KSA Digital Twin Market Outlook to 2030

Region:Saudi Arabia

Author(s):Yogita Sahu

Product Code:KROD2585

Region:Saudi Arabia

Author(s):Yogita Sahu

Product Code:KROD2585

October 2024

97

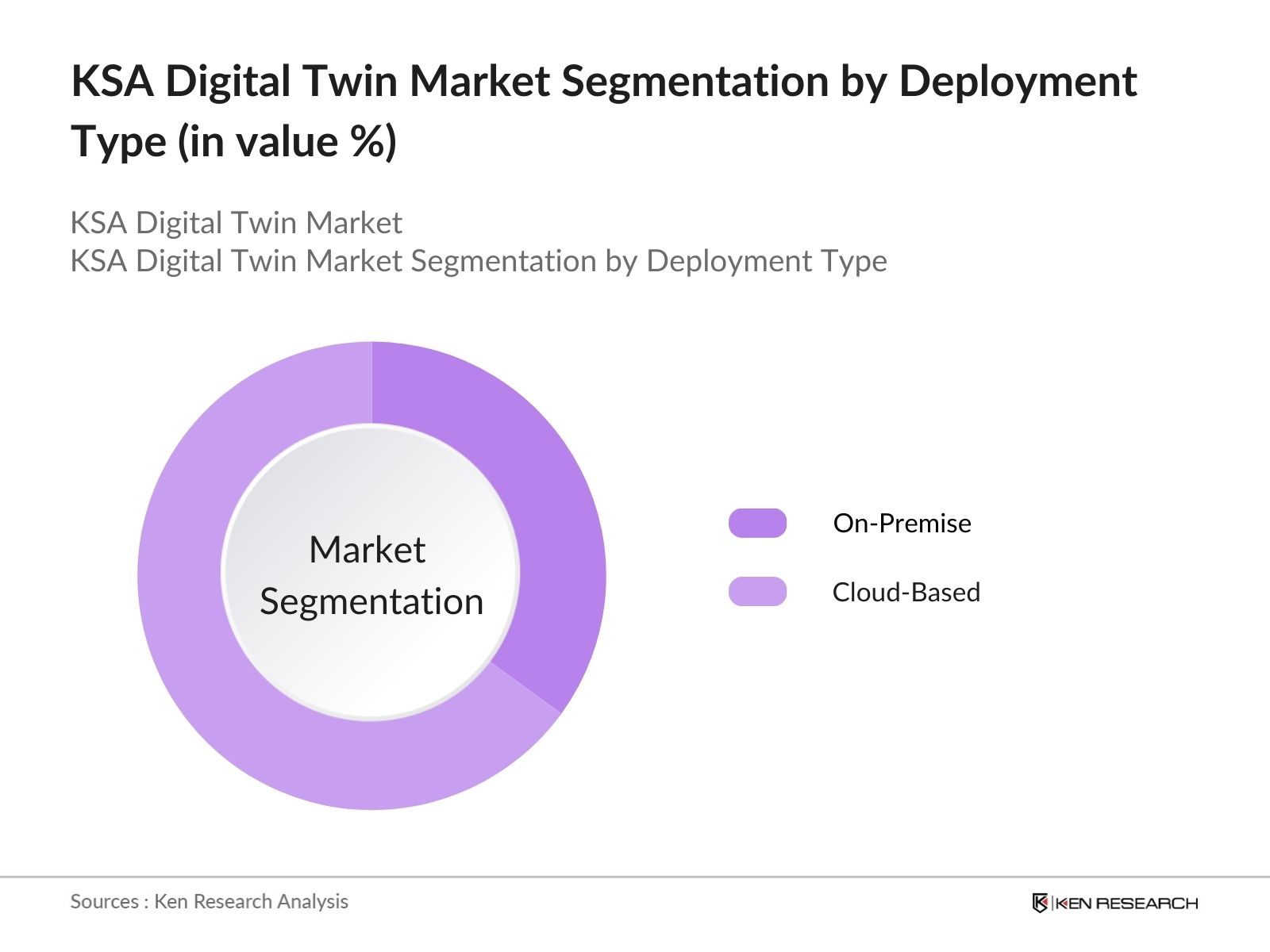

By Deployment Type: The market is segmented by deployment type into On-Premise and Cloud-Based. Cloud-based solutions have dominated the market due to the flexibility, scalability, and cost-effectiveness they offer. Cloud-based digital twins enable real-time data integration and remote monitoring, which are vital for industries like oil & gas and manufacturing, where operational efficiency is key.

