KSA Fashion Market Outlook to 2030

Region:Middle East

Author(s):Mukul

Product Code:KROD3803

October 2024

95

About the Report

KSA Fashion Market Overview

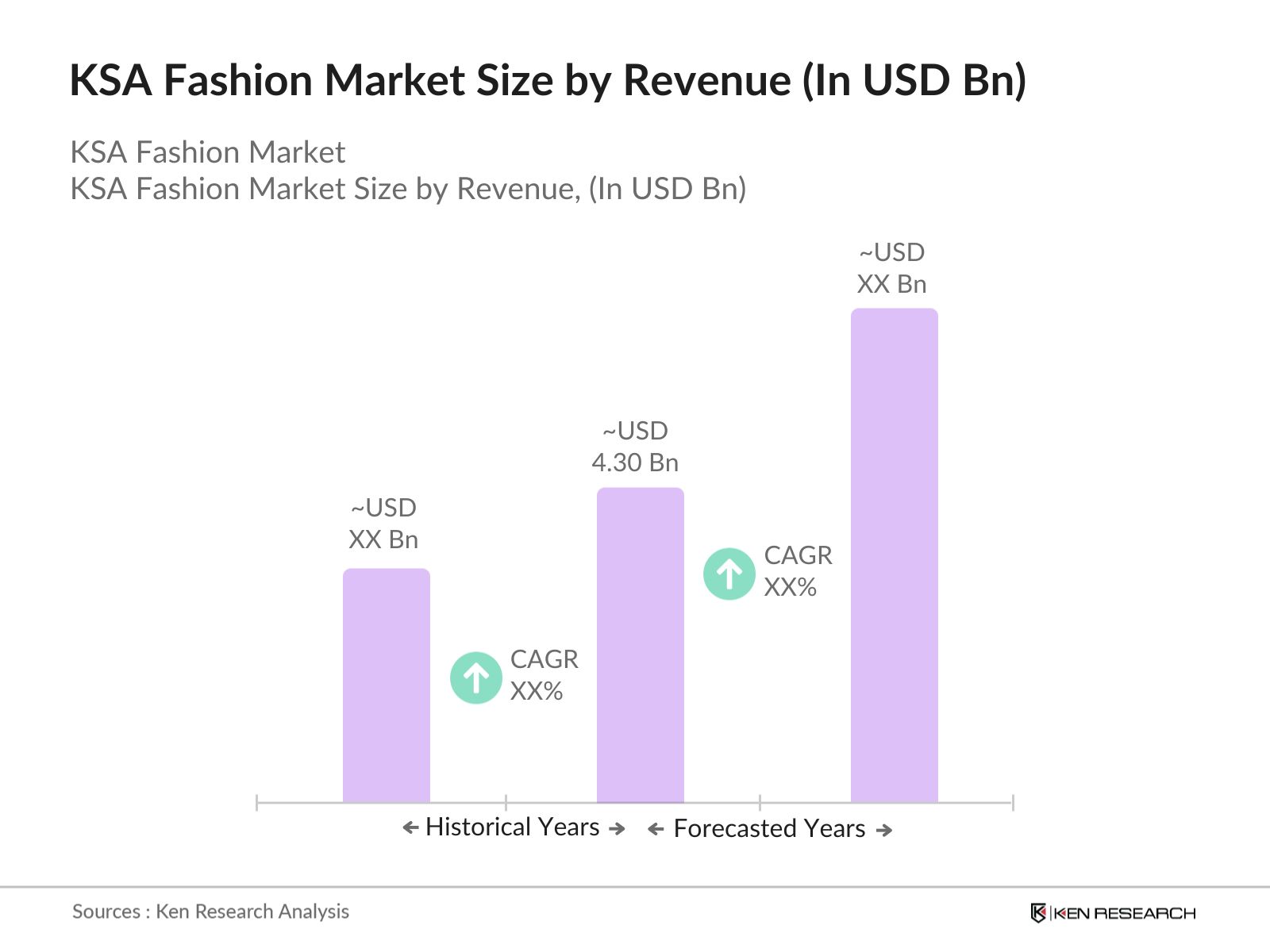

- The KSA fashion market size by revenue USD 4.30 billion, based on a five-year historical analysis. The market is primarily driven by the increasing demand for luxury fashion and the shift towards online retail. As consumer preferences evolve, brands are adapting to the rise of e-commerce, offering exclusive collections and personalized services online. In addition, the KSA government’s Vision 2030 plan has promoted the growth of the retail and fashion sectors by focusing on economic diversification and infrastructure development. This push towards modernization, coupled with the rise in disposable income, has further boosted the demand for high-end and contemporary fashion.

- The fashion market in KSA is dominated by cities such as Riyadh, Jeddah, and Dammam. These cities have the highest concentration of high-net-worth individuals and a strong presence of international and local fashion brands. Riyadh, being the capital, attracts significant investments from luxury retailers, while Jeddah benefits from its status as a major commercial hub. Dammam, with its growing industrial base and consumer spending, also plays a crucial role in the fashion market. The urbanization in these cities has led to the proliferation of luxury malls and fashion retail spaces, solidifying their dominance in the market.

- The Saudi government has imposed import duties on foreign fashion products to encourage the growth of the local fashion industry. In 2023, import duties on apparel and footwear averaged 12%, making international brands more expensive for consumers. This policy is designed to promote local fashion production and reduce reliance on imports, creating opportunities for Saudi designers and manufacturers. The higher import duties have also driven international brands to establish local production facilities, further boosting domestic employment and contributing to the Kingdom's economic diversification goals under Vision 2030.

