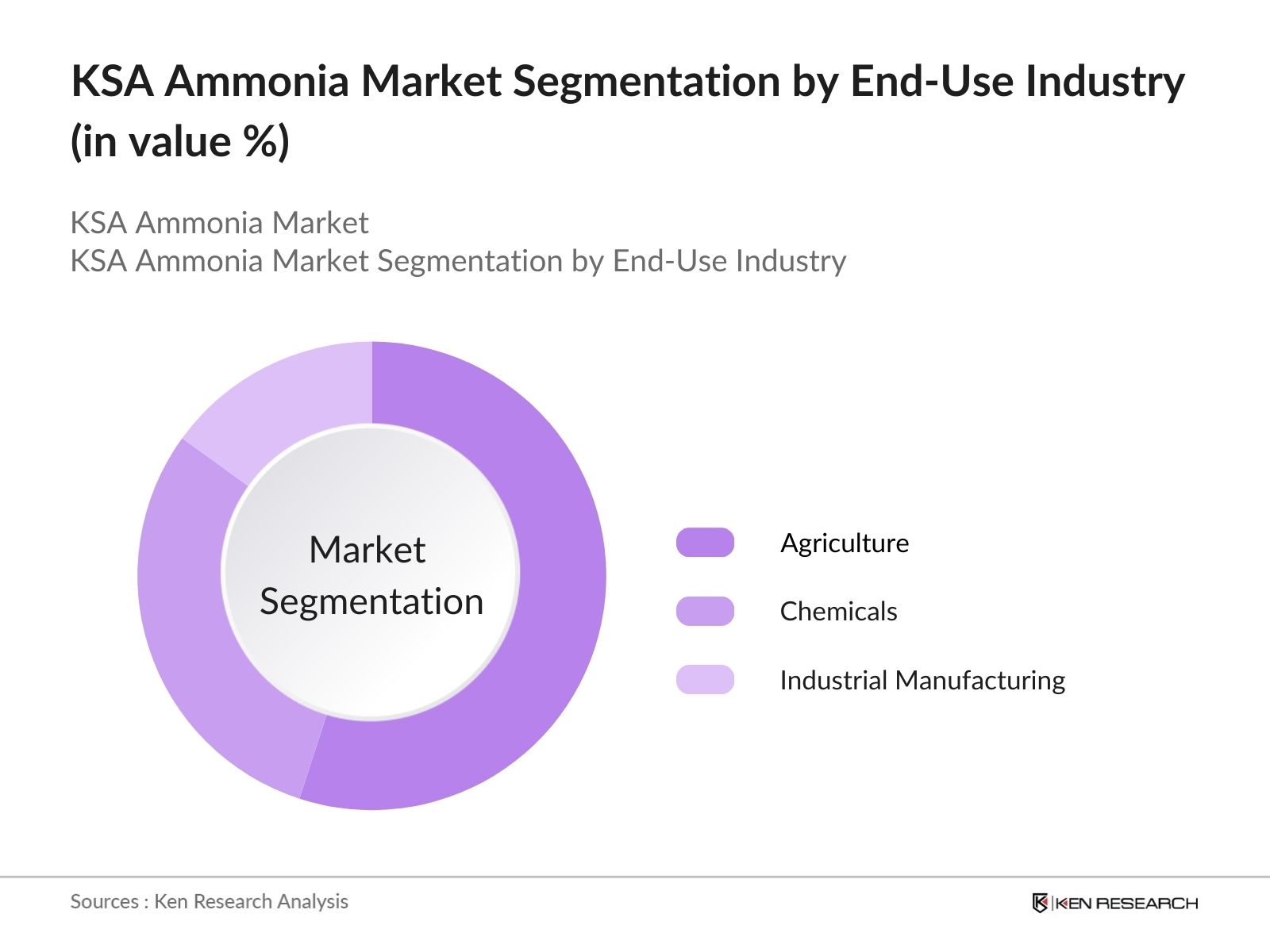

By End-Use Industry: The ammonia market in Saudi Arabia is segmented by end-use industries, including agriculture, chemicals, and industrial manufacturing. Agriculture holds a dominant position within this segmentation, primarily due to the high demand for ammonia in fertilizer production. The increasing global need for food security and Saudi Arabia's focus on enhancing its agricultural productivity have driven this segment's growth. The chemicals sector follows, utilizing ammonia for manufacturing nitric acid and other derivatives essential for various industrial processes.