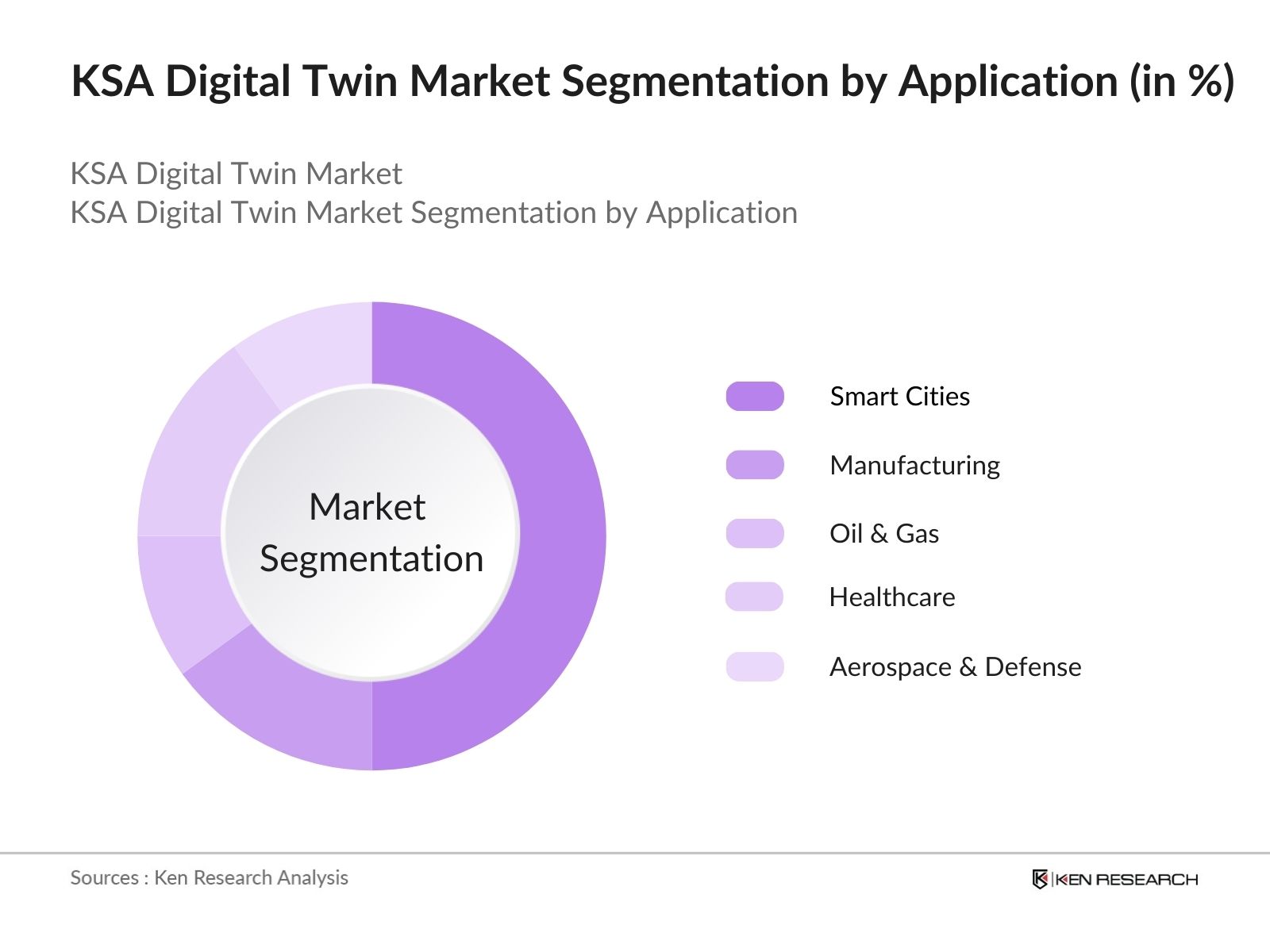

By Application: The market is also segmented by application into Smart Cities, Manufacturing, Oil & Gas, Healthcare, and Aerospace & Defense. The smart cities segment currently dominates the market due to the government's heavy investment in projects like NEOM and other urban transformation initiatives. The integration of digital twins in these smart city projects allows for real-time monitoring, predictive maintenance, and efficient energy usage, making it an essential tool in urban planning and management.

The market is dominated by a mix of international tech giants and regional players. Companies like Siemens, General Electric, and IBM have established a strong presence due to their expertise in industrial IoT and software solutions. Local players, in collaboration with global firms, are also making inroads, particularly in sectors like oil & gas and manufacturing.

