KSA Cereal Market Outlook to 2030

Region:Middle East

Author(s):Mukul

Product Code:KROD3569

October 2024

93

About the Report

KSA Cereal Market Overview

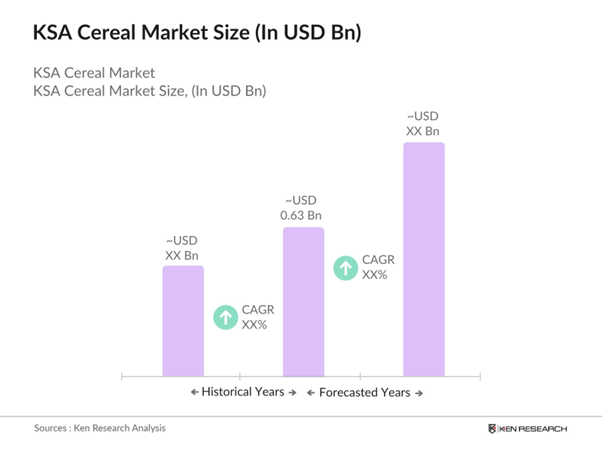

- The Kingdom of Saudi Arabia cereal market is valued at USD 0.63 billion, reflecting a steady demand driven by rising health consciousness and an increasing shift toward convenient and packaged food options. The market is primarily driven by the population's growing awareness of the benefits of whole grains, oats, and high-fiber cereals, which are being incorporated into everyday meals. Additionally, the government's Vision 2030 initiative has further fueled demand by focusing on improving food security and supporting local production, which encourages the growth of domestic cereal brands.

- Major cities such as Riyadh, Jeddah, and Dammam dominate the KSA cereal market due to their large populations, higher purchasing power, and evolving urban lifestyles that prioritize convenience in meal preparation. These cities also benefit from well-established retail chains and an increasing trend toward online grocery shopping, which helps facilitate the availability and accessibility of cereal products. Furthermore, expatriate communities in these cities, particularly those from Western countries, contribute to the growing demand for cereals in both hot and cold forms as breakfast staples.

- The SFDA plays a crucial role in regulating the quality and safety of cereal products in Saudi Arabia. The authority has stringent guidelines for food manufacturers, ensuring that cereals meet high standards for nutritional content, food safety, and labeling. In 2024, the SFDA introduced updated regulations for reducing sugar and sodium levels in breakfast cereals as part of a broader health initiative to combat rising obesity and diabetes rates. These regulatory requirements compel cereal manufacturers to reformulate products to meet health objectives.

KSA Cereal Market Segmentation

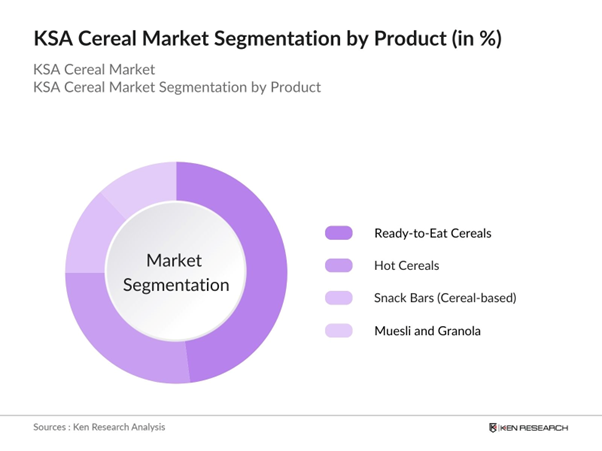

- By Product Type: The KSA cereal market is segmented by product type into ready-to-eat cereals, hot cereals, snack bars (cereal-based), and muesli and granola. Among these, ready-to-eat cereals hold the dominant market share, driven by their convenience, diverse flavor options, and widespread availability in hypermarkets and supermarkets. Additionally, major brands such as Kelloggs and Nestl, which have established strong brand recognition, continue to introduce innovative products that cater to local taste preferences and dietary trends, including whole-grain, fortified, and sugar-free options.

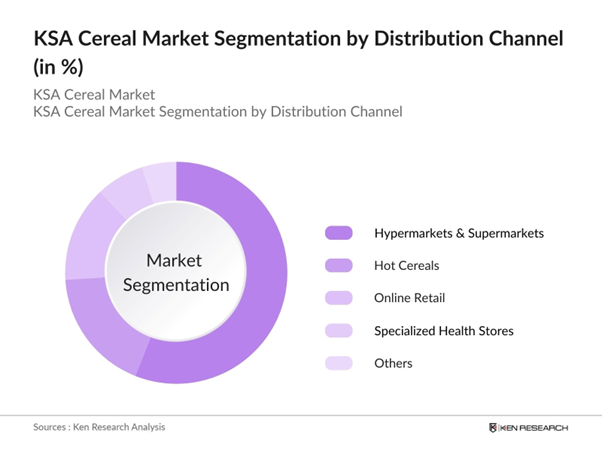

- By Distribution Channel: The cereal market in KSA is segmented by distribution channel into hypermarkets & supermarkets, convenience stores, online retail, specialized health stores, and others (traditional markets, local vendors). Hypermarkets and supermarkets dominate the market, accounting for the largest share due to their extensive reach and wide product variety. Consumers in urban areas frequently visit these stores for household groceries, and the presence of international and local cereal brands in these outlets ensures easy access.

