KSA Biofuel Market Outlook to 2030

Region:Middle East

Author(s):Mukul

Product Code:KROD2915

October 2024

81

About the Report

KSA Biofuel Market Overview

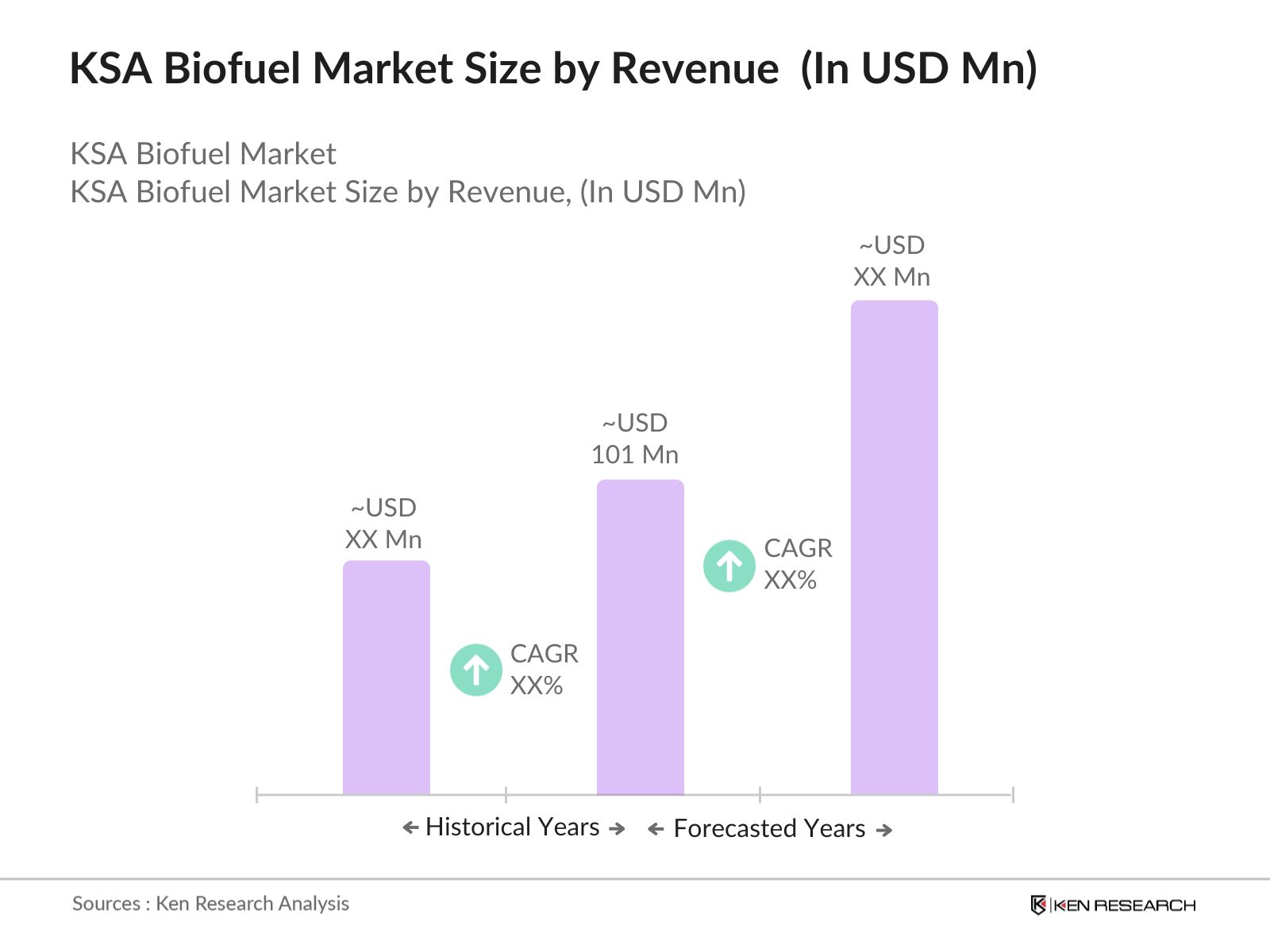

- The biofuel market in Saudi Arabia size by revenue at USD 101 million based on a five-year historical analysis. This market is primarily driven by Saudi Arabia's push toward diversifying its energy mix as part of Vision 2030 and reducing reliance on crude oil exports. The focus on renewable energy sources, along with government incentives, has bolstered domestic production capacity and consumption of biofuels.

