KSA Diabetes Drugs Market Outlook to 2030

Region:Middle East

Author(s):Abhinav kumar

Product Code:KROD7563

December 2024

100

About the Report

KSA Diabetes Drugs Market Overview

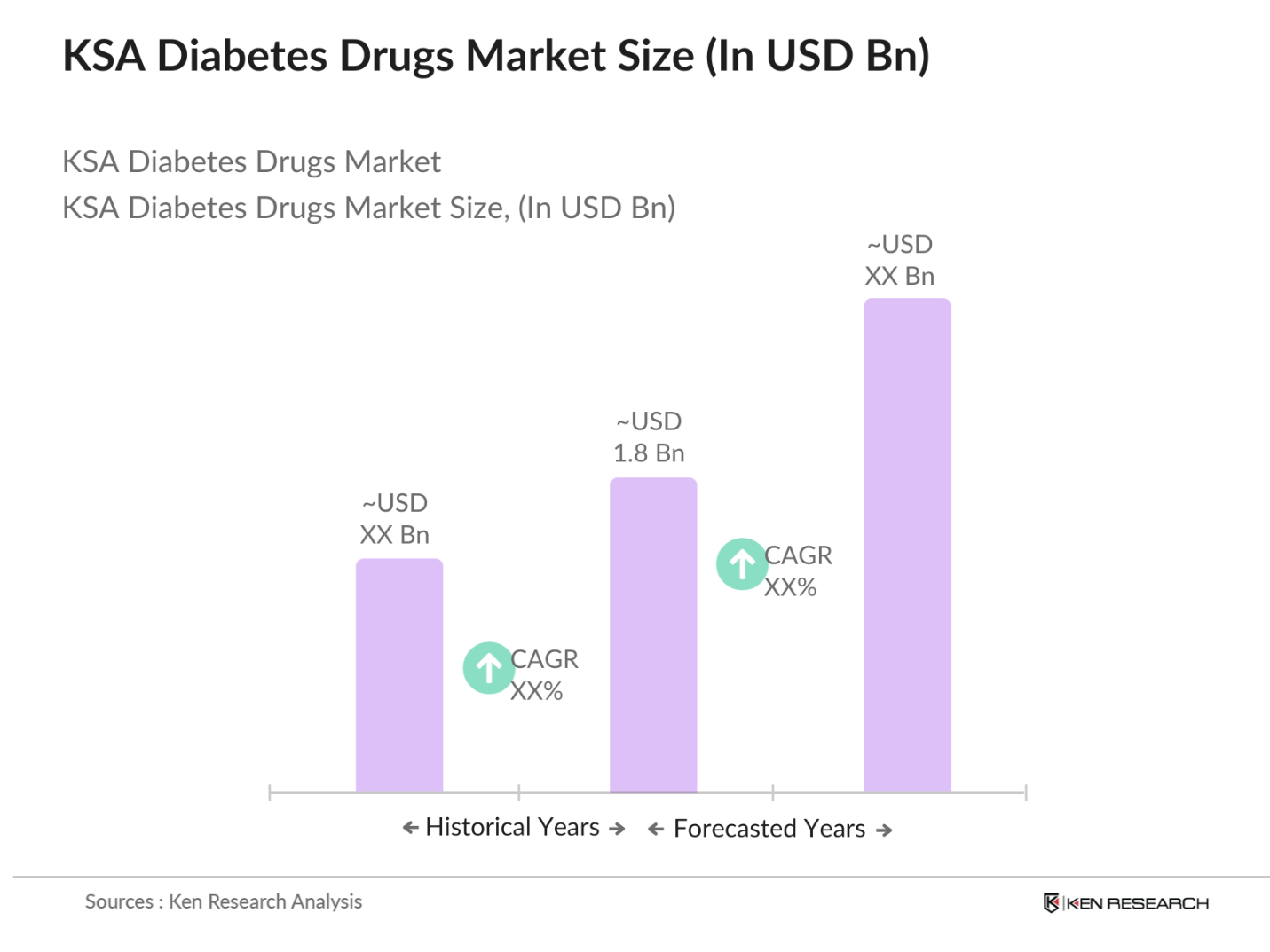

- The KSA diabetes drugs market is valued at USD 1.8 billion, based on a five-year historical analysis. The market's growth is driven by the increasing prevalence of diabetes, especially Type 2 diabetes, which is linked to lifestyle factors such as obesity and sedentary habits. Additionally, the government's health initiatives, including Saudi Vision 2030, focus on improving healthcare access and providing subsidized medications, further boosting market demand. Rising awareness about early diagnosis and continuous treatment for diabetes is pushing the demand for advanced drugs such as insulin analogs and oral antidiabetic drugs.

- The market is dominated by urban centers like Riyadh, Jeddah, and Dammam due to their advanced healthcare infrastructure and larger diabetic patient population. These cities have a higher concentration of hospitals, clinics, and specialized diabetes treatment centers, making them key drivers in the market. Furthermore, the population in these areas has a higher prevalence of sedentary lifestyles, further increasing the diabetes incidence rate and leading to higher demand for diabetes medications.

- The Saudi Food and Drug Authority (SFDA) plays a crucial role in regulating diabetes drugs in the Kingdom. In 2024, SFDA updated its guidelines to fast-track the approval process for innovative diabetes treatments, including biosimilars and biologics. The SFDAs stringent guidelines ensure that all diabetes medications undergo rigorous safety and efficacy testing before being approved for use. These regulations are designed to maintain high standards of healthcare, ensuring that patients receive safe and effective treatment options.

