KSA Construction Market Outlook to 2030

Region:Saudi Arabia

Author(s):Shreya Garg

Product Code:KROD9334

Region:Saudi Arabia

Author(s):Shreya Garg

Product Code:KROD9334

December 2024

97

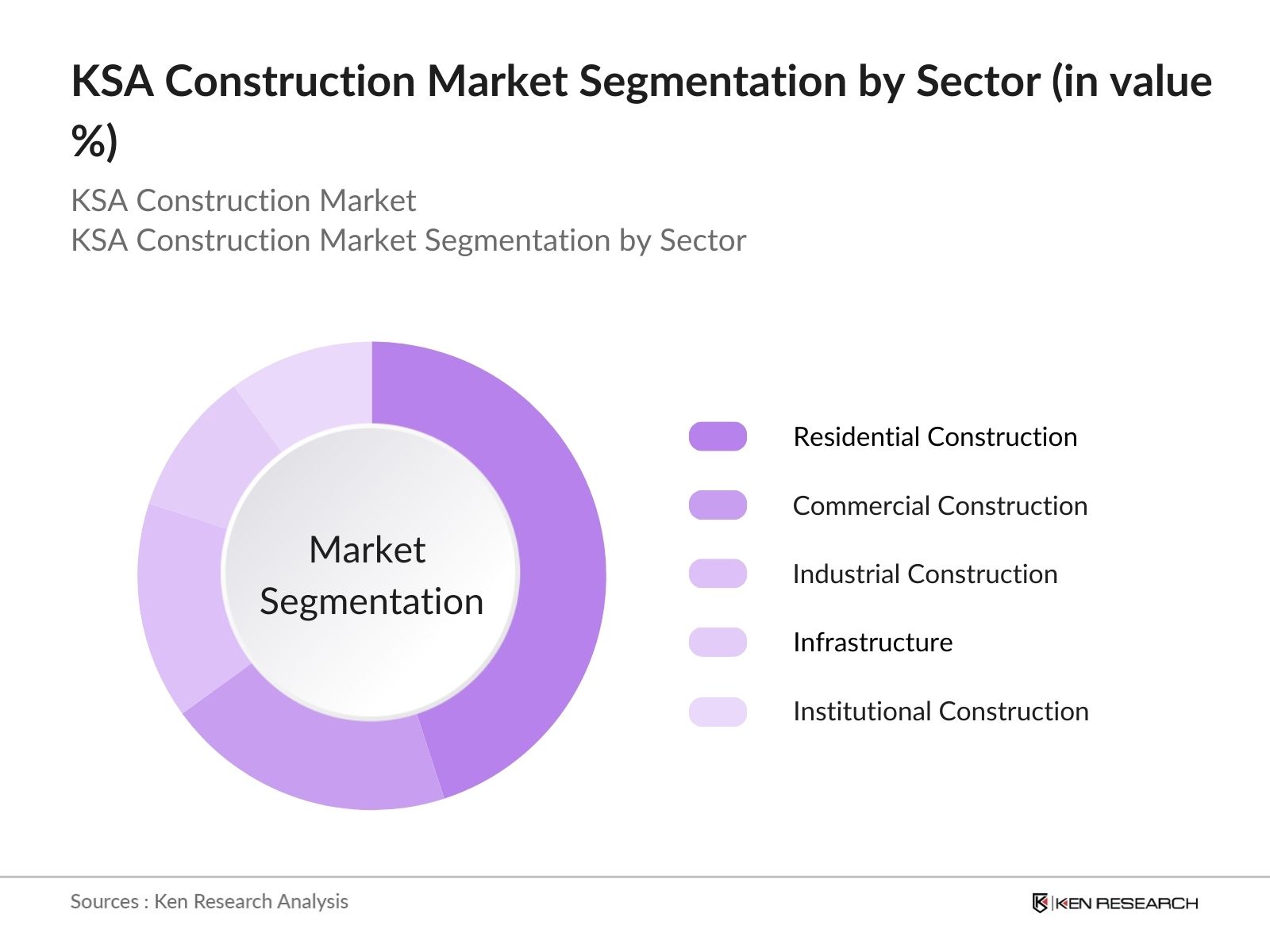

By Sector: The KSA construction market is segmented by sector into residential construction, commercial construction, industrial construction, infrastructure, and institutional construction. The residential construction sector holds the dominant market share due to the increasing demand for affordable housing projects and luxury developments driven by population growth and urbanization. Large-scale housing programs initiated by the government to cater to citizens under Vision 2030 further bolster this sector. Additionally, real estate developers are investing in high-end residential complexes and gated communities in cities like Riyadh and Jeddah to meet the demands of the expanding upper-middle-class population.

