KSA Aquaculture Feed Market Outlook to 2029

Region:Middle East

Author(s):Shashank, Rhythm

Product Code:KR1498

April 2025

80-100

About the Report

KSA Aquaculture Feed Market Overview

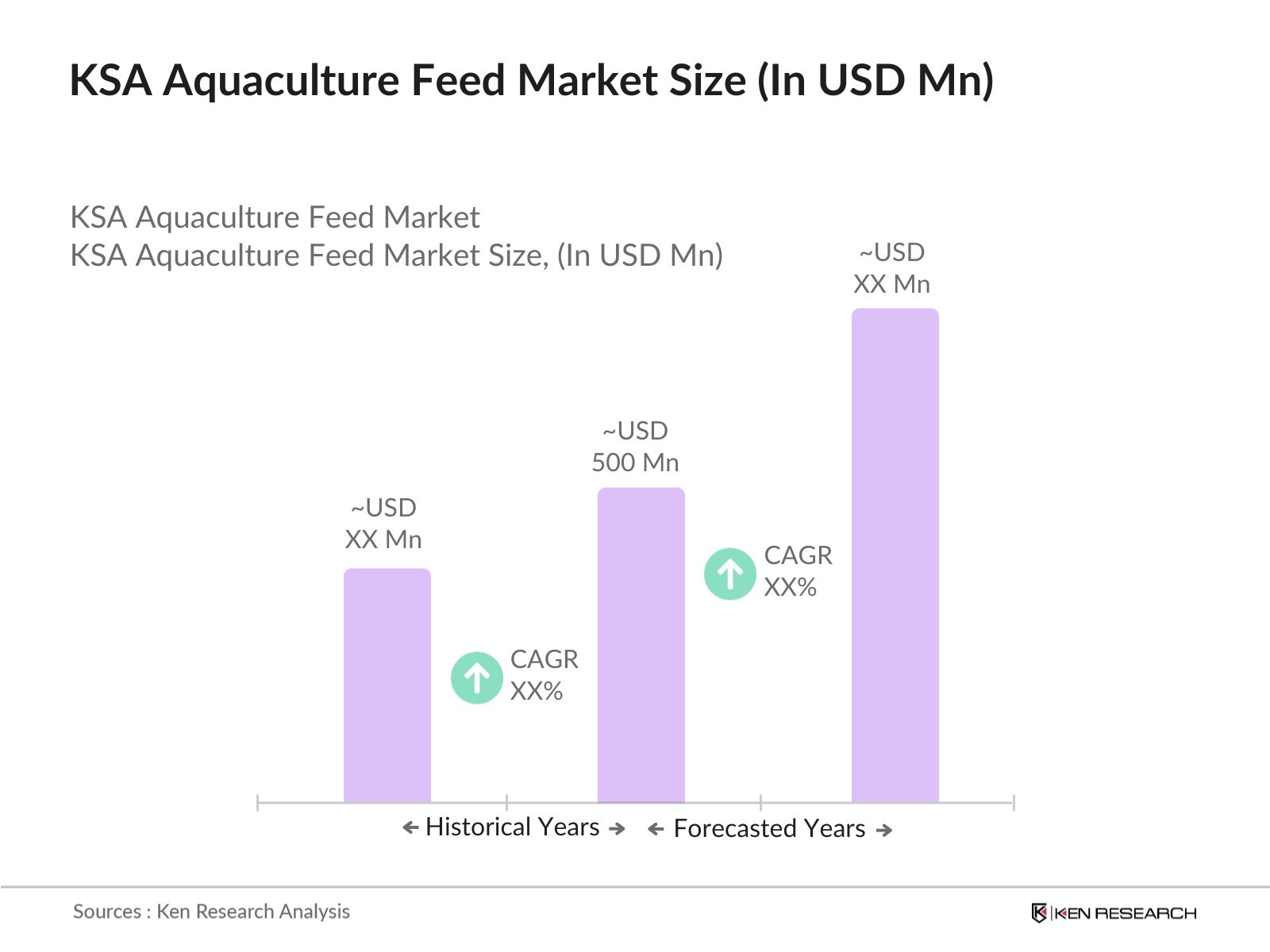

- The KSA aquaculture feed market is valued at USD 500 million, based on a five-year historical analysis. The rapid expansion of the seafood sector, particularly in high-value species such as Red Sea White Leg shrimp and European sea bream, has driven feed demand. The market is further strengthened by rising prices of nutrient-rich and premium feed formulations, which support species-specific health and growth. This shift toward high-quality aquafeed aligns with national efforts to improve seafood self-sufficiency and reduce reliance on imports.