KSA Diabetes Drugs Market Segmentation

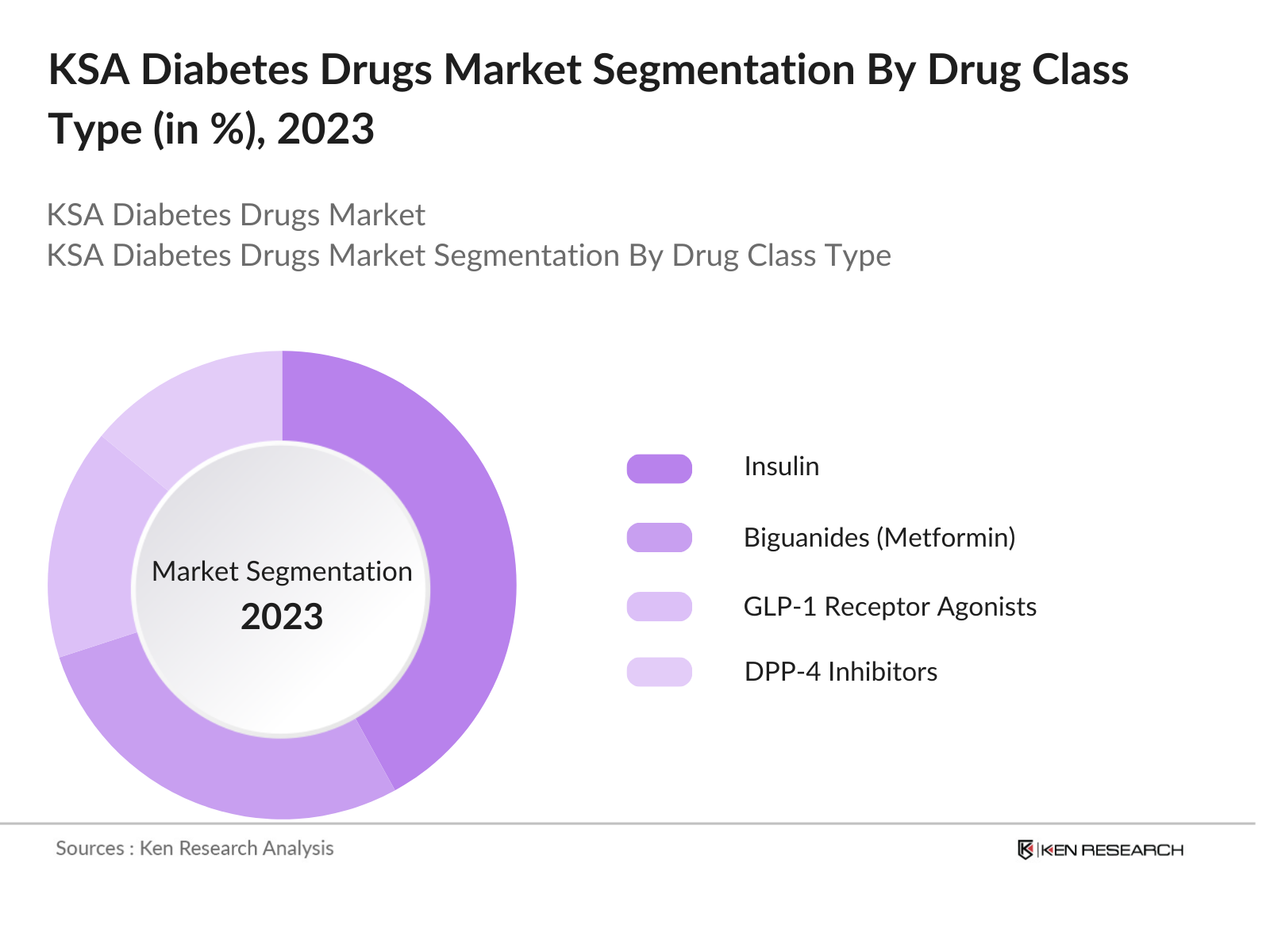

By Drug Class: The KSA diabetes drugs market is segmented by drug class into insulin, biguanides (metformin), GLP-1 receptor agonists, DPP-4 inhibitors, and SGLT-2 inhibitors. Recently, insulin has a dominant market share in KSA under this segmentation, primarily due to its widespread use in managing both Type 1 and advanced Type 2 diabetes. With advancements in insulin analogs and their improved efficacy and ease of administration, insulin continues to be the treatment of choice for many patients requiring intensive glucose control. The high prevalence of Type 1 diabetes also contributes significantly to the demand for insulin in the KSA market.