The KSA ammonia market is dominated by a few key players, including local and regional giants such as SAFCO and Ma'aden. These companies benefit from integrated operations, access to natural gas, and government support, allowing them to maintain competitive production costs. Furthermore, the market is highly consolidated, with companies leveraging joint ventures and partnerships to expand their global footprint. The players listed below are instrumental in shaping the KSA ammonia market landscape.

|

Company Name |

Establishment Year |

Headquarters |

Annual Production Capacity (MT) |

Market Reach |

R&D Expenditure (USD) |

Partnerships |

Export Share |

Employee Strength |

Investment Initiatives |

|

Saudi Arabian Fertilizer Co. (SAFCO) |

1965 |

Jubail |

- |

- |

- |

- |

- |

- |

- |

|

Ma'aden |

1997 |

Riyadh |

- |

- |

- |

- |

- |

- |

- |

|

SABIC |

1976 |

Riyadh |

- |

- |

- |

- |

- |

- |

- |

|

Al-Jubail Fertilizer Company (Al-Bayroni) |

1983 |

Jubail |

- |

- |

- |

- |

- |

- |

- |

|

Gulf Petrochemical Industries Company (GPIC) |

1980 |

Bahrain |

- |

- |

- |

- |

- |

- |

- |

KSA ammonia market is expected to witness moderate growth, driven by continued investment in low-carbon and green ammonia technologies. The government's Vision 2030 strategy, which aims to diversify the economy and reduce dependence on oil, is encouraging investments in sustainable ammonia production methods. Additionally, increasing demand for nitrogen-based fertilizers due to rising agricultural activities and the growing importance of ammonia as a hydrogen carrier for clean energy solutions are likely to fuel market expansion.

|

Product Type |

Liquid Ammonia |

|

End-Use Industry |

Agriculture |

|

Application |

Fertilizer Production |

|

Region |

Riyadh |

|

Distribution Channel |

Direct Sales |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Dynamics Overview (Key Drivers, Challenges, and Opportunities)

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones (Capacity Expansions, Strategic Alliances)

