KSA Catheter Market Outlook to 2030

Region:Saudi Arabia

Author(s):Yogita Sahu

Product Code:KROD6939

Region:Saudi Arabia

Author(s):Yogita Sahu

Product Code:KROD6939

December 2024

93

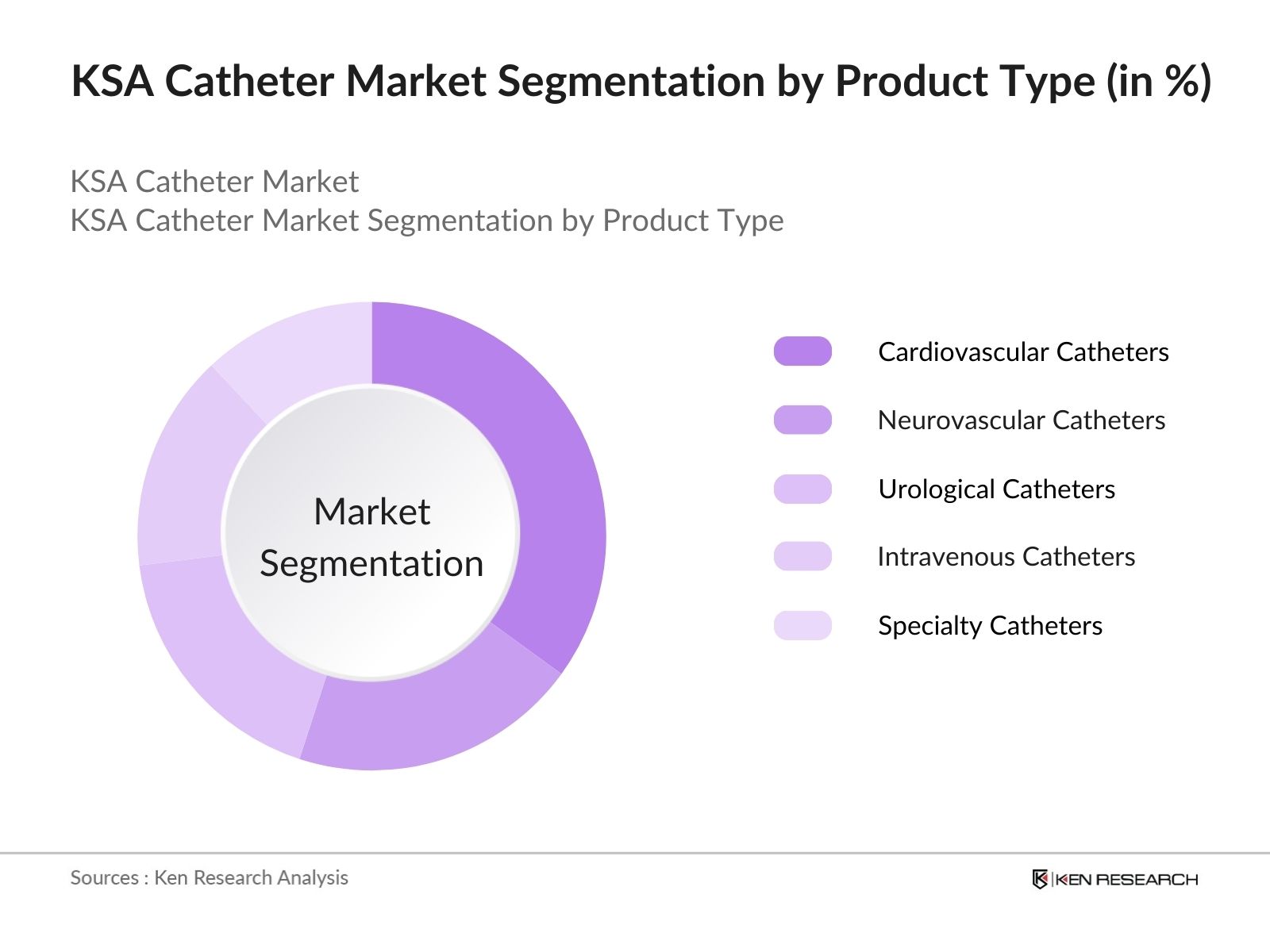

By Product Type: The market is segmented by product type into cardiovascular catheters, neurovascular catheters, urological catheters, intravenous catheters, and specialty catheters. Cardiovascular catheters hold the dominant market share due to the rising number of cardiovascular diseases, such as coronary artery disease and arrhythmia, which require frequent catheter-based interventions. The demand for these procedures is steadily increasing due to the aging population and the adoption of minimally invasive treatments.