- Riyadh and Jeddah are the dominant cities in the KSA biofuel market due to their well-developed infrastructure, proximity to major biofuel production facilities, and access to feedstock sources such as agricultural waste and municipal solid waste. Additionally, these cities host several key industrial players contributing to significant production capacity, creating a competitive edge for local biofuel manufacturers.

- The NREP is Saudi Arabias key initiative driving renewable energy adoption, including biofuels. The program, launched in 2020, targets the generation of 58.7 GW of renewable energy by 2030, including biofuel integration in energy production. The program aims to reduce greenhouse gas emissions by 130 million tons annually, contributing to Saudi Arabia's Vision 2030 objectives. Biofuels are expected to play a role in achieving this target by diversifying energy sources and providing an alternative to fossil fuels.

KSA Biofuel Market Segmentation

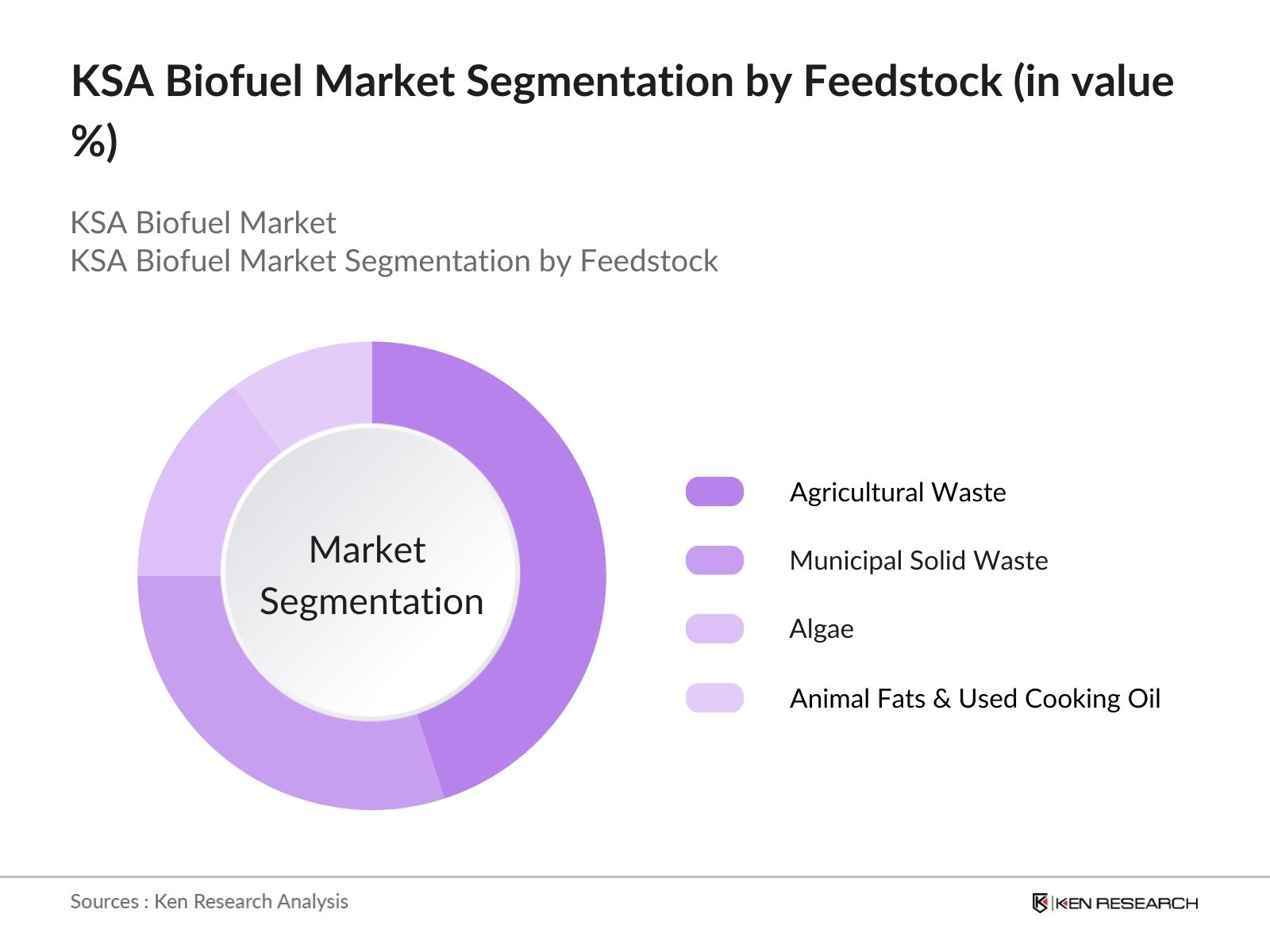

- By Feedstock Type: The KSA biofuel market is segmented by feedstock type into agricultural waste, municipal solid waste, algae, and animal fats & used cooking oil. Agricultural waste dominates this segment due to the abundance of crop residues and other plant-based waste materials available from Saudi Arabias agricultural regions. This feedstock is widely available and cost-effective, making it a prime choice for biofuel production.