|

Company Name |

Established |

Headquarters |

Revenue (2023) |

No. of Employees |

Major Industry Focus |

Partnerships |

R&D Investments |

Patent Holdings |

Regional Focus |

|

Siemens AG |

1847 |

Munich, Germany |

|||||||

|

General Electric |

1892 |

Boston, USA |

|||||||

|

IBM Corporation |

1911 |

Armonk, USA |

|||||||

|

Microsoft Corporation |

1975 |

Redmond, USA |

|||||||

|

Bentley Systems |

1984 |

Exton, USA |

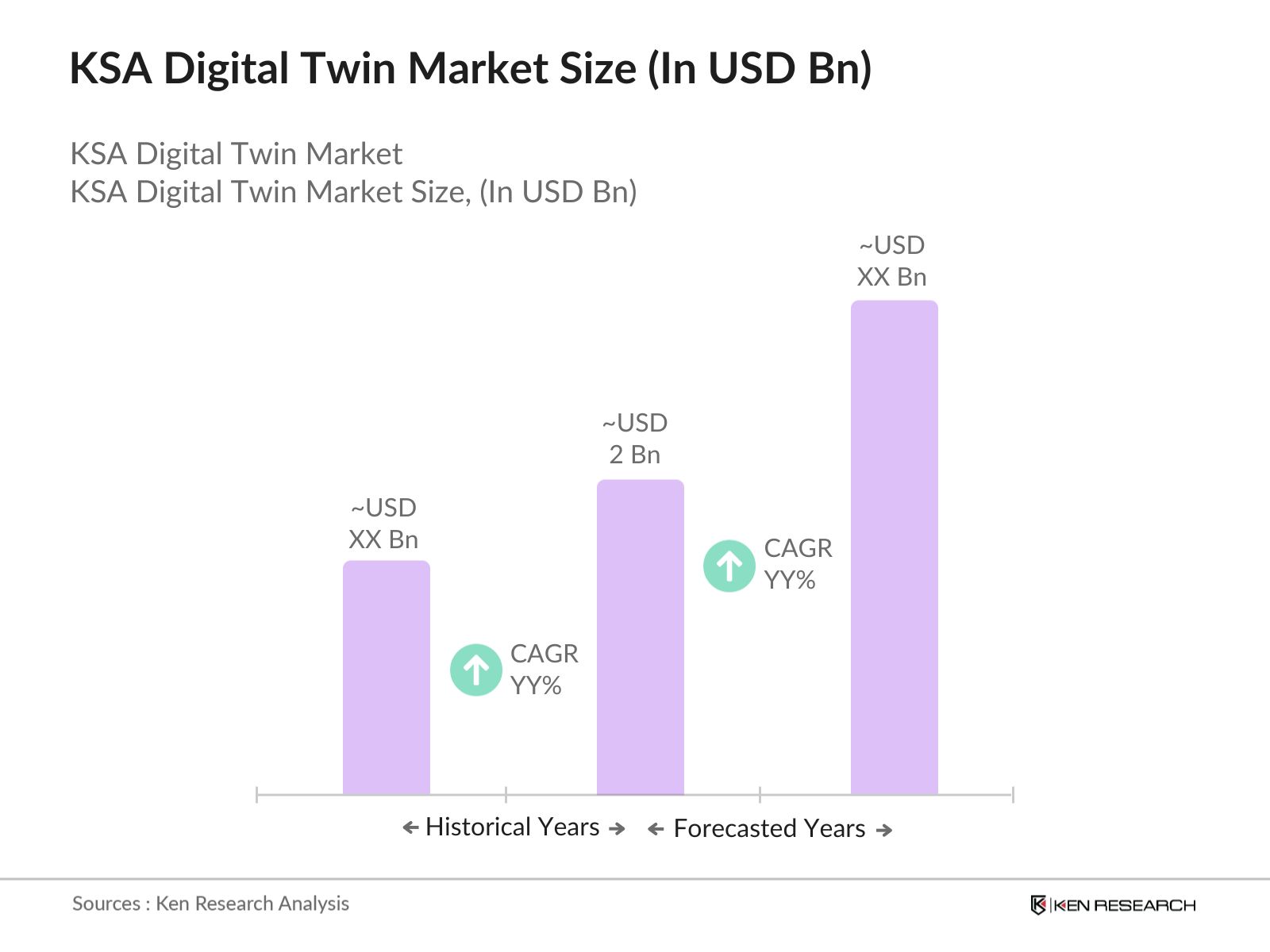

Over the next five years, the KSA digital twin industry is expected to witness substantial growth driven by continuous government support, advancements in digital twin technology, and increasing demand for smart city solutions. The focus on digital transformation as part of Vision 2030, along with large-scale infrastructure projects. The rise in adoption across sectors like oil & gas, healthcare, and manufacturing also points towards an expansion of the market.

|

By Deployment Type |

On-Premise |

|

Cloud-Based |

|

|

By Application |

Smart Cities |

|

Manufacturing |

|

|

Oil & Gas |

|

|

Healthcare |

|

|

Aerospace & Defense |

|

|

By Technology |

IoT-Enabled Digital Twins |

|

AI and Machine Learning Integration |

|

|

Edge Computing for Twins |

|

|

Simulation Software |

|

|

By End-User |

Government |

|

Manufacturing Industries |

|

|

Healthcare Providers |

|

|

Oil & Gas Corporations |

|

|

Aerospace |

|

|

By Region |

Central Region |

|

Eastern Province |

|

|

Western Region |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Government Vision 2030 Initiatives

