KSA Diagnostic Imaging Market Outlook to 2030

Region:Middle East

Author(s):Meenakshi

Product Code:KROD3564

November 2024

98

About the Report

KSA Diagnostic Imaging Market Overview

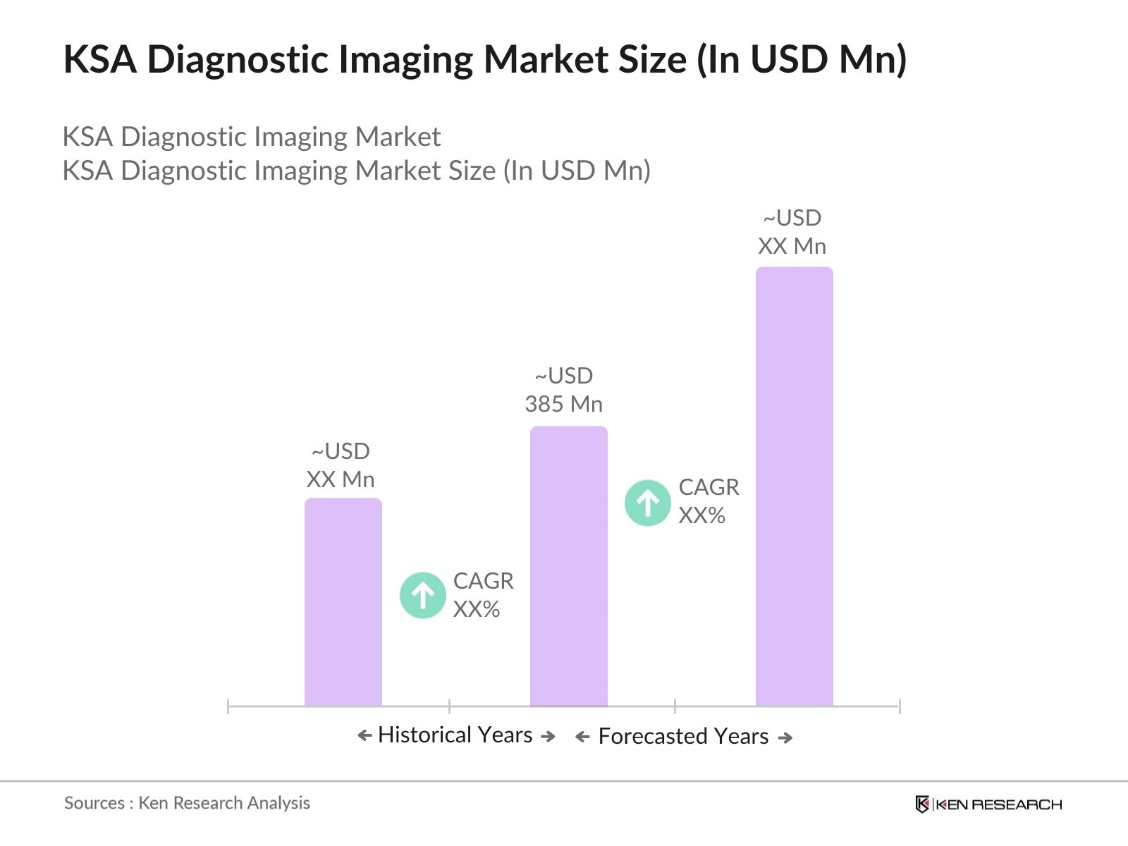

- The Kingdom of Saudi Arabia (KSA) diagnostic imaging market is valued at USD 385 million, driven primarily by the nation's healthcare transformation initiatives under Vision 2030. The market is shaped by increasing government investment in healthcare infrastructure, growing demand for advanced medical technologies, and a rise in non-communicable diseases like cardiovascular diseases and cancer.

- Riyadh, Jeddah, and Dammam dominate the diagnostic imaging market in KSA due to their advanced healthcare infrastructure and concentration of high-end medical facilities. These cities house the majority of tertiary hospitals and diagnostic centers, leading the demand for sophisticated diagnostic imaging modalities such as MRI and CT scanners. Additionally, the high population density and relatively higher disposable incomes in these cities enable a stronger demand for premium diagnostic services.

