KSA Apparel Market Outlook to 2030

Region:Middle East

Author(s):Yogita Sahu

Product Code:KROD6255

November 2024

95

About the Report

KSA Apparel Market Overview

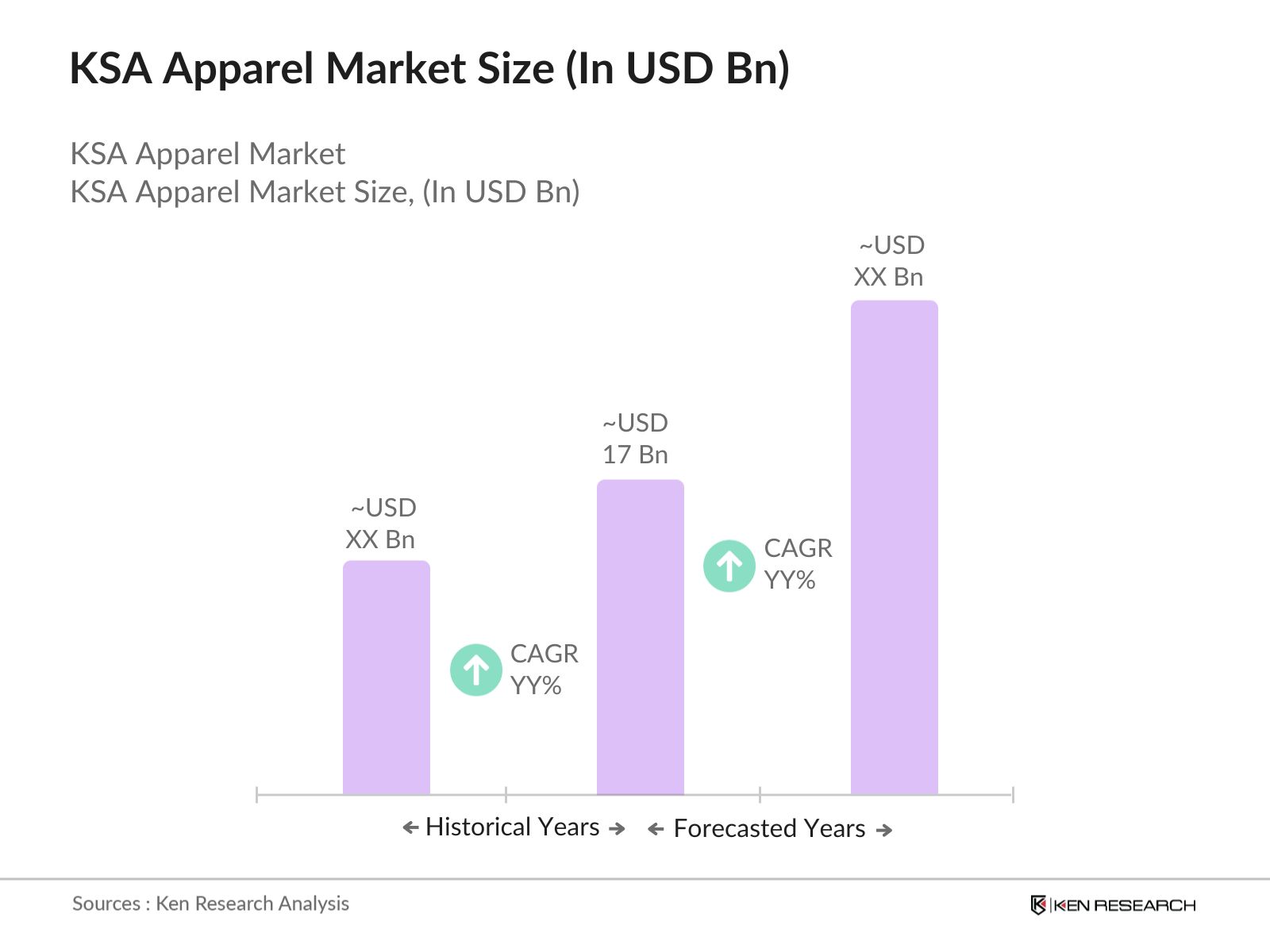

- The KSA Apparel market, valued at USD 17 billion, is driven primarily by increasing disposable incomes, evolving consumer preferences, and a rapidly expanding retail sector. The demand for apparel, particularly in the premium and mid-range segments, is bolstered by the Kingdoms young and fashion-conscious population. This growth is supported by the government's economic diversification efforts under Vision 2030, which emphasizes the retail sector as a key area for economic expansion.

