KSA ICT Market Outlook to 2030

Region:Middle East

Author(s):Sanjeev

Product Code:KROD3840

October 2024

94

About the Report

Market Overview

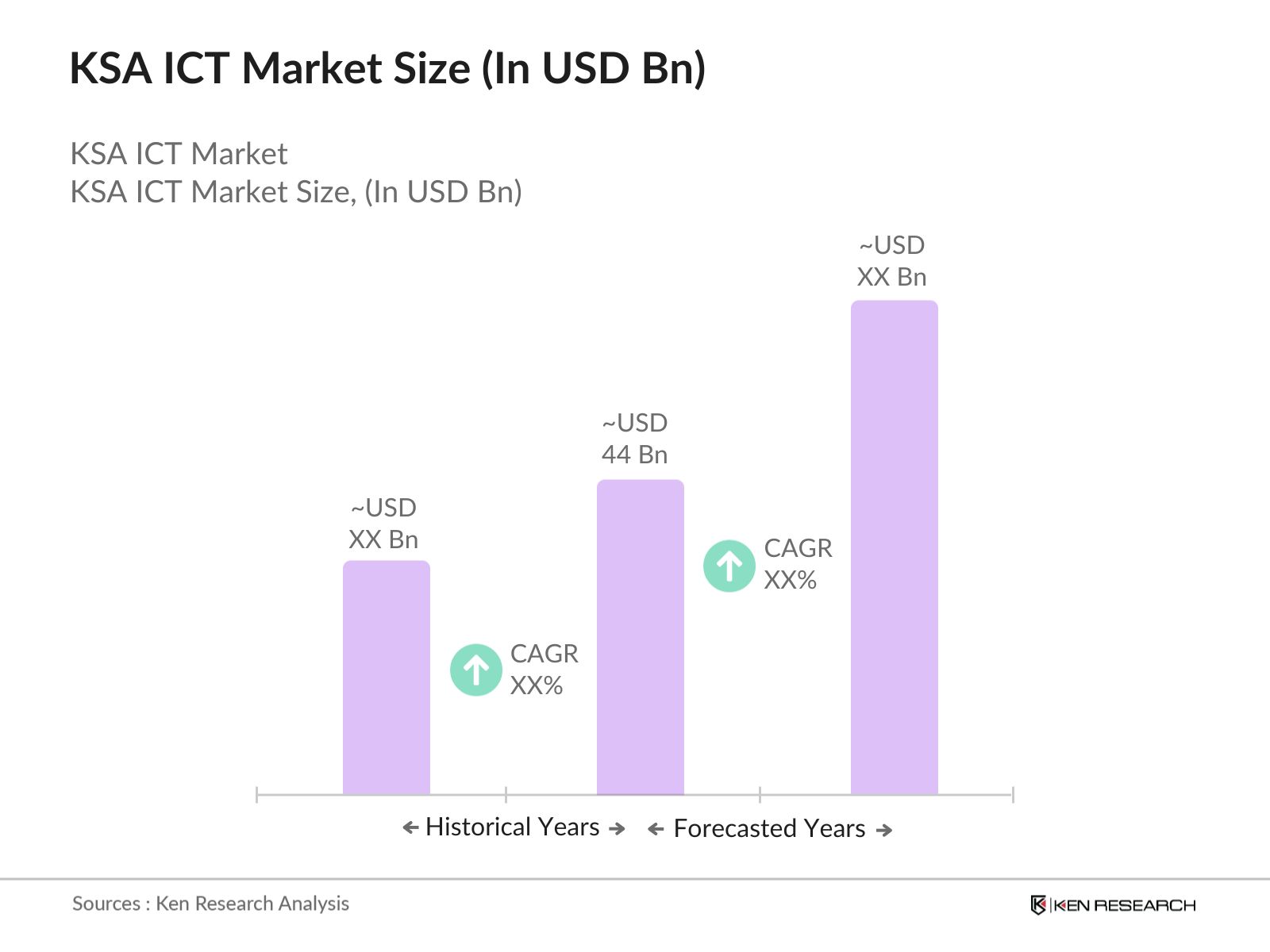

- The KSA ICT market is valued at USD 44 billion, driven by increasing investments in digital infrastructure, cloud computing, and 5G networks. Government initiatives such as Vision 2030 are key drivers, aiming to diversify the economy and reduce dependence on oil. The rapid adoption of IoT, AI, and smart city projects further fuels this market, with investments from both public and private sectors. Sources like the World Bank and the Saudi Ministry of Communications and Information Technology highlight the importance of ICT in transforming KSA into a digital economy.

