KSA Coffee Market Outlook to 2030

Region:Saudi Arabia

Author(s):Yogita Sahu

Product Code:KROD10234

Region:Saudi Arabia

Author(s):Yogita Sahu

Product Code:KROD10234

December 2024

84

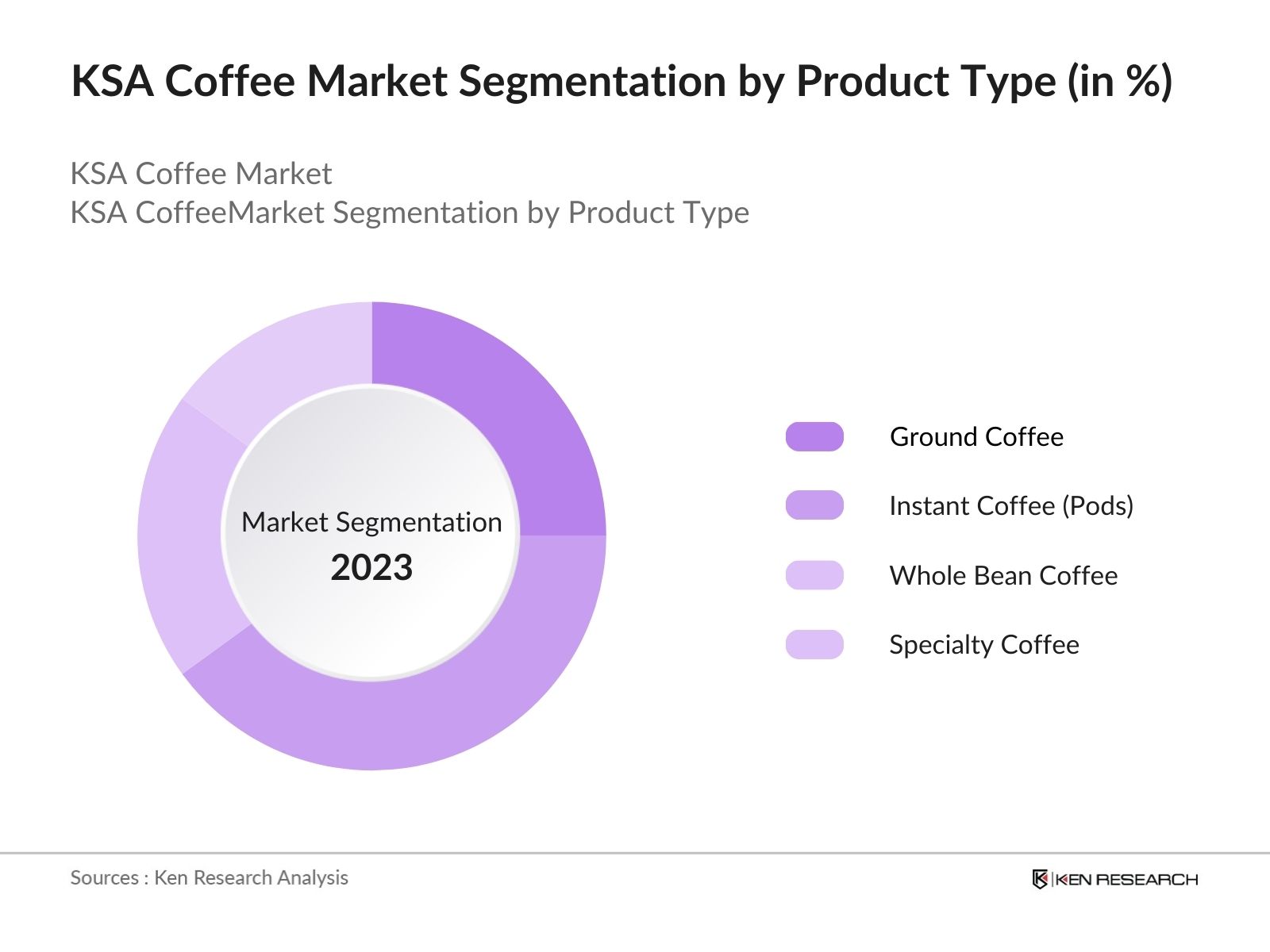

By Product Type: The market is segmented by product type into ground coffee, instant coffee (pods and capsules), whole bean coffee, and specialty coffee. Recently, instant coffee has dominated the product type segmentation, primarily due to the convenience it offers to busy consumers. With more individuals working longer hours, instant coffee provides a quick and easy way to enjoy coffee, leading to its growing popularity. Brands like Nestl and Keurig have strengthened their market positions by introducing high-quality pods and capsules that appeal to this demand.