- The Saudi Food and Drug Authority (SFDA) strictly regulates the import and use of diagnostic imaging devices, requiring adherence to local and international standards. In 2024, the SFDA has implemented rigorous guidelines for the registration and certification of medical devices, including diagnostic imaging systems, to ensure patient safety and device efficacy. These regulations cover product testing, certification, and post-market surveillance.

KSA Diagnostic Imaging Market Segmentation

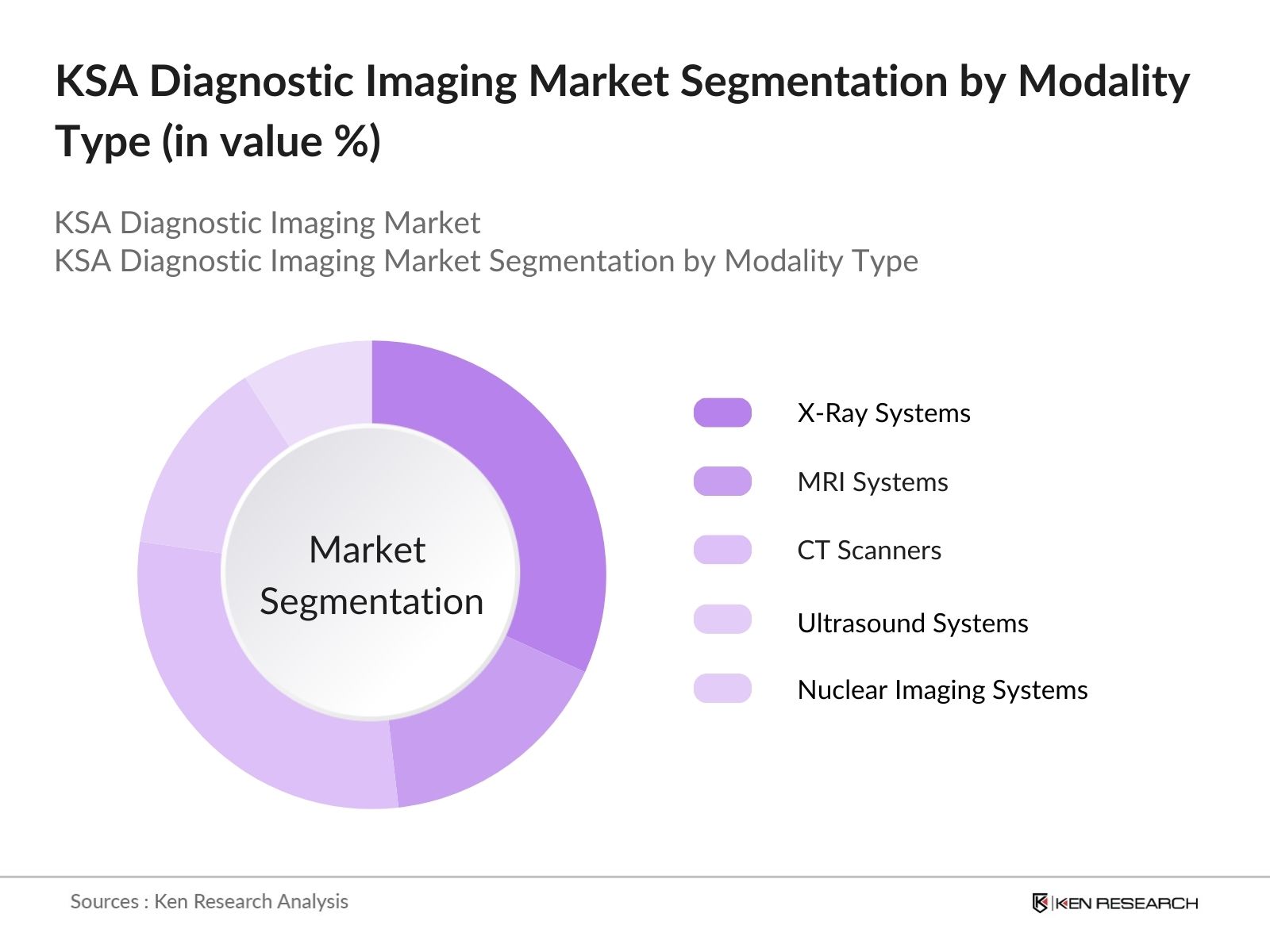

By Modality Type: The KSA diagnostic imaging market is segmented by modality type into X-Ray Systems, MRI Systems, CT Scanners, Ultrasound Systems, and Nuclear Imaging Systems. The CT Scanners hold a dominant market share under the modality type segment due to their widespread use in the detection of complex medical conditions like cardiovascular diseases, cancer, and neurological disorders. CT scanners provide rapid and highly