KSA Autonomous Vehicle Market Outlook to 2030

Region:Middle East

Author(s):Naman Rohilla

Product Code:KROD7753

Region:Middle East

Author(s):Naman Rohilla

Product Code:KROD7753

December 2024

89

The KSA autonomous vehicle market is dominated by several key players, ranging from global automakers to local tech innovators. The market consolidation highlights the competitive edge held by companies with R&D investments and strategic partnerships. Global firms such as Tesla and Waymo are expanding their operations in KSA through collaborations with local entities, leveraging the countrys favourable regulatory environment and robust investment in smart infrastructure.

Over the next five years, the KSA autonomous vehicle market is expected to experience growth, driven by continuous government support, advancements in autonomous driving technology, and increasing consumer interest in AI-driven mobility solutions. The development of smart cities, particularly NEOM, is a central factor propelling the adoption of autonomous vehicles. Additionally, international players are expected to strengthen their presence through collaborations with local industries, enhancing market competitiveness.

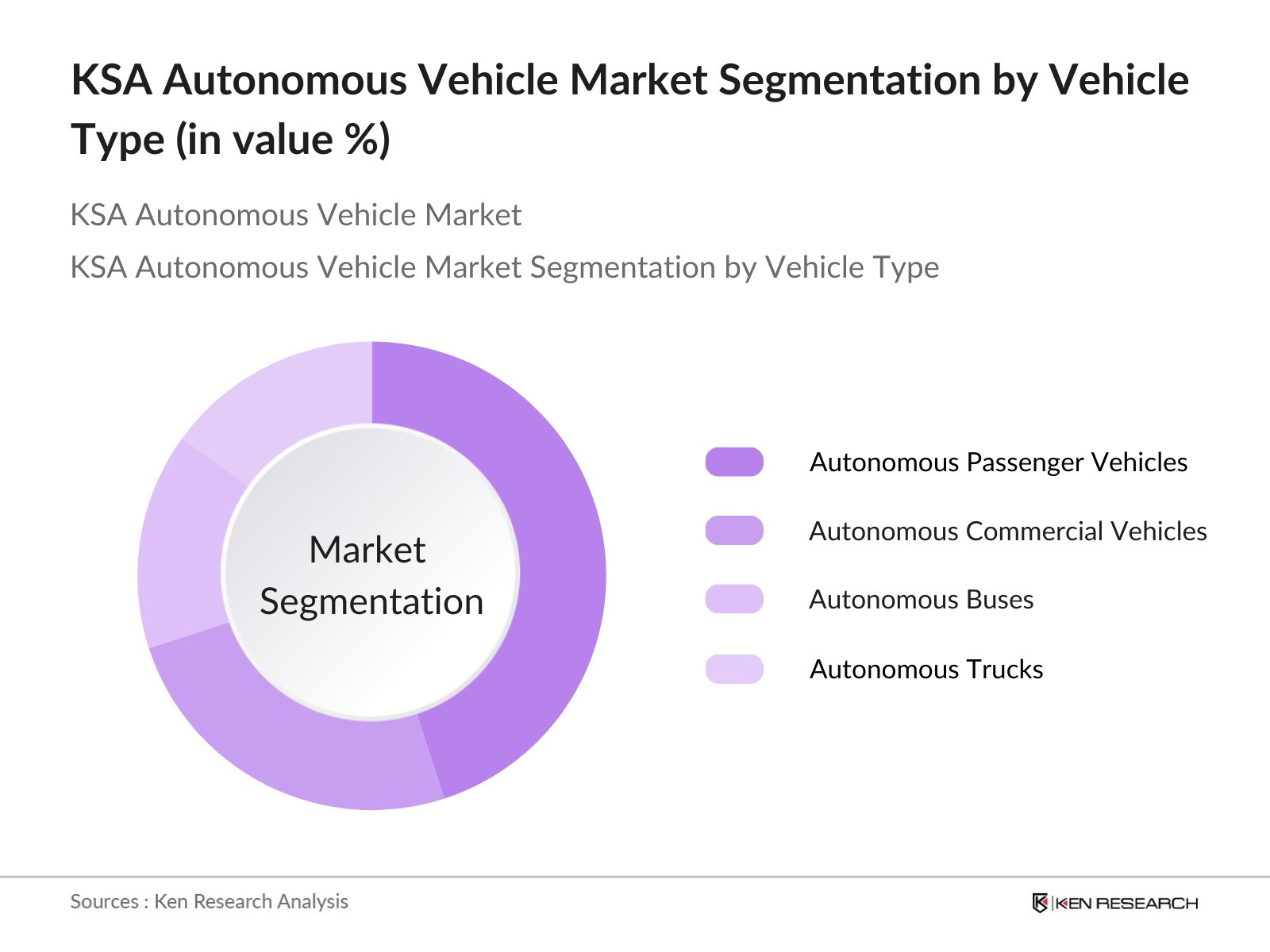

By Vehicle Type | Autonomous Passenger Vehicles Autonomous Commercial Vehicles Autonomous Buses Autonomous Trucks |