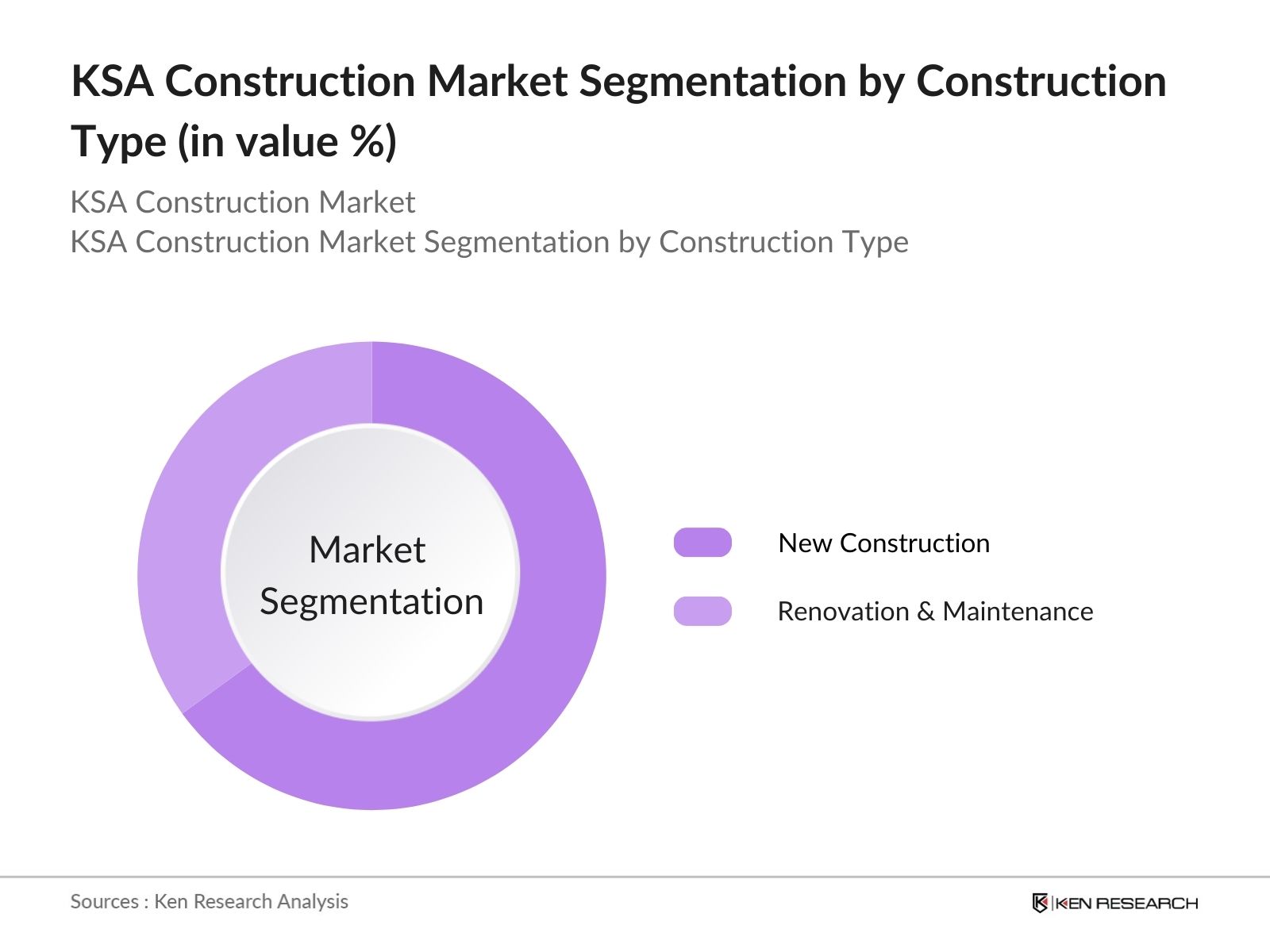

By Construction Type: The market is further segmented by construction type into new construction and renovation & maintenance. New construction dominates this segment due to the large-scale development of new cities, such as NEOM and The Red Sea Project, which require entirely new infrastructure and residential, commercial, and entertainment facilities. Moreover, the government's aggressive push to build smart cities and enhance public infrastructure is contributing to the predominance of new construction projects across the country.