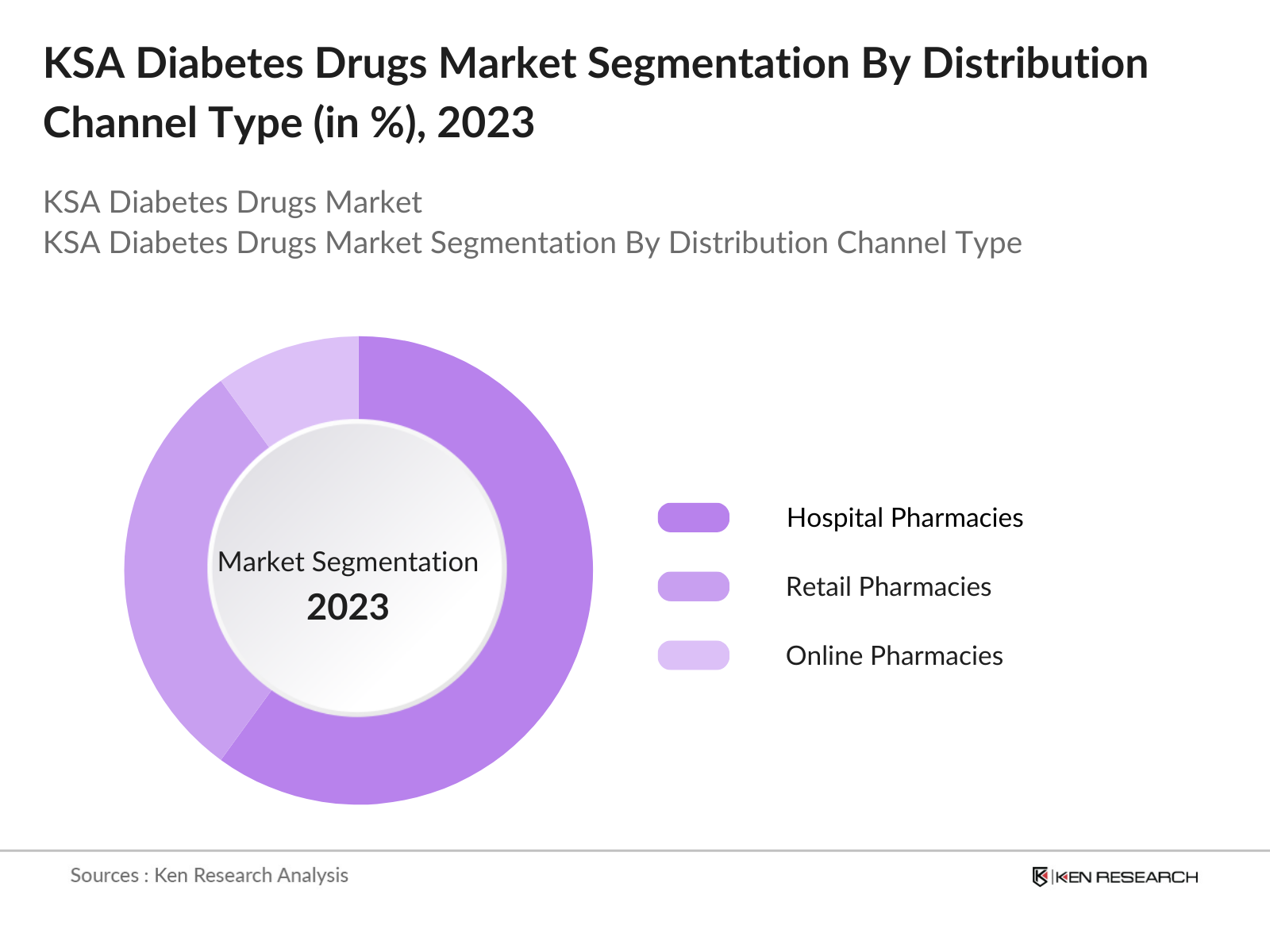

By Distribution Channel: The market is also segmented by distribution channels into hospital pharmacies, retail pharmacies, and online pharmacies. Hospital pharmacies hold the largest market share due to the centralized healthcare system in Saudi Arabia, where most diabetes patients receive prescriptions and treatments directly from hospitals. As healthcare access is expanding through the Vision 2030 initiative, hospital pharmacies remain the primary point of distribution for insulin and other diabetes medications. The convenience and trust patients place in hospitals for their chronic disease management contribute to the dominance of this sub-segment.

KSA Diabetes Drugs Market Competitive Landscape

The KSA diabetes drugs market is dominated by a few major international and regional players, reflecting the concentrated nature of the pharmaceutical industry in the region. Key companies such as Novo Nordisk and Sanofi lead in insulin production and advanced diabetes treatments, while local players are increasingly focusing on oral antidiabetic drugs. This consolidation highlights the significant influence of these key companies, which dominate the market through their established distribution networks, brand recognition, and partnerships with healthcare providers.

|

Company |

Establishment Year |

Headquarters |

Number of Employees |

Revenue (USD Bn) |

Product Portfolio |

Market Entry Date in KSA |

R&D Investments |

Local Partnerships |

Key Diabetes Drugs |

|

Novo Nordisk |

1923 |

Denmark |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Sanofi |

1973 |

France |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

AstraZeneca |

1999 |

UK |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Eli Lilly |

1876 |

USA |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Merck & Co. |

1891 |

USA |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

KSA Diabetes Drugs Industry Analysis

Growth Drivers

- Increasing Prevalence of Type 2 Diabetes: The Kingdom of Saudi Arabia (KSA) is facing a significant public health challenge with the rise in Type 2 diabetes cases. According to the Saudi Ministry of Health, as of 2023, over 4 million adults in the country have been diagnosed with diabetes. The International Diabetes Federation reports that the prevalence rate of diabetes in KSA is among the highest in the world. Urbanization, sedentary lifestyles, and dietary habits contribute to this growing number. The economic burden due to diabetes-related healthcare costs is estimated to be USD 3.8 billion annually.