KSA Fashion Market Segmentation

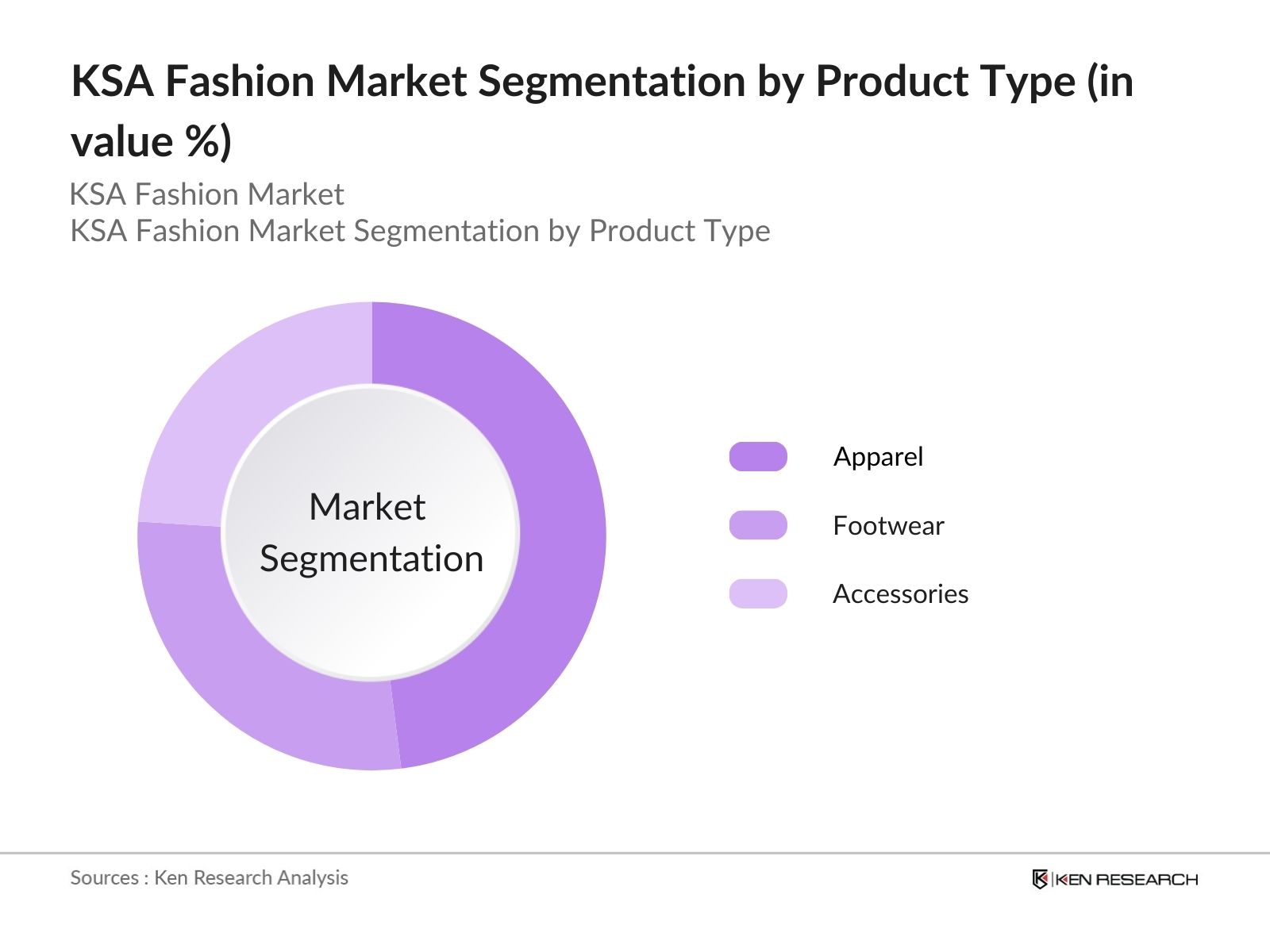

- By Product Type: The KSA fashion market is segmented by product type into apparel, footwear, and accessories. Recently, apparel dominated the market, driven by the demand for modest fashion, which aligns with cultural norms in the region. Local brands offering modest apparel and international brands launching specific collections for the KSA market have contributed to this segment’s growth. The trend towards high-end luxury apparel has also played a part in this segment’s dominance, especially with consumers increasingly seeking exclusive and premium-quality products.

