KSA Feminine Hygiene Market Outlook to 2030

Region:Middle East

Author(s):Shambhavi Awasthi

Product Code:KROD2423

December 2024

86

About the Report

KSA Feminine Hygiene Market Overview

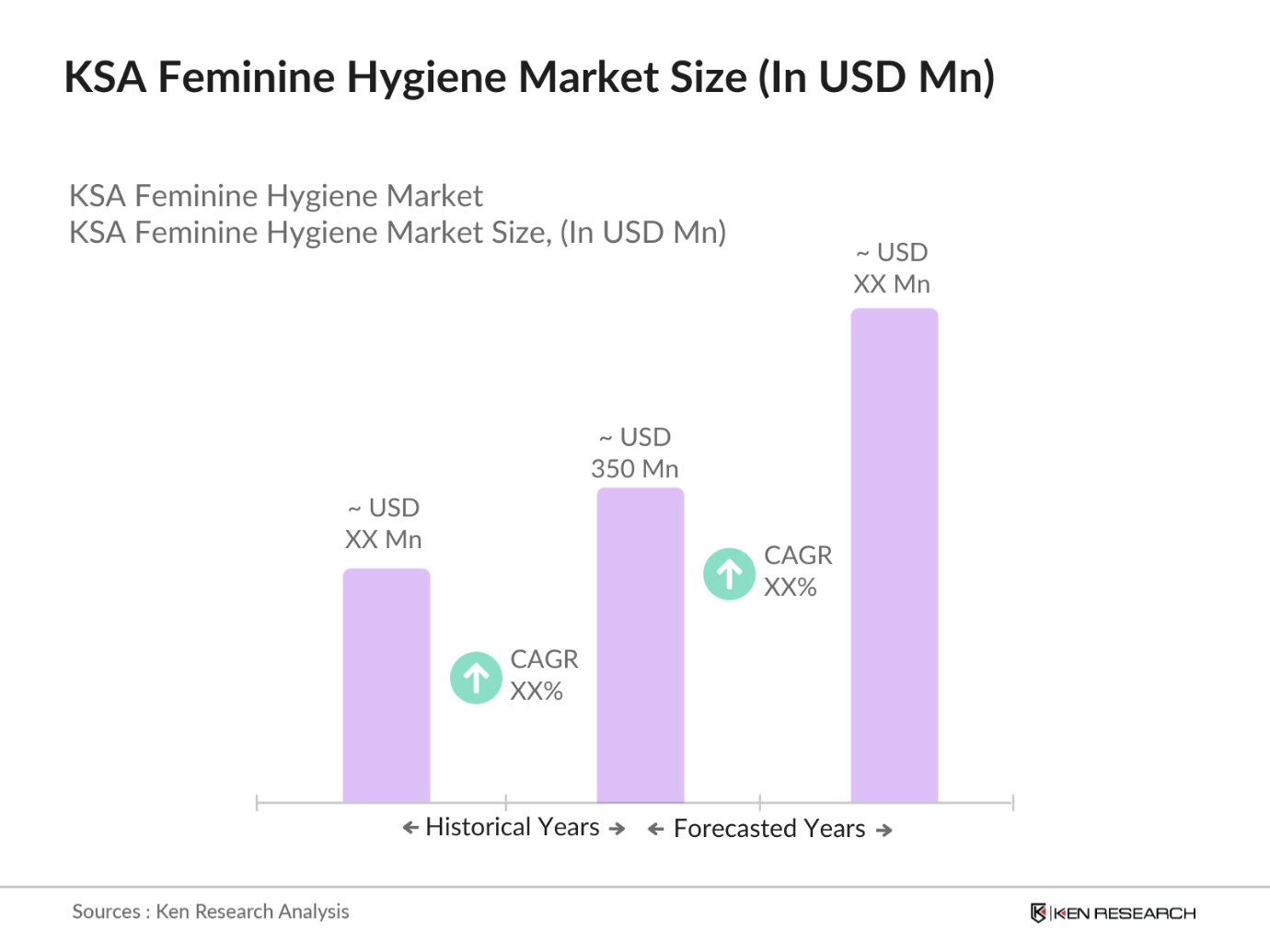

- The Saudi Arabian (KSA) feminine hygiene market in 2023 is valued at USD 350 million. The market's expansion is driven by increased consumer awareness regarding feminine health and hygiene, alongside urbanization and the growing disposable income of women. Rising education levels and increased participation of women in the workforce further stimulate demand for various feminine hygiene products, from sanitary pads to tampons and menstrual cups.

