KSA Contact Lenses Market Outlook to 2030

Region:Middle East

Author(s):Sanjana

Product Code:KROD3766

October 2024

81

About the Report

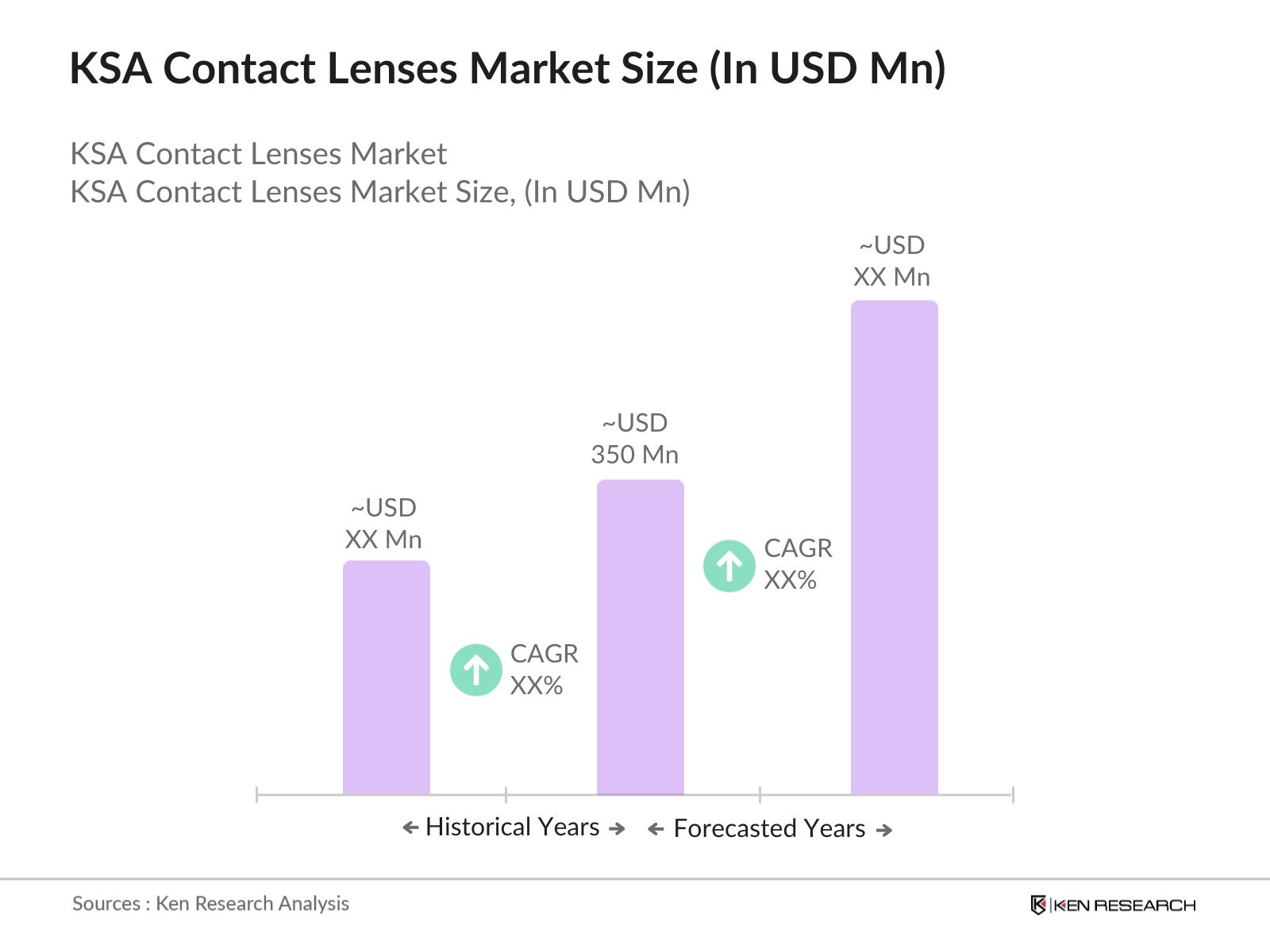

KSA Contact Lenses Market Overview

- The KSA Contact Lenses Market is valued at USD 350 million, with consistent growth driven by a combination of rising eye health issues and an increased demand for aesthetic lenses among the younger population. Factors such as advancements in contact lens technology, the adoption of silicone hydrogel lenses, and growing awareness about eye care are also propelling the market. These trends are supported by healthcare infrastructure improvements and increasing disposable incomes, leading to higher lens adoption rates.

