KSA Electric Commercial Vehicles Market Outlook to 2030

Region:Middle East

Author(s):Vijay Kumar

Product Code:KROD3788

December 2024

90

About the Report

KSA Electric Commercial Vehicles Market Overview

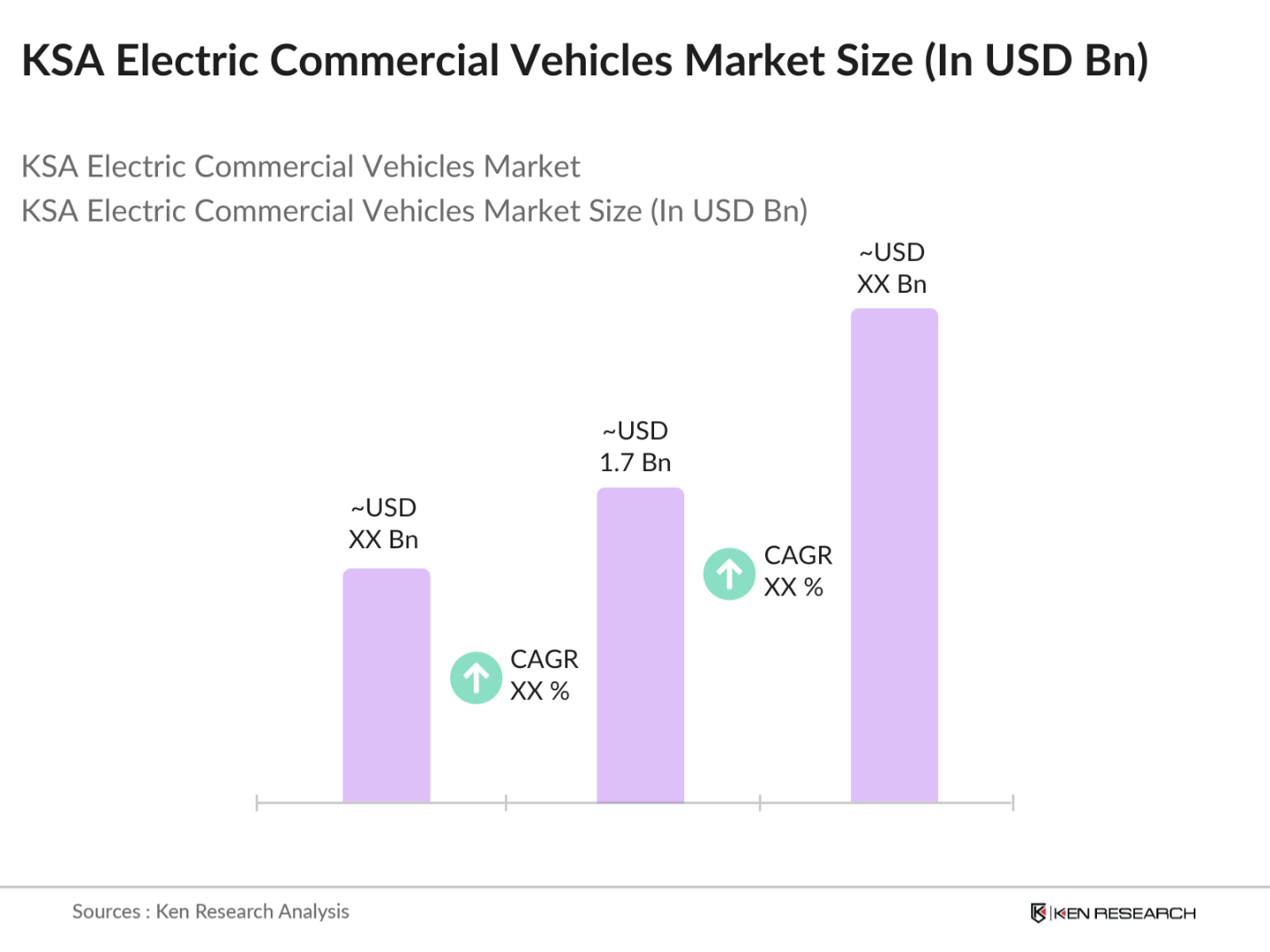

- The KSA Electric Commercial Vehicles market is valued at USD 1.7 billion, based on a five-year historical analysis. This markets growth is primarily driven by government initiatives aimed at reducing carbon emissions, coupled with technological advancements in electric vehicle infrastructure, including charging stations. Additionally, increasing awareness around sustainable transportation options has led businesses to transition their commercial fleets to electric vehicles, particularly within the logistics and municipal sectors. These factors are enhancing the demand for electric commercial vehicles across KSA.