- Prominent players in the KSA feminine hygiene market include global and regional companies like Procter & Gamble, Kimberly-Clark, Johnson & Johnson, Unicharm, and Lil-Lets Group. These companies dominate the market by offering a wide range of products such as sanitary napkins, tampons, panty liners, and menstrual cups. Procter & Gambles "Always" and Kimberly-Clarks "Kotex" are particularly popular due to their extensive marketing and distribution network across KSA, ensuring accessibility in both urban and rural areas.

- In 2023, the Saudi government continued its efforts toward female empowerment through initiatives like Tamkeen, which focuses on improving womens access to basic health necessities, including hygiene products. Subsidized programs have been implemented in schools across Riyadh and Jeddah to provide free menstrual hygiene products to girls, a development that is expected to boost demand significantly. Furthermore, the Ministry of Health launched awareness campaigns promoting menstrual health education in early 2024.

- Major cities such as Riyadh, Jeddah, and Dammam dominate the feminine hygiene market due to higher population density, better healthcare infrastructure, and a larger share of working women. These cities also host the majority of retail and e-commerce platforms where feminine hygiene products are readily accessible. Moreover, women in these cities have higher disposable incomes, allowing them to opt for premium hygiene products, contributing to market growth.

KSA Feminine Hygiene Market Segmentation

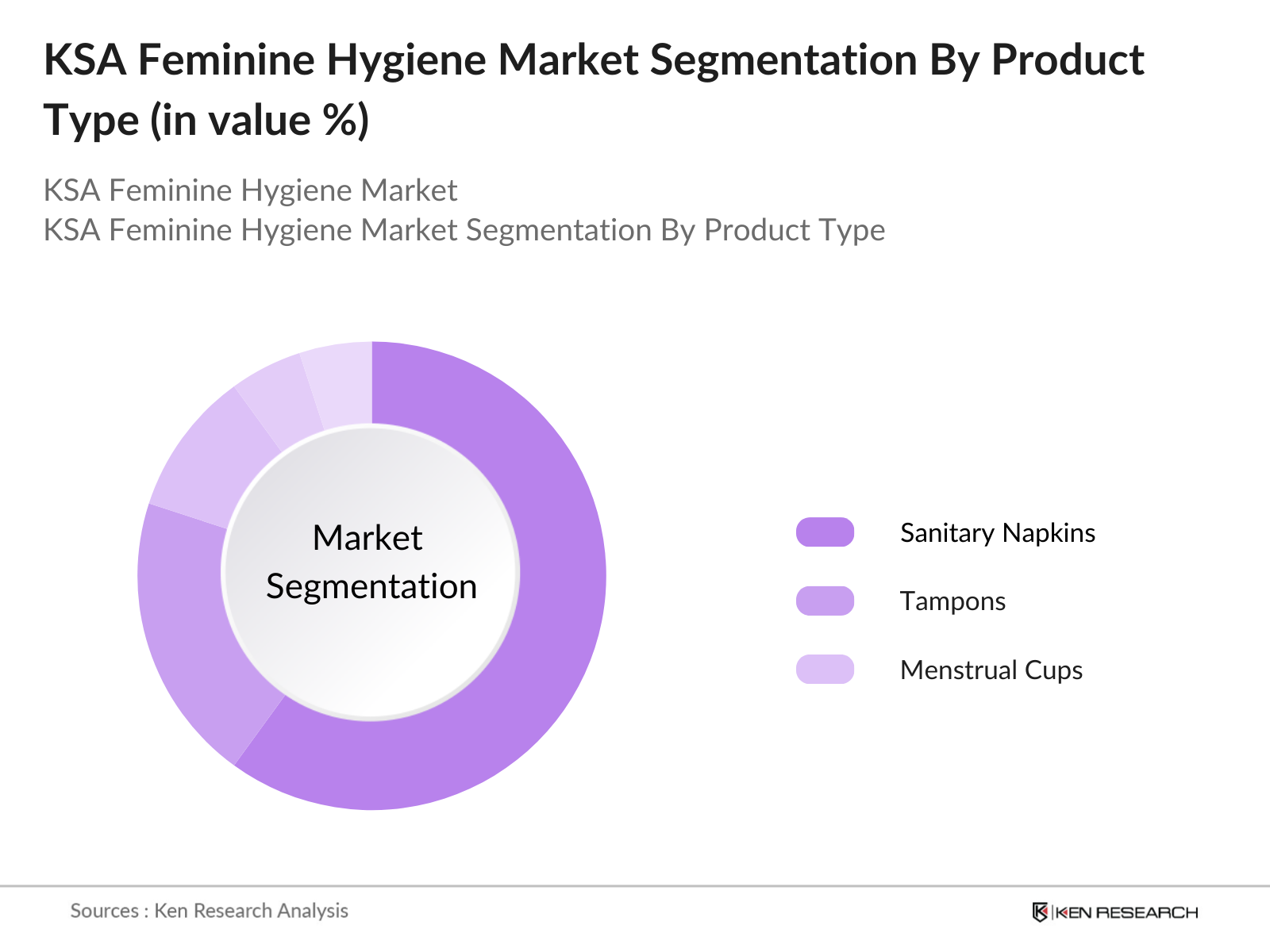

By Product Type: The KSA feminine hygiene market is segmented by product type into sanitary napkins, tampons, and menstrual cups. In 2023, sanitary napkins held the dominant market share. This dominance is attributed to the product's widespread use across all demographics, its convenience, and the continued cultural preference for sanitary napkins over other products like tampons or menstrual cups. Moreover, large-scale awareness campaigns have boosted the sales of sanitary napkins among younger girls and women.