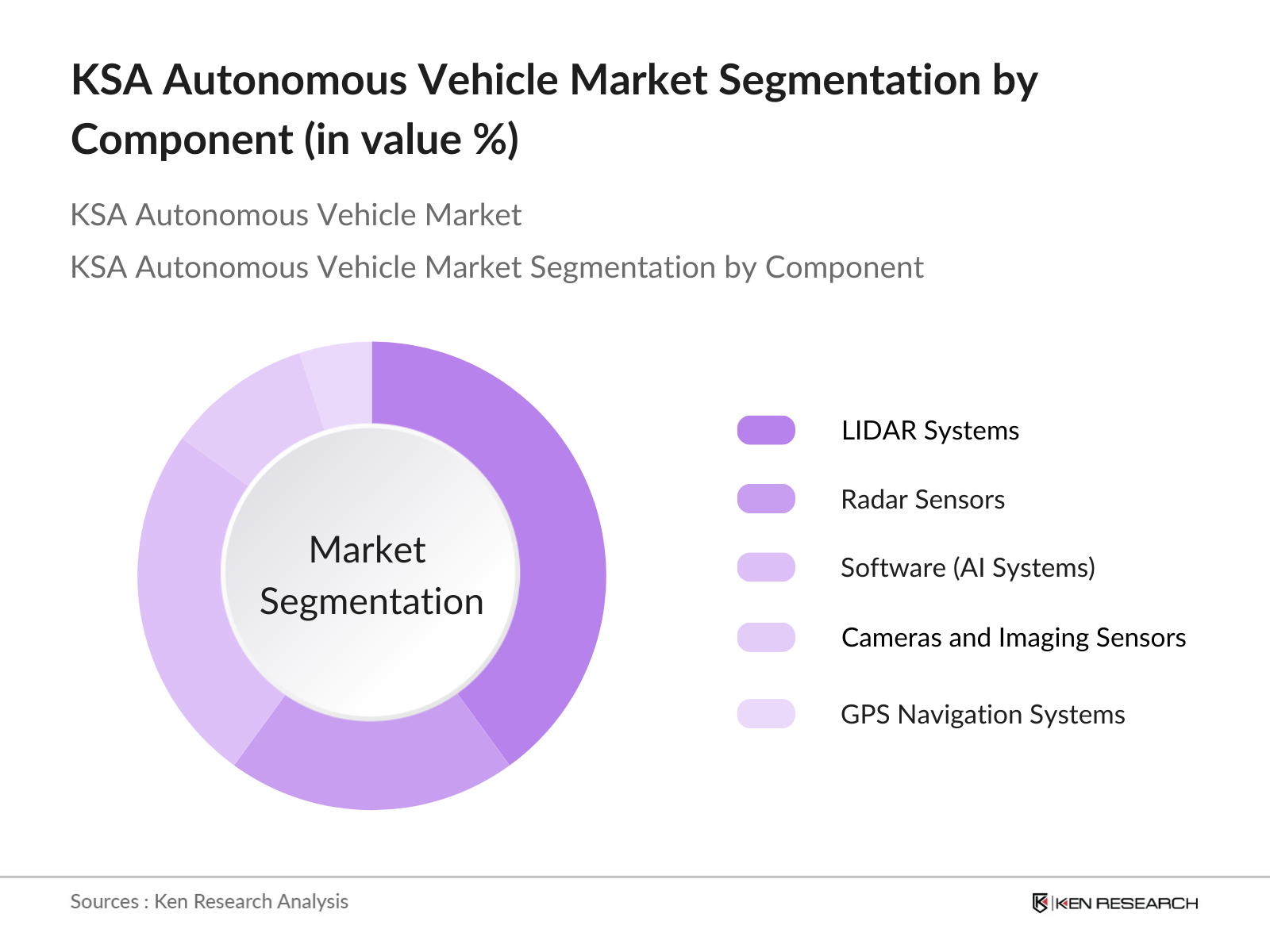

By Component | LIDAR Systems Radar Sensors Software (Autonomous Driving Software) Cameras and Imaging Sensors GPS and Navigation Systems |

By Application | Autonomous Ride-Hailing Services Freight Transport and Logistics Public Transportation Last-Mile Delivery |

By Level of Automation | Level 1 Driver Assistance Level 2 Partial Automation Level 3 Conditional Automation Level 4 High Automation Level 5 Full Automation |

By Region | Riyadh Jeddah Eastern Province Mecca Medina |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Government Initiatives (e.g., Vision 2030, Public Investment Fund)