- Major cities like Riyadh and Jeddah dominate the KSA Contact Lenses market, largely due to their higher population densities, access to advanced healthcare services, and affluent demographics. Riyadh, being the capital and the largest city, serves as a key hub for medical professionals, and optical stores contribute to significant lens sales. Jeddahs strong tourism industry also influences the demand for premium and daily disposable lenses, particularly among international visitors seeking convenience and high-quality eye care.

- Saudi Arabia imposes import tariffs on optical products, including contact lenses. In 2024, the import tariff on contact lenses was set at 5%, impacting both pricing and market competition. Despite these tariffs, the demand for imported lenses remains high, with the Kingdom importing over 15 million pairs of contact lenses in 2023. The tariffs aim to encourage local manufacturing, with the government offering incentives for companies to set up production facilities within the country.

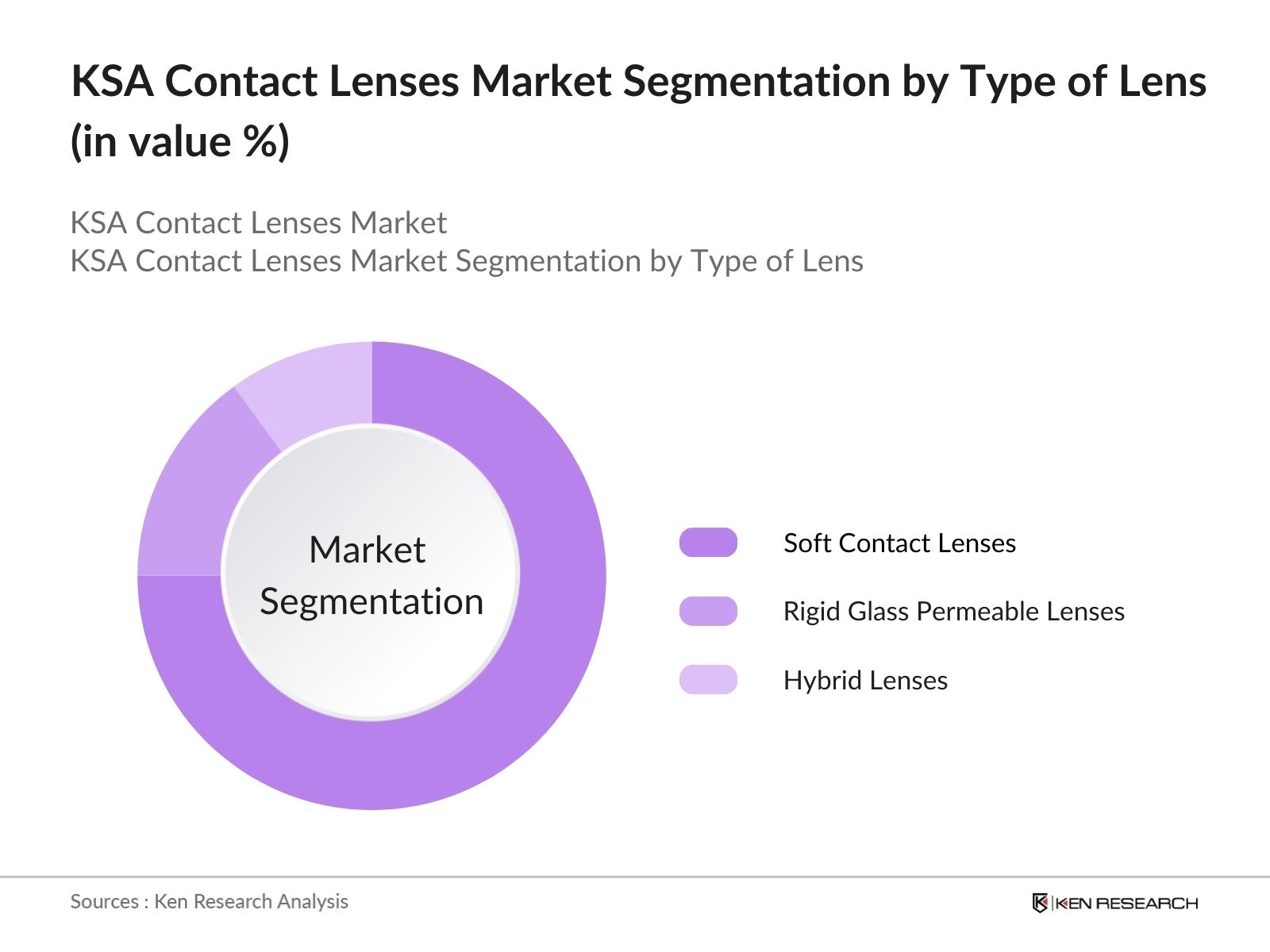

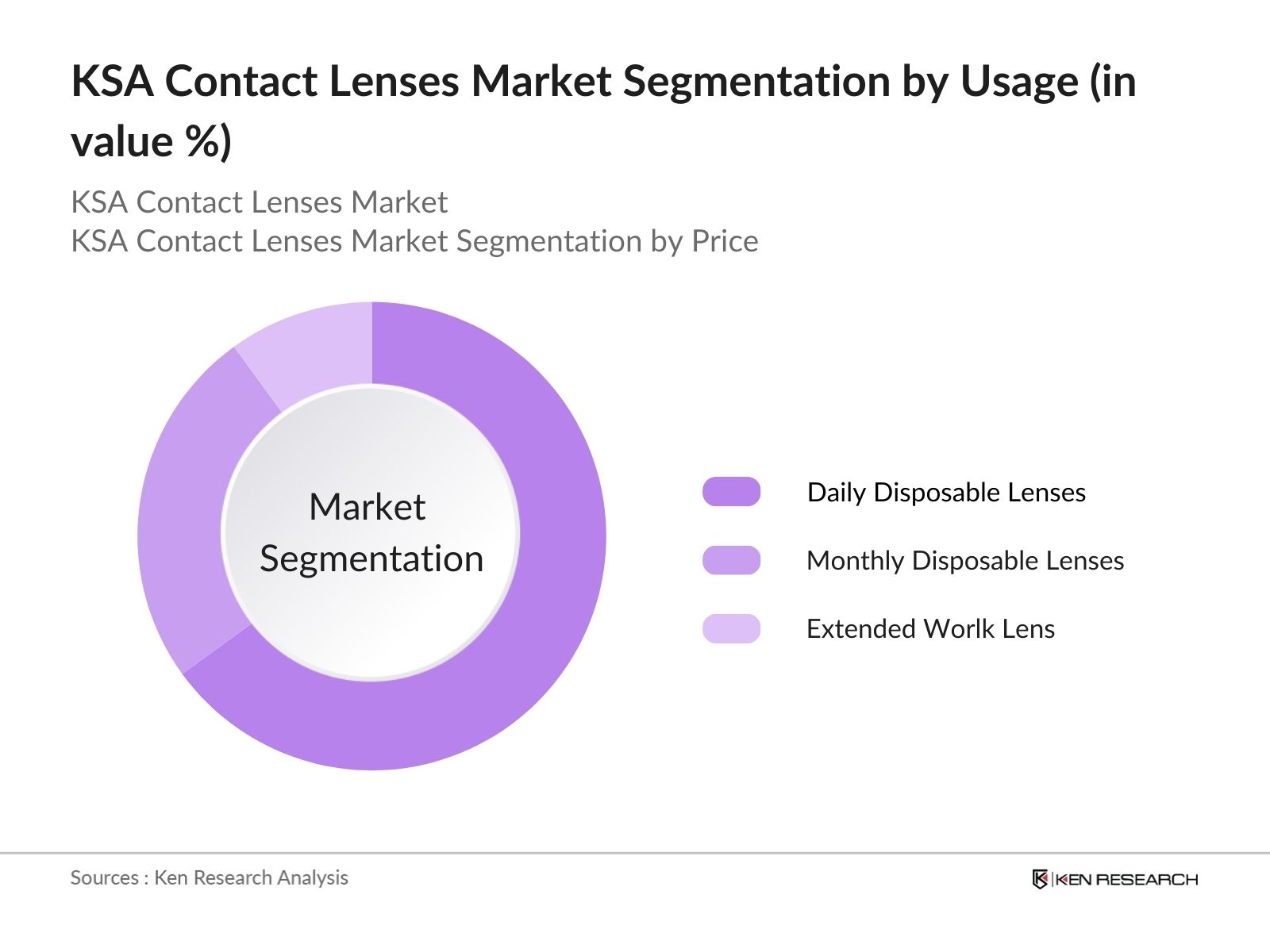

KSA Contact Lenses Market Segmentation

By Type of Lens: The KSA Contact Lenses market is segmented by lens type into soft contact lenses, rigid gas permeable (RGP) lenses, and hybrid lenses. Soft contact lenses dominate this segment due to their comfort, affordability, and wide usage for both corrective and cosmetic purposes. These lenses are particularly popular among the youth, who prefer daily disposable options for their convenience and reduced risk of infection. Major companies like Johnson & Johnson and CooperVision offer extensive product lines of soft lenses, further driving their dominance in the market.

