KSA Food and Beverage Market Outlook to 2030

Region:Saudi Arabia

Author(s):Abhinav Kumar

Product Code:KROD1259

Region:Saudi Arabia

Author(s):Abhinav Kumar

Product Code:KROD1259

January 2025

89

The KSA Food and Beverage Market can be segmented by various factors such as Product Type, Distribution Channel, and Region.

By Product Type: The KSA Food and Beverage Market is segmented by product type into dairy products, bakery products, and beverages. In 2023, dairy products dominated this subsegment due to the strong demand for milk, cheese, and yogurt, driven by traditional dietary preferences and increasing health awareness among consumers.

By Distribution Channel: The market is also segmented by distribution channel into Supermarkets and Hypermarkets, Convenience Stores, and Online Retail. In 2023, Supermarkets and Hypermarkets held the dominant share, attributed to their extensive reach, wide product range, and the growing trend of one-stop shopping experiences. These large retail chains offer consumers the convenience of purchasing all their food and beverage needs under one roof.

By Region: The KSA Food and Beverage Market is segmented by region into North, South, East, and West. In 2023, the Western region held the largest market share due to its large population, significant number of tourists and pilgrims, and well-established food retail infrastructure. The presence of key market players and the region's role as a commercial hub also contribute to its dominance.

|

Company |

Establishment Year |

Headquarters |

|

Almarai |

1977 |

Riyadh |

|

Savola Group |

1979 |

Jeddah |

|

SADAFCO |

1976 |

Jeddah |

|

Nadec |

1981 |

Riyadh |

|

Albaik |

1974 |

Jeddah |

The KSA Food and Beverage Market is poised for substantial growth by 2028, propelled by continuous technological innovations and the strategic expansion of local food production initiatives.

|

By Product Type |

Dairy Products Bakery Products Beverages |

|

By Distribution Channel |

Supermarkets and Hypermarkets Convenience Stores Online Retail |

|

By Region |

North South East West |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Demand for Organic Products

3.1.2. Growth of E-commerce in Food and Beverage

3.1.3. Increased Health Awareness

3.1.4. Expansion of Food Service Outlets

3.2. Restraints

3.2.1. High Operational Costs

3.2.2. Regulatory Challenges

3.2.3. Supply Chain Disruptions

3.3.4 Fluctuating Raw Material Prices

3.3. Opportunities

3.3.1. Expansion in Organic Food Segment

3.3.2. Digitalization in Retail

3.3.3. Growth in E-commerce

3.4. Trends

3.4.1. Rise in Plant-Based Products

3.4.2. Popularity of Convenience Foods

3.4.3. Growth of Halal Food Market

3.5. Government Regulation

3.5.1. Food Safety Standards

3.5.2. Import Tariffs and Duties

3.5.3. Subsidies and Incentives

3.5.4. Localization of Food Production

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Competition Ecosystem

4.1 By Product Type (in Value %)

4.1. Beverages

4.1.2. Dairy Products

4.1.3. Bakery and Confectionery

4.1.4. Processed Foods

4.1.5. Others

4.2. By Distribution Channel (in Value %)

4.2.1. Supermarkets/Hypermarkets

4.2.2. Online Stores

4.2.3. Convenience Stores

4.2.4. Specialty Stores

4.2.5. Others

4.3. By Region (in Value %)

4.3.1. North

4.3.2. South

4.3.3. East

4.3.4. West

5.1 Detailed Profiles of Major Companies

5.1.1. Almarai

5.1.2. Savola Group

5.1.3. National Food Industries Co.

5.1.4. SADAFCO

5.1.5. Nestl Saudi Arabia

5.1.6. PepsiCo

5.1.7. Al Safi Danone

5.1.8. Nadec

5.1.9. Al Othaim

5.1.10. Herfy

5.1.11. Kraft Heinz Saudi Arabia

5.1.12. Coca-Cola Bottling Company Saudi Arabia

5.1.13. Al Rabie Saudi Foods Co. Ltd.

5.1.14. Gulf West Company

5.1.15. Basamh Trading Co. Ltd.

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7.1. Food Safety Regulations

7.2. Compliance Requirements

7.3. Certification Processes

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9.1. By Product Type (in Value %)

9.2. By Distribution Channel (in Value %)

9.3. By Region (in Value %)

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Disclaimer Contact UsEcosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Collating statistics on KSA food and beverage market over the years, penetration of marketplaces and service providers ratio to compute revenue generated for KSA food and beverage market. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Building market hypothesis and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple food and beverage suppliers and distributors to understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from food and beverage suppliers and distributors.