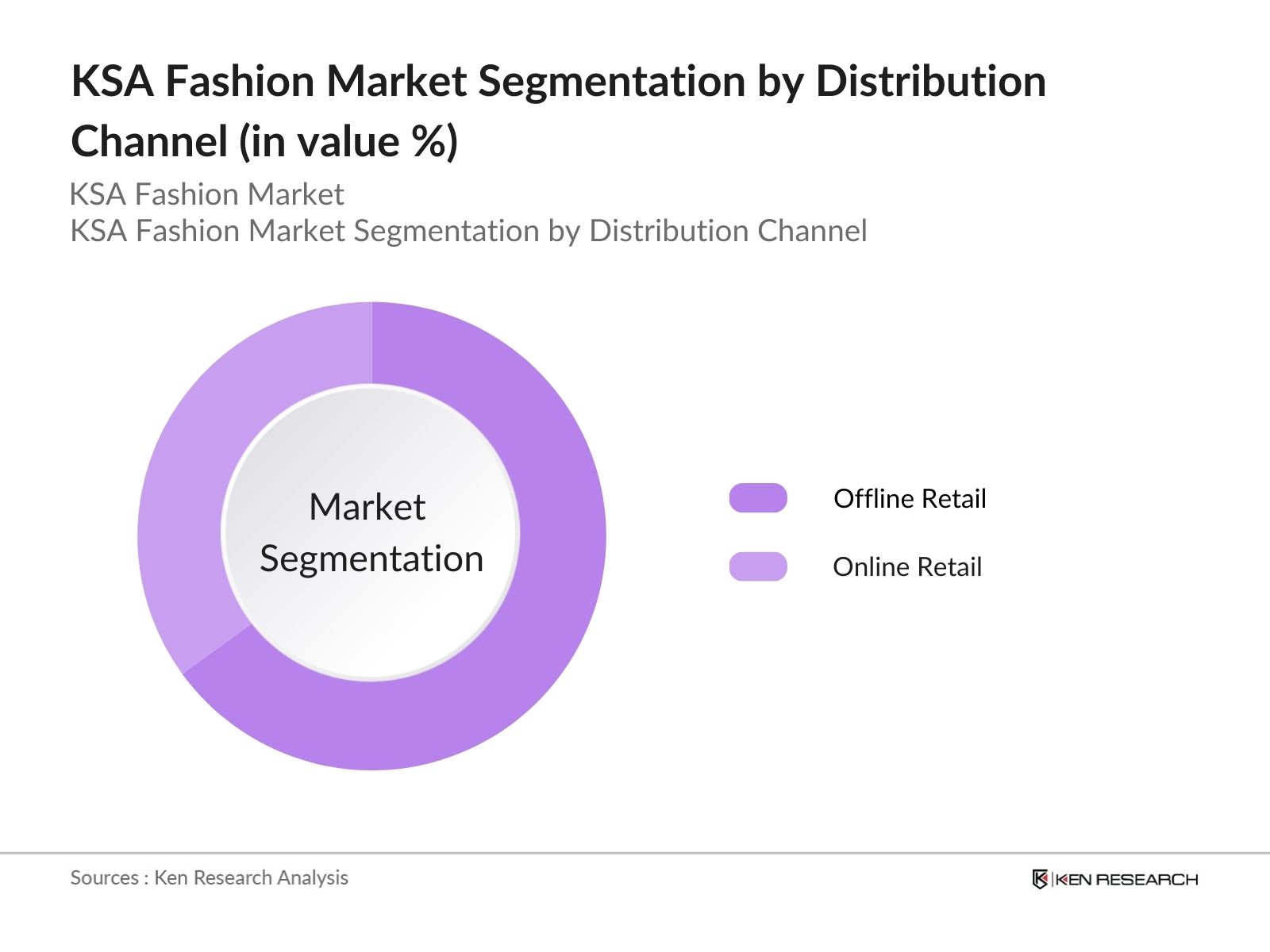

- By Distribution Channel: The KSA fashion market is also segmented by distribution channel into online retail and offline retail. offline retail dominated the market, with a growing number of consumers preferring the convenience of shopping through e-commerce platforms. The rise of mobile commerce and social media influencers promoting fashion trends online has significantly boosted the online segment. Additionally, brands have been investing in omnichannel strategies, integrating their online and offline operations to offer seamless shopping experiences.

KSA Fashion Market Competitive Landscape

The KSA fashion market is dominated by a few key players, with local brands and international luxury brands having a significant presence. Companies such as Femi9, Zara (Inditex Group), and Max Fashion hold substantial market shares due to their wide distribution networks, strong brand appeal, and ability to adapt to local tastes. These companies have leveraged online platforms and fashion influencers to increase consumer engagement, solidifying their positions in the market.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

No. of Stores |

Target Market |

Product Focus |

E-Commerce Presence |

Key Expansion Initiatives |

|

Femi9 |

1999 |

Riyadh, KSA |

|

|

|

|

|

|

|

Zara (Inditex Group) |

1974 |

Arteixo, Spain |

|

|

|

|

|

|

|

Max Fashion (Landmark) |

2004 |

Dubai, UAE |

|

|

|

|

|

|

|

Louis Vuitton |

1854 |

Paris, France |

|

|

|

|

|

|

|

Gucci |

1921 |

Florence, Italy |

|

|

|

|

|

|

KSA Fashion Industry Analysis

KSA Fashion Market Growth Drivers

- Rise of E-Commerce (Online Retail Adoption): E-commerce adoption in Saudi Arabia has grown exponentially, driven by a young, tech-savvy population and government-led initiatives to boost digital infrastructure. In 2023, the number of internet users in Saudi Arabia reached 36 million, representing almost 98% of the total population. The surge in online shopping has bolstered the fashion retail sector, with e-commerce fashion sales increasing by 30% year-on-year. Initiatives like the National Transformation Program have enhanced digital payments, boosting e-commerce adoption, making online retail a critical growth driver for the fashion industry.