By Usage: The market is also segmented by usage into daily disposable lenses, monthly disposable lenses, and extended wear lenses. Daily disposable lenses hold the largest market share due to their convenience, reduced cleaning requirement, and suitability for individuals with sensitive eyes. These lenses have seen increased adoption in urban centers where busy lifestyles demand quick and easy-to-use solutions. The rise in awareness about hygiene and infection risks has also contributed to the dominance of daily disposables.

KSA Contact Lenses Market Competitive Landscape

The KSA Contact Lenses market is highly competitive, with major players dominating due to their extensive product portfolios, strong distribution networks, and innovations in lens technology. Companies such as Johnson & Johnson and Alcon (Novartis) lead the market with their advanced silicone hydrogel lenses, while local brands focus on affordable alternatives for lower-income consumers. International players dominate due to their brand recognition and consistent product innovation.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD Mn) |

Product Range |

Global Presence |

R&D Investment |

Sustainability Initiatives |

Key Markets |

|---|---|---|---|---|---|---|---|---|

|

Johnson & Johnson |

1886 |

USA |

90 |

Extensive |

High |

Significant |

Yes |

Global |

|

Alcon (Novartis) |

1945 |

Switzerland |

60 |

Wide |

High |

Significant |

Yes |

Global |

|

Bausch + Lomb |

1853 |

USA |

55 |

Broad |

High |

Moderate |

Yes |

Global |

|

CooperVision |

1958 |

USA |

50 |

Comprehensive |

High |

Moderate |

Yes |

Global |

|

Hoya Vision Care |

1941 |

Japan |

45 |

Specialized |

Medium |

Moderate |

Yes |

Asia, Global |

KSA Contact Lenses Market Analysis

Growth Drivers

- Rising Eye Disorders: In Saudi Arabia, the rising incidence of eye disorders, such as myopia and hyperopia, is driving demand for contact lenses. A study conducted in Riyadh found that myopia affected approximately 48.7% of adults, while hyperopia was present in about 25.2% of participants. This increase in eye disorders directly correlates with the growing demand for corrective lenses, including contact lenses.

- Increasing Preference for Aesthetic Lenses: The growing preference for aesthetic lenses among young consumers in Saudi Arabia is contributing to market growth. The rise in social media usage and beauty trends has significantly influenced this market segment. With 35 million social media users in Saudi Arabia, the visibility of aesthetic lenses has led to a spike in demand. This trend is expected to continue, further driven by celebrity endorsements and beauty influencers.

- Availability of Affordable Options: The increased availability of affordable contact lens options has broadened the customer base. In 2023, Saudi Arabia experienced a notable increase in disposable income levels, supported by a decrease in unemployment and growth in the non-oil private sector. The per capita disposable income was reported to be $27,680. This has contributed to the affordability and purchase of these products. The affordability, combined with healthcare subsidies covering eye exams and prescriptions, has allowed more consumers to opt for contact lenses over traditional glasses.

Challenges

- High Manufacturing Costs: Manufacturing contact lenses involves complex processes and advanced materials, leading to high production costs. Additionally, the cost of raw materials, such as silicone and hydrogels, increased by due to global supply chain disruptions, further driving up the manufacturing expenses. These high production costs pose a significant barrier to new entrants in the Saudi market and impact the final pricing for consumers.

- Limited Penetration in Rural Areas: The contact lens market in Saudi Arabia remains largely urban-focused, with limited penetration in rural areas. According to the General Authority for Statistics, 75% of contact lens sales in 2023 occurred in Riyadh, Jeddah, and Dammam. The rural population, comprising faces limited access to optical stores and healthcare services. While urban areas are well-served by large retail chains, the lack of distribution networks and retail presence in smaller towns and rural areas hinders market expansion.