- Dominant cities in the market include Riyadh, Jeddah, and Dammam. These cities dominate the market due to their large population densities, higher disposable incomes, and a growing expatriate population. Riyadh, as the capital, is the hub for major retail activities, while Jeddah, being a commercial center and gateway to the holy cities of Makkah and Madinah, attracts consumer spending.

- To reduce dependence on imports, the government has incentivized local apparel production under the "Made in Saudi" program. By 2024, around SAR 8 billion has been invested in textile manufacturing plants within industrial cities such as Jeddah and Riyadh. These efforts are aimed at promoting domestic production of fashion and apparel, creating job opportunities while ensuring a more resilient supply chain for the industry.

KSA Apparel Market Segmentation

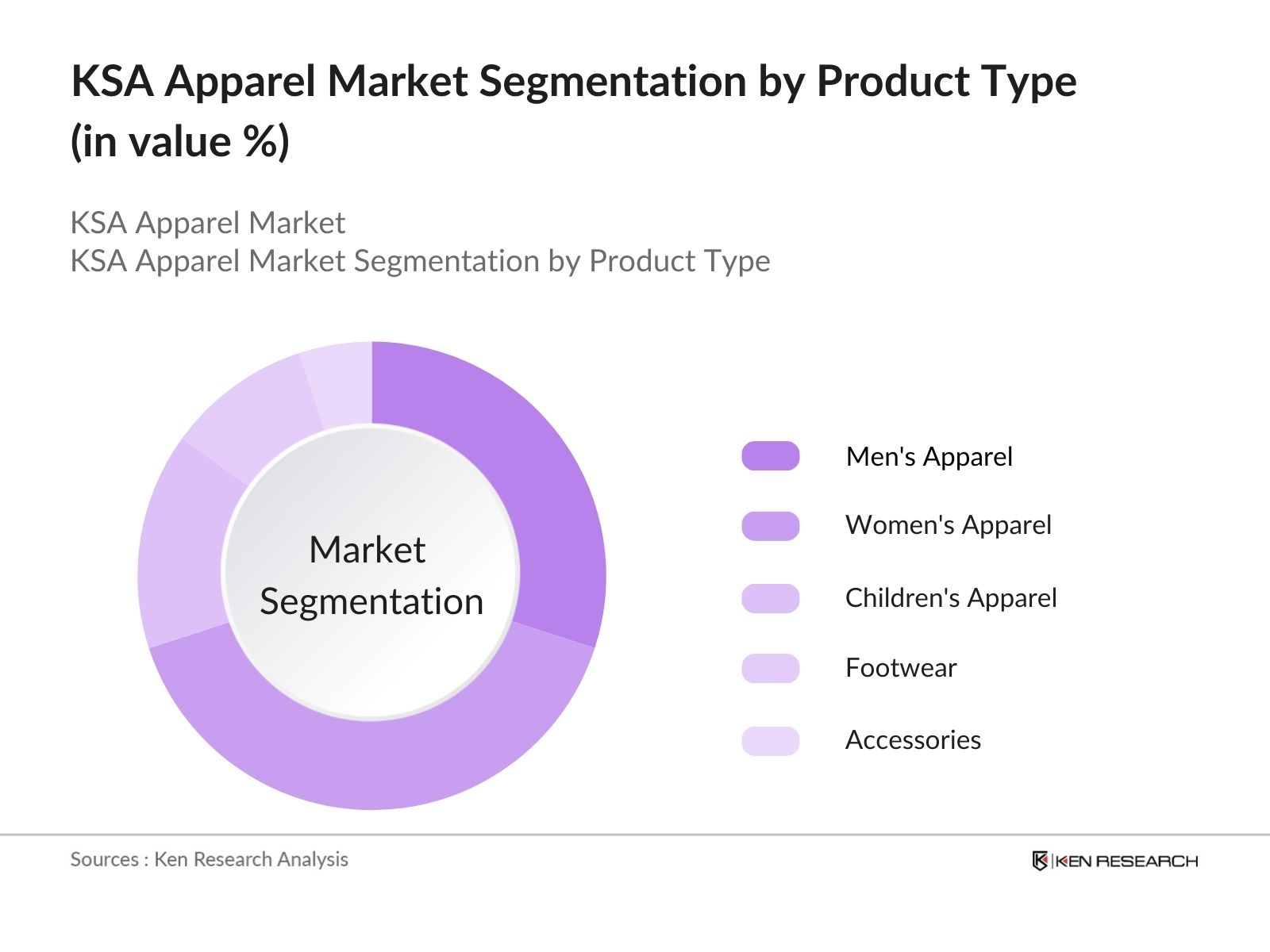

By Product Type: The market is segmented by product type into men's apparel, women's apparel, children's apparel, footwear, and accessories. Women's apparel has had a dominant market share under the segmentation of product type due to shifting cultural norms that allow for more diverse and modern clothing options. Women in the Kingdom are increasingly embracing global fashion trends, which has led to a rise in demand for both modest fashion, such as abayas, and Western-style apparel.