(Source: Saudi Communications and Information Technology Commission) - Changing Consumer Preferences: Saudi consumers, particularly the younger generation, are increasingly influenced by Western fashion trends due to increased exposure through social media and global travel. Over 70% of the Saudi population is under 35, a demographic that is driving demand for international fashion brands and styles. Platforms like Instagram and TikTok, with millions of Saudi users, have become key influencers in shaping consumer behavior. The result is a growing interest in casual and luxury Western fashion, which has spurred international brands like Gucci and Zara to expand their presence in the region.

(Source: Saudi General Authority for Statistics) - Increase in Disposable Income (Impact on Luxury Fashion): In 2023, Saudi Arabia’s GDP per capita was approximately $25,000, and rising disposable income has played a critical role in boosting demand for luxury fashion. Saudi Arabia’s luxury goods market grew by 12% in 2023, with brands like Louis Vuitton, Chanel, and Dior seeing increased sales. The Kingdom's affluent population, along with the growing middle class, is fueling a preference for high-end fashion. Additionally, luxury spending by Saudi women has grown substantially, driven by increased female participation in the workforce and financial independence.

KSA Fashion Market Restraints

- Supply Chain Disruptions: Logistical challenges, including delayed shipments and rising transportation costs, have disrupted Saudi Arabia's fashion supply chain. In 2023, freight costs increased by nearly 25%, largely driven by global inflation and the increased price of oil, impacting the ability of fashion retailers to maintain inventory. The ongoing global supply chain disruptions have caused delays in the import of fabrics, clothing, and luxury fashion products, leading to longer waiting times for consumers. This issue is further exacerbated by the limited local production of fashion goods, making the sector heavily reliant on imports.

- Cultural Barriers in Fashion Preferences: Despite the influence of Western fashion, there are significant cultural barriers in Saudi Arabia that affect consumer preferences. The Kingdom's conservative society prefers modest clothing styles that align with Islamic values. In 2023, around 55% of Saudi women reported prioritizing modest fashion over Western trends. This has posed a challenge for international brands that do not cater to the modest fashion segment. The growth of this market has led to brands like Dolce & Gabbana and Nike launching modest fashion lines, but the challenge of balancing modern trends with traditional values persists.

KSA Fashion Market Future Outlook

Over the next five years, the KSA fashion market is expected to experience substantial growth, driven by a combination of government initiatives, technological advancements in retail, and increasing consumer demand for premium and luxury products. E-commerce is projected to play a key role, as more consumers embrace online shopping. Sustainability and the rise of local fashion designers are also expected to be important trends shaping the market, with modest fashion continuing to dominate. The growing emphasis on fashion technology, including virtual reality and AI-driven personalized experiences, will further transform the fashion landscape in KSA.

Market Opportunities

- Local Fashion Designers (Emerging Fashion Talent): The rise of local fashion designers represents a key opportunity for the Saudi fashion market. In 2023, Saudi Arabia hosted the second edition of Fashion Futures, a global fashion forum aimed at promoting local talent. The government has also launched initiatives to support emerging designers, such as the "Fashion Incubator" program, which provides mentorship and funding to young Saudi designers. As local designers gain international recognition, the export of Saudi fashion products is projected to rise, positioning the Kingdom as a hub for Middle Eastern fashion talent.

- Sustainability in Fashion (Eco-Friendly Apparel Demand): Demand for sustainable fashion is growing in Saudi Arabia, aligning with global trends. In 2023, approximately 35% of Saudi consumers indicated a preference for eco-friendly apparel, particularly among younger demographics. This shift has prompted brands like Adidas and Stella McCartney to introduce sustainable collections in the Saudi market. Local brands are also capitalizing on this trend, with several Saudi designers using eco-friendly materials like organic cotton and recycled fabrics. As environmental awareness increases, sustainability is expected to become a key differentiator for fashion brands in the Kingdom.