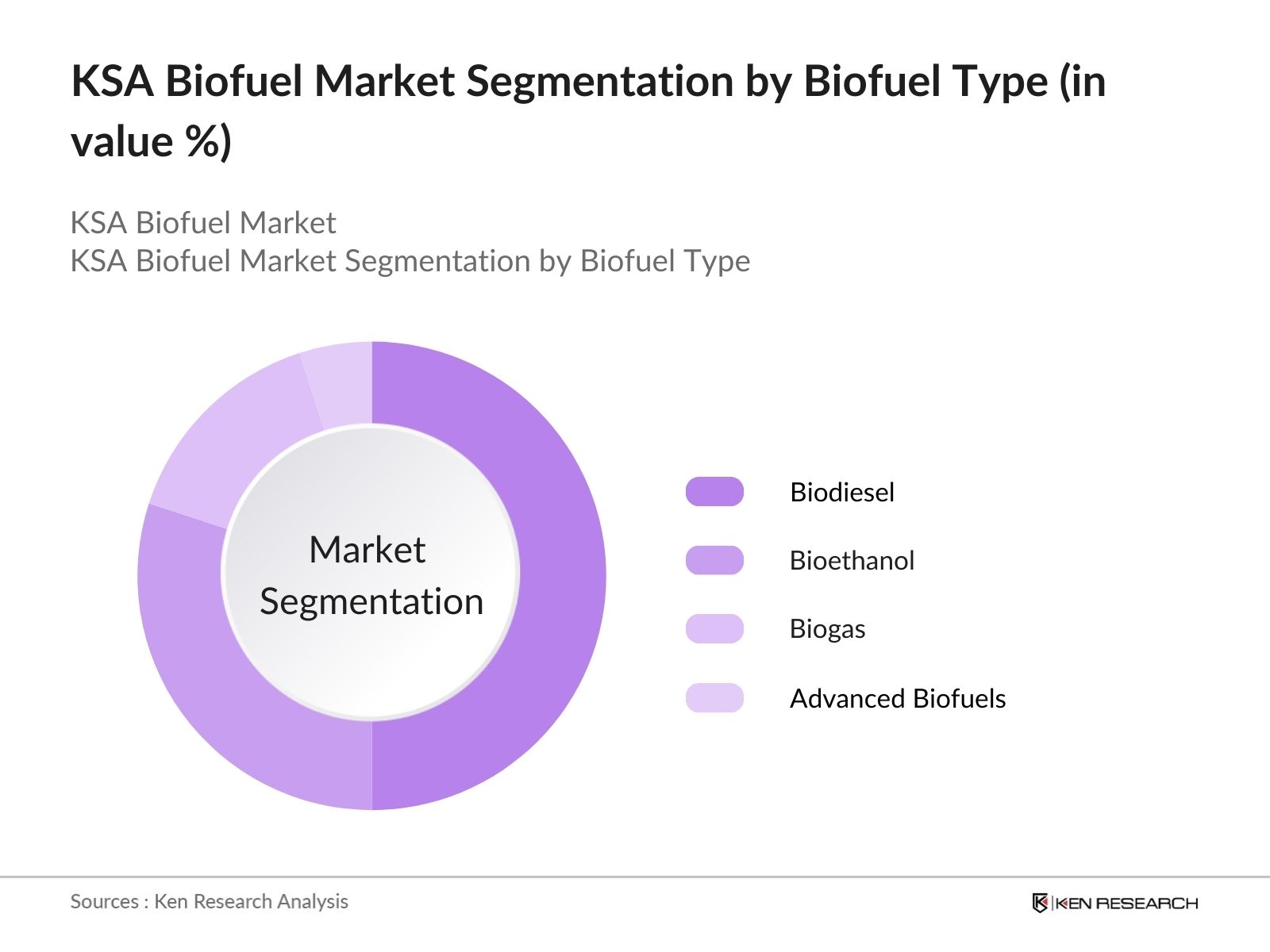

- By Biofuel Type: The biofuel market is further segmented by biofuel type into biodiesel, bioethanol, biogas, and advanced biofuels (second-generation biofuels). Biodiesel holds the dominant share in this segment. Its use in the transport and power generation sectors is growing rapidly, supported by government mandates for biodiesel blending. The flexibility in feedstock types, from vegetable oils to animal fats, enhances its wide-scale adoption.

KSA Biofuel Market Competitive Landscape

The KSA biofuel market is characterized by a few dominant players, both local and international. Companies like Saudi Aramco and SABIC have entered the biofuel market, leveraging their extensive expertise in the energy sector. Additionally, the market includes international companies collaborating with local entities to meet increasing domestic and international demand.

|

Company |

Establishment Year |

Headquarters |

Feedstock Sources |

Production Capacity |

Technology Expertise |

Geographic Presence |

R&D Investments |

Market Strategy |

|

Saudi Aramco |

1933 |

Dhahran, KSA |

||||||

|

SABIC |

1976 |

Riyadh, KSA |

||||||

|

Yanbu Biofuel Company |

1992 |

Yanbu, KSA |

||||||

|

Neste Corporation |

1948 |

Espoo, Finland |

||||||

|

Renewable Energy Group (REG) |

2006 |

Ames, USA |

KSA Biofuel Industry Analysis

KSA Biofuel Market Growth Drivers:

- International Demand for Biofuels: Saudi Arabia is well-positioned to cater to the growing global demand for biofuels. The European Union, for example, imported 23 million barrels of biofuels in 2023, creating export opportunities for Saudi producers. With stringent carbon reduction policies worldwide, international demand for sustainable energy sources like biofuels has grown. Saudi Arabia is investing in expanding its biofuel capacity to meet this demand, with a 2023 export focus targeting Europe, Asia, and Africa.

- Domestic Feedstock Availability: Saudi Arabia's agricultural sector produces significant quantities of biomass that can be converted into biofuel feedstock. The country generated over 20 million tons of agricultural residues annually by 2023, primarily from date palms and livestock waste. These biomass resources present a viable alternative for biofuel production. In 2023, the Saudi Ministry of Environment, Water, and Agriculture began focusing on developing biofuel from domestic feedstocks, lowering the reliance on imported fuel and helping to meet the increasing energy demand of 1.6% annually.