3.1.2. Increasing Adoption in Manufacturing and Infrastructure

3.1.3. Expansion of Smart Cities and IoT Ecosystem

3.1.4. Demand for Asset Optimization and Predictive Maintenance

3.2. Market Challenges

3.2.1. High Initial Deployment Costs

3.2.2. Limited Skilled Workforce in Digital Twin Implementation

3.2.3. Integration with Legacy Systems

3.3. Opportunities

3.3.1. Integration with AI and Machine Learning Models

3.3.2. Collaboration with International Tech Firms

3.3.3. Growing Adoption Across Energy, Oil & Gas Sectors

3.4. Trends

3.4.1. Rising Use of Digital Twins in Healthcare

3.4.2. Growing Focus on Sustainability and Decarbonization

3.4.3. Expansion of Edge Computing for Real-Time Twin Operations

3.5. Government Regulation

3.5.1. National Digital Transformation Program

3.5.2. Regulatory Framework for Smart Infrastructure

3.5.3. Guidelines for AI and IoT Integration

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Deployment Type (In Value %)

4.1.1. On-Premise

4.1.2. Cloud-Based

4.2. By Application (In Value %)

4.2.1. Smart Cities

4.2.2. Manufacturing

4.2.3. Oil & Gas

4.2.4. Healthcare

4.2.5. Aerospace & Defense

4.3. By Technology (In Value %)

4.3.1. IoT-Enabled Digital Twins

4.3.2. AI and Machine Learning Integration

4.3.3. Edge Computing for Twins

4.3.4. Simulation Software

4.4. By End-User (In Value %)

4.4.1. Government

4.4.2. Manufacturing Industries

4.4.3. Healthcare Providers

4.4.4. Oil & Gas Corporations

4.4.5. Aerospace

4.5. By Region (In Value %)

4.5.1. Central Region

4.5.2. Eastern Province

4.5.3. Western Region

5.1. Detailed Profiles of Major Companies

5.1.1. Siemens AG

5.1.2. General Electric

5.1.3. IBM Corporation

5.1.4. Microsoft Corporation

5.1.5. Oracle Corporation

5.1.6. Dassault Systmes

5.1.7. Bentley Systems

5.1.8. ABB Group

5.1.9. Honeywell International Inc.

5.1.10. PTC Inc.

5.1.11. Ansys Inc.

5.1.12. Bosch.IO

5.1.13. Schneider Electric

5.1.14. AVEVA Group PLC

5.1.15. Hexagon AB

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Market Presence, Revenue, Industry Focus, Technology Patents, Innovation Index, Partnerships/Collaborations)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Compliance with National Smart Infrastructure Standards

6.2. Digital Twin Integration Guidelines in Energy Sector

6.3. Data Privacy and Security in Digital Twin Deployments

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Deployment Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Go-To-Market Strategies

9.4. White Space Opportunity Analysis

The first phase involves constructing a comprehensive ecosystem map of all stakeholders within the KSA Digital Twin Market. This step is based on in-depth desk research using secondary databases to identify the critical variables influencing the market, such as technological adoption, industrial demand, and government policies.

We analyzed historical data from industry reports to determine market penetration, the ratio of deployments across sectors, and revenue generation trends. This stage also included evaluating service quality metrics, ensuring the reliability and accuracy of the revenue forecasts.

Market hypotheses were developed and validated through consultations with industry experts via computer-assisted telephone interviews (CATIs). These discussions provided vital financial and operational insights from key market players.

This phase involved direct engagement with industry stakeholders such as manufacturers, service providers, and government agencies to verify data. The insights gathered from these interactions were synthesized with bottom-up market estimates, ensuring a comprehensive and accurate analysis of the KSA Digital Twin Market.

The KSA Digital Twin market is valued at USD 2 billion, driven by the increasing adoption of smart city projects, digital transformation initiatives, and industrial automation.

The KSA Digital Twin market faces challenges such as high initial implementation costs, limited local expertise in digital twin technology, and integration issues with legacy systems.

Key players in the KSA digital twin market include Siemens AG, General Electric, IBM Corporation, Microsoft Corporation, and Bentley Systems. These companies dominate due to their expertise in digital solutions and strategic partnerships in Saudi Arabia.

The KSA digital twin market is propelled by factors such as government support under Vision 2030, smart city projects like NEOM, and the adoption of digital twin technology in industries like oil & gas and manufacturing.

Opportunities in the KSA digital twin market include the growing integration of AI and machine learning, the expansion of smart cities, and the rising demand for real-time operational insights and predictive maintenance solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.