- Riyadh and Jeddah are the leading cities in the adoption of electric commercial vehicles in KSA. Riyadh's position as the Kingdom's capital, coupled with government-led pilot projects and substantial urban logistics demand, contributes to its dominance. Jeddahs importance stems from its strategic position as a trade and logistics hub, where electric vehicles are increasingly preferred for commercial fleets to mitigate pollution and reduce operational expenses.

- To promote electric vehicle adoption, the Saudi government has introduced various subsidies and incentives. In 2024, the Public Investment Fund (PIF) invested $1.5 billion in Lucid Motors to support the production of electric sedans and SUVs within the kingdom. Additionally, the government offers tax exemptions and reduced registration fees for electric vehicle owners, making EVs more accessible to consumers and businesses.

KSA Electric Commercial Vehicles Market Segmentation

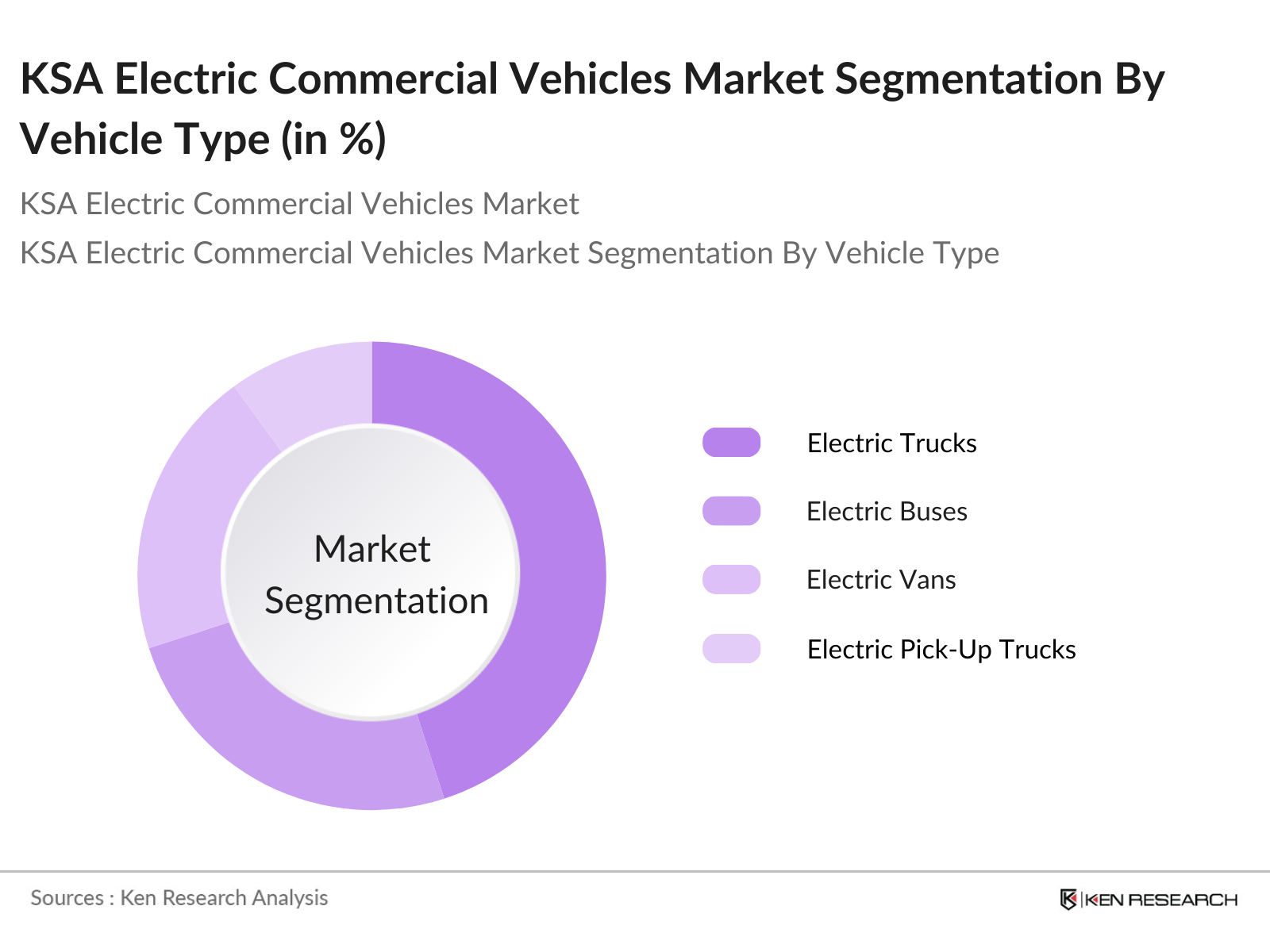

By Vehicle Type The market is segmented by vehicle type, which includes electric trucks, electric buses, electric vans, and electric pick-up trucks. Currently, electric trucks hold a significant market share under this segmentation due to their critical role in the transportation and logistics sector. With companies aiming to lower their carbon footprints and operational costs, electric trucks are increasingly favored for their efficiency in heavy-duty tasks, especially for intercity and last-mile delivery.