- Riyadh and Jeddah are the dominant cities in the KSA ICT market. Riyadh, the capital, serves as the administrative and business hub, attracting massive ICT investments for government e-services and enterprise solutions. Jeddah, being a key commercial and trade center, sees strong demand for ICT services in the logistics, retail, and telecom sectors. Both cities benefit from advanced infrastructure and government support, making them the key drivers of ICT growth in the country.

- The National Cybersecurity Authority (NCA) in KSA has implemented stringent cybersecurity regulations to safeguard digital assets. By 2023, KSA had invested USD 1.5 billion in enhancing its cybersecurity framework. These regulations are critical for protecting sensitive data across industries such as finance, healthcare, and government services. Compliance with these regulations is expected to increase the demand for cybersecurity solutions by 2024.

KSA ICT Market Segmentation

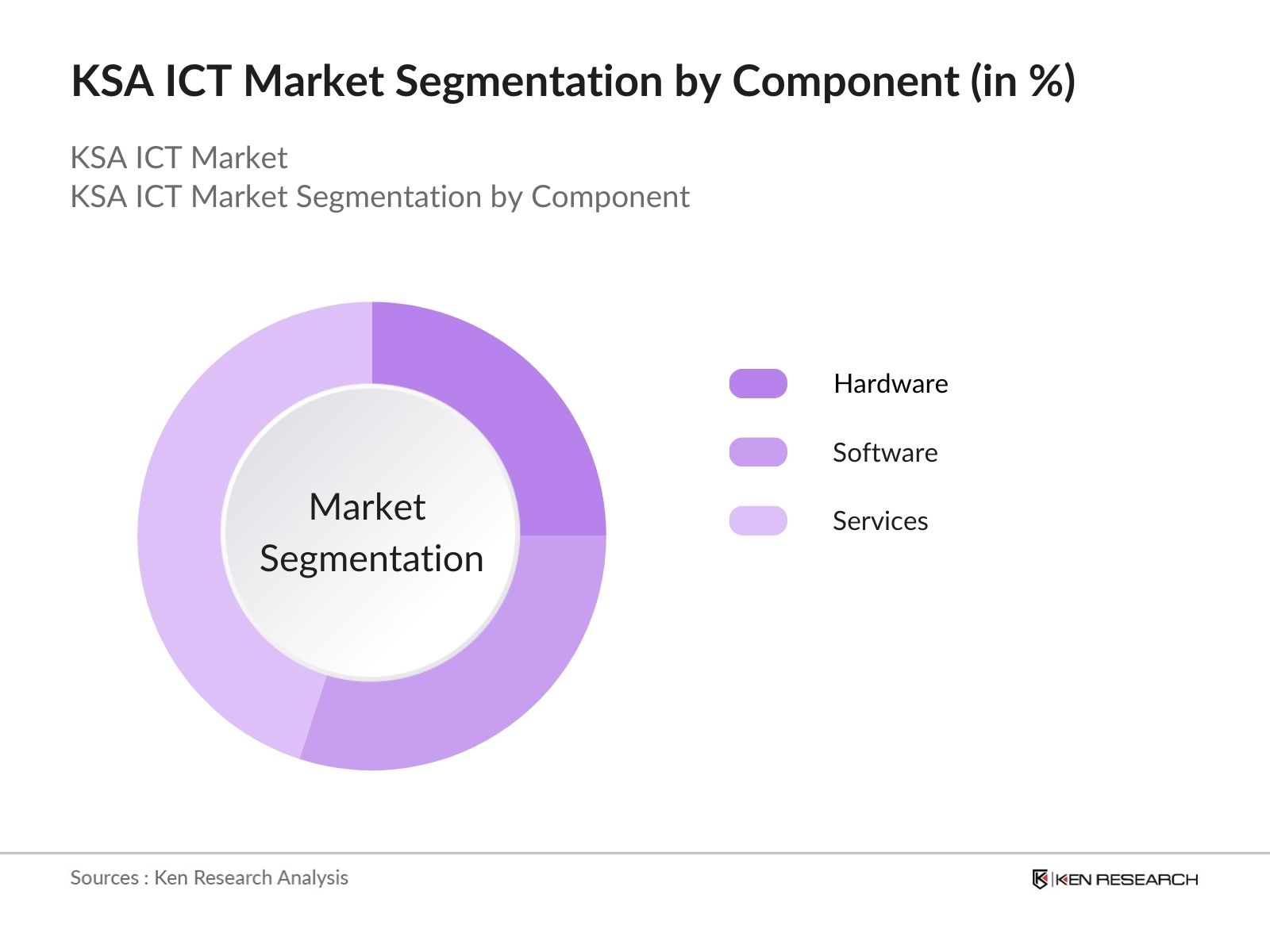

By Component: The market is segmented by component into hardware, software, and services. The services segment holds the dominant market share due to the growing demand for managed services, cloud solutions, and cybersecurity services. Government projects, especially in the public and smart city sectors, rely heavily on these services for implementation and management, driving their continued dominance.