detailed imaging, which is crucial for accurate diagnosis and treatment planning, making them an indispensable tool in both emergency and routine diagnostics. Their ability to combine high resolution with quick processing times has contributed significantly to their dominance.

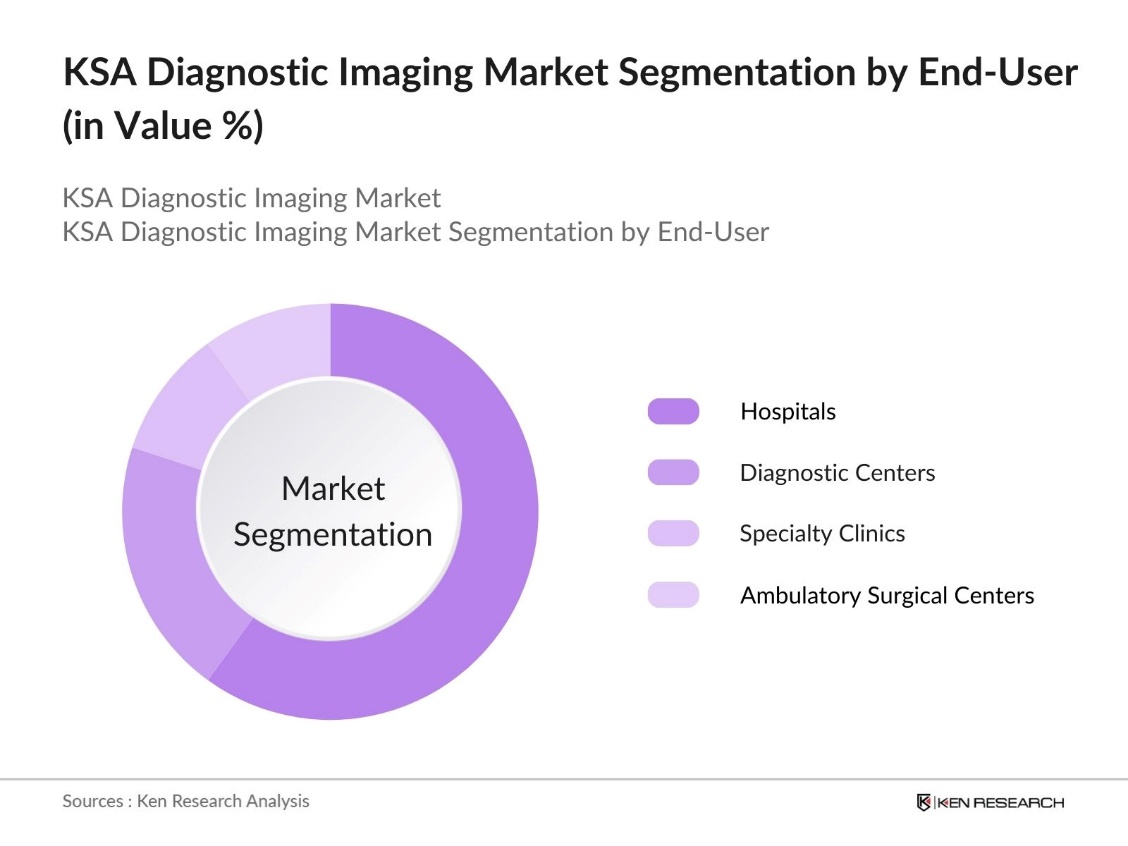

By End-User: The market is segmented by end-user into Hospitals, Diagnostic Centers, Specialty Clinics, and Ambulatory Surgical Centers. The Hospitals are the dominant end-user in the KSA diagnostic imaging market due to their extensive infrastructure and capacity to handle a high volume of patients. Large hospitals, particularly in urban areas, invest heavily in advanced diagnostic imaging equipment to ensure they meet the complex healthcare needs of patients. Hospitals also benefit from government initiatives and funding, allowing them to acquire cutting-edge imaging technologies, which helps solidify their position as the primary end-user segment.