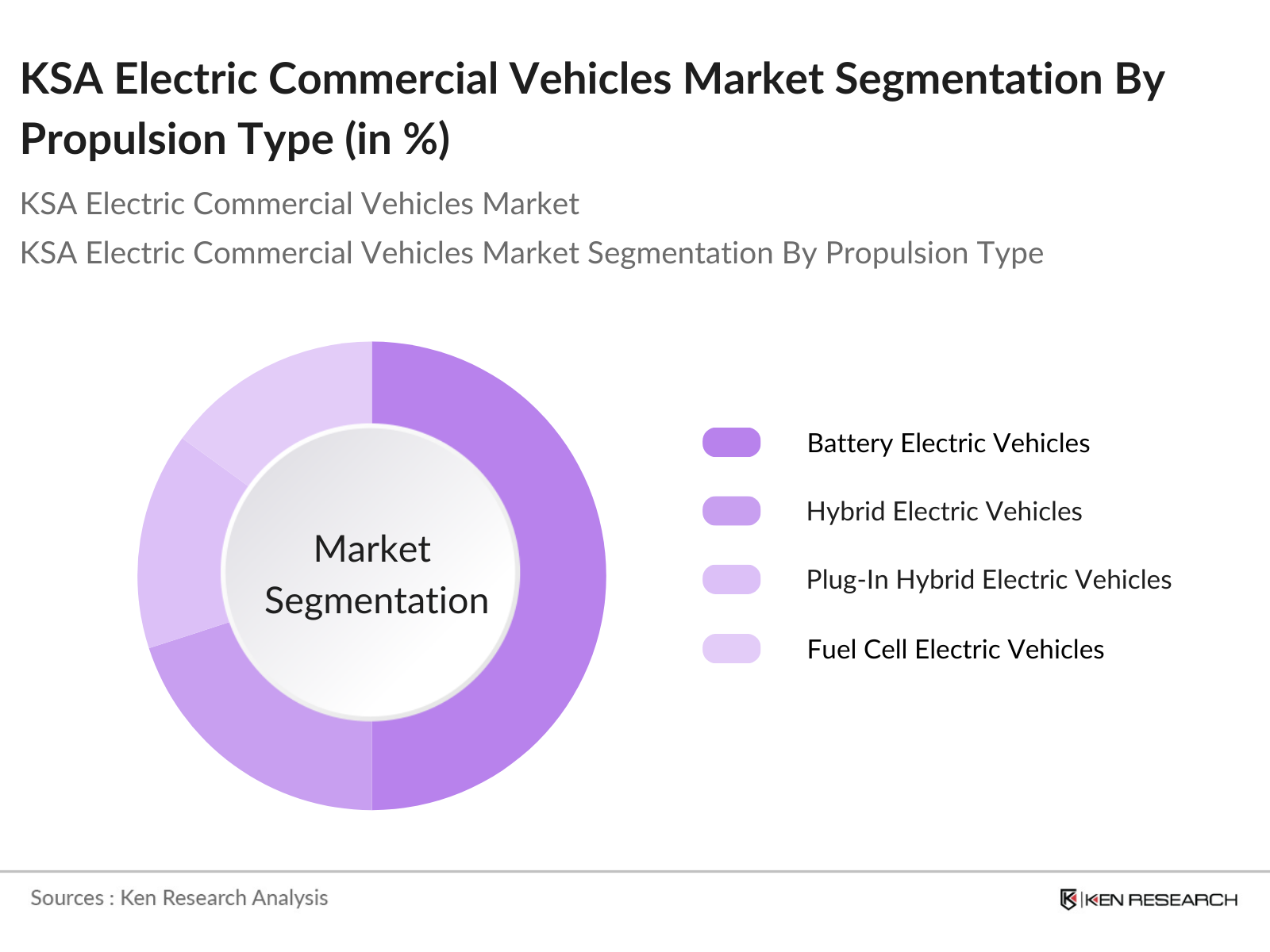

By Propulsion Type In terms of propulsion type, the market is divided into Battery Electric Vehicles (BEV), Hybrid Electric Vehicles (HEV), Plug-In Hybrid Electric Vehicles (PHEV), and Fuel Cell Electric Vehicles (FCEV). BEVs currently dominate this segmentation due to advancements in battery technology and the availability of subsidies, making them more cost-effective for commercial fleet operators. Additionally, BEVs align with KSAs goal to transition towards sustainable energy and zero-emission transportation.

KSA Electric Commercial Vehicles Market Competitive Landscape

The KSA electric commercial vehicle market is dominated by a combination of local and global players. These companies are leading the sector due to their investments in technological innovation, robust distribution networks, and strategic partnerships with local stakeholders. The KSA markets competitive landscape is defined by a few major players, which includes global manufacturers like Hyundai Motors, BYD Motors, and Scania AB, alongside emerging local players.

KSA Electric Commercial Vehicles Industry Analysis

Growth Drivers

- Expansion of Charging Infrastructure: The Saudi government is actively developing EV charging infrastructure to support the anticipated increase in electric vehicles. In 2024, the kingdom announced plans to install over 5,000 public charging stations nationwide by 2025, focusing on urban centers and major highways. This initiative aims to alleviate range anxiety and promote EV adoption among consumers and commercial fleets. Additionally, partnerships with private sector entities are encouraged to expedite infrastructure development.

- Increasing Environmental Regulations: Saudi Arabia has implemented stringent environmental regulations to reduce greenhouse gas emissions and combat climate change. The kingdom's commitment to the Paris Agreement includes reducing carbon emissions by 130 million tons by 2030. To achieve this, policies such as fuel economy standards and emission reduction targets have been introduced, incentivizing the transition to electric commercial vehicles. These regulations align with global efforts to mitigate environmental impact and promote sustainable transportation solutions.