- Technological Advancements in Biofuel Production: Saudi Arabia is advancing biofuel production technologies to make them more efficient and cost-effective. The country is exploring second-generation biofuels from non-food crops, leveraging enzymes and advanced processing methods. In 2023, the government invested $2.2 billion in biofuel R&D projects, including collaboration with international companies to scale up domestic production. The strategic implementation of AI and IoT to optimize biofuel production further highlights the nation's focus on technological innovations to meet growing energy demands and environmental targets.

KSA Biofuel Market Restraints

- Lack of Infrastructure: Saudi Arabias biofuel infrastructure is underdeveloped, with limited refineries and pipelines dedicated to biofuel production and distribution. As of 2023, the country had less than 5 biofuel-specific facilities, compared to over 100 oil refineries. This limited capacity restricts the growth of biofuel in the domestic energy mix. The Ministry of Energy is planning to invest in building dedicated biofuel pipelines, which could alleviate the infrastructure gap by 2025, but the current state remains a significant market challenge.

- Competition with Fossil Fuels: Fossil fuels dominate the Saudi energy landscape, with oil production reaching 9.1 million barrels per day in 2023. Biofuels face stiff competition from cheap and readily available fossil fuels, especially given Saudi Arabias vast oil reserves. The low cost of fossil fuel production makes it difficult for biofuels to compete in terms of pricing, and government subsidies for oil further exacerbate the challenge. According to the World Bank, fossil fuel subsidies in Saudi Arabia exceeded $28 billion in 2023, limiting biofuel market penetration.

KSA Biofuel Market Future Outlook

Over the next five years, the KSA biofuel market is expected to see strong growth driven by government incentives, increasing global demand for sustainable energy sources, and the diversification of the Kingdom's energy portfolio. The expansion of biofuel production facilities and investment in second-generation biofuels will also play a key role in shaping the market. Furthermore, technological advancements in biofuel production processes are expected to reduce costs and improve efficiency, thereby increasing biofuel adoption across various industries

Market Opportunities

- Increasing Adoption of Advanced Biofuels: Saudi Arabia has significant potential in the production and use of second-generation biofuels. In 2023, the global advanced biofuel market was valued at $21 billion, with Saudi Arabia emerging as a key player due to its investments in biomass conversion technologies. The governments focus on non-food biomass sources, such as algae and waste oils, offers an opportunity for sustainable growth. With advancements in production technologies, Saudi Arabia is poised to cater to domestic energy demand, which grew to 409 TWh in 2023, and capitalize on growing international interest in advanced biofuels.

- Potential for Export Markets: Saudi Arabia's strategic location makes it a prime candidate for exporting biofuels to Europe and Asia, where demand is increasing due to stringent carbon emissions regulations. In 2023, Europes demand for biofuels grew by 5 million barrels, with Saudi Arabia well-positioned to meet this demand. The Kingdom is currently negotiating export agreements with countries like Germany and Japan, aiming to increase biofuel exports by 15% over the next five years. Export market expansion provides a significant growth opportunity for Saudi biofuel producers.

Scope of the Report

|

Segment |

Sub-Segments |

|

Feedstock Type |

Agricultural Waste |

|

Municipal Solid Waste |

|

|

Algae |

|

|

Animal Fats and Used Cooking Oil |

|

|

Biofuel Type |

Biodiesel |

|

Bioethanol |

|

|

Biogas |

|

|

Advanced Biofuels (Second-Generation Biofuels) |

|

|

Application |

Transportation (Road Transport, Aviation, Marine) |

|

Power Generation |

|

|

Industrial Usage |

|

|

Production Technology |

Fermentation |

|

Transesterification |

|

|

Pyrolysis |

|

|

Gasification |

|

|

Region |

Central Region |

|

Western Region |

|

|

Eastern Region |

|

|

Northern Region |

|

|

Southern Region |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Biofuel Production Companies