3.1.2. Advancements in AI and Machine Learning (Autonomous Vehicle Software Integration)

3.1.3. Shift Towards Sustainable Transportation (Reduced Carbon Footprint, EV Integration)

3.1.4. Urban Mobility Infrastructure (Smart Cities Development, High-Tech Roads)

3.2. Market Challenges

3.2.1. Regulatory Barriers (Approval and Testing Regulations)

3.2.2. High Capital Investment (Initial R&D and Technology Costs)

3.2.3. Public Acceptance and Safety Concerns (Perception of Autonomous Vehicles)

3.2.4. Cybersecurity Risks (Data Privacy and Autonomous System Hacking)

3.3. Opportunities

3.3.1. Expansion in Commercial Fleets (Logistics, Ride-Sharing)

3.3.2. Government-Private Partnerships (Pilot Programs, National Testing Zones)

3.3.3. Growing Investments from International Tech Firms (Market Penetration by Global OEMs)

3.3.4. Autonomous Vehicle Adoption in Mega Projects (NEOM, Qiddiya, Red Sea Project)

3.4. Trends

3.4.1. EV and Autonomous Vehicle Convergence (Integration of Electric Powertrains)

3.4.2. Use of AI-Based Decision Making (Advanced Traffic Management and Routing Systems)

3.4.3. Autonomous Public Transport (Self-Driving Buses and Shuttles in Smart Cities)

3.4.4. Rise in Shared Mobility Solutions (Autonomous Ride-Hailing Platforms)

3.5. Regulatory Framework

3.5.1. Ministry of Transport and Logistic Services Guidelines

3.5.2. Autonomous Vehicle Testing and Certification Standards (King Abdulaziz City for Science and Technology KACST Initiatives)

3.5.3. Emission Norms and Environmental Policies (Alignment with Vision 2030 Goals)

3.5.4. Data Privacy Laws and Cybersecurity Protocols

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Automotive OEMs, Tech Startups, Government Entities)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem (Innovation Clusters, International Tech Collaborations)

4.1. By Vehicle Type (In Value %)

4.1.1. Autonomous Passenger Vehicles

4.1.2. Autonomous Commercial Vehicles

4.1.3. Autonomous Buses

4.1.4. Autonomous Trucks

4.2. By Component (In Value %)

4.2.1. LIDAR Systems

4.2.2. Radar Sensors

4.2.3. Software (Autonomous Driving Software, AI Systems)

4.2.4. Cameras and Imaging Sensors

4.2.5. GPS and Navigation Systems

4.3. By Application (In Value %)

4.3.1. Autonomous Ride-Hailing Services

4.3.2. Freight Transport and Logistics

4.3.3. Public Transportation

4.3.4. Last-Mile Delivery

4.4. By Level of Automation (In Value %)

4.4.1. Level 1 Driver Assistance

4.4.2. Level 2 Partial Automation

4.4.3. Level 3 Conditional Automation

4.4.4. Level 4 High Automation

4.4.5. Level 5 Full Automation

4.5. By Region (In Value %)

4.5.1. Riyadh

4.5.2. Jeddah

4.5.3. Eastern Province

4.5.4. Mecca

4.5.5. Medina

5.1. Detailed Profiles of Major Competitors

5.1.1. NEOM Tech & Digital Company

5.1.2. Saudi Aramco

5.1.3. Lucid Motors

5.1.4. Tesla Inc.

5.1.5. General Motors

5.1.6. Aptiv

5.1.7. Uber ATG

5.1.8. Waymo

5.1.9. Nvidia Corporation

5.1.10. Mobileye

5.1.11. Baidu Apollo

5.1.12. Zoox (Amazon)

5.1.13. Intel Corporation

5.1.14. Aurora Innovation

5.1.15. Velodyne Lidar

5.2. Cross Comparison Parameters (Market-Specific)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Autonomous Vehicle Standards

6.2. Compliance Requirements

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Vehicle Type (In Value %)

8.2. By Component (In Value %)

8.3. By Application (In Value %)

8.4. By Level of Automation (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The first step in this research involved identifying critical stakeholders, including OEMs, technology providers, and regulatory bodies. Secondary research was conducted using proprietary databases, and government reports to define key market variables affecting the KSA autonomous vehicle market, such as fleet sizes, regulatory influences, and R&D activities.

Historical data from industry reports and government sources were used to analyze market penetration and market dynamics. The evaluation focused on fleet sizes, market revenue, and the growth of autonomous vehicle services, which provided insights into market opportunities and challenges.

Hypotheses regarding market growth were validated through interviews with industry experts, including representatives from Saudi government agencies and leading autonomous vehicle manufacturers. This step ensured that the report was based on practical insights and validated market data.

The final phase involved synthesizing the gathered data and insights to produce a comprehensive and validated report. Additional engagement with autonomous vehicle providers ensured that the data represented current market conditions, offering a robust analysis of the KSA autonomous vehicle market.

