KSA Natural Gas Market Outlook to 2030

Region:Saudi Arabia

Author(s):Shreya Garg

Product Code:KROD5785

Region:Saudi Arabia

Author(s):Shreya Garg

Product Code:KROD5785

December 2024

99

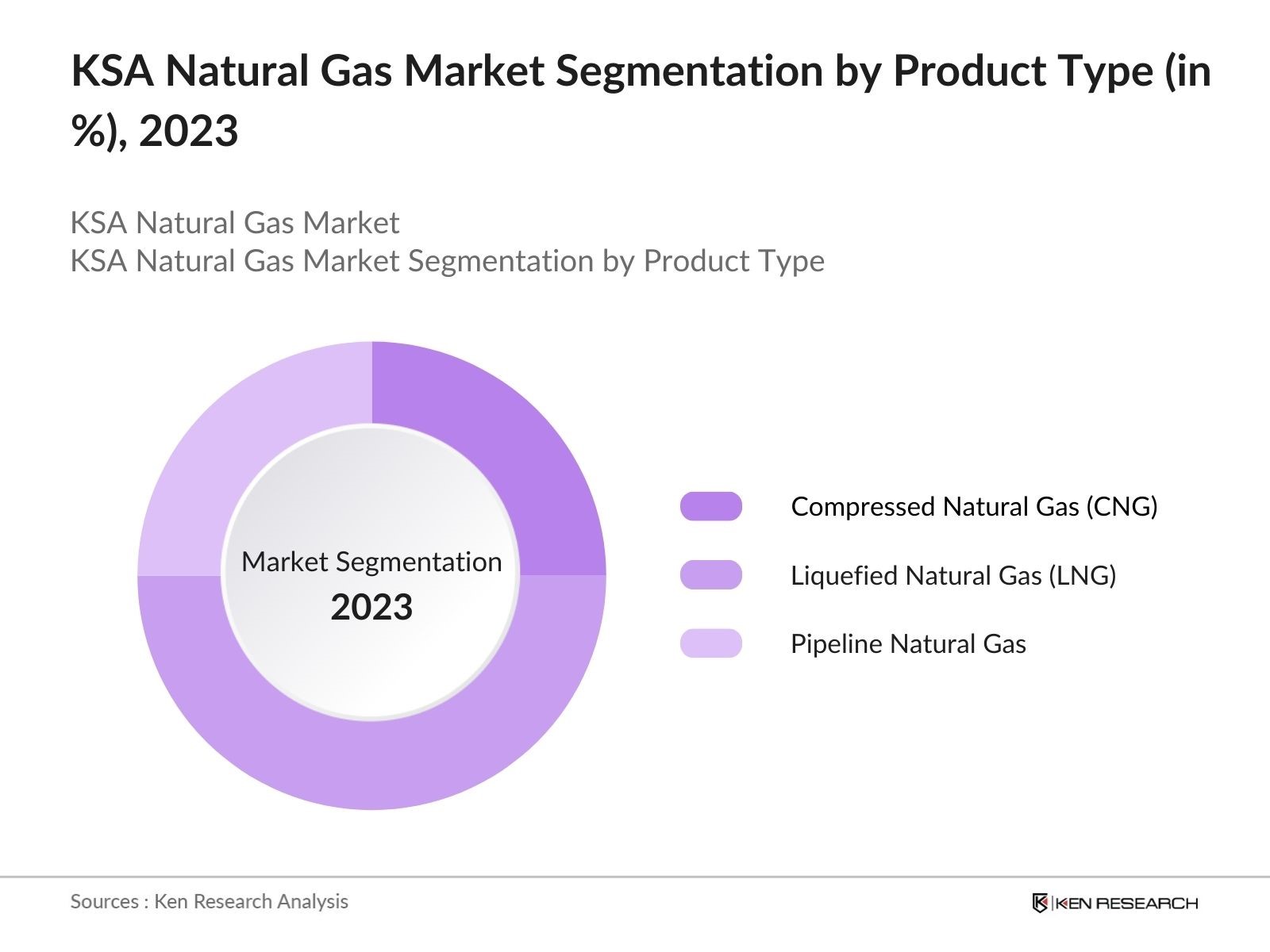

By Product Type: The market is segmented by product type into compressed natural gas (CNG), liquefied natural gas (LNG), and pipeline natural gas. Liquefied natural gas (LNG) holds a dominant market share due to its flexibility in transportation and storage, making it ideal for both domestic consumption and exports. Saudi Arabia's push to become a leading global LNG exporter has accelerated the development of LNG facilities, driving demand. LNGs competitive advantage over other gas forms lies in its ability to cater to a broader range of applications, from power generation to industrial processes.

By Application: The market is also segmented by application into power generation, industrial usage, and residential consumption. Power generation dominates the market share due to the kingdoms heavy reliance on natural gas to fuel electricity production. The transition from oil to natural gas in power plants has not only reduced emissions but also allowed for more cost-effective and reliable energy production. The shift towards gas-fired power plants is aligned with Saudi Arabias environmental sustainability goals under Vision 2030, contributing to the dominance of this segment.