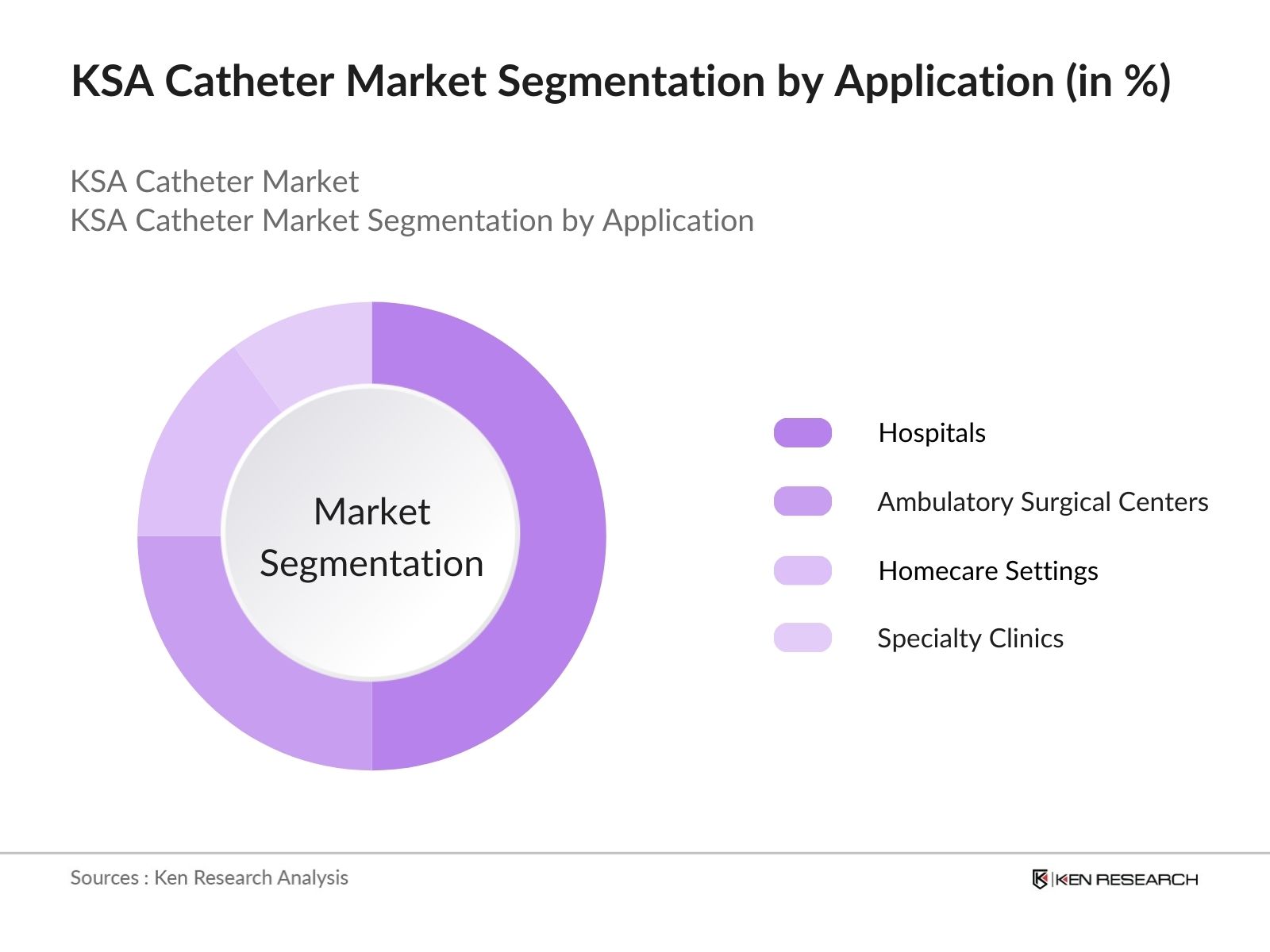

By Application: The market is also segmented by application into hospitals, ambulatory surgical centers (ASCs), homecare settings, and specialty clinics. Hospitals hold the largest market share due to their extensive use of catheters for inpatient and surgical procedures. Hospitals have the infrastructure and specialized staff to handle complex catheterization, including cardiovascular and neurovascular interventions. Additionally, hospital stores manage a large inventory of medical devices, including a variety of catheters, ensuring a steady supply for procedures.