- Geographical dominance within Saudi Arabia's aquaculture feed market is anchored by major aquaculture zones in coastal provinces, particularly along the Red Sea. Cities such as Jazan, Umluj, and Al Lith are witnessing growing aquaculture activity due to favorable marine ecosystems and direct government backing. These regions benefit from proximity to production zones, export terminals, and seafood processing hubs, making them focal points for feed distribution. Their strategic location and alignment with Vision 2030's aquaculture goals contribute to their lead in shaping feed consumption patterns.

- Saudi Arabia's aquaculture feed market is guided by Vision 2030 programs like NTP and ADP, aiming for seafood self-sufficiency. The SAMAQ certification ensures quality compliance, while MEWAs Agricultural Development Fund supports up to 75% of capital costs for feed projects. The Agricultural Subsidy Program has allocated over SAR 50 million so far, promoting local feed manufacturing, food security, and reduced import reliance.

KSA Aquaculture Feed Market Segmentation

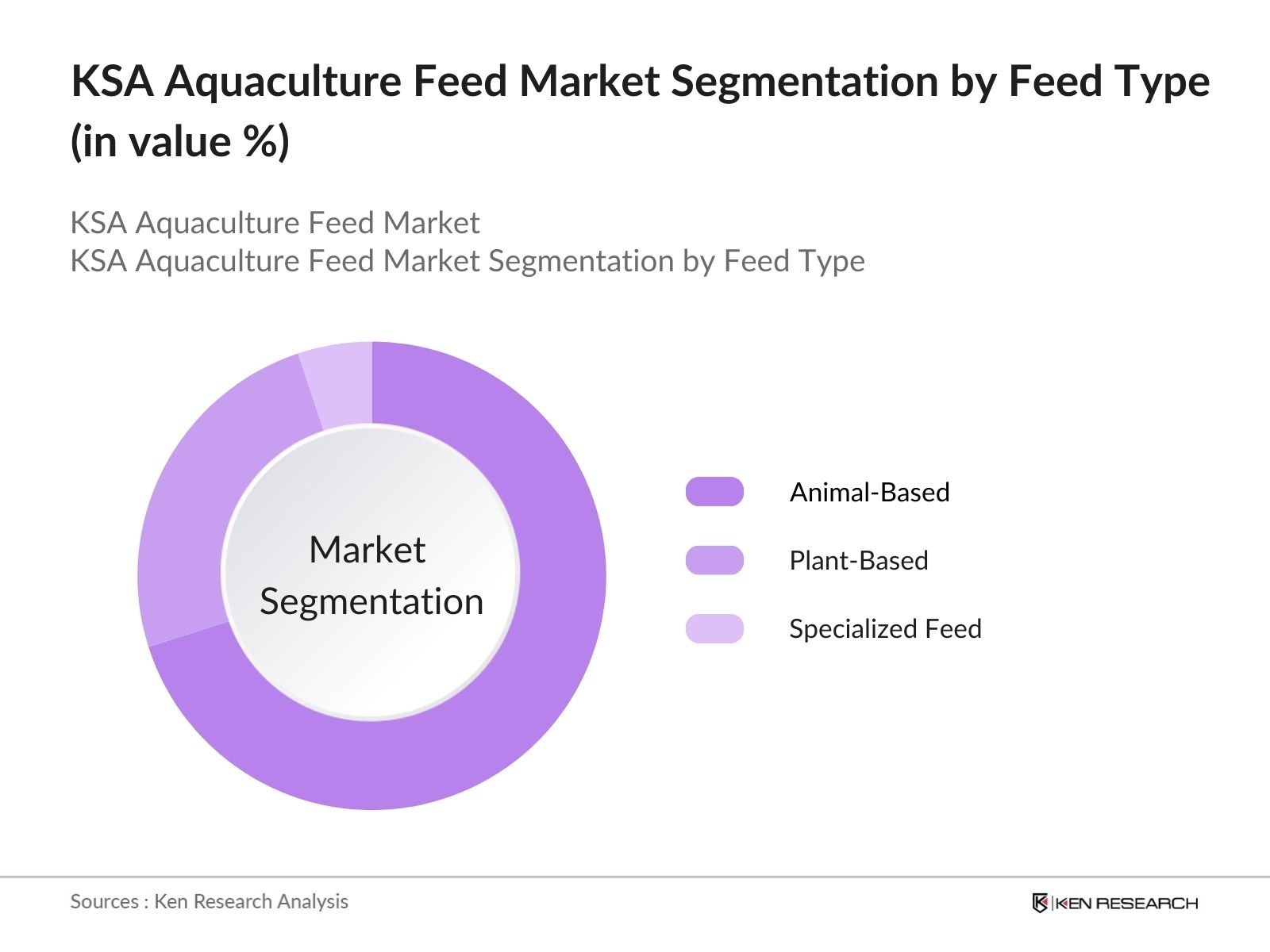

By Feed Type: The KSA Aquaculture Feed market is segmented by feed type into Animal-Based, Plant-Based, and Specialized Feeds. Animal-based feed holds a dominant share due to its superior protein absorption and lower feed conversion ratio, making it ideal for high-value species like sea bass and shrimp. Plant-based feed is preferred in semi-intensive farms as a cost-effective protein source, while Specialized Feed supports nutritional needs in stress-prone or disease-sensitive aquaculture environments.