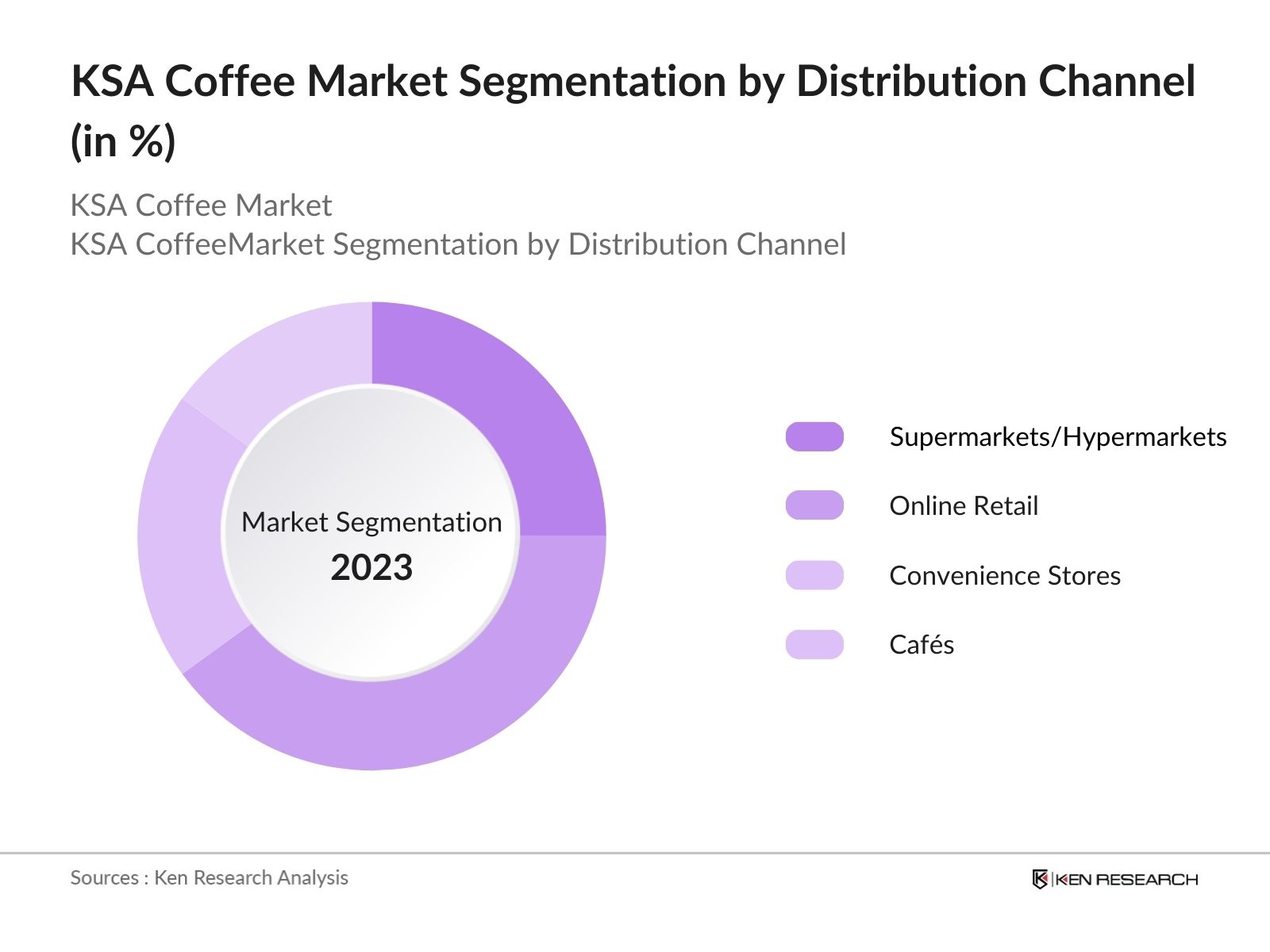

By Distribution Channel: The market is also segmented by distribution channels, including supermarkets and hypermarkets, online retail, convenience stores, and cafs. Supermarkets and hypermarkets lead in market share as they provide a one-stop shop for coffee products, from instant coffee to premium specialty beans. The widespread availability of various brands and the convenience of shopping for groceries alongside coffee make this channel the preferred choice for most consumers.