The KSA natural gas market is dominated by key players, with Saudi Aramco at the forefront due to its vast reserves, technological prowess, and significant infrastructure investments. Other global and local companies such as GASCO and SABIC also hold substantial shares, leveraging their expertise and strong market presence.

|

Company Name |

Establishment Year |

Headquarters |

Employees |

Revenue (USD Bn) |

Gas Production Capacity (BCF/D) |

LNG Facilities |

Strategic Partnerships |

R&D Investment |

Geographical Presence |

|

Saudi Aramco |

1933 |

Dhahran, KSA |

|||||||

|

GASCO |

1963 |

Riyadh, KSA |

|||||||

|

SABIC |

1976 |

Riyadh, KSA |

|||||||

|

Petro Rabigh |

2005 |

Rabigh, KSA |

|||||||

|

TotalEnergies |

1924 |

Courbevoie, France |

The KSA natural gas market is projected to see strong growth in the coming years, driven by government initiatives under Vision 2030 and continuous investments in natural gas infrastructure. Saudi Arabia aims to increase its share of natural gas in the energy mix, moving away from reliance on oil for power generation. Expansion of LNG facilities and rising demand from industrial sectors will further boost the market's growth. Technological advancements in gas extraction and processing will also play a pivotal role in shaping the future of the market, ensuring increased efficiency and sustainability.

|

By Product Type |

CNG LNG Pipeline Gas |

|

By Application |

Power Generation Industrial, Residential |

|

By Extraction Technology |

Conventional Unconventional |

|

By Distribution Mode |

Pipeline Shipping |

|

By Region |

Eastern Province Western Province Central Region Northern Region |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Demand for Energy [Market Demand]

3.1.2. Rising Industrialization [Industrial Expansion]

3.1.3. Strategic Investments in Gas Infrastructure [Investment Trends]

3.1.4. Government Initiatives and Vision 2030 [Regulatory Support]

3.2. Market Challenges

3.2.1. High Extraction and Processing Costs [Cost Efficiency]

3.2.2. Environmental Concerns and Regulations [Sustainability]

3.2.3. Competition from Renewable Energy [Market Diversification]

3.3. Opportunities

3.3.1. Expansion of LNG (Liquefied Natural Gas) Facilities [Export Potential]

3.3.2. Partnerships with International Energy Firms [Collaborative Ventures]

3.3.3. Technological Advancements in Gas Extraction [Innovation]

3.4. Trends

3.4.1. Adoption of Digital Technologies in Gas Operations [Digitalization]

3.4.2. Growth in Domestic Gas Consumption [Consumer Demand]

3.4.3. Shift towards Cleaner Energy Sources [Green Energy]

3.5. Government Regulation

3.5.1. Saudi Energy Efficiency Program (SEEP) [Energy Policy]

3.5.2. Gas Allocation Policies for Domestic and Industrial Use [Regulatory Framework]

3.5.3. Export Regulations for Natural Gas and LNG [Export Policy]

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Compressed Natural Gas (CNG)

4.1.2. Liquefied Natural Gas (LNG)

4.1.3. Pipeline Natural Gas

4.2. By Application (In Value %)

4.2.1. Power Generation

4.2.2. Industrial Usage

4.2.3. Residential Consumption

4.3. By Extraction Technology (In Value %)

4.3.1. Conventional Natural Gas

4.3.2. Unconventional Natural Gas

4.4. By Distribution Mode (In Value %)

4.4.1. Pipeline Network

4.4.2. Shipping (LNG)

4.5. By Region (In Value %)

4.5.1. Eastern Province

4.5.2. Western Province

4.5.3. Central Region

4.5.4. Northern Region

5.1. Detailed Profiles of Major Competitors

5.1.1. Saudi Aramco

5.1.2. National Gas and Industrialization Company (GASCO)

5.1.3. SABIC (Saudi Basic Industries Corporation)

5.1.4. Petro Rabigh

5.1.5. Schlumberger

5.1.6. Halliburton

5.1.7. TotalEnergies

5.1.8. Shell Saudi Arabia

5.1.9. ExxonMobil

5.1.10. Baker Hughes

5.1.11. Linde Saudi Arabia

5.1.12. BP Middle East

5.1.13. Chevron

5.1.14. Eni Saudi Arabia

5.1.15. Gazprom

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Revenue, Inception Year, Market Share, Product Offering, Regional Presence, Investment in R&D)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Environmental Compliance Standards

6.2. Gas Extraction and Processing Regulations

6.3. Gas Export Certification Process

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Extraction Technology (In Value %)

8.4. By Distribution Mode (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The first step involves creating an ecosystem map of all major players in the KSA natural gas market, leveraging desk research and proprietary databases to define critical variables like demand, infrastructure, and export potential.

In this stage, we compile historical data on market penetration, revenue streams, and energy consumption trends to accurately assess the current state of the market. We analyze gas consumption patterns and infrastructure development to provide insights into market dynamics.

This phase includes validating market hypotheses through interviews with industry experts, gathering insights from key players in the market. These consultations refine the data collected and offer a deeper understanding of strategic market factors.