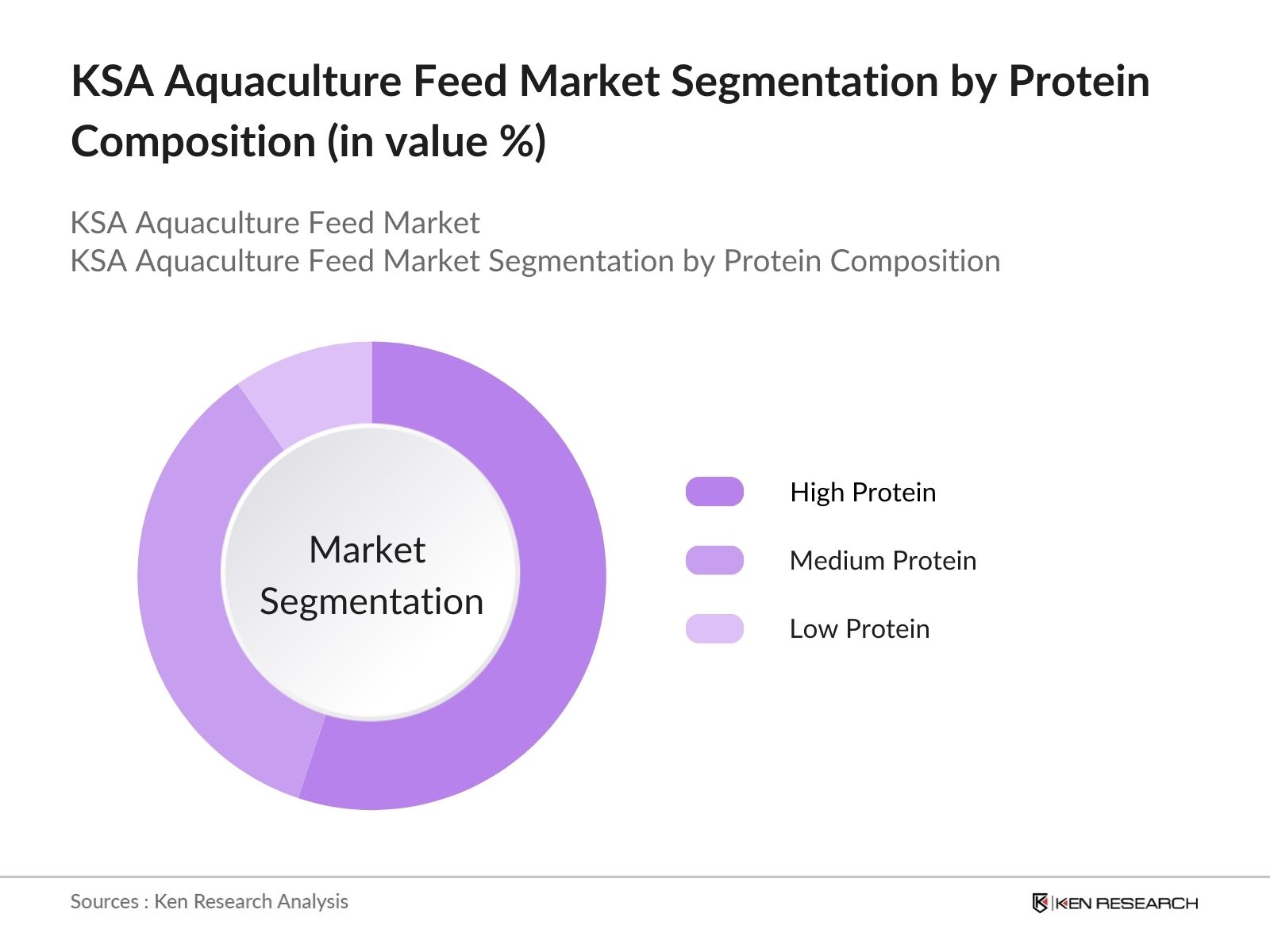

By Protein Composition: The KSA Aquaculture Feed market is segmented by protein content into high, medium, and low protein feeds. High protein feed dominates the segment, primarily due to its critical role in intensive aquaculture systems and its effectiveness in supporting the growth of high-value fish species. These feeds are widely used across commercial farms to enhance feed conversion efficiency and ensure optimal weight gain, especially during peak production cycles targeting export-grade yields.

KSA Aquaculture Feed Market Competitive Landscape

The KSA Aquaculture Feed market is dominated by integrated domestic producers leveraging vertically integrated supply chains and robust feed mill infrastructure. Leading companies such as NAQUA and ARASCO cater to large-scale demand through customized formulations and streamlined distribution. International players like Skretting, Adisseo, Bernaqua, and Alltech Coppens address the premium segment with specialized imports. Emerging innovators such as Calysta are introducing alternative proteins, while firms like Cargill are expanding capacity via local alliances, strengthening the market's profitability and diversity.

KSA Aquaculture Feed Market Analysis

Growth Drivers

- Rising Aquaculture Production Targets: Saudi Arabia aims to boost aquaculture output from 190,000 tons to 530,000 tons by 2030, directly impacting feed consumption. Government-backed subsidies, streamlined regulations, and large-scale investment incentives are attracting new entrants and empowering existing players to scale operations, thereby amplifying feed demand across both inland and coastal aquaculture farms.

- Shifting Toward High-Efficiency Feeds: Farmers increasingly adopt feeds with superior Feed Conversion Ratios (FCRs), especially for shrimp and seabass. Specialized and high-protein feeds, despite their higher costs, improve growth rates, reduce disease incidence, and shorten culture cycles. This performance advantage drives long-term preference among commercial-scale farmers, boosting volumes of functional feed consumption.