- Rising Geriatric Population: Saudi Arabia's population is aging, with citizens over the age of 60 projected to comprise around 10% of the population by 2025. The Saudi General Authority for Statistics indicates that as of 2023, approximately 5 million people are aged 60 and above. This segment is particularly vulnerable to Type 2 diabetes, as older adults are more prone to chronic conditions due to physiological changes. With increased life expectancy, managing diabetes in older adults is a critical area of focus for the healthcare sector in KSA.

- Growing Awareness on Early Diagnosis: The Saudi Ministry of Health has launched several public health campaigns to increase awareness of diabetes and the importance of early diagnosis. In 2023, more than 2 million people participated in free nationwide screening programs, resulting in the early detection of diabetes in over 200,000 individuals. Educational programs on lifestyle changes and regular check-ups are being promoted, particularly in urban areas, to mitigate the long-term effects of the disease. These initiatives are crucial for reducing complications and healthcare costs associated with late-stage diabetes.

Market Challenges

- High Cost of Innovative Therapies: Innovative diabetes therapies, including GLP-1 receptor agonists and SGLT-2 inhibitors, are increasingly available in KSA. However, the high cost of these treatments poses a challenge. For example, GLP-1 receptor agonists can cost between SAR 1,200-2,500 (USD 320-665) per month, which can be prohibitive for many patients without insurance coverage. The Saudi healthcare system is currently balancing the introduction of advanced therapies with cost-effective options, but the affordability issue remains a barrier to widespread access.

- Limited Access to Healthcare in Remote Areas: Access to quality healthcare services remains limited in rural and remote regions of Saudi Arabia. The General Authority for Statistics reports that nearly 15% of the Saudi population lives in areas with limited healthcare infrastructure. Diabetes management is especially challenging in these areas due to the scarcity of specialists and advanced treatment options. Although the government has been expanding telemedicine and mobile healthcare units, logistical and financial constraints continue to impede equitable healthcare access across the country.

KSA Diabetes Drugs Market Future Outlook

Over the next five years, the KSA diabetes drugs market is expected to witness significant growth driven by government efforts to improve diabetes care, advancements in drug delivery systems, and increased awareness about diabetes management. The introduction of innovative drug classes, such as SGLT-2 inhibitors and GLP-1 receptor agonists, is anticipated to further boost the market. Additionally, Saudi Vision 2030s focus on healthcare development, along with increased private investments in the healthcare sector, is expected to create new opportunities for market players. The shift towards more personalized diabetes treatment approaches, including digital health solutions, is also likely to fuel future market growth.

Opportunities

- Expanding Healthcare Infrastructure: Saudi Arabia is undergoing a rapid expansion of its healthcare infrastructure, with the government investing SAR 50 billion (USD 13.3 billion) in new hospital projects in 2024. This expansion includes the establishment of specialized diabetes centers and clinics in both urban and rural areas. Additionally, new hospitals are being equipped with advanced diagnostic tools and treatment technologies to better manage chronic conditions such as diabetes. This infrastructure expansion is expected to improve patient access to diabetes care, fostering growth in the diabetes drugs market.

- Increased Focus on Personalized Medicine: Personalized medicine, which tailors treatment plans based on individual genetic and lifestyle factors, is gaining traction in Saudi Arabia's healthcare system. In 2024, the Ministry of Health launched pilot projects focusing on genetic testing for diabetes patients to optimize drug efficacy and reduce side effects. These initiatives are being supported by collaborations with global pharmaceutical companies. The shift towards personalized care is expected to drive demand for specialized diabetes drugs, particularly those designed for specific patient profiles.