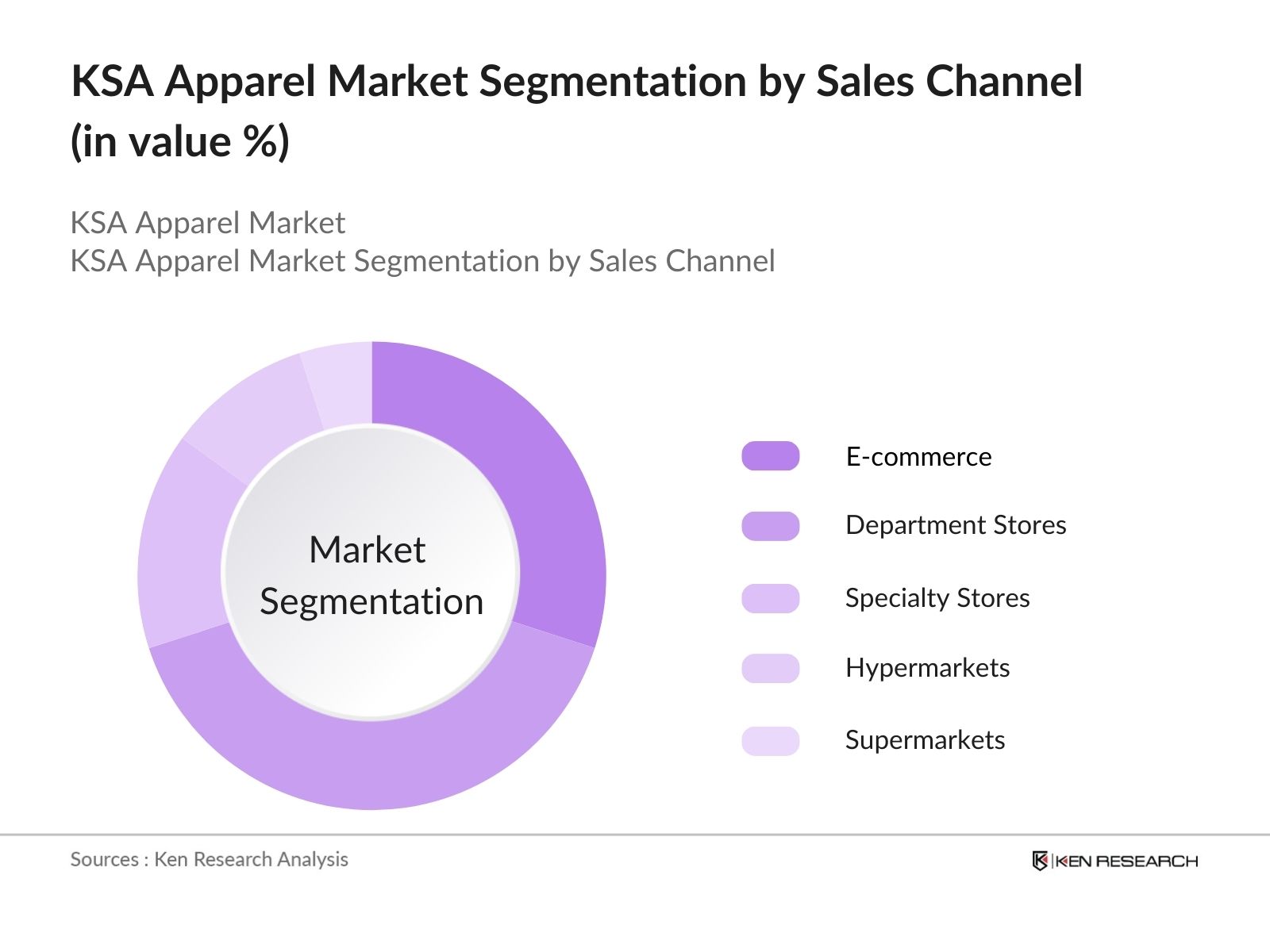

By Sales Channel: The market is segmented by sales channel into e-commerce, department stores, specialty stores, and hypermarkets/supermarkets. E-commerce is rapidly emerging as the dominant sales channel due to its convenience, extensive product range, and competitive pricing. The penetration of internet and smartphone usage across the Kingdom has made online shopping more accessible, especially for younger consumers.

KSA Apparel Market Competitive Landscape

The market is dominated by both local retailers and international brands. The market's competitive landscape showcases an increasing trend of mergers and acquisitions, partnerships with influencers, and the entry of global fast fashion brands.

|

Company Name |

Establishment Year |

Headquarters |

No. of Employees |

Inception Year |

Annual Revenue (USD) |

Market Presence |

Product Range |

Local Partnerships |

Key Innovations |

|

Alhokair Fashion Retail |

1990 |

Riyadh, KSA |

|||||||

|

Fawaz Abdulaziz Alhokair Co |

1991 |

Riyadh, KSA |

|||||||

|

Landmark Group |

1973 |

Dubai, UAE |

|||||||

|

Zara (Inditex) |

1975 |

Spain |

|||||||

|

Nike, Inc. |

1964 |

USA |

KSA Apparel Market Analysis

Market Growth Drivers

- Government Support for Retail and E-commerce Expansion: In line with the Vision 2030 plan, the Saudi government is actively supporting the growth of the retail and e-commerce sectors, particularly in the apparel market. The launch of platforms such as SADAD and the E-Commerce Council, along with financial reforms to promote digital transactions, has increased the accessibility of fashion products.