The market is dominated by a mix of global and regional players, each bringing advanced medical solutions to the market. The competitive landscape is shaped by product innovation, regulatory approvals, and strategic partnerships with healthcare institutions.

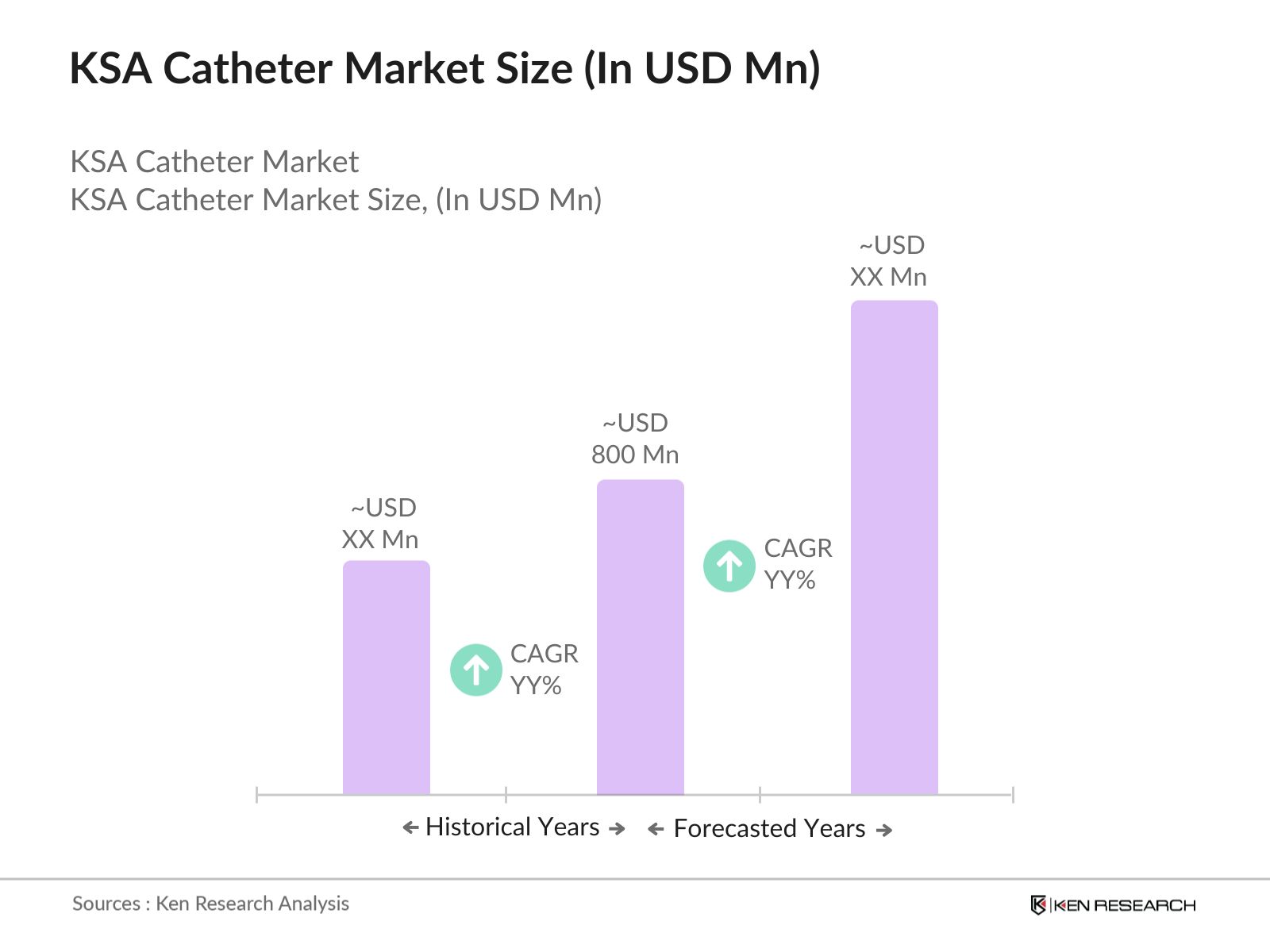

Over the next five years, the KSA catheter industry is expected to experience steady growth, driven by an increase in chronic diseases, especially cardiovascular and urological conditions, which are prevalent in the country.