- Rising Demand for Sustainable Transport Solutions: There is a growing demand for sustainable transport solutions in Saudi Arabia, driven by environmental awareness and economic diversification goals. The logistics and transportation sectors are increasingly adopting electric commercial vehicles to reduce operational costs and carbon footprints. For instance, in 2024, several logistics companies in the kingdom integrated electric trucks into their fleets, aiming to decrease fuel expenses and comply with environmental regulations. This shift reflects a broader trend towards sustainability in the transportation industry.

Market Challenges

- High Initial Investment and Maintenance Costs: The adoption of electric commercial vehicles in Saudi Arabia faces challenges due to high initial investment and maintenance costs. Electric trucks and buses require significant upfront capital, often exceeding that of traditional diesel vehicles. Additionally, specialized maintenance and the need for trained technicians contribute to higher operational expenses. These financial barriers can deter small and medium-sized enterprises from transitioning to electric fleets, despite long-term cost savings from reduced fuel consumption and lower emissions.

- Limited Charging Infrastructure and Long Charging Times: Despite ongoing efforts, Saudi Arabia's EV charging infrastructure remains limited, particularly in rural and remote areas. As of 2024, the majority of charging stations are concentrated in major cities, posing challenges for long-haul commercial vehicles. Furthermore, current charging technologies result in longer downtime compared to refueling conventional vehicles, impacting fleet efficiency. Addressing these issues requires substantial investment in fast-charging networks and advancements in battery technology to reduce charging times.