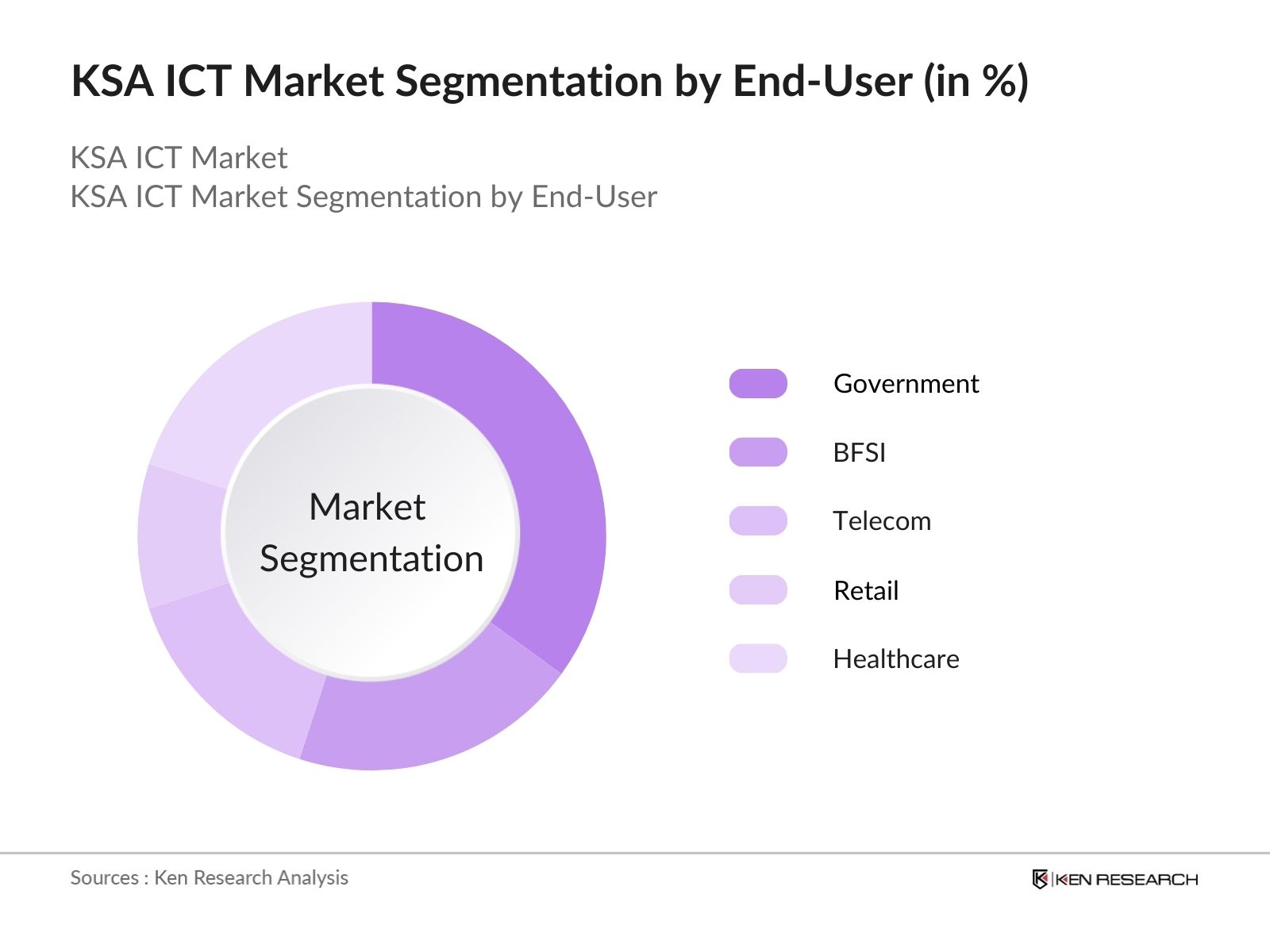

By End-User: The market is segmented by end-user into government, BFSI, telecom, healthcare, and retail. The government sector dominates the market, fueled by investments in e-government services, smart cities, and digital transformation under Vision 2030. The governments focus on building a digital infrastructure to support the economy drives the need for advanced ICT solutions in this segment.

KSA ICT Competitive Landscape

The KSA ICT market is highly competitive, with key players focusing on expanding their service portfolios and investing in cutting-edge technologies like AI, cloud computing, and cybersecurity. Leading companies such as Saudi Telecom Company (STC) and Mobily are at the forefront, benefiting from their established market presence and government contracts. International players like Microsoft and Cisco are also investing heavily in the region to expand their footprint.

Competitive Landscape Table

|

Company Name |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

No. of Employees |

Product Portfolio |

Market Segment Focus |

Strategic Partnerships |

|

STC (Saudi Telecom Co.) |

1998 |

Riyadh, KSA |

|||||

|

Mobily (Etihad Etisalat) |

2004 |

Riyadh, KSA |

|||||

|

Zain KSA |

2008 |

Riyadh, KSA |

|||||

|

Microsoft Corporation |

1975 |

Redmond, USA |

|||||

|

Cisco Systems Inc. |

1984 |

San Jose, USA |

KSA ICT Industry Analysis

Growth Drivers:

- 5G Network Expansion: The Kingdom of Saudi Arabia (KSA) has been rapidly expanding its 5G networks, aiming to cover 50 cities by the end of 2024. With over 15 million mobile internet users reported in 2023, 5G network rollouts are enhancing connectivity, enabling faster data transfer speeds. This expansion is a key part of the nations Vision 2030 goals to drive digital transformation and improve infrastructure for smart cities and digital services. According to the Ministry of Communications and Information Technology (MCIT), the investment in 5G infrastructure in 2024 has surpassed USD 3 billion.

- Digital Government Initiatives (Vision 2030): KSAs Vision 2030 aims to digitally transform the public sector through initiatives like the National Digital Transformation Program. As part of this strategy, government services are moving online, with more than 30% of public services already digitized by 2023. By 2024, the government is investing USD 12 billion to modernize its IT infrastructure and promote e-governance. This program is expected to accelerate growth in the ICT sector as more sectors, such as healthcare and education, become digitally integrated.

- Increase in Demand for E-Commerce: With over 28 million active internet users in KSA, the demand for e-commerce is surging. As of 2023, the online retail sector generated more than USD 7 billion, a number that is projected to increase due to growing mobile penetration and digital payment systems. KSAs ICT infrastructure is expanding to support this growth, particularly through investments in logistics and cloud-based platforms that ensure scalability and reliability for e-commerce platforms.