In the final stage, we synthesize the data by collaborating with natural gas companies to ensure accuracy. This approach combines bottom-up data collection with expert consultation to deliver a comprehensive market report.

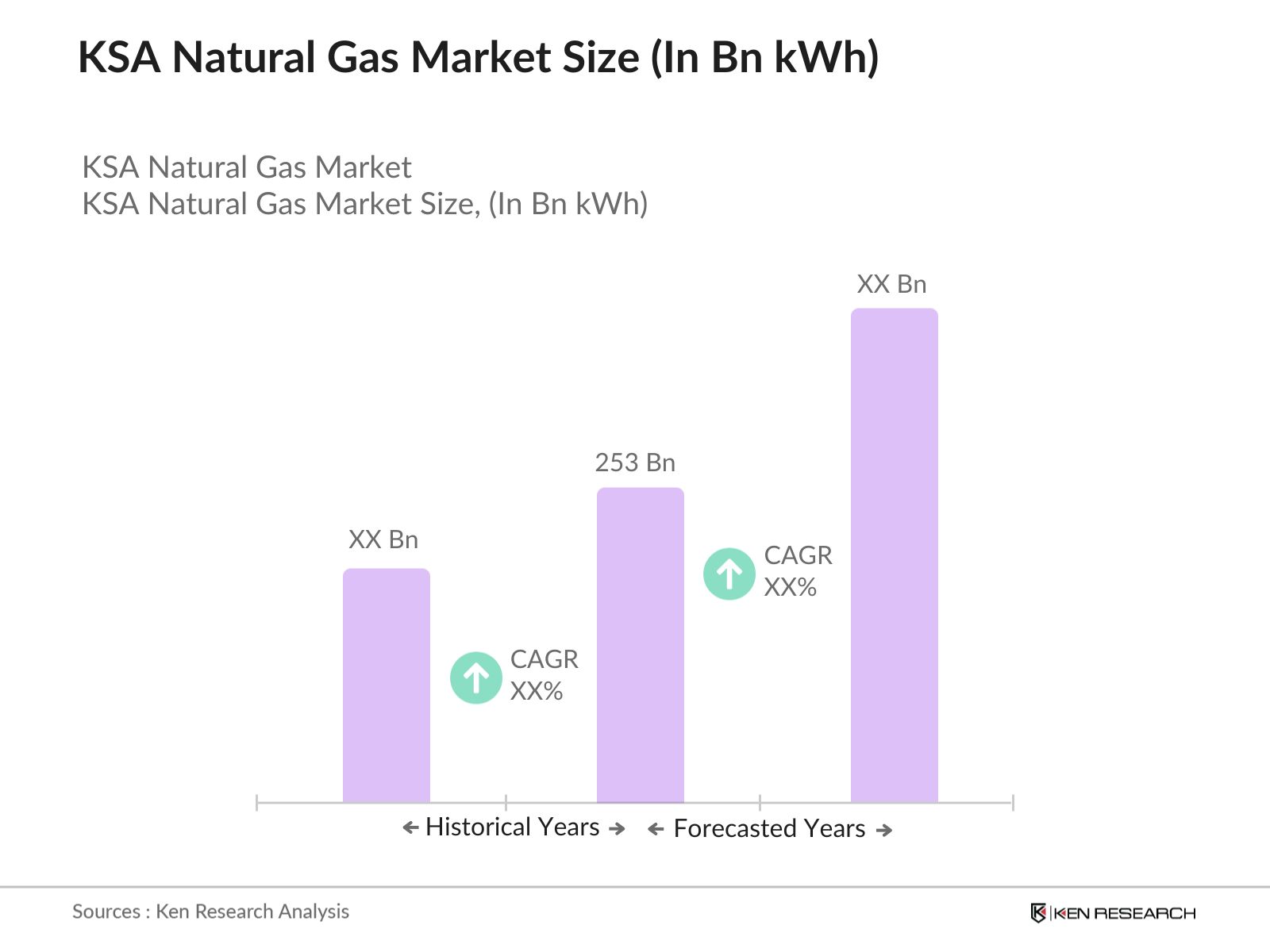

The KSA natural gas market is valued at 253 billion KWh, driven by increasing demand for cleaner energy sources, government investments, and expansion of LNG facilities to meet domestic and export needs.

Key challenges in the KSA natural gas market include high costs of extraction and processing, environmental concerns, and competition from renewable energy sources. These factors may impact the profitability and growth potential of the market.

Major players in the KSA natural gas market include Saudi Aramco, GASCO, SABIC, Petro Rabigh, and TotalEnergies. These companies dominate the market due to their strong infrastructure, technological capabilities, and strategic investments.

The KSA natural gas market is propelled by increased demand for energy, government initiatives under Vision 2030, and advancements in LNG infrastructure, enabling Saudi Arabia to tap into both domestic and international markets.

Opportunities in the KSA natural gas market include expanding LNG exports, technological advancements in gas extraction, and potential partnerships with international energy companies to enhance production and distribution capabilities.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.