KSA Electric Commercial Vehicles Market Future Outlook

Over the next five years, the KSA electric commercial vehicles market is poised for growth. Factors such as government incentives, increasing environmental consciousness, and advancements in battery efficiency are expected to drive this expansion. The focus on reducing greenhouse gas emissions and operational costs across public and private sectors will further bolster demand for electric commercial vehicles.

Market Opportunities

- Technological Advancements in Battery Efficiency: Advancements in battery technology present significant opportunities for Saudi Arabia's electric commercial vehicle market. In 2024, the Saudi Arabian Mining Company (Ma'aden) successfully piloted lithium extraction from seawater, aiming to support domestic battery production. This development could lead to more efficient and cost-effective batteries, enhancing vehicle range and reducing charging times. Investing in local battery manufacturing aligns with the kingdom's Vision 2030 goals of economic diversification and technological innovation.

- Potential for Strategic Partnerships with Global OEMs: Saudi Arabia's electric vehicle sector can benefit from strategic partnerships with global Original Equipment Manufacturers (OEMs). In 2024, Indian EV maker Wardwizard Innovations announced plans to establish a joint venture in the kingdom, including the creation of assembly and EV cell plants. Such collaborations can facilitate technology transfer, enhance local manufacturing capabilities, and accelerate the deployment of electric commercial vehicles. These partnerships also support job creation and contribute to the development of a robust EV ecosystem within the country.

Scope of the Report

|

Vehicle Type |

Electric Trucks Electric Buses Electric Vans Electric Pick-Up Trucks |

|

Propulsion Type |

Battery Electric Vehicles (BEV) Hybrid Electric Vehicles (HEV) Plug-In Hybrid Electric Vehicles (PHEV) Fuel Cell Electric Vehicles (FCEV) |

|

Range |

0-150 Miles 151-250 Miles 251-400 Miles Above 400 Miles |

|

Battery Capacity |

Less than 100 kWh 100 kWh 200 kWh 201 kWh 300 kWh Above 300 kWh |

|

Region |

Northern and Central Region Western Region Southern Region Eastern Region |

Products

Key Target Audience

Logistics and Transportation Companies

Municipal and Public Transport Authorities

Fleet Management Service Providers

Automotive Parts Suppliers

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (Ministry of Transport, Saudi Standards, Metrology and Quality Organization)

Environmental Protection Agencies

Electric Vehicle Infrastructure Providers

Companies

Players Mentioned in the Report

IVECO

Scania AB

Volvo AG

Renault Group

Lucid Motors

Chevrolet Inc.

Hyundai Motors

Ford Motor Company

Nissan Motor Corporation

Tesla, Inc.

Table of Contents

1. Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Market Size (In USD Million)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Market Analysis