The KSA construction market is dominated by a combination of large local companies and international players, each playing a significant role in the execution of major projects across the Kingdom. The local firms have a strong understanding of regulatory requirements and local construction practices, while international companies bring in advanced technology and expertise for large-scale projects such as NEOM and The Red Sea Project. This balance has fostered healthy competition and collaboration in the sector.

|

Company Name |

Establishment Year |

Headquarters |

No. of Projects |

Revenue (USD) |

Key Sector Focus |

Technology Use |

Major Clients |

Sustainability Certifications |

Contract Type |

|

Saudi Binladin Group |

1931 |

Jeddah, Saudi Arabia |

|||||||

|

El Seif Engineering Contracting |

1975 |

Riyadh, Saudi Arabia |

|||||||

|

Nesma & Partners Contracting |

1981 |

Al Khobar, Saudi Arabia |

|||||||

|

Hyundai Engineering & Construction |

1947 |

Seoul, South Korea |

|||||||

|

Al-Muhaidib Contracting |

1975 |

Riyadh, Saudi Arabia |

The KSA construction market is projected to experience significant growth, driven by the government's strategic focus on infrastructure and urban development. Large-scale initiatives like Vision 2030 and Saudi Green Initiative are expected to propel the construction industry into new domains, including sustainable and eco-friendly construction practices. The integration of technology in construction, such as Building Information Modeling (BIM) and modular construction, will further boost operational efficiency and project timelines. Additionally, ongoing foreign investment and the creation of new business hubs will likely drive increased demand for both residential and commercial construction.

|

By Sector |

Residential Commercial Industrial Infrastructure Institutional |

|

By Construction Type |

New Construction Renovation Maintenance |

|

By Building Material |

Concrete Steel Glass Plastic Others |

|

By Region |

Central West East South |

|

By Project Type |

Mega Projects Mid-sized Projects Small-scale Projects |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate (GDP growth contribution, public vs. private sector construction)

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones (Mega projects, government initiatives like Vision 2030)