- Expansion of Digital and Automated Farming: Smart aquaculture tools such as auto-feeders, IoT-based sensors, and predictive software are enhancing feed efficiency. By reducing overfeeding and monitoring real-time growth metrics, these technologies help farmers optimize feed usage and reduce costs. Their rising adoption supports greater accuracy in feed formulation and drives demand for precision-targeted feed solutions.

Market Challenges

- Dependence on Imported Raw Materials: A significant portion of key feed inputs, such as fishmeal, soybean meal, and micronutrients, are imported, leaving domestic manufacturers exposed to global commodity price shocks. Currency fluctuations, supply disruptions, and international trade policy changes can lead to volatile feed prices, affecting cost predictability and margins across the value chain.

- Environmental Regulations and Water Salinity Issues: Strict environmental standards mandate controlled discharge and nutrient leaching limits, pushing producers to innovate in low-pollution feeds. Meanwhile, variable salinity levels in brackish farms require adaptive formulations to ensure palatability and digestion. This adds R&D pressure and raises production costs for smaller or less tech-enabled feed producers in KSA.

KSA Aquaculture Feed Market Future Outlook

Over the next five years, the KSA Aquaculture Feed Market is expected to witness accelerated growth. Key enablers include increased domestic feed production, strategic government incentives for feed mill expansion, and the adoption of smart aquaculture practices. Rising export opportunities to GCC and African nations are also anticipated to boost regional demand, reinforcing KSA's position as a central hub for aquafeed manufacturing and innovation.