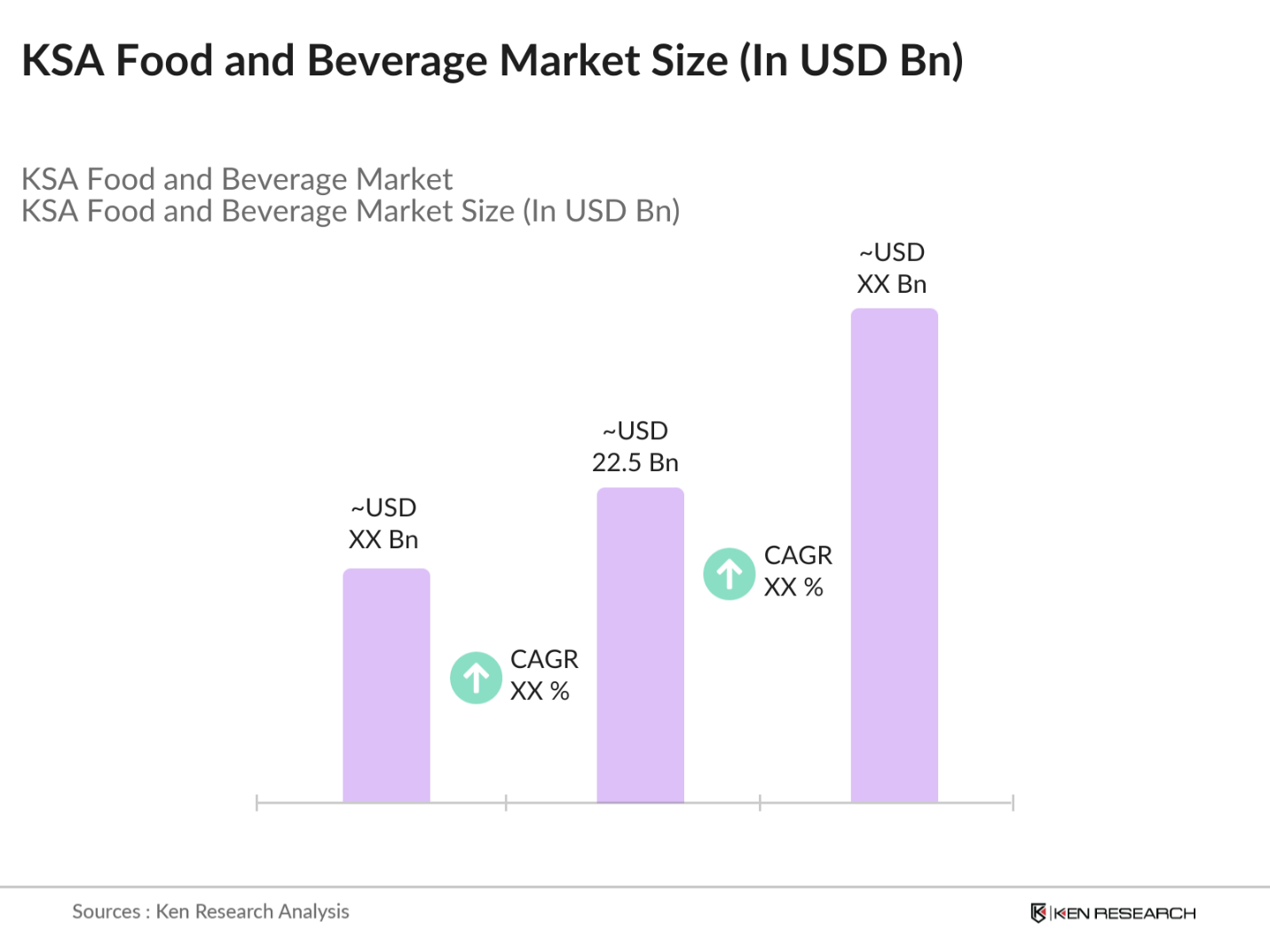

The KSA Food and Beverage market reached a valuation of USD 22.5 billion in 2023, driven by increasing urbanization, rising disposable incomes, and a growing preference for diverse and convenient food options. The market's robust growth is also supported by significant investments in food processing and retail infrastructure.

Key players in the market include Almarai, Savola Group, SADAFCO, Nadec, and Albaik, which dominate the market owing to their extensive distribution networks, strong brand presence, and diverse product portfolios.

The market is propelled by factors such as rising disposable incomes, increasing health awareness, and government initiatives like Vision 2030, aimed at boosting local food production and reducing reliance on imports.

The food and beverage market in Saudi Arabia faces challenges such as high costs of raw materials, infrastructure limitations, and dependence on imports for key ingredients, which necessitate strategic adjustments by organized players to navigate these challenges effectively.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.