Scope of the Report

|

Drug Class |

Insulin Biguanides GLP-1 Receptor Agonists DPP-4 Inhibitors SGLT-2 Inhibitors |

|

Diabetes Type |

Type 1 Diabetes Type 2 Diabetes |

|

Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies |

|

Route of Administration |

Oral Drugs Injectable Drugs |

|

Region |

Riyadh Jeddah Eastern Province Mecca Medina |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Saudi Food and Drug Authorities

Private Healthcare Industries

Diabetes Research Cntres

Pharmaceutical Manufacturing Companies

Hospital Chains and Clinic Industries

Investor and Venture Capitalist Firms

Insurance Companies

Companies

Players Mentioned in the Report

Novo Nordisk

Sanofi

AstraZeneca

Eli Lilly

Merck & Co.

Boehringer Ingelheim

Pfizer

GlaxoSmithKline (GSK)

Novartis

Medtronic

Table of Contents

1. KSA Diabetes Drugs Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Based on Prevalence of Diabetes in Population)

1.4. Market Segmentation Overview

2. KSA Diabetes Drugs Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis (Impact of Diabetes Awareness Campaigns)

2.3. Key Market Developments and Milestones (e.g., Adoption of Innovative Drugs, Regulatory Approvals)

3. KSA Diabetes Drugs Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Prevalence of Type 2 Diabetes

3.1.2. Rising Geriatric Population

3.1.3. Government Healthcare Initiatives (Vision 2030 Health Focus)

3.1.4. Growing Awareness on Early Diagnosis

3.2. Market Challenges

3.2.1. High Cost of Innovative Therapies

3.2.2. Limited Access to Healthcare in Remote Areas

3.2.3. Regulatory and Pricing Pressures

3.3. Opportunities

3.3.1. Expanding Healthcare Infrastructure

3.3.2. Increased Focus on Personalized Medicine

3.3.3. Strategic Collaborations with Global Pharma Companies

3.4. Trends

3.4.1. Adoption of Biosimilars

3.4.2. Shift Towards Digital Therapeutics (Mobile Apps for Diabetes Management)

3.4.3. Growth in GLP-1 Receptor Agonists and SGLT-2 Inhibitors Usage

3.5. Government Regulations

3.5.1. Saudi Food and Drug Authority (SFDA) Guidelines for Diabetes Drugs

3.5.2. National Diabetes Control Program

3.5.3. Public-Private Partnerships in Healthcare Initiatives

3.6. SWOT Analysis (Market-Specific Factors for KSA)

3.7. Stakeholder Ecosystem (Pharma Companies, Healthcare Providers, Regulatory Bodies)

3.8. Porters Five Forces (Competition, Buyer Power, Regulatory Influence)

3.9. Competitive Ecosystem

4. KSA Diabetes Drugs Market Segmentation

4.1. By Drug Class (In Value %)

4.1.1. Insulin

4.1.2. Biguanides (Metformin)

4.1.3. GLP-1 Receptor Agonists

4.1.4. DPP-4 Inhibitors

4.1.5. SGLT-2 Inhibitors

4.2. By Diabetes Type (In Value %)

4.2.1. Type 1 Diabetes

4.2.2. Type 2 Diabetes

4.3. By Distribution Channel (In Value %)

4.3.1. Hospital Pharmacies

4.3.2. Retail Pharmacies

4.3.3. Online Pharmacies

4.4. By Route of Administration (In Value %)

4.4.1. Oral Drugs

4.4.2. Injectable Drugs (Insulin, GLP-1 Agonists)

4.5. By Region (In Value %)

4.5.1. Riyadh

4.5.2. Jeddah

4.5.3. Eastern Province

4.5.4. Mecca

4.5.5. Medina

5. KSA Diabetes Drugs Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Sanofi

5.1.2. Novo Nordisk

5.1.3. AstraZeneca

5.1.4. Eli Lilly

5.1.5. Merck & Co.

5.1.6. Boehringer Ingelheim

5.1.7. Johnson & Johnson

5.1.8. Pfizer

5.1.9. GlaxoSmithKline (GSK)

5.1.10. Novartis

5.1.11. Medtronic

5.1.12. Takeda Pharmaceuticals

5.1.13. Cipla

5.1.14. Biocon

5.1.15. Abbott Laboratories

5.2 Cross Comparison Parameters (Number of Employees, Market Share, Product Portfolio, Global Presence, Market Entry Date, KSA-Specific Partnerships, Distribution Network, Innovation in Drug Delivery Systems)