3.1 Growth Drivers

3.1.1 Government Initiatives Supporting EV Adoption

3.1.2 Expansion of Charging Infrastructure

3.1.3 Increasing Environmental Regulations

3.1.4 Rising Demand for Sustainable Transport Solutions

3.2 Market Challenges

3.2.1 High Initial Investment and Maintenance Costs

3.2.2 Limited Charging Infrastructure and Long Charging Times

3.2.3 Consumer Concerns on Range and Reliability

3.3 Opportunities

3.3.1 Technological Advancements in Battery Efficiency

3.3.2 Potential for Strategic Partnerships with Global OEMs

3.3.3 Expansion in Emerging Sectors (Logistics and Public Transport)

3.4 Trends

3.4.1 Rise in Autonomous Electric Vehicles

3.4.2 Increasing Use of Renewable Energy in Charging Infrastructure

3.4.3 Development of Urban Logistics Hubs for EV Fleets

3.5 Government Regulations

3.5.1 Emission Reduction and Carbon Neutrality Targets

3.5.2 Subsidies and Incentives for Electric Vehicle Adoption

3.5.3 Local Manufacturing Initiatives for EV Parts

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape

4. Market Segmentation

4.1 By Vehicle Type (In Value %)

4.1.1 Electric Trucks

4.1.2 Electric Buses

4.1.3 Electric Vans

4.1.4 Electric Pick-Up Trucks

4.2 By Propulsion Type (In Value %)

4.2.1 Battery Electric Vehicles (BEV)

4.2.2 Hybrid Electric Vehicles (HEV)

4.2.3 Plug-In Hybrid Electric Vehicles (PHEV)

4.2.4 Fuel Cell Electric Vehicles (FCEV)

4.3 By Range (In Value %)

4.3.1 0-150 Miles

4.3.2 151-250 Miles

4.3.3 251-400 Miles

4.3.4 Above 400 Miles

4.4 By Battery Capacity (In Value %)

4.4.1 Less than 100 kWh

4.4.2 100 kWh - 200 kWh

4.4.3 201 kWh - 300 kWh

4.4.4 Above 300 kWh

4.5 By Region (In Value %)

4.5.1 Northern and Central Region

4.5.2 Western Region

4.5.3 Southern Region

4.5.4 Eastern Region

5. Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 IVECO

5.1.2 Scania AB

5.1.3 Volvo AG

5.1.4 Renault Group

5.1.5 Lucid Motors

5.1.6 Chevrolet Inc.

5.1.7 Hyundai Motors

5.1.8 Ford Motor Company

5.1.9 Nissan Motor Corporation

5.1.10 Tesla, Inc.

5.1.11 BYD Motors Inc.

5.1.12 Daimler Truck AG

5.1.13 Paccar Inc.

5.1.14 Canoo Inc.

5.1.15 Tata Motors

5.2 Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Product Portfolio, Market Share, Regional Presence, Strategic Initiatives)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.6.1 Venture Capital Funding

5.6.2 Government Grants

5.6.3 Private Equity Investments

6. Regulatory Framework

6.1 Environmental Standards

6.2 Compliance and Certification Requirements

6.3 Import Tariffs and Subsidy Programs

7. Future Market Size (In USD Million)

7.1 Market Size Projections

7.2 Key Drivers of Future Growth

8. Future Market Segmentation

8.1 By Vehicle Type (In Value %)

8.2 By Propulsion Type (In Value %)

8.3 By Range (In Value %)

8.4 By Battery Capacity (In Value %)

8.5 By Region (In Value %)

9. Analysts Recommendations

9.1 TAM, SAM, and SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping the KSA electric commercial vehicle ecosystem by identifying major stakeholders and industry drivers. This includes analyzing key regulatory and economic factors impacting the markets growth trajectory.

Step 2: Market Analysis and Construction

This phase entails gathering historical market data to assess market penetration, the volume of electric vehicle deployment, and revenue contributions. Market trends, customer preferences, and technological developments are analyzed to ensure accuracy in data interpretation.

Step 3: Hypothesis Validation and Expert Consultation

We developed market hypotheses that were validated through in-depth interviews with industry experts. These consultations provided insights into competitive positioning and strategic priorities directly from key market players.

Step 4: Research Synthesis and Final Output

The synthesis process integrates findings from various data sources, including interviews and proprietary databases, to produce a comprehensive and reliable market analysis. A robust bottom-up approach ensures precision in revenue and market share estimates, tailored for stakeholders in the KSA electric commercial vehicle market.

Frequently Asked Questions

01. How big is the KSA Electric Commercial Vehicles Market?

The KSA Electric Commercial Vehicles market is valued at USD 1.7 billion, based on a five-year historical analysis. This markets growth is primarily driven by government initiatives aimed at reducing carbon emissions, coupled with technological advancements in electric vehicle infrastructure, including charging stations.

02. What challenges does the KSA Electric Commercial Vehicles Market face?

Challenges include the high initial costs of electric commercial vehicles, limited charging infrastructure, and concerns around battery life and maintenance.

03. Who are the major players in the KSA Electric Commercial Vehicles Market?

Key players include IVECO, Scania AB, BYD Motors, Hyundai Motors, and Lucid Motors. These companies dominate due to their advanced technology and strategic partnerships.

04. What drives growth in the KSA Electric Commercial Vehicles Market?

Growth drivers include government incentives, technological advancements in battery efficiency, and a growing emphasis on reducing carbon emissions across logistics and public transport sectors.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.