KSA Diagnostic Imaging Market Competitive Landscape

The KSA diagnostic imaging market is dominated by a mix of global and regional players. These companies are investing heavily in R&D and forming strategic partnerships to maintain their foothold in this growing market. The competitive landscape is characterized by innovation in imaging technologies, strategic collaborations, and a focus on expanding into rural and underserved areas to increase market penetration.

|

Company Name |

Establishment Year |

Headquarters |

Product Range |

Global Presence |

R&D Investment |

Recent Acquisition |

Local Partnerships |

AI Integration |

Modality Innovation |

|

GE Healthcare |

1892 |

Chicago, USA |

|||||||

|

Siemens Healthineers |

1847 |

Erlangen, Germany |

|||||||

|

Philips Healthcare |

1891 |

Amsterdam, Netherlands |

|||||||

|

Canon Medical Systems |

1930 |

Otawara, Japan |

|||||||

|

Mindray Medical International |

1991 |

Shenzhen, China |

KSA Diagnostic Imaging Industry Analysis

Growth Drivers

- Rise in Non-Communicable Diseases (e.g., Cardiovascular, Cancer): Non-communicable diseases (NCDs), such as cardiovascular diseases and cancers, are significant contributors to the rise in demand for diagnostic imaging in Saudi Arabia. For instance, one report states that NCDs account for approximately 35% of deaths in the Kingdom, leading to higher demand for early detection through imaging technologies like MRI and CT scans. Cardiovascular diseases are particularly concerning. This surge in NCD cases is pushing healthcare facilities to invest heavily in advanced diagnostic imaging systems to enhance disease detection.

- Technological Advancements in Imaging Systems (e.g., AI Integration): Technological advancements, particularly the integration of artificial intelligence (AI) into diagnostic imaging systems, are driving market growth in Saudi Arabia. In 2024, the Saudi government has supported AI applications in healthcare, including AI-powered imaging solutions that improve diagnostic accuracy and speed. AI integration aids radiologists in detecting complex diseases, such as cancers and neurodegenerative disorders. This technology is being rapidly adopted in major healthcare institutions, where AI is assisting in interpreting large volumes of imaging data.

- Increased Medical Tourism: Saudi Arabia's expanding medical tourism sector is playing a key role in boosting the diagnostic imaging market. By positioning itself as a regional healthcare center, the country is attracting patients from abroad who seek advanced medical treatments. The growing demand for diagnostic services, including imaging technologies like PET scans and MRIs, is driving the need for state-of-the-art infrastructure. This trend is especially advantageous for private hospitals that depend on modern diagnostic imaging systems.

Market Challenges

- High Cost of Diagnostic Imaging Equipment: The high cost of acquiring advanced diagnostic imaging equipment, such as MRI machines and CT scanners, poses a significant challenge for healthcare providers in Saudi Arabia. Smaller hospitals and clinics, especially in rural areas, face difficulties investing in these technologies due to the substantial initial capital expenditure and ongoing maintenance costs. This limits accessibility to modern diagnostic imaging technologies across the healthcare system.

- Lack of Skilled Radiologists and Technicians: Another challenge in Saudi Arabia's diagnostic imaging market is the shortage of skilled radiologists and imaging technicians. This shortage is especially critical in rural and remote areas, where healthcare facilities struggle to attract qualified professionals. The limited availability of specialized training programs and certification processes for imaging technicians further exacerbates this issue, impeding the effective use of advanced imaging systems.