The market is dominated by both global and local players. Major global companies like Nestl, Starbucks, and Jacobs Douwe Egberts have established a presence in the country, while local companies like Baja and Brew92 have made inroads by focusing on the unique preferences of Saudi consumers.

|

Company Name |

Year of Establishment |

Headquarters |

Key Products |

Revenue (2023) |

No. of Employees |

Market Position |

R&D Investments |

Distribution Network |

Sustainability Initiatives |

|

Nestl S.A. |

1867 |

Vevey, Switzerland |

|||||||

|

Baja |

1997 |

Jeddah, KSA |

|||||||

|

Starbucks Corporation |

1971 |

Seattle, USA |

|||||||

|

Jacobs Douwe Egberts |

2015 |

Amsterdam, Netherlands |

|||||||

|

Brew92 |

2015 |

Riyadh, KSA |

Over the next five years, the KSA Coffee industry is expected to experience growth driven by factors such as the increasing demand for premium coffee products, the expansion of specialty coffee chains, and government initiatives to boost local coffee production under Vision 2030.

|

By Product Type |

Ground Coffee Instant Coffee (Pods, Capsules) Whole Bean Coffee Specialty Coffee Coffee Substitutes |

|

By Category |

Organic Coffee Conventional Coffee |

|

By Distribution Channel |

Supermarkets and Hypermarkets Convenience Stores Online Retail Cafs and Restaurants |

|

By End User |

Household Foodservice (Hotels, Restaurants), Commercial Offices |

|

By Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Expansion of Specialty Coffee Shops

3.1.2. Government Initiatives (Vision 2030, Saudi Coffee Year)

3.1.3. Rising Coffee Consumption Among Youth

3.1.4. Increasing Popularity of Single-Serve Brewing Systems

3.2. Market Challenges

3.2.1. Rising Agricultural Input Costs

3.2.2. Competition from Tea and Healthier Beverages

3.2.3. Limited Domestic Coffee Production

3.2.4. Supply Chain Disruptions

3.3. Opportunities

3.3.1. Growth of Certified and Organic Coffee Products

3.3.2. Expansion into Online and Direct-to-Consumer Channels

3.3.3. Caf Culture and Social Influences on Consumption

3.3.4. Collaboration with Local Farmers for Sustainable Production

3.4. Trends

3.4.1. Increasing Demand for Ethical and Sustainable Coffee

3.4.2. Product Innovation in Coffee Flavors and Formats

3.4.3. Integration of Coffee into Foodservice Sector

3.4.4. Emergence of Specialty Coffee Competitions

3.5. Government Regulation

3.5.1. Import and Export Tariffs on Coffee Products

3.5.2. Food and Beverage Safety Regulations

3.5.3. Taxation Policies on Coffee and Related Goods

3.5.4. Support for Local Coffee Production

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Ground Coffee

4.1.2. Instant Coffee (Pods, Capsules)

4.1.3. Whole Bean Coffee

4.1.4. Specialty Coffee

4.1.5. Coffee Substitutes

4.2. By Category (In Value %)

4.2.1. Organic Coffee

4.2.2. Conventional Coffee

4.3. By Distribution Channel (In Value %)

4.3.1. Supermarkets and Hypermarkets

4.3.2. Convenience Stores

4.3.3. Online Retail

4.3.4. Cafs and Restaurants

4.4. By End User (In Value %)

4.4.1. Household

4.4.2. Foodservice (Hotels, Restaurants)

4.4.3. Commercial Offices

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. West

4.5.4. North

5.1. Detailed Profiles of Major Companies

5.1.1. Baja Food Industries Co.

5.1.2. Nestl S.A.

5.1.3. Starbucks Corporation

5.1.4. Jacobs Douwe Egberts

5.1.5. Keurig Dr Pepper

5.1.6. Luigi Lavazza S.p.A.

5.1.7. Yousef Al Rajhi Group

5.1.8. Zino Davidoff Group

5.1.9. Food Empire Holdings Ltd.

5.1.10. ILLYCAFF S.p.A.

5.1.11. Kimbo S.p.A.

5.1.12. Brew92

5.1.13. Saudi Goody Products Marketing Company

5.1.14. Societe Est. Michel Najjar

5.1.15. Power Root (M) Sdn. Bhd.

5.2. Cross Comparison Parameters (Revenue, Market Share, Distribution Reach, Product Innovation)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital and Private Equity Investments

5.8. Government Grants

6.1. Coffee Quality Standards

6.2. Compliance and Certification Requirements

6.3. Import and Export Laws

6.4. Regulations on Coffee Product Labeling

KSA Coffee Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Growth

8.1. By Product Type (In Value %)

8.2. By Category (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe initial phase involves mapping all key stakeholders within the KSA Coffee Market. We leveraged both internal and external data sources to identify critical variables such as coffee production, consumption trends, and distribution channels.

This step focused on analyzing historical data of the KSA Coffee Market, specifically focusing on the demand for instant and specialty coffee. We also evaluated the impact of caf culture on consumption patterns, using data from retail chains and independent shops.

We validated our market hypotheses by conducting interviews with key players, including caf owners, coffee manufacturers, and industry experts. This feedback helped in refining market estimates and providing a realistic outlook for future growth.

In the final phase, we synthesized the research findings and combined them with industry insights. The report was finalized with data from both primary and secondary research, ensuring a comprehensive view of the KSA Coffee Market.