Scope of the Report

|

By Product Type |

Apparel (Casual Wear, Formal Wear, Traditional Wear, Sportswear) |

|

Footwear (Sports Shoes, Casual Shoes, Formal Shoes, Traditional Footwear) |

|

|

Accessories (Bags, Watches, Jewelry, Eyewear) |

|

|

By Consumer Group |

Men Women Children |

|

By Distribution Channel |

Online Retail (E-Commerce, Brand Websites) |

|

Offline Retail (Department Stores, Boutiques, Hypermarkets) |

|

|

By Price Range |

Mass Market Premium Market Luxury Market |

|

By Region |

Riyadh Jeddah Dammam Mecca and Medina Rest of KSA |

Products

Key Target Audience

- Fashion Retailers and Distributors

- Local Fashion Designers

- E-Commerce Platforms

- Luxury Brands and Boutiques

- Investment and Venture Capitalist Firms

- Government and Regulatory Bodies (Ministry of Commerce, Saudi Customs)

- Modest Fashion Manufacturers

- Footwear and Accessories Producers

Time Period Captured in the Report:

- Historical Period: 2018-2023

- Base Year: 2023

- Forecast Period: 2023-2028

Companies

- Femi9

- Zara (Inditex Group)

- Max Fashion (Landmark Group)

- Louis Vuitton

- Gucci

- Dolce & Gabbana

- H&M Group

- Mango

- Splash Fashions

- Nike Inc.

- Adidas A

- Burberry Group

- Modanisa

- Alhannah Islamic Clothing

- Saudi Fashion House

Table of Contents

1. KSA Fashion Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Key Market Indicators and Metrics

1.4. Overview of Fashion Consumption Patterns

1.5. Evolution of the Fashion Ecosystem in KSA

2. KSA Fashion Market Size (In USD Bn)

2.1. Historical Market Size (Market Value in USD, CAGR)

2.2. Year-On-Year Growth Analysis (Apparel, Footwear, Accessories)

2.3. Key Market Developments and Milestones (Key Growth Milestones)

3. KSA Fashion Market Analysis

3.1. Growth Drivers

3.1.1. Government Initiatives (Vision 2030 Impact)

3.1.2. Rise of E-Commerce (Online Retail Adoption)

3.1.3. Changing Consumer Preferences (Influence of Western Trends)

3.1.4. Increase in Disposable Income (Impact on Luxury Fashion)

3.2. Market Challenges

3.2.1. High Competition from International Brands

3.2.2. Supply Chain Disruptions (Logistics Challenges)

3.2.3. Cultural Barriers in Fashion Preferences

3.2.4. Impact of Global Economic Uncertainties

3.3. Opportunities

3.3.1. Local Fashion Designers (Emerging Fashion Talent)

3.3.2. Sustainability in Fashion (Eco-Friendly Apparel Demand)

3.3.3. Growth of Modest Fashion Segment

3.3.4. Integration of Technology in Fashion Retail (Virtual Fitting, AI-based Recommendations)

3.4. Trends

3.4.1. Rise in Demand for Modest Fashion

3.4.2. Increasing Influence of Social Media Fashion Influencers

3.4.3. Rise in Rental Fashion Services

3.4.4. Fashion-Tech Integration (Smart Fabrics, 3D Printing)

3.5. Government Regulations

3.5.1. Import Duties on Foreign Fashion Products

3.5.2. Nationalization of Retail Workforce Policies (Saudization Impact)

3.5.3. Intellectual Property Rights in Fashion

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Retailers, Designers, Distributors)