|

Product Type |

Cardiovascular Neurovascular Urological Intravenous Specialty Catheters |

|

Application |

Hospitals ASCs Homecare Specialty Clinics |

|

Material |

Stainless Steel Platinum Iridium Other Advanced Materials |

|

End-User |

Hospital Stores Retail Stores Others |

|

Region |

Central Western Eastern Northern Southern |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Demand Drivers)

1.4. Market Segmentation Overview (Catheter Types and Use Cases)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments (Technological Advancements and Material Innovations)

3.1. Growth Drivers (Adoption of Minimally Invasive Procedures, Rising Chronic Diseases)

3.2. Market Challenges (Regulatory Approvals, Quality Control)

3.3. Opportunities (Increased Use of Remote Monitoring, Telemedicine)

3.4. Trends (Advanced Material Usage, Digital Healthcare Integration)

3.5. Government Regulation (Health Ministry Initiatives, Medical Device Regulation in KSA)

3.6. SWOT Analysis

3.7. Porters Five Forces

3.8. Competition Ecosystem

4.1. By Product Type (In Value %)

Cardiovascular Catheters

Neurovascular Catheters

Urological Catheters

Intravenous Catheters

Specialty Catheters

4.2. By Application (In Value %)

Hospitals

Ambulatory Surgical Centers

Homecare

Specialty Clinics

4.3. By Material (In Value %)

Stainless Steel

Platinum Iridium

Other Advanced Materials

4.4. By End-User (In Value %)

Hospital Stores

Retail Stores (E-commerce and Pharmacies)

Other Distribution Channels

4.5. By Region (In Value %)

Central

Western

Eastern

Northern

Southern

5.1. Detailed Profiles of Major Companies

5.1.1. Boston Scientific Corp

5.1.2. Medtronic PLC

5.1.3. Teleflex Inc

5.1.4. Nipro Corp

5.1.5. Terumo Corp

5.1.6. Qx Medical

5.1.7. Seigla Medical

5.1.8. B. Braun Melsungen AG

5.1.9. Edwards Lifesciences Corp

5.1.10. Abbott Laboratories

5.1.11. Cardinal Health

5.1.12. Cook Medical Inc.

5.1.13. Coloplast Corp

5.1.14. Smiths Medical

5.1.15. BD (Becton, Dickinson and Company)

5.2. Cross Comparison Parameters (Revenue, Market Share, Product Portfolio, Regulatory Approvals)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Subsidies

6.1. Compliance Requirements

6.2. Certification Processes

6.3. Import-Export Regulations (Medical Devices in Saudi Arabia)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Material (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsIn the initial phase, we map the ecosystem of the KSA catheter market. Extensive desk research and secondary data sources such as government healthcare reports and databases provide insight into critical market variables.

This phase involves collecting historical data on market size, product penetration, and hospital infrastructure. Evaluating the number of medical devices per capita and healthcare service quality helps verify market trends and future growth prospects.

We validate market assumptions through interviews with industry experts, including healthcare providers and executives from catheter manufacturing companies. These insights help refine the statistical models used in forecasting.

The final phase involves consolidating the collected data into a comprehensive report, integrating primary data from manufacturers and end-users, ensuring accurate market size projections and analysis.

The KSA catheter market was valued at USD 800 million, driven by the increasing prevalence of chronic diseases such as cardiovascular and neurovascular disorders, as well as the demand for minimally invasive procedures.

Challenges in the KSA catheter market include stringent regulatory approvals, concerns over quality control and infection risks, and the need for continuous innovation in catheter materials to ensure patient safety and comfort during long-term usage.

Key players in the KSA catheter market include Boston Scientific Corp, Medtronic PLC, Teleflex Inc, Nipro Corp, and Terumo Corp, dominating the market with their advanced product portfolios and established presence in the region.

The KSA catheter market is primarily driven by the rising incidence of chronic diseases, particularly cardiovascular and urological disorders, advancements in catheter technology, and the growing adoption of minimally invasive surgical procedures in major healthcare facilities across the country.

Over the next five years, the KSA catheter market is expected to grow steadily, with increased demand for specialized catheters, continued advancements in telemedicine and healthcare infrastructure, and more investments in healthcare from both the public and private sectors.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.