KSA ICT Market Challenges

High Initial Investment in ICT Infrastructure: The development of ICT infrastructure in KSA requires significant initial investments, posing a challenge for smaller enterprises to participate in the digital transformation. This cost burden affects the pace of private sector innovation due to high capital expenditure requirements. Despite ongoing government efforts, securing adequate infrastructure financing remains a challenge for many companies.

Lack of Local Skilled Workforce: KSAs ICT sector faces a shortage of local talent in advanced digital skills such as AI, cloud computing, and cybersecurity. While the government is making efforts to upskill local talent, the gap between the demand and supply of skilled workers continues to present a challenge for sustainable growth in the ICT sector.

KSA ICT Market Future Outlook

Over the next five years, the KSA ICT market is poised for remarkable growth, driven by the rapid adoption of digital services, the expansion of cloud and AI technologies, and the nationwide rollout of 5G networks. With continued government support under Vision 2030, KSA is expected to become a regional leader in ICT, with strong demand across sectors such as healthcare, retail, and education.

Market Opportunities

- High Initial Investment in ICT Infrastructure: The development of ICT infrastructure in KSA demands high initial investments, with over USD 15 billion allocated for 5G and data centers as of 2024. This cost burden limits smaller enterprises from fully participating in the digital transformation. According to the MCIT, this has raised concerns about the pace of private sector innovation due to high capital expenditure requirements. Despite government efforts, infrastructure financing remains a challenge for many companies.

- Lack of Local Skilled Workforce: KSAs ICT sector faces a shortage of local talent in advanced digital skills such as AI, cloud computing, and cybersecurity. The Human Resources Development Fund reports that by 2024, the demand for skilled workers in the ICT industry will exceed supply by 200,000 positions. The government has allocated USD 1.5 billion to upskill local talent, but the gap between demand and supply remains a challenge for sustainable ICT growth.

Scope of the Report

|

By Component |

Hardware Software Services |

|

By Deployment Model |

On-Premise Cloud-based Hybrid |

|

By End-User |

Government BFSI Telecom Retail Healthcare |

|

By Technology |

5G Cloud IoT AI Blockchain |

|

By Region |

North East West South |

Products

Key Target Audience

Government and Regulatory Bodies (Communications and Information Technology Commission, CITC)

Banks and Financial Institutes

Telecom Service Providers

Cloud and IT Infrastructure Providers

Cybersecurity Firms

Healthcare Providers

BFSI Industry Leaders

Data Center Operators

Investments and Venture Capitalist Firms

Companies

List of Major Players in KSA ICT Market

-

STC (Saudi Telecom Company)

Mobily (Etihad Etisalat)

Zain KSA

Microsoft Corporation

Cisco Systems Inc.

Oracle Corporation

IBM Corporation

Huawei Technologies Co. Ltd.

Amazon Web Services (AWS)

Google Cloud

SAP SE

Ericsson AB

Dell Technologies

Hewlett Packard Enterprise (HPE)

Accenture

Table of Contents

1. KSA ICT Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. KSA ICT Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. KSA ICT Market Analysis