- Increased Expat Population Contributing to Apparel Sales: Saudi Arabia has seen an inflow of expatriates due to its diversifying economy, which includes the growth of the entertainment and tourism sectors. According to the Ministry of Human Resources and Social Development, the expat population reached over 10.5 million in 2024. This demographic expansion has brought different cultural influences and diverse apparel preferences, fueling demand for both traditional and western-style clothing across the market.

- Rise of Tourism as a Key Economic Driver: With Saudi Arabia's increasing focus on developing the tourism sector under the Vision 2030 plan, the market for apparel has seen a boost. The government reported that 10 million international tourists visited Saudi Arabia in 2024, driven by mega-events like Riyadh Season and the opening of cultural and entertainment hubs. This rise in tourism is boosting demand for fashion apparel, as visitors purchase clothing during their travels, benefiting retail sales across the country.

Market Challenges

- Increase in Local Apparel Manufacturing: By 2029, Saudi Arabia will see significant growth in local apparel manufacturing, supported by continued investments in domestic textile plants. The Vision 2030 plan estimates that local production will rise by an additional 50,000 units annually, reducing the country's reliance on imported garments and boosting export potential, particularly to neighboring GCC countries. This will create a more self-sufficient and competitive apparel industry.

- Shift Towards Sustainable and Ethical Fashion: Sustainability will be a key trend in the Saudi apparel market over the next five years, with both consumers and retailers becoming more eco-conscious. The Green Saudi Initiative will support the rise of sustainable fashion brands and products, with the government projecting that at least 20% of apparel sold by 2029 will come from eco-friendly sources. Retailers will also focus on transparency in their supply chains, providing consumers with more ethically sourced options.