KSA Cereal Market Competitive Landscape

The KSA cereal market is competitive, with key players focusing on product innovation, expanding distribution networks, and introducing healthier product lines to cater to the growing demand for nutritious breakfast options. The presence of global giants like Kelloggs and Nestl alongside strong regional players such as Almarai adds depth to the competitive landscape. The market is also seeing collaborations between international and local players to meet the evolving consumer preferences for functional and organic cereals.

|

Company |

Established |

Headquarters |

Global Reach |

Product Innovation |

Sustainability Initiatives |

Local Partnerships |

Retail Presence |

Marketing Strategy |

|

Kelloggs |

1906 |

USA |

||||||

|

Nestl S.A. |

1867 |

Switzerland |

||||||

|

Almarai |

1977 |

KSA |

||||||

|

Cereal Partners Worldwide |

1991 |

Switzerland |

||||||

|

Natures Path Foods, Inc. |

1985 |

Canada |

KSA Cereal Industry Analysis

Market Growth Drivers

- Rising Health Consciousness: Health consciousness in Saudi Arabia is driving consumer demand for organic and whole-grain cereals. According to the Saudi Ministry of Health, lifestyle diseases such as obesity and diabetes affect over 30 million residents, leading to increased awareness of healthier eating habits. Whole grain cereals, which provide higher fiber and essential nutrients, are gaining popularity. Organic cereal products, free from pesticides and artificial additives, align with this health trend. As of 2024, government-backed initiatives like the Healthy Food Strategy further encourage citizens to shift towards organic and whole-grain products as part of a balanced diet.

- Increasing Consumer Shift to Packaged Food: With a rapidly urbanizing population, the Saudi cereal market has seen a substantial shift towards packaged food products. In 2024, Saudi Arabias urban population reached approximately 34 million people, representing 83% of the total population, according to the General Authority for Statistics. This shift toward urban lifestyles has fueled demand for convenient and time-saving food products like packaged cereals. Increased participation of women in the workforce, now constituting 36% of the labor force, also contributes to a higher demand for convenient food options, including ready-to-eat cereals.

- Government Initiatives for Local Food Production: Saudi Arabia's Vision 2030 aims to reduce reliance on food imports, and the cereal market is a key focus. Under the National Transformation Program, the government is promoting domestic grain production to enhance food security. By 2024, the Saudi Agricultural Development Fund allocated SAR 4 billion in loans to support local farmers in growing wheat and barley. The country aims to locally source 60% of its cereal consumption by the end of this decade. This initiative, along with advanced agricultural technologies, is expected to boost domestic cereal production significantly.

Market Restraints

- Fluctuating Raw Material Prices (Wheat, Barley, and Oats): The cereal market in Saudi Arabia is highly sensitive to the global volatility of raw material prices, especially wheat, barley, and oats. According to data from the International Monetary Fund (IMF), global wheat prices spiked in 2022 due to supply chain disruptions and inflationary pressures. These fluctuations affect cereal manufacturers' costs, which ultimately get passed on to consumers. Additionally, Saudi Arabias dependency on imported grains exacerbates the situation, making the market vulnerable to international price swings and supply chain uncertainties.

- Consumer Price Sensitivity (Affordability vs Premium Cereals): Price sensitivity is a significant factor in the Saudi cereal market, where household incomes vary widely. Data from the General Authority for Statistics show that the average household income in Saudi Arabia is SAR 14,823 per month, with consumers in lower-income brackets prioritizing affordability over premium cereal products. While demand for premium, organic, and health-focused cereals is growing, the majority of the population still favors more affordable, mass-market cereal options. This dynamic creates a challenge for cereal brands that aim to balance premium product offerings with price-conscious consumer demands.

KSA Cereal Market Future Outlook

Over the next few years, the KSA cereal market is expected to witness significant growth, driven by continuous consumer interest in healthier and more convenient breakfast options. As urbanization accelerates, and consumer preferences evolve toward functional and organic foods, the demand for innovative cereal products will continue to rise. Moreover, increasing disposable incomes and growing online retail penetration are expected to enhance the distribution of cereal products across the country. Government efforts to boost domestic production in line with Vision 2030 will likely provide further impetus for growth in the local cereal market.