3.1 Growth Drivers

3.1.1 Petrochemical Industry Expansion

3.1.2 Rising Agricultural Demand for Fertilizer Production

3.1.3 Increasing Domestic and Export Demand

3.2 Market Challenges

3.2.1 Fluctuating Natural Gas Prices

3.2.2 Environmental and Regulatory Compliance

3.2.3 Limited Skilled Labor and Technical Expertise

3.3 Opportunities

3.3.1 Strategic Investments in Green Ammonia Production

3.3.2 Export Potential to Emerging Markets

3.3.3 Technological Advancements in Ammonia Storage and Transportation

3.4 Trends

3.4.1 Integration of Carbon Capture and Storage (CCS) Technologies

3.4.2 Shift Towards Low-Carbon Ammonia Production

3.4.3 Partnerships in Hydrogen-Ammonia Projects

3.5 Government Regulations

3.5.1 KSA National Chemical Industry Policies

3.5.2 Environmental and Safety Standards for Ammonia Plants

3.5.3 Export Restrictions and Trade Policies

3.6 SWOT Analysis

3.7 Porters Five Forces Analysis (Ammonia Production, Supply Chain, and Trade)

3.8 Industry Stakeholder Ecosystem (Producers, Suppliers, Distributors, and End-users)

3.9 Competition Ecosystem

4.1 By Product Type (In Value %)

4.1.1 Liquid Ammonia

4.1.2 Gas Ammonia

4.1.3 Anhydrous Ammonia

4.2 By End-Use Industry (In Value %)

4.2.1 Agriculture (Fertilizers)

4.2.2 Chemicals (Nitric Acid, Urea)

4.2.3 Industrial Manufacturing (Textiles, Plastics)

4.3 By Application (In Value %)

4.3.1 Fertilizer Production

4.3.2 Refrigeration Systems

4.3.3 Pollution Control (NOx Reduction)

4.4 By Region (In Value %)

4.4.1 Riyadh

4.4.2 Eastern Province

4.4.3 Jeddah

4.4.4 Mecca

4.5 By Distribution Channel (In Value %)

4.5.1 Direct Sales

4.5.2 Third-Party Distributors

4.5.3 Export Channels

5.1 Detailed Profiles of Major Companies

5.1.1 Saudi Arabian Fertilizer Company (SAFCO)

5.1.2 Ma'aden (Saudi Arabian Mining Company)

5.1.3 SABIC (Saudi Basic Industries Corporation)

5.1.4 Al-Jubail Fertilizer Company (Al-Bayroni)

5.1.5 Qatar Fertiliser Company (QAFCO)

5.1.6 Petrochemical Conversion Company (PCC)

5.1.7 Gulf Petrochemical Industries Company (GPIC)

5.1.8 National Fertilizer Company (Mada)

5.1.9 Emirates Chemical Company (ECC)

5.1.10 Naser Al Hajri Corporation

5.1.11 Global Chemical Company

5.1.12 Arabian Fertilizer Company

5.1.13 Agrium Middle East Fertilizer Company

5.1.14 SABIC Agribusiness

5.1.15 Qatar Chemical and Petrochemical Marketing and Distribution Company (Muntajat)

5.2 Cross Comparison Parameters (Revenue, Production Capacity, Export Volume, Geographical Presence, Market Share, Investment Initiatives, R&D Spend, Key Partnerships)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants and Incentives

5.9 Private Equity Investments

6.1 Environmental Regulations (Emissions, Waste Management, Safety Standards)

6.2 Compliance Requirements (ISO Standards, Certification Processes)

6.3 Tax Policies and Import Duties

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Product Type (In Value %)

8.2 By End-Use Industry (In Value %)

8.3 By Application (In Value %)

8.4 By Region (In Value %)

8.5 By Distribution Channel (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Marketing Strategies

9.3 White Space Opportunity Analysis

9.4 Future Investment Recommendations

The first step in the research process involved creating a comprehensive map of stakeholders within the KSA ammonia market. Extensive desk research and database analysis were used to define critical variables, such as production capacities, distribution channels, and end-user demand patterns.

In this step, historical data on production, distribution, and consumption trends were gathered and analyzed. This included examining the impact of market dynamics on ammonia prices, supply chains, and export activities. Insights into market segmentation by region, product type, and end-use were derived from this analysis.

Industry experts were consulted to validate the initial market data through interviews and surveys. These interactions helped confirm production estimates, regional demand variations, and emerging trends in green ammonia production.

The final stage involved synthesizing the validated data into a comprehensive market analysis report. The report includes insights into market trends, growth drivers, challenges, and opportunities, ensuring accuracy through cross-verification with secondary and primary research sources.