Market Opportunities

- Export-Driven Demand for Premium Feed: Saudi Arabia's focus on boosting seafood exports is increasing the demand for high-quality, nutrient-rich aquafeed. With export species like European sea bream and barramundi gaining traction, feed formulations with enhanced protein content and growth promoters are in demand. The country exported over 60,000 tons of aquaculture products in 2023, which is expected to grow further, creating space for value-added feed solutions aligned with international standards.

- Vision 2030-Linked Infrastructure Expansion: The government's Vision 2030 targets 100% seafood self-sufficiency through domestic production. Infrastructure expansion, including hatcheries and feed mills, is underway with financial support from MEWA and NFDP. This national push opens opportunities for feed companies to scale operations, develop localized formulations, and partner with farm clusters. The establishment of over 10 new aquafeed formulations under ADP by KAUST also signals a shift towards specialized, performance-driven feed R&D.

Scope of the Report

|

By Species |

Shrimps |

|

By Feed Type |

Animal-based |

|

By Protein Composition |

High (>35%) |

|

By End Use |

Human consumption |

|

By Feed Form |

Pelleted |

|

By Channel |

Direct |

Products

Key Target Audience

- Large-scale Marine and Inland Aquaculture Farm Owners

- Specialized Shrimp and Tilapia Hatchery Operators

- Regional Feed Importers, Distributors, and Cold Chain Wholesalers

- Ministry of Environment, Water and Agriculture (MEWA) – Aquaculture Division

- Vertically Integrated Seafood Processing & Exporting Companies

- Aquatic Feed Formulation Scientists and Marine Nutrition Experts

- ESG-Focused Aquaculture Investment Funds and Green Capital Firms

- Technology Providers for Precision Aquafeed and Feeding Automation

Companies

Players Mentioned in the Report

NAQUA

ARASCO

Skretting

Adisseo

Bernaqua

Table of Contents

1. Market Taxonomy

2. Executive Summary

2.1 Market Overview of KSA Aquaculture Feed Market

2.2 Ecosystem of Players in the Market

3. KSA Aquaculture Market Overview

3.1 KSA Seafood Demand and Domestic Production Scenario

3.2 Demand Stability Evaluation of the KSA Aquaculture Sector

3.3 Value Chain Analysis of the Aqua Feed Market

3.4 Vision 2030 Impact on Aquaculture Feed Market

3.5 Existing Government Incentives, Policies & Subsidies in the Market

4. KSA Aquaculture Feed Market Sizing

4.1 Historical, Current Market Sizing and Future Projections (Volume), 2019–2030F

4.2 Market Sizing Calculations – By Value, 2024

4.3 Historical, Current Market Sizing and Future Projections (Value), 2019–2030F

4.4 CAGR Component Split for the Market

5. KSA Aquaculture Feed Market Segmentations

5.1 Market Segmentation by Species, 2024 & 2030F

5.2 Total Seafood Consumption and Aquaculture Production by Major Species, 2024

5.3 Market Segmentation by Protein Composition, 2024 & 2030F

5.4 Market Segmentation by Feed Type, 2024 & 2030F

5.5 Market Segmentation by Feed Form, 2024 & 2030F

5.6 Market Segmentation by End User, 2024 & 2030F

5.7 Market Segmentation by Distribution, 2024 & 2030F

6. Competition Scenario

6.1 Competition Overview

6.2 Cross Comparison of Major Players in the KSA Aquaculture Feed Market

7. Consumer Behavior Analysis

7.1 Consumer Profile

7.2 Feed Preference

7.3 Needs and Pain Points

7.4 Procurement Analysis

8. Analyst Recommendations

8.1 Growth-Profitability Analysis

8.2 Market Opportunity Analysis

9. Research Methodology

9.1 Market Definitions and Assumptions

9.2 Abbreviations Used

9.3 Research Approach and Sample Size Inclusion

9.4 Industry Experts Interviewed

9.5 Consolidated Research Approach

9.6 Primary Research Approach

9.7 Research Limitations and Conclusion

Appendix: Expert Interview Transcripts

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The research began with a comprehensive mapping of the KSA Aquaculture Feed value chain, including feed manufacturers, hatcheries, aquaculture farms, distribution partners, and regulatory bodies such as MEWA, SFDA, and SAMAQ. Secondary research was conducted through proprietary and public sources like company websites, government reports, industry articles, and global databases (e.g., World Bank, Statista, GASTAT). This phase helped identify key variables such as feed type (Animal, Plant, Specialized), protein composition (High, Medium, Low), species breakdown, and pricing benchmarks. These inputs shaped the hypothesis framework and segmentation logic for the study.