Market Opportunities

- Innovations in Functional and Fortified Cereals (Nutritional Value, Protein-Rich Cereals): Saudi Arabia's growing health-conscious population is driving demand for functional and fortified cereals that offer additional nutritional benefits. The Ministry of Health reports that 17 million Saudis are seeking diets high in protein and essential vitamins to combat rising lifestyle diseases. Cereals fortified with iron, calcium, and protein have seen an uptick in demand, providing a key opportunity for manufacturers to introduce new product lines. Innovation in cereals that target specific health needs, such as those designed for diabetic or hypertensive individuals, presents significant growth potential.

- Expansion of Organic Cereal Offerings (Demand for Clean Label Products): The demand for organic cereal products is expanding in Saudi Arabia, driven by consumer preferences for clean label products free from synthetic additives. According to the Saudi Organic Farming Association, the organic food sector has grown significantly, with over 52,000 hectares dedicated to organic farming by 2024. This provides cereal producers with an opportunity to introduce more organic varieties to the market, aligning with the growing consumer demand for transparency and healthy ingredients. Increased investment in local organic farming also supports the government's Vision 2030 objectives for food security and sustainability.

Scope of the Report

|

Product Type |

Ready-to-Eat Cereals |

|

Hot Cereals |

|

|

Snack Bars (Cereal-based) |

|

|

Muesli and Granola |

|

|

Distribution Channel |

Hypermarkets & Supermarkets |

|

Convenience Stores |

|

|

Online Retail |

|

|

Specialized Health Stores |

|

|

Others (Local vendors, traditional markets) |

|

|

Ingredient Type |

Whole Grains |

|

Refined Grains |

|

|

Organic Ingredients |

|

|

Gluten-Free Ingredients |

|

|

Consumer Demographics |

Kids |

|

Adults |

|

|

Elderly |

|

|

Sports Enthusiasts (Functional cereals) |

|

|

Region |

Riyadh |

|

Jeddah |

|

|

Dammam |

|

|

Al Khobar |

|

|

Other Cities |

Products

Key Target Audience

Supermarkets and Hypermarkets

Online Retailers

Convenience Stores

Specialized Health Stores

Government and Regulatory Bodies (Saudi Food and Drug Authority - SFDA)

Cereal Manufacturers

Investors and Venture Capital Firms

Agricultural Producers

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

Kelloggs

Nestl S.A.

Weetabix Ltd.

General Mills, Inc.

Almarai

Cereal Partners Worldwide

Natures Path Foods, Inc.

The Hain Celestial Group

PepsiCo, Inc. (Quaker)

Sanitarium Health Food Company

Hero Group

Clif Bar & Company

Post Holdings, Inc.

Bob's Red Mill

Organic Foods & Caf

Table of Contents

1. KSA Cereal Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. KSA Cereal Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. KSA Cereal Market Analysis

3.1 Growth Drivers

3.1.1 Rising Health Consciousness (Organic, whole grain trends)

3.1.2 Increasing Consumer Shift to Packaged Food (Convenience and lifestyle changes)

3.1.3 Government Initiatives for Local Food Production (Vision 2030, food security)

3.1.4 Expanding Retail Chains and Online Grocery Market (E-commerce integration, supermarkets growth)

3.2 Market Challenges

3.2.1 High Dependency on Imported Grains (Supply chain risks, tariff policies)

3.2.2 Fluctuating Raw Material Prices (Wheat, barley, and oats)

3.2.3 Consumer Price Sensitivity (Affordability vs premium cereals)

3.3 Opportunities

3.3.1 Innovations in Functional and Fortified Cereals (Nutritional value, protein-rich cereals)

3.3.2 Expansion of Organic Cereal Offerings (Demand for clean label products)

3.3.3 Increasing Popularity of Gluten-Free and Specialty Diet Cereals

3.4 Trends

3.4.1 Rise of Sustainable Packaging in Cereal Products

3.4.2 Focus on Clean Label and Non-GMO Ingredients

3.4.3 Growth in Ready-to-Eat Breakfast Cereals (Single-serve, grab-and-go products)

3.5 Government Regulations

3.5.1 Saudi Food and Drug Authority (SFDA) Guidelines for Food Quality

3.5.2 Import Tariffs and Subsidy Policies for Local Production

3.5.3 Nutritional Labeling Requirements and Standards

3.5.4 Support for Local Grain Production (Agricultural reforms under Vision 2030)

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (Local and global suppliers, retailers, distributors)