3.1. Growth Drivers (Urbanization, Digital Transformation, Cloud Adoption)

3.1.1. Expansion of 5G Networks

3.1.2. Digital Government Initiatives (Vision 2030)

3.1.3. Increase in Demand for E-Commerce

3.1.4. Technological Advancements in AI and IoT

3.2. Market Challenges (Infrastructure, Investment Costs, Cybersecurity)

3.2.1. High Initial Investment in ICT Infrastructure

3.2.2. Lack of Local Skilled Workforce

3.2.3. Regulatory and Compliance Hurdles

3.3. Opportunities (Cloud Computing, Data Centers, AI Integration)

3.3.1. Expansion of Cloud and Edge Computing Services

3.3.2. Growing Demand for Data Center Infrastructure

3.3.3. Adoption of AI, Big Data, and Analytics in Business Sectors

3.4. Trends (Digital Economy, AI & Automation)

3.4.1. Rise of Smart City Projects

3.4.2. Increased Use of Artificial Intelligence in Various Sectors

3.4.3. Growth of Fintech and Digital Payment Solutions

3.4.4. IoT Integration Across Industries (Healthcare, Retail, Logistics)

3.5. Government Regulation (Digital Transformation Policies, Data Privacy Laws)

3.5.1. Vision 2030 Digital Infrastructure Initiatives

3.5.2. Cybersecurity Framework Regulations

3.5.3. Data Localization and Privacy Regulations

3.5.4. Taxation on Digital Platforms and E-Commerce

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. KSA ICT Market Segmentation

4.1. By Component (In Value %)

4.1.1. Hardware

4.1.2. Software

4.1.3. Services

4.2. By Deployment Model (In Value %)

4.2.1. On-Premise

4.2.2. Cloud-based

4.2.3. Hybrid

4.3. By End-User (In Value %)

4.3.1. Government

4.3.2. Banking, Financial Services, and Insurance (BFSI)

4.3.3. Telecom

4.3.4. Retail

4.3.5. Healthcare

4.4. By Technology (In Value %)

4.4.1. 5G Network Infrastructure

4.4.2. Cloud Computing

4.4.3. Internet of Things (IoT)

4.4.4. Artificial Intelligence (AI)

4.4.5. Blockchain

4.5. By Region (In Value %)

4.5.1. East

4.5.2. West

4.5.3. North

4.5.4. South

5. KSA ICT Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. STC (Saudi Telecom Company)

5.1.2. Mobily (Etihad Etisalat)

5.1.3. Zain KSA

5.1.4. Cisco Systems Inc.

5.1.5. Huawei Technologies Co. Ltd.

5.1.6. Oracle Corporation

5.1.7. Microsoft Corporation

5.1.8. IBM Corporation

5.1.9. SAP SE

5.1.10. Ericsson AB

5.1.11. Amazon Web Services (AWS)

5.1.12. Google Cloud

5.1.13. Dell Technologies

5.1.14. Hewlett Packard Enterprise (HPE)

5.1.15. Accenture

5.2. Cross Comparison Parameters (Headquarters, Revenue, No. of Employees, Service Portfolio, Inception Year, Market Share, Key Clientele, Strategic Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Joint Ventures, Investments)

5.5. Mergers & Acquisitions

5.6. Investment Analysis

5.7. Venture Capital and Private Equity Investments

5.8. Government Grants and Funding

6. KSA ICT Market Regulatory Framework

6.1. Data Protection Laws

6.2. Telecom Licensing Regulations

6.3. Compliance Requirements for ICT Companies

6.4. Spectrum Allocation and Management Policies

7. KSA ICT Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. KSA ICT Future Market Segmentation

8.1. By Component (In Value %)

8.2. By Deployment Model (In Value %)

8.3. By End-User (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9. KSA ICT Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Market Entry Strategies

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

This initial phase involves mapping the KSA ICT market's key stakeholders and variables such as service providers, regulatory bodies, and end-users. Extensive desk research utilizing secondary and proprietary databases is conducted to gather relevant industry-level data and identify market dynamics.

Step 2: Market Analysis and Construction

Historical data is analyzed to understand market trends and segment performance. This includes assessing the penetration of telecom, cloud computing, and AI in the country and evaluating the contribution of different regions and sectors to the market's revenue.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions are validated through interviews with industry experts and consultations with key players in the KSA ICT ecosystem. These insights help refine the data and provide a comprehensive view of the market.

Step 4: Research Synthesis and Final Output

Finally, the data is synthesized into a cohesive report, ensuring all insights from primary and secondary sources are incorporated. The findings are cross-validated to ensure a reliable and accurate portrayal of the KSA ICT market.

Frequently Asked Questions

01. How big is the KSA ICT Market?

02. What are the challenges in the KSA ICT Market?

03. Who are the major players in the KSA ICT Market?

04. What are the growth drivers of the KSA ICT Market?

05. What opportunities exist in the KSA ICT Market?

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.