KSA Contact Lenses Market Future Outlook

The KSA Contact Lenses market is expected to experience significant growth over the coming years, driven by the increasing prevalence of eye disorders, rising awareness regarding eye care, and continued advancements in contact lens technology. The introduction of smart lenses and lenses with enhanced oxygen permeability are key trends that will shape the markets future. Additionally, the expansion of e-commerce platforms in the KSA will further boost sales, as more consumers turn to online channels for convenience and broader product availability.

Market Opportunities

- Advancements in Smart Contact Lenses: The development of smart contact lenses presents significant growth opportunities. In 2023, Saudi Arabia's King Abdullah University of Science and Technology (KAUST) announced breakthroughs in smart lens technology capable of measuring glucose levels in diabetic patients. With over 4 million diabetic individuals in the Kingdom, such innovations could cater to a large portion of the population. Furthermore, global collaborations with tech companies have led to research investments of over SAR 1 billion in smart lens development, positioning Saudi Arabia as a hub for advanced contact lens technology.

- Rising Medical Tourism: Saudi Arabia's Vision 2030 initiative has propelled medical tourism, especially in eye care, offering another avenue for contact lens market expansion. In 2023, over 200,000 medical tourists visited the Kingdom, many seeking specialized treatments, including refractive surgeries and custom contact lenses. The countrys growing reputation as a medical hub, coupled with advanced healthcare facilities, is expected to attract more international patients, boosting the demand for high-quality contact lenses.

Scope of the Report

|

Segments |

Sub-segments |

|

Type of Lens |

Soft Contact Lenses |

|

Rigid Gas Permeable (RGP) Lenses |

|

|

Hybrid Lenses |

|

|

Material |

Silicone Hydrogel |

|

Polymethyl Methacrylate (PMMA) |

|

|

Hydrogel |

|

|

Usage |

Daily Disposable Lenses |

|

Monthly Disposable Lenses |

|

|

Extended Wear Lenses |

|

|

Distribution Channel |

Optical Stores |

|

Online Retail |

|

|

Hospitals and Clinics |

|

|

Region |

Riyadh |

|

Jeddah |

|

|

Dammam |

|

|

Mecca |

|

|

Medina |

Products

Key Target Audience

Contact Lens Manufacturers

Lens Care Product Manufacturers

Eyewear Manufacturers

Pharmaceutical Companies

Health and Wellness Companies

Government and Regulatory Bodies (Saudi FDA)

Investment and Venture Capitalist Firms

Companies

Major Players Mentioned in the Report

Johnson & Johnson

Alcon (Novartis)

Bausch + Lomb

CooperVision

Hoya Vision Care

Menicon Co. Ltd.

Seed Co. Ltd.

St. Shine Optical Co.

BenQ Materials Corp.

Clearlab International

Neo Vision Co.

Pegavision Corporation

Blanchard Contact Lenses

Camax Optical Corp.

Hanita Lenses R.C.

Table of Contents

1. KSA Contact Lenses Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. KSA Contact Lenses Market Size (In USD Mn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. KSA Contact Lenses Market Analysis