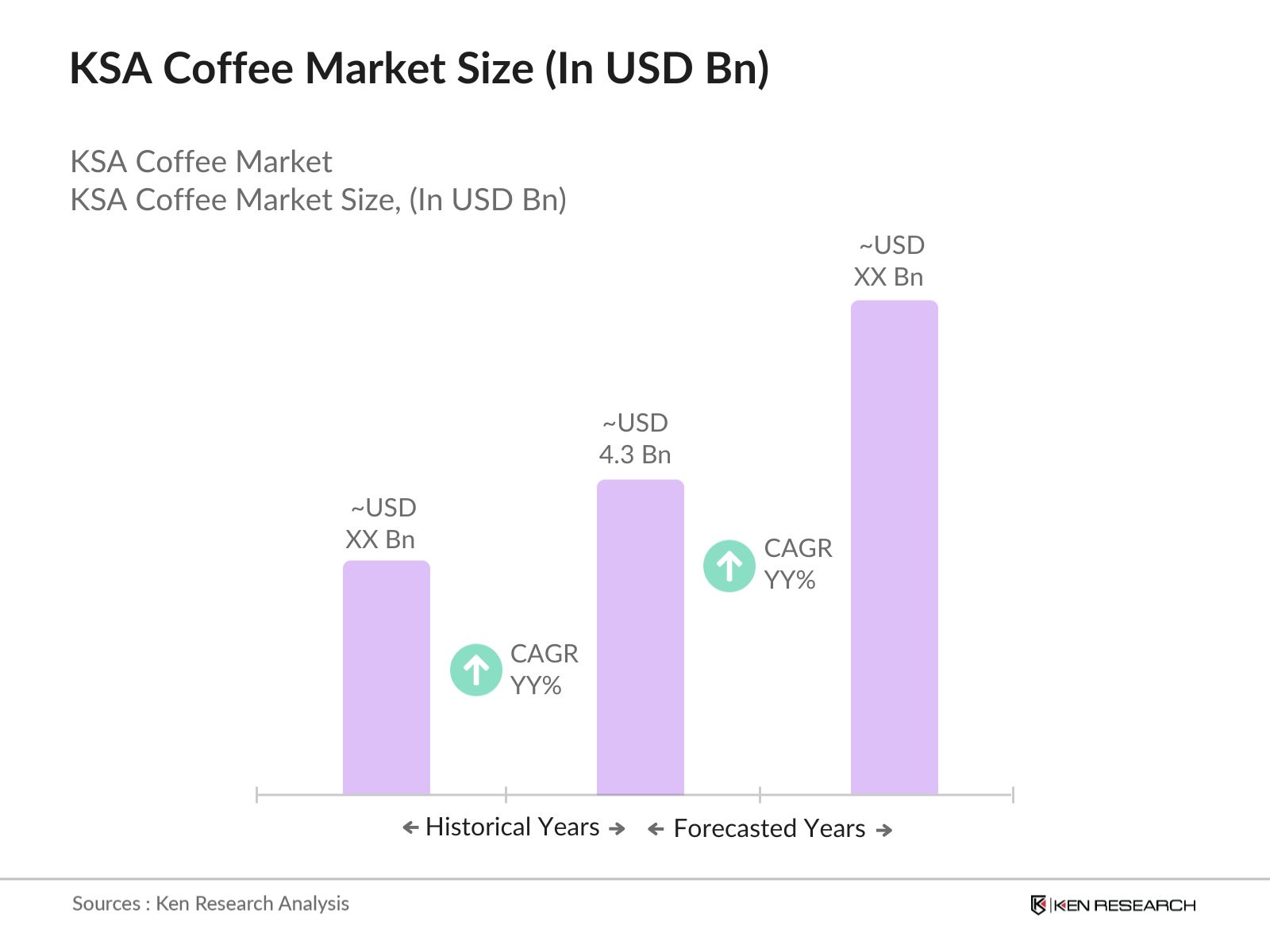

The KSA Coffee Market is valued at USD 4.3 billion, driven by the increasing demand for premium and specialty coffee products, as well as government initiatives to support local coffee production.

The KSA Coffee Market faces challenges such as rising agricultural input costs, competition from tea and other beverages, and logistical hurdles in expanding local production.

Key players in the KSA Coffee Market include Nestl, Starbucks, Baja, Jacobs Douwe Egberts, and Brew92, all of whom dominate due to their extensive distribution networks and focus on innovation.

The KSA Coffee Market is driven by the increasing popularity of specialty coffee, government initiatives to promote coffee consumption, and the rise of caf culture in urban areas like Riyadh and Jeddah.

Opportunities in the KSA Coffee Market include the rising demand for certified and sustainable coffee products, along with the potential for expanding distribution through online channels and supermarkets.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.