Step 2: Market Analysis and Construction

Market sizing was executed using a triangulated approach that factored in aquaculture production volumes by species, feed conversion ratios (FCRs), and average price per ton across feed categories. Feed demand was derived using base-year aquaculture output (190K tons in 2024), multiplied by FCRs specific to fish, shrimp, and crustaceans. Pricing inputs for animal, plant, and specialized feed were gathered through supplier interviews. Segmentation was developed across dimensions such as feed type, protein content, form, end-use, and distribution mode. The analysis also incorporated government incentives, climate conditions, and production scale to estimate both volume and value outlooks through 2030.

Step 3: Hypothesis Validation and Expert Consultation

Primary research involved over 4050 stakeholders, including aquaculture feed manufacturers, procurement heads, hatchery managers, and regulatory officials. CATI (Computer-Assisted Telephonic Interviews) were conducted with representatives from leading companies such as NAQUA, ARASCO, Adisseo, Skretting, Bernaqua, and Alltech Coppens. Interviews explored feed price ranges, production capacity, demand trends, procurement behavior, and input sourcing challenges. Additionally, insights from 1015 production officers and 510 professionals from regulatory bodies helped validate assumptions on licensing norms, quality standards, and procurement cycles. Industry databases like Vedak, Insight Alpha, and Guidepoint were also used to supplement field inputs.

Step 4: Research Synthesis and Final Output

Data obtained through primary interviews and secondary sources was cross-validated using sanity checks involving multiple stakeholders. Segment-level insights were synthesized, and base-year figures were calibrated using feedback from large feed suppliers and aquaculture farms. Forecasts were built on the back of aquaculture expansion targets (Vision 2030), evolving feed preferences, and regulatory developments. Market estimates factored in innovation trends in feed (e.g., functional and medicated feed), raw material sourcing shifts, price fluctuations, and international trade influences. The final output provides a robust view of the KSA aquafeed market across demand drivers, bottlenecks, and growth outlook up to 2030.

Frequently Asked Questions

01. How big is the KSA Aquaculture Feed Market?

The KSA Aquaculture Feed Market was valued at USD 500 million, driven by rising seafood consumption and expanding domestic aquaculture production. Growth is supported by private sector investments and improved feed technology adoption.

02. What are the challenges in the KSA Aquaculture Feed Market?

The KSA Aquaculture Feed Market faces challenges such as dependence on imported raw materials, leading to cost volatility and supply delays. Additionally, salinity variability across coastal regions affects feed performance, necessitating species-specific feed adaptations. Small-scale producers also struggle with limited R&D capacity and competition from vertically integrated players.

03. Who are the major players in the KSA Aquaculture Feed Market?

Key players in the KSA Aquaculture Feed Market include NAQUA, ARASCO, Skretting, Adisseo, Bernaqua, and Alltech Coppens. These companies offer a wide portfolio of shrimp and fish feed across high-protein, plant-based, and specialized categories. Upcoming entrants like Cargill and Calysta are establishing local production to tap into the regions aquaculture growth.

04. What are the growth drivers of the KSA Aquaculture Feed Market?

KSA Aquaculture Feed Market growth is fueled by increasing domestic aquaculture output, rising demand for high-performance feed with better FCRs, and the governments push for seafood self-sufficiency under Vision 2030. Additionally, export opportunities and partnerships for sustainable feed innovations are expanding the market potential.

05. Which segment dominates the KSA Aquaculture Feed Market?

By feed type, Animal-Based feed holds a dominant in KSA Aquaculture Feed Market position due to its superior nutritional profile and better feed conversion efficiency, making it a preferred choice among commercial aquaculture farms. Within protein composition, High-Protein feed is most widely used, supporting intensive farming practices. Species-wise, shrimp and seabass production contribute the most to feed consumption, driven by their demand for high-performance and quality feed.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.