3.1 Growth Drivers

3.1.1 Urbanization and Population Growth

3.1.2 Investment in Infrastructure (transportation, utilities)

3.1.3 Government Vision 2030 initiatives

3.1.4 Foreign Direct Investment (FDI) in Construction Projects

3.2 Market Challenges

3.2.1 Shortage of Skilled Labor (nationalization initiatives, reliance on expats)

3.2.2 Rising Material Costs (cement, steel, construction inputs)

3.2.3 Complex Regulatory Requirements

3.2.4 Environmental Compliance and Sustainability (green building standards, energy efficiency)

3.3 Opportunities

3.3.1 Expansion of Housing Projects (affordable housing, luxury residential projects)

3.3.2 Growth of Smart City Initiatives (Neom, The Red Sea Project)

3.3.3 Increased Demand for Healthcare and Education Facilities

3.3.4 New Partnerships with Global Contractors

3.4 Trends

3.4.1 Integration of Smart Technologies (BIM, IoT in construction)

3.4.2 Modular and Prefabricated Construction

3.4.3 Rise of Public-Private Partnerships (PPPs)

3.4.4 Sustainable Construction Practices

3.5 Government Regulation

3.5.1 Vision 2030 Strategy

3.5.2 Building Code Standards

3.5.3 Local Content Regulations (In-Kingdom Total Value Add - IKTVA)

3.5.4 Environmental Regulations

3.6 SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7 Stakeholder Ecosystem

3.7.1 Key Contractors

3.7.2 Key Suppliers and Material Providers

3.7.3 Government Agencies and Regulatory Bodies

3.8 Porters Five Forces

3.9 Competition Ecosystem

4.1 By Sector (in Value %)

4.1.1 Residential Construction

4.1.2 Commercial Construction

4.1.3 Industrial Construction

4.1.4 Infrastructure (roads, bridges, ports, airports)

4.1.5 Institutional Construction (education, healthcare, government buildings)

4.2 By Construction Type (in Value %)

4.2.1 New Construction

4.2.2 Renovation and Maintenance

4.3 By Building Material (in Value %)

4.3.1 Concrete

4.3.2 Steel

4.3.3 Glass

4.3.4 Plastic and Composites

4.3.5 Others

4.4 By Region (in Value %)

4.4.1 Central (Riyadh, Qassim)

4.4.2 West (Jeddah, Makkah, Madinah)

4.4.3 East (Dammam, Al-Khobar)

4.4.4 South (Asir, Jazan)

4.5 By Project Type (in Value %)

4.5.1 Mega Projects (Neom, Red Sea, Qiddiya)

4.5.2 Mid-sized Projects

4.5.3 Small-scale Projects

5.1 Detailed Profiles of Major Companies

5.1.1 Saudi Binladin Group

5.1.2 Saudi Oger Ltd.

5.1.3 El Seif Engineering Contracting Co.

5.1.4 Al-Muhaidib Contracting Company

5.1.5 Nesma & Partners Contracting Co. Ltd.

5.1.6 Almabani General Contractors

5.1.7 Al Rashid Trading & Contracting Company (RTCC)

5.1.8 Abdullah A. M. Al-Khodari Sons Company

5.1.9 Shibh Al Jazira Contracting Co. Ltd.

5.1.10 CCE Saudi Construction Engineering

5.1.11 Redco Construction - Almana

5.1.12 Hyundai Engineering & Construction Co.

5.1.13 Al Harbi Trading & Contracting Co. Ltd.

5.1.14 Al-Fouzan Trading & General Construction Co.

5.1.15 Al Ayuni Investment and Contracting Company

5.2 Cross Comparison Parameters (Number of Projects, Headquarters, Revenue, Local Workforce Percentage, Major Contracts, Use of Smart Technology, Green Certifications, Key Clients)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Public-Private Partnership Projects

5.8 Government Tenders and Contracts

6.1 Building and Construction Codes

6.2 Zoning and Land-use Regulations

6.3 Local Content Requirements (IKTVA)

6.4 Certification Processes for Green Building Standards

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth (Urbanization, Infrastructure, and Mega Projects)

8.1 By Sector (Residential, Commercial, Industrial, Infrastructure, Institutional)

8.2 By Construction Type (New Construction, Renovation and Maintenance)

8.3 By Region (Central, Western, Eastern, Southern)

8.4 By Material (Concrete, Steel, Glass, Others)

8.5 By Project Type (Mega, Mid-sized, Small-scale)

9.1 Customer Segmentation Analysis

9.2 Strategic Market Positioning

9.3 Expansion Opportunities in Underserved Regions

9.4 Key Partnership and Joint Venture Recommendations

Disclaimer Contact UsThis phase involved extensive desk research and data collection from government reports, proprietary databases, and industry publications. The objective was to define key variables influencing the KSA construction market, such as economic indicators, regulatory frameworks, and construction material pricing.

Data from various historical sources was aggregated to construct a comprehensive analysis of the KSA construction market. Key trends, market penetration, and revenue distribution were evaluated to ensure the reliability and accuracy of the data used in the report.

Consultations with industry experts, including contractors, government officials, and real estate developers, were conducted to validate market hypotheses. These consultations provided critical insights into market dynamics and operational challenges.

The final step involved synthesizing all collected data and expert feedback into a cohesive report. Cross-referencing the data with the bottom-up approach ensured an accurate representation of the market.