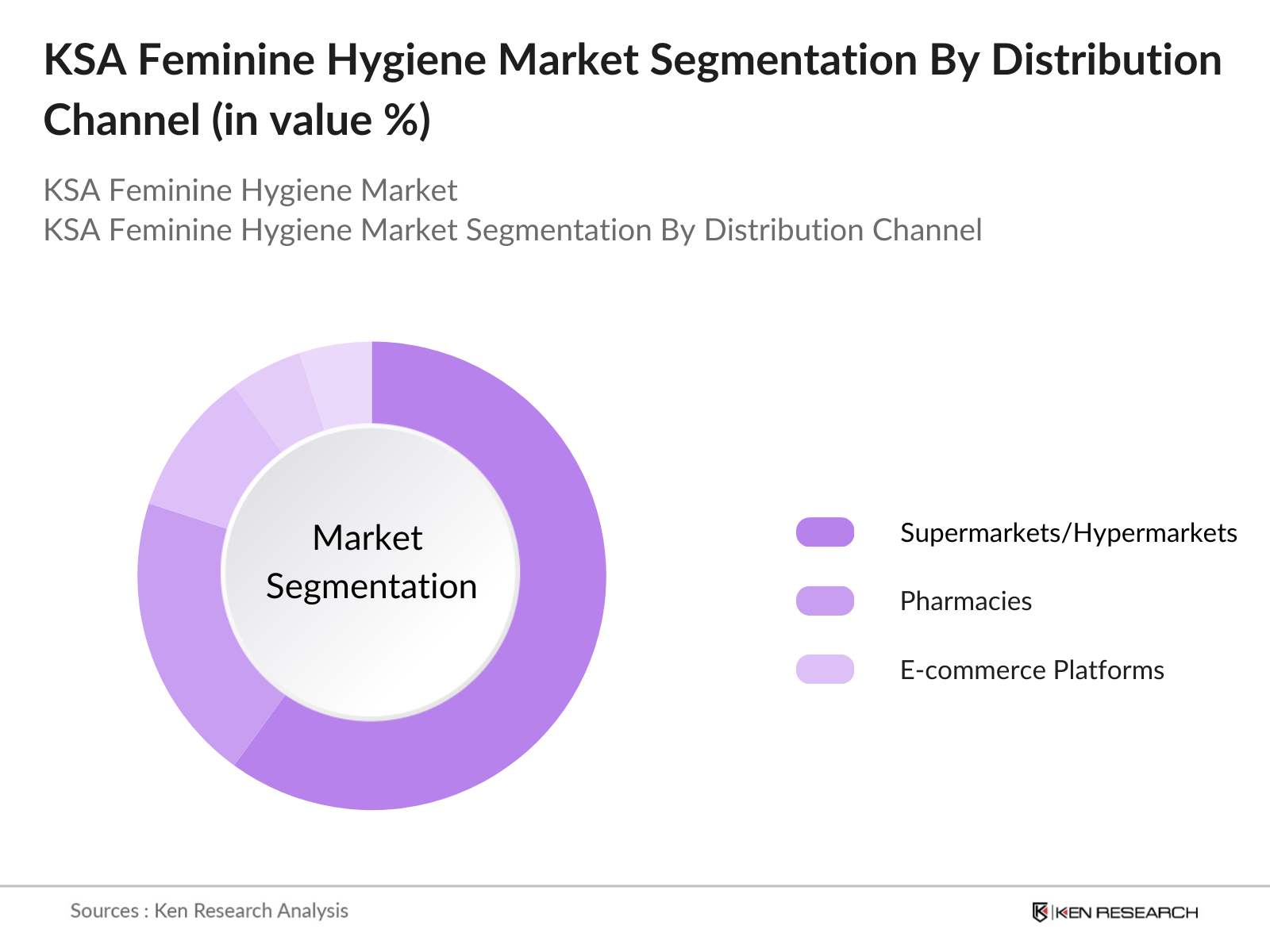

By Distribution Channel: The distribution of feminine hygiene products in KSA is segmented into supermarkets and hypermarkets, pharmacies, and e-commerce platforms. In 2023, supermarkets and hypermarkets dominated the market share. This is primarily because these outlets offer an array of products under one roof, and consumers prefer buying hygiene products during routine shopping trips. Furthermore, supermarkets frequently run promotions, which attract price-sensitive customers, contributing to their dominance.

By Region: The feminine hygiene market in KSA is regionally segmented into Central, Western, Eastern, Northern and Southern regions. In 2023, the Western region holds the largest market share. This dominance is attributed to the region's high population density, increased urbanization, and the presence of major cities like Jeddah. Additionally, the Western region benefits from better access to healthcare facilities and education, which has led to heightened awareness and adoption of feminine hygiene products.

KSA Feminine Hygiene Market Competitive Landscape

|

Company |

Establishment Year |

Headquarters |

|

Procter & Gamble |

1837 |

Cincinnati, USA |

|

Kimberly-Clark |

1872 |

Irving, USA |

|

Johnson & Johnson |

1886 |

New Brunswick, USA |

|

Unicharm |

1961 |

Tokyo, Japan |

|

Lil-Lets Group |

1954 |

Birmingham, UK |

- Procter & Gamble: In 2023, Procter & Gamble announced a new partnership with the Saudi Ministry of Health to launch educational campaigns across the nation, emphasizing menstrual hygiene. The company also introduced biodegradable packaging for its Always brand, which has been a hit in Jeddahs eco-conscious market. Furthermore, P&G invested USD 20 million in expanding its distribution networks within KSA, particularly focusing on rural areas to boost product availability.