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape

4. KSA Cereal Market Segmentation

4.1 By Product Type (In Value %)

4.1.1 Ready-to-Eat Cereals

4.1.2 Hot Cereals

4.1.3 Snack Bars (Cereal-based)

4.1.4 Muesli and Granola

4.2 By Distribution Channel (In Value %)

4.2.1 Hypermarkets & Supermarkets

4.2.2 Convenience Stores

4.2.3 Online Retail

4.2.4 Specialized Health Stores

4.2.5 Others (Local vendors, traditional markets)

4.3 By Ingredient Type (In Value %)

4.3.1 Whole Grains

4.3.2 Refined Grains

4.3.3 Organic Ingredients

4.3.4 Gluten-Free Ingredients

4.4 By Consumer Demographics (In Value %)

4.4.1 Kids

4.4.2 Adults

4.4.3 Elderly

4.4.4 Sports Enthusiasts (Functional cereals)

4.5 By Region (In Value %)

4.5.1 Riyadh

4.5.2 Jeddah

4.5.3 Dammam

4.5.4 Al Khobar

4.5.5 Other Cities

5. KSA Cereal Market Competitive Analysis

5.1 Detailed Profiles of Major Competitors

5.1.1 Nestl S.A.

5.1.2 Kelloggs

5.1.3 Weetabix Ltd.

5.1.4 General Mills, Inc.

5.1.5 Almarai

5.1.6 Cereal Partners Worldwide

5.1.7 Natures Path Foods, Inc.

5.1.8 The Hain Celestial Group

5.1.9 PepsiCo, Inc. (Quaker)

5.1.10 Sanitarium Health Food Company

5.1.11 Hero Group

5.1.12 Clif Bar & Company

5.1.13 Post Holdings, Inc.

5.1.14 Bob's Red Mill

5.1.15 Organic Foods & Caf

5.2 Cross Comparison Parameters (Number of Employees, Revenue, Product Portfolio, Global vs Local Presence, Innovation Capabilities, Sustainability Practices, Supply Chain Strength, Consumer Satisfaction Ratings)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Private Equity Investments

6. KSA Cereal Market Regulatory Framework

6.1 SFDA Cereal Product Quality Standards

6.2 Import Policies and Tariff Framework

6.3 Food Labeling and Safety Compliance

6.4 Organic Certification and Regulatory Requirements

7. KSA Cereal Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. KSA Cereal Future Market Segmentation

8.1 By Product Type (In Value %)

8.2 By Distribution Channel (In Value %)

8.3 By Ingredient Type (In Value %)

8.4 By Consumer Demographics (In Value %)

8.5 By Region (In Value %)

9. KSA Cereal Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives and Consumer Targeting

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

In this initial phase, we mapped out the KSA cereal market ecosystem, identifying key stakeholders, including cereal manufacturers, retailers, and regulatory bodies. Secondary research was conducted using databases such as Euromonitor, Statista, and government publications to understand the market structure and dynamics. The goal was to define the core variables affecting the market, including consumer preferences, product innovations, and distribution trends.

Step 2: Market Analysis and Construction

We compiled historical data on cereal consumption, pricing trends, and market penetration rates in the KSA market. This involved evaluating data from local retailers and consumer surveys to assess the relative performance of different product types, including ready-to-eat cereals, hot cereals, and snack bars. Our analysis also covered distribution channels such as hypermarkets, supermarkets, and online retail platforms.

Step 3: Hypothesis Validation and Expert Consultation

Our research team engaged in consultations with industry experts from leading cereal manufacturers and retailers. These discussions provided valuable insights into operational challenges, consumer demand trends, and competitive strategies. The data gathered helped validate our initial findings and refine our market forecasts.

Step 4: Research Synthesis and Final Output

The final stage involved synthesizing data from both primary and secondary research sources. We conducted a thorough review of product segments, consumer behavior, and sales performance to develop a comprehensive and accurate forecast for the KSA cereal market. This ensured that our findings were well-grounded and reflected the market's current dynamics.

Frequently Asked Questions

1. How big is the KSA Cereal Market?

The KSA cereal market is valued at USD 0.63 billion, driven by rising consumer demand for nutritious and convenient breakfast options such as ready-to-eat cereals and snack bars.

2. What are the challenges in the KSA Cereal Market?

Key challenges include high dependency on imported raw materials like grains, fluctuating prices of ingredients such as oats and wheat, and the growing consumer price sensitivity, particularly for premium cereals.

3. Who are the major players in the KSA Cereal Market?

Key players include Kelloggs, Nestl, General Mills, Almarai, and Weetabix. These companies dominate due to their strong brand recognition, extensive distribution networks, and continuous product innovation.

4. What are the growth drivers of the KSA Cereal Market?

The market is primarily driven by rising health consciousness among consumers, the increasing preference for packaged and convenient food, and growing investments in local production under the governments Vision 2030 initiative.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.