5.3 Market Share Analysis (Key Competitors)

5.4 Strategic Initiatives (Partnerships, Licensing Deals, Joint Ventures)

5.5 Mergers and Acquisitions

5.6 Investment Analysis (Focus on KSA Market)

5.7 Venture Capital Funding (Focus on Diabetes Management Startups)

5.8 Government Grants (KSA Healthcare Initiatives)

5.9 Private Equity Investments

6. KSA Diabetes Drugs Market Regulatory Framework

6.1 SFDA Regulatory Landscape

6.2 Compliance Requirements (Drug Approval, Clinical Trials)

6.3 Certification Processes (Pharmaceutical Manufacturing Standards)

7. KSA Diabetes Drugs Market Future Size (In USD Mn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth (e.g., Prevalence of Diabetes, Rising Demand for New Treatments)

8. KSA Diabetes Drugs Market Future Segmentation

8.1 By Drug Class (In Value %)

8.2 By Diabetes Type (In Value %)

8.3 By Distribution Channel (In Value %)

8.4 By Route of Administration (In Value %)

8.5 By Region (In Value %)

9. KSA Diabetes Drugs Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Marketing Initiatives (Targeting Healthcare Providers, Consumer Awareness Campaigns)

9.3 Customer Cohort Analysis (By Diabetes Type, Age Group)

9.4 White Space Opportunity Analysis (Underserved Patient Segments)

Research Methodology

Step 1: Identification of Key Variables

This initial phase involves constructing a comprehensive ecosystem map of the KSA diabetes drugs market. It includes identifying major stakeholders, such as drug manufacturers, healthcare providers, and regulatory bodies. Extensive desk research utilizing government data, industry reports, and proprietary databases is conducted to pinpoint critical market variables, including diabetes prevalence rates and regulatory guidelines.

Step 2: Market Analysis and Construction

Historical data related to market size, drug adoption rates, and diabetes prevalence is analyzed to assess growth patterns. Market penetration ratios are calculated to determine the level of drug accessibility in different regions. We also assess the market's operational framework and distribution networks to ensure accuracy in revenue projections.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses, such as the demand for innovative diabetes drugs, are developed and validated through consultations with key market experts. These experts, representing pharmaceutical companies and healthcare institutions, provide practical insights that enrich our data and validate market projections.

Step 4: Research Synthesis and Final Output

The final phase synthesizes data from multiple sources, including direct consultations with industry stakeholders. A bottom-up approach is used to validate the data, and insights on future market trends are drawn. This ensures that the final report provides an accurate and comprehensive view of the KSA diabetes drugs market.

Frequently Asked Questions

1. How big is the KSA Diabetes Drugs Market?

The KSA diabetes drugs market is valued at USD 1.8 billion, driven by the increasing prevalence of diabetes and government initiatives aimed at improving healthcare infrastructure.

2. What are the challenges in the KSA Diabetes Drugs Market?

Challenges in the market include high costs of innovative therapies, limited healthcare access in rural areas, and stringent regulatory processes for new drug approvals.

3. Who are the major players in the KSA Diabetes Drugs Market?

Key players in the market include Novo Nordisk, Sanofi, AstraZeneca, Eli Lilly, and Merck & Co. These companies dominate due to their established drug portfolios and partnerships with healthcare providers.

4. What are the growth drivers of the KSA Diabetes Drugs Market?

The market is propelled by the rising prevalence of Type 2 diabetes, increased healthcare access through Vision 2030 initiatives, and growing awareness of advanced diabetes treatments.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.