- Kimberly-Clark: Kimberly-Clark, with its popular Kotex brand, reported an increase in sales in 2023, driven by its strategic partnership with local e-commerce platforms. The company has also introduced innovative tampon and panty liner products tailored to the needs of Saudi women. In 2024, Kimberly-Clark plans to expand its product offerings in the kingdom, focusing on eco-friendly solutions in alignment with KSAs growing interest in sustainable living.

KSA Feminine Hygiene Market Analysis

Growth Drivers

- Increased Female Labor Participation (2021-2024)

The Saudi governments Vision 2030 plan has actively pushed for greater female labor participation. In 2024, female labor force participation reached 34.5%, compared to 19.4% in 2021. This shift has directly impacted the feminine hygiene market as more working women prioritize personal hygiene products due to their active lifestyles. A 2023 report from the General Authority for Statistics (GASTAT) highlighted that working women in KSA have increased their spending on sanitary napkins and tampons by 10% annually from 2021 to 2024. - Rising Population of Women in Urban Centers (2021-2024)

The number of women residing in Saudi Arabias urban centers, particularly in cities like Riyadh and Jeddah, grew by 1.2 million between 2021 and 2024. The increasing urbanization is driven by employment opportunities and better healthcare access, which has, in turn, led to higher consumption of feminine hygiene products. The GASTAT data for 2024 also indicates a 6% annual rise in feminine hygiene product sales in urban retail stores, significantly contributing to the market's growth. - Government Healthcare Spending (2021-2024)

The Saudi government allocated SAR 180 billion for healthcare in 2024, an increase from SAR 140 billion in 2021. This increased expenditure includes a focus on womens health, with the introduction of programs like the National Health Transformation Program (2022) which improved access to affordable feminine hygiene products in government-run healthcare facilities. The program has made feminine hygiene products available in 85% of hospitals and clinics across the Kingdom, increasing product usage among women of all income levels.

Challenges

- Cultural Taboo and Stigma (2021-2024)

Despite advancements in education and healthcare, discussing menstrual health remains stigmatized in certain conservative regions of Saudi Arabia. This cultural barrier has hindered the broader adoption of feminine hygiene products, particularly in rural areas. A 2024 study by the Saudi Ministry of Health revealed that 35% of women in rural regions still relied on traditional menstrual management methods, limiting market penetration for modern feminine hygiene products. - High Costs of Premium Products (2021-2024)

Premium feminine hygiene products, such as organic tampons and menstrual cups, have seen slow adoption due to their higher prices. In 2024, a report by the Saudi Consumer Protection Authority revealed that only 15% of consumers in Saudi Arabia are opting for these premium products, as they are often twice as expensive as standard sanitary napkins. This cost barrier has limited the market growth for these eco-friendly products despite growing awareness of their environmental benefits.

Government Initiatives (2021-2025)

- Womens Health Empowerment Program (2023)

Launched by the Saudi Ministry of Health in 2023, this program focuses on improving access to menstrual hygiene products in schools and universities. The initiative has distributed over 3 million sanitary napkins across 5,000 educational institutions in its first year. The program also includes menstrual health education workshops for students and aims to normalize discussions about menstruation, thereby reducing stigma in the long term. - National Health Transformation Program (2022)

As part of Vision 2030, the National Health Transformation Program, initiated in 2022, aims to improve healthcare access across all regions of Saudi Arabia. This includes subsidies for essential healthcare products, such as feminine hygiene items, in public healthcare facilities. By the end of 2024, over 85% of hospitals had made basic feminine hygiene products, including sanitary napkins, freely available, contributing to a wider market reach.

KSA Feminine Hygiene Market Future Outlook

The KSA feminine hygiene market is expected to witness substantial growth over the next five years, driven by rising awareness of menstrual health and ongoing governmental support. Saudi Arabias Vision 2030 is set to further empower women economically, leading to increased spending on personal hygiene products. Furthermore, with a younger population becoming more health-conscious and the government rolling out more healthcare initiatives, the market is likely to experience steady growth until 2028. The focus on sustainability and eco-friendly products will also play a crucial role in shaping consumer preferences in the coming years.