3.8. Porter’s Five Forces Analysis

3.9. Competitive Ecosystem (Local vs International Brands)

4. KSA Fashion Market Segmentation (In Value %)

4.1. By Product Type

4.1.1. Apparel (Casual Wear, Formal Wear, Traditional Wear, Sportswear)

4.1.2. Footwear (Sports Shoes, Casual Shoes, Formal Shoes, Traditional Footwear)

4.1.3. Accessories (Bags, Watches, Jewelry, Eyewear)

4.2. By Consumer Group

4.2.1. Men

4.2.2. Women

4.2.3. Children

4.3. By Distribution Channel

4.3.1. Online Retail (E-Commerce, Brand Websites)

4.3.2. Offline Retail (Department Stores, Boutiques, Hypermarkets)

4.4. By Price Range

4.4.1. Mass Market

4.4.2. Premium Market

4.4.3. Luxury Market

4.5. By Region

4.5.1. Riyadh

4.5.2. Jeddah

4.5.3. Dammam

4.5.4. Mecca and Medina

4.5.5. Rest of KSA

5. KSA Fashion Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Saudi Fashion House

5.1.2. Zara (Inditex Group)

5.1.3. H&M Group

5.1.4. Femi9

5.1.5. Max Fashion (Landmark Group)

5.1.6. Alhannah Islamic Clothing

5.1.7. Modanisa

5.1.8. Louis Vuitton

5.1.9. Nike Inc.

5.1.10. Adidas AG

5.1.11. Dolce & Gabbana

5.1.12. Gucci

5.1.13. Burberry Group

5.1.14. Mango

5.1.15. Splash Fashions

5.2. Cross Comparison Parameters (Revenue, Store Count, Market Share, Target Consumer)

5.3. Market Share Analysis

5.4. Strategic Initiatives (New Store Openings, E-Commerce Expansion)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Funding, Partnerships)

5.7. Venture Capital Funding in the Fashion Sector

5.8. Private Equity Investments

5.9. Government Grants for Fashion Industry

6. KSA Fashion Market Regulatory Framework

6.1. Trade Regulations for Fashion Imports

6.2. Compliance with Local Cultural Norms

6.3. Certification and Labeling Requirements

7. KSA Fashion Future Market Size (In USD Bn)

7.1. Market Size Projections

7.2. Key Factors Influencing Future Market Growth

8. KSA Fashion Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Consumer Group (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By Price Range (In Value %)

8.5. By Region (In Value %)

9. KSA Fashion Market Analyst's Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Retail Expansion Strategies

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The research begins with identifying key variables that shape the KSA fashion market, including product demand trends, distribution channels, and consumer preferences. Data is collected through an extensive review of market reports and proprietary databases.

Step 2: Market Analysis and Construction

Using historical data from credible sources, the market is analyzed to assess past performance. This phase includes reviewing the penetration rates of luxury and mass-market segments and evaluating the influence of e-commerce on overall market growth.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are constructed based on the data collected. These are validated through direct consultations with key market stakeholders, including fashion retailers, designers, and government bodies, providing firsthand insights into market dynamics.

Step 4: Research Synthesis and Final Output

All data gathered through primary and secondary research is synthesized into a comprehensive market report. This final output includes validated figures for market size, segmentation analysis, and competitive dynamics, ensuring accuracy and reliability.

Frequently Asked Questions

01. How big is the KSA Fashion Market?

The KSA fashion market size by revenue USD 4.30 billion, primarily driven by a rise in online shopping, luxury fashion demand, and government support for retail expansion under Vision 2030.

02. What are the challenges in the KSA Fashion Market?

Key challenges include stiff competition from international brands, supply chain disruptions due to the pandemic, and adapting to the evolving tastes of KSA consumers, especially in terms of modest fashion preferences.

03. Who are the major players in the KSA Fashion Market?

Major players include Femi9, Zara (Inditex Group), Max Fashion, Louis Vuitton, and Gucci. These brands dominate the market with their wide distribution networks and appeal to both mass and luxury consumer segments.

04. What are the growth drivers of the KSA Fashion Market?

Growth is driven by government initiatives under Vision 2030, the rise of online shopping, increasing disposable income, and a growing demand for luxury fashion, especially among the urban population in cities like Riyadh and Jeddah.

|

Product Type |

Market Share (2023) |

|

Apparel |

48% |

|

Footwear |

28% |

|

Accessories |

24% |

|

Distribution Channel |

Market Share (2023) |

|

Online Retail |

35% |

|

Offline Retail |

65% |

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.