KSA Apparel Market Future Outlook

Over the next five years, the KSA apparel industry is expected to continue its growth trajectory, driven by favorable government policies, technological advancements in retail, and increasing consumer demand for diverse fashion options. The Kingdom's Vision 2030 plan, which seeks to diversify the economy away from oil dependence, includes the expansion of the retail and fashion sectors as a key component of economic transformation.

Future Market Opportunities

- Increase in Local Apparel Manufacturing: By 2029, Saudi Arabia will see growth in local apparel manufacturing, supported by continued investments in domestic textile plants. The Vision 2030 plan estimates that local production will rise by an additional 50,000 units annually, reducing the country's reliance on imported garments and boosting export potential, particularly to neighboring GCC countries.

- Shift Towards Sustainable and Ethical Fashion: Sustainability will be a key trend in the Saudi apparel market over the next five years, with both consumers and retailers becoming more eco-conscious. The Green Saudi Initiative will support the rise of sustainable fashion brands and products, with the government projecting that at least 20% of apparel sold by 2029 will come from eco-friendly sources. Retailers will also focus on transparency in their supply chains, providing consumers with more ethically sourced options.

Scope of the Report

|

Product Type |

Men's Apparel Women's Apparel Children's Apparel Footwear Accessories |

|

Sales Channel |

E-commerce Department Stores Specialty Stores Hypermarkets/Supermarkets |

|

End-Use |

Casual Wear Formal Wear Sportswear, Workwear |

|

Material Type |

Cotton Synthetic Fabrics Wool Blended Fabrics |

|

Region |

North East West South |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Banks and Financial Institution

Textile and fabric manufacturers

Fashion designers and apparel manufacturers

Government and regulatory bodies (Ministry of Commerce, Saudi Standards, Metrology and Quality Organization)

Investors and venture capitalist firms

Private Equity Firms

Logistics and distribution companies

Companies

Players Mentioned in the Report:

Alhokair Fashion Retail

Fawaz Abdulaziz Alhokair Co.

Landmark Group

Nike, Inc.

Adidas AG

H&M Hennes & Mauritz AB

Zara (Inditex)

Lululemon Athletica Inc.

Puma SE

Levi Strauss & Co.

Max Fashion

Bershka

The Body Shop

Mango

Aldo

Table of Contents

1. KSA Apparel Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. KSA Apparel Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. KSA Apparel Market Analysis

3.1. Growth Drivers

3.1.1. Growing Population (Population growth rate, urban-rural ratio)

3.1.2. Increased Disposable Income (GDP per capita)

3.1.3. Changing Consumer Preferences (Consumer spending on fashion, shift towards casual wear)

3.1.4. Rise in E-commerce Penetration (E-commerce penetration, internet usage)

3.2. Market Challenges

3.2.1. Supply Chain Disruptions (Import dependency, logistics challenges)

3.2.2. Intense Competition (Market fragmentation, pricing pressures)

3.2.3. Fluctuating Raw Material Costs (Textile prices, cotton prices)

3.3. Opportunities

3.3.1. Growth in Women's Apparel (Shift towards modern fashion, cultural changes)

3.3.2. Rising Demand for Modest Fashion (Growing preference for abayas and hijabs)

3.3.3. Increasing Popularity of Sustainable Apparel (Demand for eco-friendly textiles, slow fashion trends)

3.4. Trends

3.4.1. Digital Transformation in Retail (AI-powered fashion, virtual fitting rooms)

3.4.2. Rise of Athleisure (Casual and activewear convergence)

3.4.3. Brand Collaborations with Influencers (Social media marketing, influencer partnerships)

3.5. Government Regulation

3.5.1. Vision 2030 Impact on Retail (National retail strategy)

3.5.2. Trade Tariffs and Import Regulations (Import duties, textile tariffs)

3.5.3. Sustainable Apparel Policies (Environmental regulations)

3.5.4. National Workforce Policies (Saudization initiatives)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.8.1. Bargaining Power of Suppliers