Future Trends

- Sustainability in Product Offerings

In the future, the KSA feminine hygiene market will witness a shift towards eco-friendly products such as biodegradable sanitary napkins, organic tampons, and menstrual cups. Companies will focus on reducing their environmental impact by offering sustainable alternatives, catering to the growing demand from eco-conscious consumers in urban regions. - Digital Health Solutions

The integration of digital health platforms will enhance the accessibility of menstrual health information. App-based solutions that track menstrual cycles and provide personalized health insights are expected to grow in popularity. By 2028, digital health solutions will become mainstream, with companies partnering with healthcare providers to offer holistic menstrual health care.

Scope of the Report

|

By Product Type |

Sanitary Napkins Tampons Menstrual Cups Panty Liners |

|

By Distribution Channel |

Supermarkets and Hypermarkets Pharmacies E-commerce Platforms Direct Sales |

|

By Age Group |

Adolescents (10-19 years) Young Adults (20-30 years Middle-aged Women (31-45 years) Older Women (46+ years) |

|

By Material Type |

Conventional Materials (Synthetic, Non-woven) Organic Cotton Biodegradable Materials |

|

By Region |

Western Region Central Region Eastern Region Northern and Southern Regions |

|

By Product Type |

Sanitary Napkins Tampons Menstrual Cups Panty Liners |

Products

Key Target Audience

Feminine Hygiene Product Manufacturers

Retail Chains (Carrefour, Panda, Lulu Hypermarket)

E-commerce Platforms (Noon, Amazon KSA)

Pharmaceutical Distributors

Non-Governmental Organizations (NGOs)

Female Health Clinics and Hospitals

Educational Institutions (specifically for womens health programs)

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (Saudi Ministry of Health, General Authority for Statistics)

Major Market Players

Procter & Gamble

Kimberly-Clark

Unicharm

Johnson & Johnson

Lil-Lets Group

Bella Hygiene

Always

Carefree

Kotex

Tampax

Saba

Naturalena Brands

Edgewell Personal Care

Sanita

Hospeco

Table of Contents

1. Saudi Arabia Feminine Hygiene Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Feminine Hygiene Market Ecosystem

1.4. Market Growth Rate

1.5. Market Segmentation Overview (by Product Type, Distribution Channel, Age Group, Material Type, and Region)

2. Saudi Arabia Feminine Hygiene Market Size (in USD billion)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones (financial and operational metrics)