KSA Diagnostic Imaging Market Future Outlook

The KSA diagnostic imaging market is poised for significant growth, driven by continuous advancements in imaging technologies, a rising prevalence of chronic diseases, and strong governmental support through healthcare reforms under Vision 2030. Increasing public-private partnerships and foreign investment will also accelerate the market's growth, particularly in underpenetrated regions of the country. In addition, the growing use of AI and machine learning in diagnostic imaging will revolutionize the accuracy and speed of diagnoses, further enhancing the demand for advanced imaging systems across KSA.

Market Opportunities

- Expansion of Radiology Centers in Rural Areas: The expansion of diagnostic radiology centers in rural areas offers a significant opportunity within Saudi Arabia's healthcare landscape. Initiatives are underway to establish new diagnostic imaging centers equipped with advanced technologies like MRI, CT, and ultrasound machines in underserved regions. These efforts are focused on addressing the healthcare accessibility gap between urban and rural areas, ultimately improving healthcare outcomes for a larger segment of the population.

- Public-Private Partnerships for Healthcare Infrastructure: Public-private partnerships (PPPs) are playing a crucial role in driving healthcare infrastructure development, including diagnostic imaging facilities. These collaborations are fostering innovation and enabling the adoption of advanced imaging technologies across both public and private hospitals. By leveraging private sector expertise and resources, these partnerships aim to accelerate healthcare transformation, particularly in diagnostic imaging services

Scope of the Report

|

By Modality Type |

X-Ray Systems MRI Systems CT Scanners Ultrasound Systems Nuclear Imaging Systems |

|

By End-User |

Hospitals Diagnostic Centers Specialty Clinics Ambulatory Surgical Centers |

|

By Application |

Oncology Cardiology Neurology Orthopedics Obstetrics & Gynecology |

|

By Technology |

2D Imaging 3D and 4D Imaging AI-Powered Imaging Digital Imaging |

|

By Region |

Central Western Eastern Northern Southern Region |

Products

Key Target Audience

Pharmaceutical Companies

Biomedical Engineering Companies

Medical Equipment Leasing Companies

Healthcare Technology Startups

Government and Regulatory Bodies (Ministry of Health, Saudi Food and Drug Authority)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

GE Healthcare

Siemens Healthineers

Philips Healthcare

Canon Medical Systems

Mindray Medical International

Hitachi Medical Systems

Carestream Health

Agfa HealthCare

Fujifilm Holdings Corporation

Esaote S.p.A.

Table of Contents

1. KSA Diagnostic Imaging Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. KSA Diagnostic Imaging Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. KSA Diagnostic Imaging Market Analysis