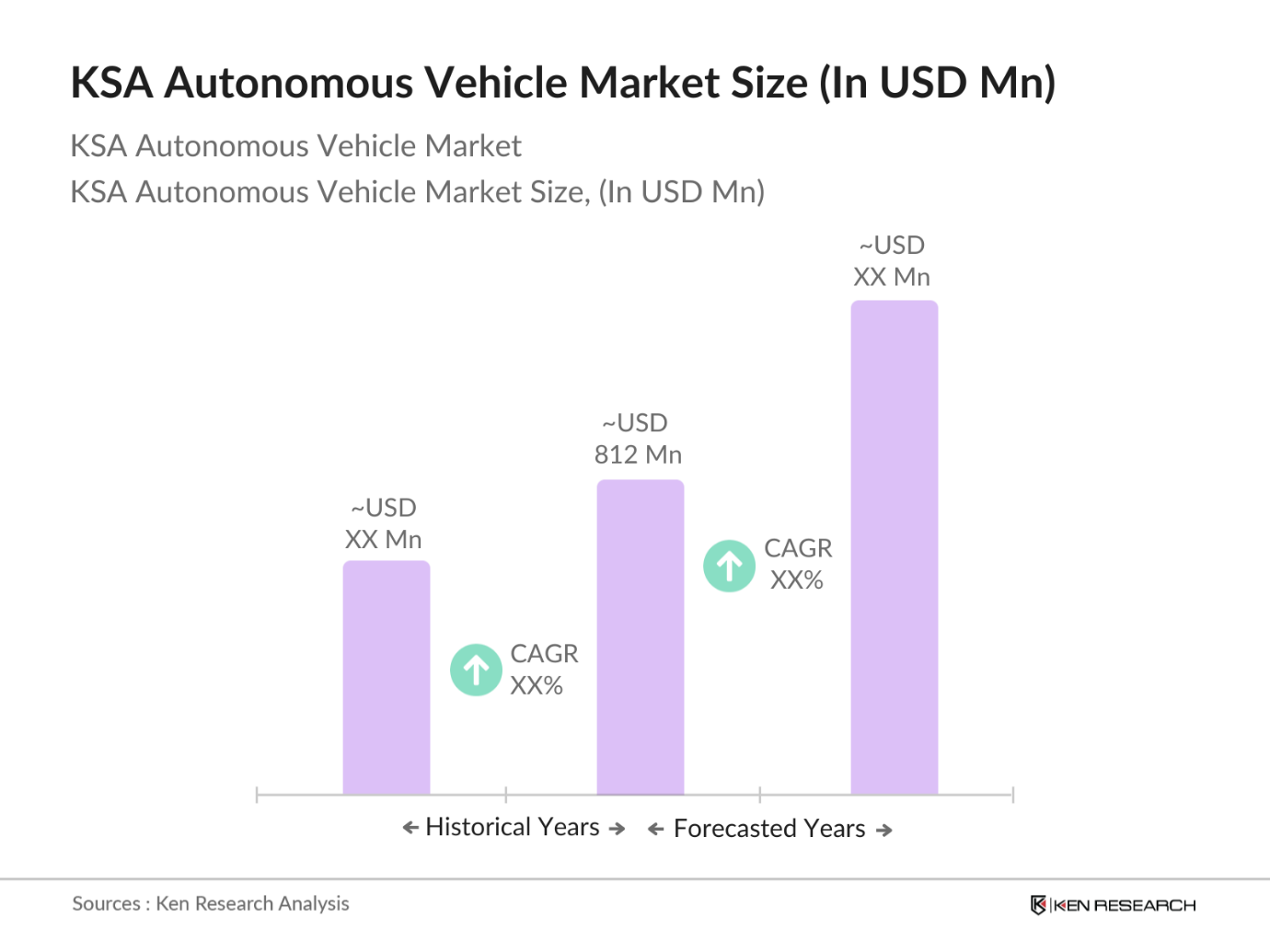

The KSA autonomous vehicle market is valued at USD 812 million, driven by investments in smart city projects, government support, and international partnerships with major autonomous technology companies.

Key challenges in the KSA autonomous vehicle market include regulatory approval for widespread autonomous vehicle usage, high upfront capital investment for R&D, and public concerns around safety and cybersecurity, which have slowed the pace of adoption.

Major players in the KSA autonomous vehicle market include NEOM Tech & Digital, Lucid Motors, Tesla Inc., Waymo, and Uber ATG. These companies have established dominance through R&D, strategic partnerships, and government collaborations.

Growth in the KSA autonomous vehicle market is driven by government-led initiatives, such as Vision 2030, which prioritize smart city development, sustainable transport, and tech innovation. Autonomous vehicle adoption is further supported by international investments and partnerships with global automakers.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.