2.4. Market Demand Trends (based on demographics, region, and product preferences)

2.5. Contribution of Domestic and Imported Products to Market Size

3. Saudi Arabia Feminine Hygiene Market Analysis

3.1. Growth Drivers

3.1.1. Increased Female Workforce Participation

3.1.2. Growing Awareness on Feminine Hygiene

3.1.3. Government Support and Initiatives

3.2. Restraints

3.2.1. Cultural Sensitivities in Rural Areas

3.2.2. High Cost of Premium Products

3.2.3. Dependence on Imported Products and Supply Chain Issues

3.3. Opportunities

3.3.1. Sustainable and Biodegradable Feminine Products

3.3.2. Expansion into Rural and Underdeveloped Regions

3.3.3. Growth of E-commerce for Hygiene Products

3.4. Trends

3.4.1. Rising Demand for Organic and Natural Products

3.4.2. Shift Towards Menstrual Cups and Reusable Products

3.4.3. Increased Focus on Digital Marketing and E-commerce

3.5. Government Regulations

3.5.1. Vision 2030: Women Empowerment and Health Focus

3.5.2. National Health Transformation Program and Impact on Market

3.5.3. Subsidies on Basic Feminine Hygiene Products in Public Institutions

3.6. SWOT Analysis (financial, operational, regulatory)

3.7. Stakeholder Ecosystem

3.8. Competitive Ecosystem (market share analysis and financial performance)

4. Saudi Arabia Feminine Hygiene Market Segmentation

4.1. By Product Type (in Value %) 4.1.1. Sanitary Napkins

4.1.2. Tampons

4.1.3. Menstrual Cups

4.1.4. Panty Liners

4.2. By Distribution Channel (in Value %) 4.2.1. Supermarkets and Hypermarkets

4.2.2. Pharmacies

4.2.3. E-commerce Platforms

4.2.4. Direct Sales

4.3. By Age Group (in Value %) 4.3.1. Adolescents (10-19 years)

4.3.2. Young Adults (20-30 years)

4.3.3. Middle-aged Women (31-45 years)

4.3.4. Older Women (46+ years)

4.4. By Material Type (in Value %) 4.4.1. Conventional Materials (Synthetic, Non-woven)

4.4.2. Organic Cotton

4.4.3. Biodegradable Materials

4.5. By Region (in Value %)

4.5.1. Western

4.5.2. Central

4.5.3. Eastern

4.5.4. Northern

4.5.5 Southern

5. Saudi Arabia Feminine Hygiene Market Cross Comparison

5.1. Detailed Profiles of Major Companies (financial and operational parameters)

5.1.1. Procter & Gamble

5.1.2. Kimberly-Clark

5.1.3. Unicharm

5.1.4. Johnson & Johnson

5.1.5. Lil-Lets Group

5.1.6. Bella Hygiene

5.1.7. Always

5.1.8. Carefree

5.1.9. Kotex

5.1.10. Saba

5.1.11. Tampax

5.1.12. Naturalena Brands

5.1.13. Hospeco

5.1.14. Sanita

5.1.15. Edgewell Personal Care

5.2. Cross Comparison Parameters (number of employees, headquarters, inception year, revenue)

6. Saudi Arabia Feminine Hygiene Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives by Key Players

6.3. Mergers, Acquisitions, and Partnerships

6.4. Investment Analysis

6.4.1. Venture Capital Funding in Feminine Hygiene Startups

6.4.2. Government Grants for Local Manufacturing

6.4.3. Private Equity Investments in Sustainable Product Lines

7. Saudi Arabia Feminine Hygiene Market Regulatory Framework

7.1. Health and Safety Standards for Feminine Hygiene Products

7.2. Compliance and Certification Processes

7.3. Government Subsidies and Price Controls

7.4. Import Tariffs and Domestic Manufacturing Incentives

8. Saudi Arabia Feminine Hygiene Future Market Size (in USD billion)

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9. Saudi Arabia Feminine Hygiene Market Segmentation (Future Projections)

9.1. By Product Type (in Value %)

9.2. By Distribution Channel (in Value %)

9.3. By Age Group (in Value %)

9.4. By Material Type (in Value %)

9.5. By Region (in Value %)

10. Saudi Arabia Feminine Hygiene Market Analysts Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. White Space Opportunity Analysis

10.3. Consumer Behavior Insights

10.4. Key Marketing Strategies and Positioning

10.5. Risk Mitigation and Contingency Plans

Frequently Asked Questions

01. How big is the Saudi Arabia Feminine Hygiene Market?

The Saudi Arabia feminine hygiene market was valued at USD 350 million in 2023, driven by increased awareness, government initiatives, and rising female workforce participation across the Kingdom.

02. What are the challenges in the Saudi Arabia Feminine Hygiene Market?

The market faces cultural stigmas around menstruation, high costs of premium products, and supply chain challenges due to import dependencies. Additionally, slow adoption of sustainable products has hindered market growth in rural regions.

03. Who are the major players in the Saudi Arabia Feminine Hygiene Market?

Key players in the market include Procter & Gamble, Kimberly-Clark, Unicharm, Johnson & Johnson, and Lil-Lets Group, dominating with their extensive distribution networks, product diversity, and local manufacturing capacities.

04. What are the growth drivers of the Saudi Arabia Feminine Hygiene Market?

Key drivers include the increasing participation of women in the workforce, urbanization, and growing awareness about menstrual hygiene due to government initiatives. There is also a rising trend towards sustainable and eco-friendly products.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.