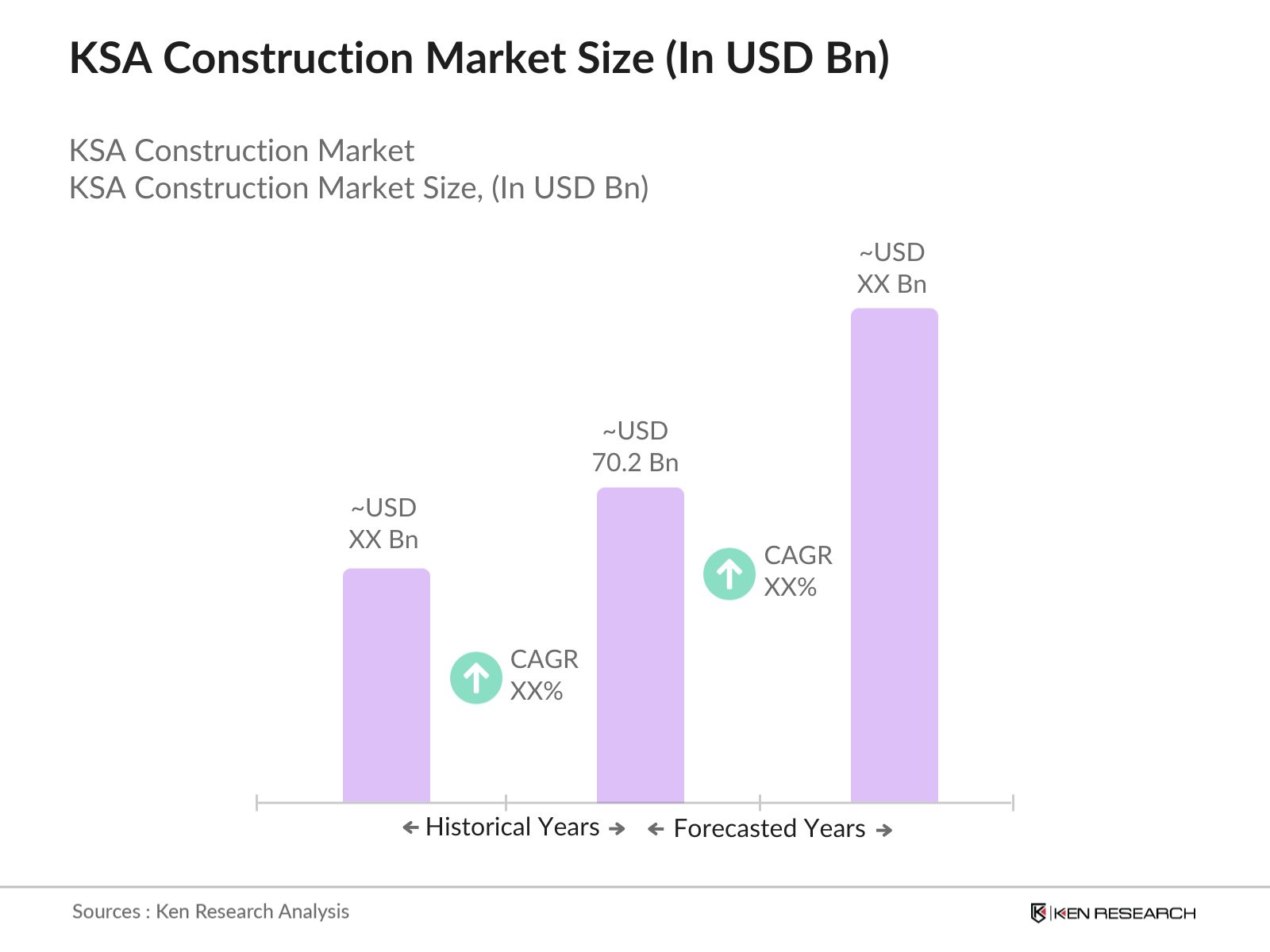

The KSA construction market is valued at USD 70.2 billion, driven by large-scale government investments in infrastructure and megaprojects like NEOM.

Challenges in the KSA construction market include high construction material costs, regulatory hurdles, and the shortage of skilled labor due to dependence on foreign workers.

Key players in the KSA construction market include Saudi Binladin Group, El Seif Engineering Contracting Co., Nesma & Partners Contracting, and Hyundai Engineering & Construction.

Growth in the KSA construction market is driven by Vision 2030, urbanization, increased demand for housing, and the development of mega infrastructure projects such as airports, roads, and industrial zones.

Residential and infrastructure sectors dominate the KSA construction market due to government programs focused on housing and large-scale city development projects.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.