Feedstock Suppliers

Transport and Logistics Companies

Energy Utilities

Government and Regulatory Bodies (Saudi Ministry of Energy, Saudi Aramco Energy Ventures)

Investment and Venture Capitalist Firms

Environmental Organizations

Industrial Users (Manufacturing, Power Generation)

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

Saudi Aramco

SABIC

Yanbu Biofuel Company

Neste Corporation

Renewable Energy Group (REG)

Archer Daniels Midland Company

POET LLC

Verbio AG

Green Plains Inc.

Tasnee

Advanced Petrochemical Company

Gulf Biofuel Co.

Al Khafrah Group

National Oilwell Varco

Royal Dutch Shell

Table of Contents

1. KSA Biofuel Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy (Feedstock Types, Biofuel Types, Production Technology)

1.3 Market Growth Rate (CAGR, Growth Drivers, Market Trends)

1.4 Market Segmentation Overview (Feedstock, Biofuel Type, Application, Technology, Region)

2. KSA Biofuel Market Size by Revenue (In USD Mn)

2.1 Historical Market Size (Demand and Supply Dynamics, Key Milestones)

2.2 Year-On-Year Growth Analysis (Production Capacity, Consumption, Trade Balance)

2.3 Key Market Developments and Milestones (Government Initiatives, Major Investments)

3. KSA Biofuel Market Analysis

3.1 Growth Drivers

3.1.1 Renewable Energy Targets

3.1.2 Domestic Feedstock Availability

3.1.3 Technological Advancements in Biofuel Production

3.1.4 International Demand for Biofuels

3.2 Market Challenges

3.2.1 High Production Costs

3.2.2 Lack of Infrastructure

3.2.3 Competition with Fossil Fuels

3.2.4 Regulatory Barriers

3.3 Opportunities

3.3.1 Increasing Adoption of Advanced Biofuels

3.3.2 Potential for Export Markets

3.3.3 Strategic Collaborations with International Firms

3.4 Trends

3.4.1 Integration of Biofuels in Transport and Aviation

3.4.2 Blending Mandates for Fuel Mix

3.4.3 Shift Towards Second-Generation Biofuels

3.5 Government Regulations

3.5.1 National Renewable Energy Program (NREP)

3.5.2 Biofuel Blending Mandates

3.5.3 Subsidies and Incentives for Biofuel Projects

3.5.4 Carbon Emission Reduction Initiatives

3.6 SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7 Stakeholder Ecosystem (Feedstock Producers, Biofuel Producers, Distributors, Consumers)