3.8.2. Bargaining Power of Buyers

3.8.3. Threat of New Entrants

3.8.4. Threat of Substitutes

3.8.5. Competitive Rivalry

3.9. Competition Ecosystem

4. KSA Apparel Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Men's Apparel

4.1.2. Women's Apparel

4.1.3. Children's Apparel

4.1.4. Footwear

4.1.5. Accessories

4.2. By Sales Channel (In Value %)

4.2.1. E-commerce

4.2.2. Department Stores

4.2.3. Specialty Stores

4.2.4. Hypermarkets/Supermarkets

4.3. By End-Use (In Value %)

4.3.1. Casual Wear

4.3.2. Formal Wear

4.3.3. Sportswear

4.3.4. Workwear

4.4. By Material Type (In Value %)

4.4.1. Cotton

4.4.2. Synthetic Fabrics

4.4.3. Wool

4.4.4. Blended Fabrics

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. West

4.5.4. South

5. KSA Apparel Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Alhokair Fashion Retail

5.1.2. Fawaz Abdulaziz Alhokair Co.

5.1.3. Landmark Group

5.1.4. Nike, Inc.

5.1.5. Adidas AG

5.1.6. H&M Hennes & Mauritz AB

5.1.7. Zara (Inditex)

5.1.8. Lululemon Athletica Inc.

5.1.9. Puma SE

5.1.10. Levi Strauss & Co.

5.1.11. Max Fashion

5.1.12. Bershka

5.1.13. The Body Shop

5.1.14. Mango

5.1.15. Aldo

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Market Penetration, Brand Recall, Product Portfolio, Local Partnerships)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government Grants

5.8 Private Equity Investments

6. KSA Apparel Market Regulatory Framework

6.1 Apparel Safety Standards

6.2 Compliance Requirements (Labelling, Certification)

6.3 Trade Policy and Import Tariffs

6.4 Workforce Regulations (Saudization Laws)

7. KSA Apparel Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. KSA Apparel Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Sales Channel (In Value %)

8.3. By End-Use (In Value %)

8.4. By Material Type (In Value %)

8.5. By Region (In Value %)

9. KSA Apparel Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Consumer Demographic Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase of the research involved the identification of key variables influencing the KSA apparel market. These variables were identified through secondary research and include consumer preferences, fashion trends, and the impact of government policies. Data was gathered from credible industry reports, government publications, and interviews with market experts.

Step 2: Market Analysis and Construction

Historical data for the KSA apparel market was analyzed to determine market size, growth trends, and consumer behavior. The construction of the market model involved analyzing key segments such as product type, sales channels, and consumer demographics.

Step 3: Hypothesis Validation and Expert Consultation

To validate the research hypotheses, consultations with industry experts were conducted through phone and email interviews. These consultations helped to refine market estimates and provided insights into future market dynamics, competitive strategies, and key growth drivers.

Step 4: Research Synthesis and Final Output

In the final phase, data was synthesized to present a comprehensive market report. The bottom-up approach was employed to ensure that all market estimates are backed by detailed industry inputs. Final outputs include key market forecasts, trends, and a strategic analysis of the competitive landscape.

Frequently Asked Questions

How big is the KSA Apparel Market?

The KSA apparel market is valued at USD 17 billion, driven by increasing disposable incomes, evolving consumer preferences, and growth in the retail sector.

What are the challenges in the KSA Apparel Market?

Challenges in the KSA apparel market include supply chain disruptions, intense competition among local and international players, and fluctuating raw material costs, particularly for textiles.

Who are the major players in the KSA Apparel Market?

Major players in the KSA apparel market include Alhokair Fashion Retail, Fawaz Abdulaziz Alhokair Co., Nike, Adidas, and Zara, which dominate due to their strong market presence and brand loyalty.

What are the growth drivers of the KSA Apparel Market?

The KSA apparel market is driven by factors such as rising disposable incomes, increased e-commerce penetration, and a young, fashion-conscious population, especially in urban areas like Riyadh and Jeddah.

How is e-commerce impacting the KSA Apparel Market?

E-commerce has rapidly emerged as a dominant sales channel in the KSA apparel market, supported by increasing internet penetration, smartphone usage, and the convenience of online shopping.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.