3.1. Growth Drivers

3.1.1. Government Healthcare Initiatives (e.g., Vision 2030)

3.1.2. Rise in Non-Communicable Diseases (e.g., Cardiovascular, Cancer)

3.1.3. Technological Advancements in Imaging Systems (e.g., AI Integration)

3.1.4. Increased Medical Tourism

3.2. Market Challenges

3.2.1. High Cost of Diagnostic Imaging Equipment

3.2.2. Lack of Skilled Radiologists and Technicians

3.2.3. Regulatory Compliance and Certification Barriers

3.3. Opportunities

3.3.1. Expansion of Radiology Centers in Rural Areas

3.3.2. Public-Private Partnerships for Healthcare Infrastructure

3.3.3. Growing Demand for Mobile and Point-of-Care Imaging

3.4. Trends

3.4.1. Adoption of AI and Machine Learning in Diagnostics

3.4.2. Shift from 2D to 3D and 4D Imaging Technologies

3.4.3. Increased Investment in Digital Radiography (DR) Systems

3.5. Government Regulations

3.5.1. Saudi FDA Regulations for Medical Devices

3.5.2. Health Sector Transformation Program (Vision 2030)

3.5.3. Licensing and Certification Requirements for Diagnostic Equipment

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.7.1. Hospitals and Clinics

3.7.2. Diagnostic Centers

3.7.3. Imaging Equipment Manufacturers

3.7.4. Government Health Authorities

3.8. Porters Five Forces

3.8.1. Bargaining Power of Suppliers

3.8.2. Bargaining Power of Buyers

3.8.3. Threat of New Entrants

3.8.4. Threat of Substitutes

3.8.5. Industry Rivalry

3.9. Competition Ecosystem

4. KSA Diagnostic Imaging Market Segmentation

4.1. By Modality Type (In Value %)

4.1.1. X-Ray Systems

4.1.2. MRI Systems

4.1.3. CT Scanners

4.1.4. Ultrasound Systems

4.1.5. Nuclear Imaging Systems

4.2. By End-User (In Value %)

4.2.1. Hospitals

4.2.2. Diagnostic Centers

4.2.3. Specialty Clinics

4.2.4. Ambulatory Surgical Centers

4.3. By Application (In Value %)

4.3.1. Oncology

4.3.2. Cardiology

4.3.3. Neurology

4.3.4. Orthopedics

4.3.5. Obstetrics & Gynecology

4.4. By Technology (In Value %)

4.4.1. 2D Imaging

4.4.2. 3D and 4D Imaging

4.4.3. AI-Powered Imaging

4.4.4. Digital Imaging

4.5. By Region (In Value %)

4.5.1. Central Region

4.5.2. Western Region

4.5.3. Eastern Region

4.5.4. Northern Region

4.5.5. Southern Region

5. KSA Diagnostic Imaging Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. GE Healthcare

5.1.2. Siemens Healthineers

5.1.3. Philips Healthcare

5.1.4. Canon Medical Systems

5.1.5. Fujifilm Holdings Corporation

5.1.6. Hitachi Medical Systems

5.1.7. Carestream Health

5.1.8. Mindray Medical International

5.1.9. Agfa HealthCare

5.1.10. Esaote S.p.A

5.1.11. Samsung Medison

5.1.12. Shimadzu Corporation

5.1.13. Hologic Inc.

5.1.14. Neusoft Medical Systems

5.1.15. Planmed Oy

5.2. Cross Comparison Parameters

(Revenue, Headquarters, Employees, Product Portfolio, Innovation Capabilities, Distribution Network, Regional Focus, Service Offerings)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. KSA Diagnostic Imaging Market Regulatory Framework

6.1. Healthcare Standards Compliance

6.2. Equipment Certification Process

6.3. Reimbursement Policies

7. KSA Diagnostic Imaging Market Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. KSA Diagnostic Imaging Market Future Segmentation

8.1. By Modality Type (In Value %)

8.2. By End-User (In Value %)

8.3. By Application (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9. KSA Diagnostic Imaging Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In the initial phase, an extensive ecosystem mapping was conducted to identify the primary stakeholders in the KSA Diagnostic Imaging Market. This step included comprehensive desk research using secondary databases, market reports, and government publications to capture a detailed understanding of market dynamics.

Step 2: Market Analysis and Construction

In this step, historical data on the market was gathered and analyzed, focusing on market penetration and the revenue generation potential across various diagnostic imaging modalities. Market penetration ratios, equipment usage, and adoption trends were assessed to ensure data reliability.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were developed based on the gathered data and validated through interviews with healthcare providers, medical device distributors, and equipment manufacturers. These insights from industry experts helped in fine-tuning the market estimates and segmentation analysis.

Step 4: Research Synthesis and Final Output

The final phase of the research involved synthesizing the gathered data with insights obtained from industry stakeholders. This ensured the creation of a robust and well-validated market report that accurately reflects the trends, challenges, and opportunities in the KSA diagnostic imaging market.

Frequently Asked Questions

01. How big is the KSA Diagnostic Imaging Market?

The KSA diagnostic imaging market is valued at USD 385 million, primarily driven by advancements in medical technology and an increase in non-communicable diseases requiring diagnostic imaging.

02. What are the challenges in the KSA Diagnostic Imaging Market?

Challenges in KSA diagnostic imaging market include high equipment costs, regulatory compliance hurdles, and a shortage of skilled radiologists to operate advanced diagnostic imaging systems.

03. Who are the major players in the KSA Diagnostic Imaging Market?

Key players in the KSA diagnostic imaging market include GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and Mindray Medical International.

04. What are the growth drivers of the KSA Diagnostic Imaging Market?

The KSA diagnostic imaging market growth drivers include government healthcare initiatives under Vision 2030, increasing demand for advanced diagnostic tools for chronic disease management, and significant technological advancements such as AI integration in imaging.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.