3.8 Porters Five Forces (Bargaining Power of Suppliers, Buyers, Threat of Substitutes, New Entrants, Rivalry)

3.9 Competitive Ecosystem (Key Competitors, New Entrants, Market Concentration)

4. KSA Biofuel Market Segmentation

4.1 By Feedstock Type (In Value %):

4.1.1 Agricultural Waste

4.1.2 Municipal Solid Waste

4.1.3 Algae

4.1.4 Animal Fats and Used Cooking Oil

4.2 By Biofuel Type (In Value %):

4.2.1 Biodiesel

4.2.2 Bioethanol

4.2.3 Biogas

4.2.4 Advanced Biofuels (Second-Generation Biofuels)

4.3 By Application (In Value %):

4.3.1 Transportation (Road Transport, Aviation, Marine)

4.3.2 Power Generation

4.3.3 Industrial Usage

4.4 By Production Technology (In Value %):

4.4.1 Fermentation

4.4.2 Transesterification

4.4.3 Pyrolysis

4.4.4 Gasification

4.5 By Region (In Value %):

4.5.1 Central Region

4.5.2 Western Region

4.5.3 Eastern Region

4.5.4 Northern Region

4.5.5 Southern Region

5. KSA Biofuel Market Competitive Analysis

5.1 Detailed Profiles of Major Companies:

5.1.1 Saudi Aramco

5.1.2 Tasnee

5.1.3 Advanced Petrochemical Company

5.1.4 Al Khafrah Group

5.1.5 Yanbu Biofuel Company

5.1.6 SABIC

5.1.7 National Oilwell Varco

5.1.8 Gulf Biofuel Co.

5.1.9 Renewable Energy Group (REG)

5.1.10 Neste Corporation

5.1.11 Archer Daniels Midland Company

5.1.12 Royal Dutch Shell

5.1.13 POET LLC

5.1.14 Verbio AG

5.1.15 Green Plains Inc.

5.2 Cross Comparison Parameters (Production Capacity, Feedstock Diversity, Geographic Presence, Revenue, Technology Focus, R&D Investment, Biofuel Yield Efficiency, Strategic Partnerships)

5.3 Market Share Analysis

5.4 Strategic Initiatives (Joint Ventures, Biofuel Production Expansion)

5.5 Mergers and Acquisitions

5.6 Investment Analysis (Government Grants, Venture Capital, Private Equity)

5.7 Government Grants (Subsidies, Carbon Credits, R&D Funds)

5.8 Private Equity Investments

6. KSA Biofuel Market Regulatory Framework

6.1 Environmental Standards (GHG Emission Limits, Renewable Fuel Standards)

6.2 Compliance Requirements (Biofuel Blending Mandates, Certification)

6.3 Certification Processes (ISCC, RSB)

7. KSA Biofuel Future Market Size by Revenue (In USD Mn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth (Renewable Energy Targets, Global Market Demand)

8. KSA Biofuel Future Market Segmentation

8.1 By Feedstock Type (In Value %)

8.2 By Biofuel Type (In Value %)

8.3 By Application (In Value %)

8.4 By Production Technology (In Value %)

8.5 By Region (In Value %)

9. KSA Biofuel Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis (Target Consumer Segments)

9.3 Marketing Initiatives (Target Marketing Channels)

9.4 White Space Opportunity Analysis (Untapped Biofuel Applications)

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying major stakeholders in the KSA biofuel market ecosystem. Extensive desk research utilizing industry databases and proprietary tools is conducted to define the key variables that affect the market dynamics, such as production capacity, feedstock availability, and biofuel adoption rates.

Step 2: Market Analysis and Construction

This phase focuses on compiling and analyzing historical data on production volumes, market penetration, and biofuel consumption across various sectors in Saudi Arabia. The analysis helps establish a reliable forecast for market trends and growth opportunities.

Step 3: Hypothesis Validation and Expert Consultation

Through interviews with industry experts, including manufacturers and energy consultants, hypotheses on market growth and potential are validated. This provides operational insights and further corroborates the data gathered from primary and secondary research.

Step 4: Research Synthesis and Final Output

Finally, a detailed synthesis of the collected data is conducted, drawing from interactions with biofuel producers. This ensures a comprehensive understanding of the KSA biofuel market, its segments, and the opportunities for future growth.

Frequently Asked Questions

1.How big is the KSA Biofuel Market?

The KSA biofuel market size by revenue USD 101 million, driven by the increasing shift towards renewable energy as part of the Kingdom's Vision 2030 initiative.

2.What are the challenges in the KSA Biofuel Market?

Key challenges in the KSA Biofuel Market include high production costs, limited infrastructure for biofuel distribution, and competition with traditional fossil fuels. Regulatory hurdles also pose a challenge to market expansion.

3.Who are the major players in the KSA Biofuel Market?

The major players in the KSA Biofuel Market include Saudi Aramco, SABIC, Neste Corporation, Renewable Energy Group, and Yanbu Biofuel Company. These companies dominate due to their large production capacities and technological advancements.

4.What are the growth drivers of the KSA Biofuel Market?

Growth drivers include government support through subsidies, increasing global demand for sustainable fuels, and advancements in biofuel production technologies, particularly in biodiesel and biogas.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.