3.1 Growth Drivers (Consumer Demand, Healthcare Access, Innovation in Lens Materials, etc.)

3.1.1 Rising Eye Disorders

3.1.2 Increasing Preference for Aesthetic Lenses

3.1.3 Availability of Affordable Options

3.2 Market Challenges (Manufacturing Complexity, Regulatory Barriers, etc.)

3.2.1 High Manufacturing Costs

3.2.2 Compliance with Health Regulations

3.2.3 Limited Penetration in Rural Areas

3.3 Opportunities (Technological Advancements, Increased Disposable Income, etc.)

3.3.1 Advancements in Smart Contact Lenses

3.3.2 Rising Medical Tourism

3.3.3 Expansion of Online Sales Channels

3.4 Trends (Customization, Online Sales, Eco-friendly Materials, etc.)

3.4.1 Personalized Contact Lenses

3.4.2 E-commerce Penetration in Optical Products

3.4.3 Sustainability in Lens Manufacturing

3.5 Government Regulations (Health Compliance, Import Tariffs, etc.)

3.5.1 Saudi FDA Guidelines for Contact Lenses

3.5.2 Import Tariffs on Optical Products

3.5.3 Health and Safety Standards for Contact Lenses

3.6 SWOT Analysis

3.7 Stake Ecosystem

3.8 Porters Five Forces

3.9 Competition Ecosystem

4. KSA Contact Lenses Market Segmentation

4.1 By Type of Lens (In Value %)

4.1.1 Soft Contact Lenses

4.1.2 Rigid Gas Permeable (RGP) Lenses

4.1.3 Hybrid Lenses

4.2 By Material (In Value %)

4.2.1 Silicone Hydrogel

4.2.2 Polymethyl Methacrylate (PMMA)

4.2.3 Hydrogel

4.3 By Usage (In Value %)

4.3.1 Daily Disposable Lenses

4.3.2 Monthly Disposable Lenses

4.3.3 Extended Wear Lenses

4.4 By Distribution Channel (In Value %)

4.4.1 Optical Stores

4.4.2 Online Retail

4.4.3 Hospitals and Clinics

4.5 By Region (In Value %)

4.5.1 Riyadh

4.5.2 Jeddah

4.5.3 Dammam

4.5.4 Mecca

4.5.5 Medina

5. KSA Contact Lenses Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Johnson & Johnson

5.1.2 Alcon (Novartis)

5.1.3 Bausch + Lomb

5.1.4 CooperVision

5.1.5 Carl Zeiss Meditec

5.1.6 Menicon

5.1.7 Hoya Vision Care

5.1.8 Seed Co. Ltd.

5.1.9 St. Shine Optical Co.

5.1.10 BenQ Materials Corp.

5.1.11 Neo Vision Co.

5.1.12 Clearlab International

5.1.13 Pegavision Corporation

5.1.14 Blanchard Contact Lenses

5.1.15 Camax Optical Corp.

5.2 Cross Comparison Parameters (Revenue, Market Share, Innovation, Global Presence, Manufacturing Capacity, Product Range, Sustainability Initiatives, Customer Base)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government Grants and Incentives

5.8 Private Equity Investments

6. KSA Contact Lenses Market Regulatory Framework

6.1 Saudi FDA Health Regulations

6.2 Compliance Requirements for Importers and Manufacturers

6.3 Certification Processes for Medical Contact Lenses

7. KSA Contact Lenses Future Market Size (In USD Mn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. KSA Contact Lenses Future Market Segmentation

8.1 By Type of Lens (In Value %)

8.2 By Material (In Value %)

8.3 By Usage (In Value %)

8.4 By Distribution Channel (In Value %)

8.5 By Region (In Value %)

9. KSA Contact Lenses Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Behavior Analysis

9.3 Marketing and Sales Strategies

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

This phase involved mapping the entire KSA Contact Lenses market ecosystem, which includes all key stakeholders such as manufacturers, distributors, and consumers. Secondary research using reliable databases was utilized to gather detailed industry-level information, ensuring all key variables, such as product types and consumer behaviors, were identified.

Step 2: Market Analysis and Construction

Historical data for the KSA Contact Lenses market was gathered and analyzed to evaluate market trends and consumer preferences. This phase also included an assessment of lens usage across various demographics, offering insights into the leading sub-segments. A comprehensive analysis of product availability and sales channels further enriched the understanding of market dynamics.

Step 3: Hypothesis Validation and Expert Consultation

The market hypotheses developed were validated through consultations with industry experts. These experts provided insights into operational aspects, including manufacturing challenges and regulatory hurdles, ensuring that the data collected was accurate and reflective of market conditions.

Step 4: Research Synthesis and Final Output

Direct interactions with major manufacturers provided critical data on sales trends, consumer preferences, and the effectiveness of various product segments. This final phase ensured that the insights presented were validated, offering a comprehensive view of the KSA Contact Lenses market.

Frequently Asked Questions

01. How big is the KSA Contact Lenses Market?

The KSA Contact Lenses market is valued at USD 350 million, with key growth drivers being increasing eye disorders and a rising preference for daily disposable lenses among consumers.

02. What are the challenges in the KSA Contact Lenses Market?

Challenges in the market include high manufacturing costs, regulatory compliance for imported lenses, and the limited penetration of advanced lens types in rural areas.

03. Who are the major players in the KSA Contact Lenses Market?

Key players include Johnson & Johnson, Alcon (Novartis), Bausch + Lomb, CooperVision, and Hoya Vision Care. These companies dominate due to their strong distribution networks and advanced product offerings.

04. What are the growth drivers of the KSA Contact Lenses Market?

The market is driven by rising demand for aesthetic lenses, increased awareness about eye care, and advancements in lens technology, particularly silicone hydrogel lenses.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.