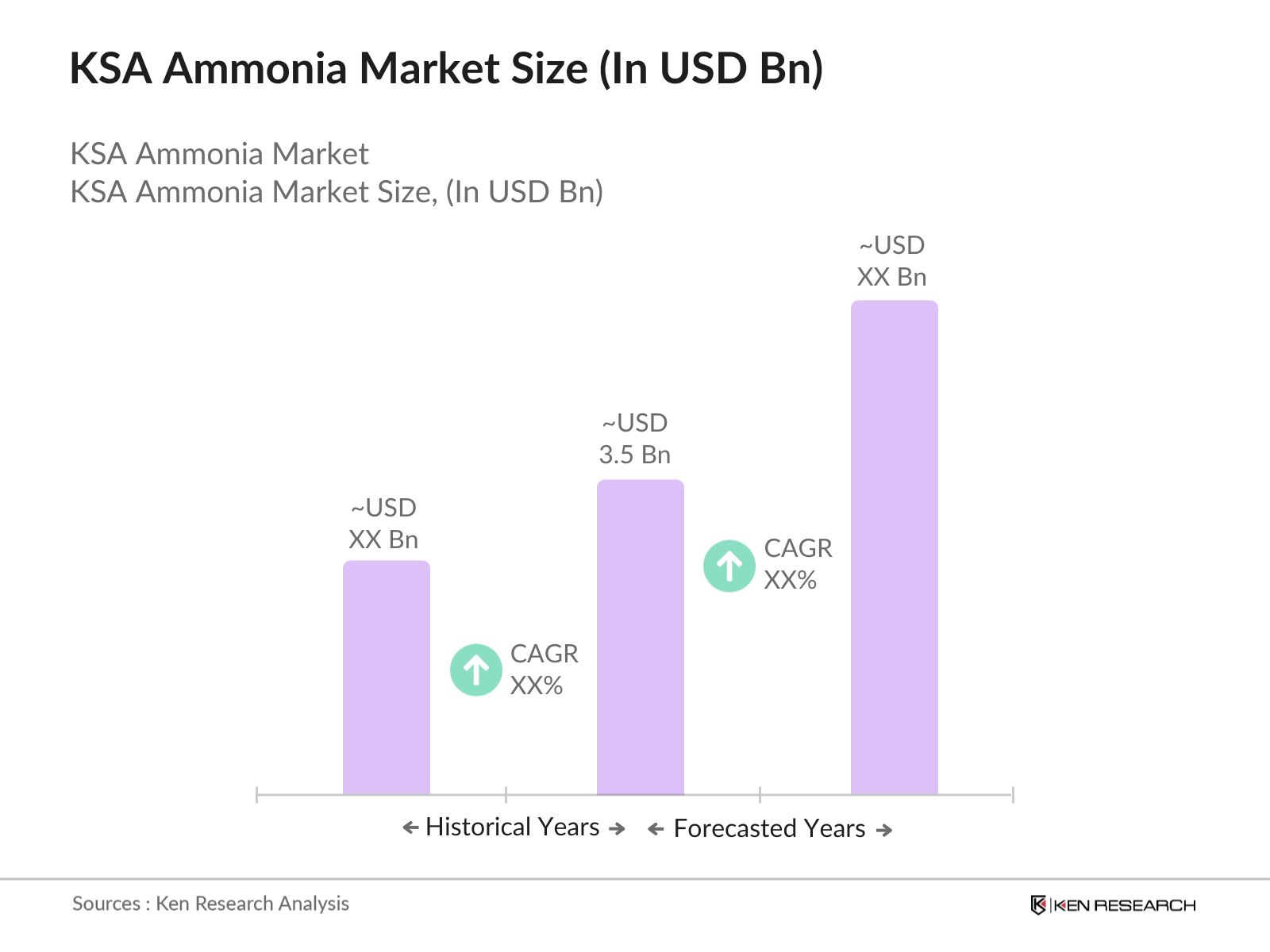

The KSA ammonia market, valued at USD 3.5 billion, driven by robust growth in the petrochemical sector and increased demand for nitrogen-based fertilizers.

Challenges of KSA Ammonia Market include fluctuating natural gas prices, environmental regulations, and a shortage of skilled labor, which complicates the expansion of production capacities and the adoption of green ammonia technologies.

Key players of KSA Ammonia Market include SAFCO, Ma'aden, SABIC, Al-Jubail Fertilizer Company, and Gulf Petrochemical Industries Company, which dominate due to their access to raw materials, government support, and strategic partnerships.

Growth drivers of KSA Ammonia Market include rising agricultural demand, expanding petrochemical production, and the increasing use of ammonia as a hydrogen carrier for clean energy solutions. Government support through Vision 2030 also plays a pivotal role in boosting investments.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.