KSA New Car Market Outlook to 2029

Region:Saudi Arabia

Author(s):Harsh Saxena

Product Code:KR1524

Region:Saudi Arabia

Author(s):Harsh Saxena

Product Code:KR1524

August 2025

90

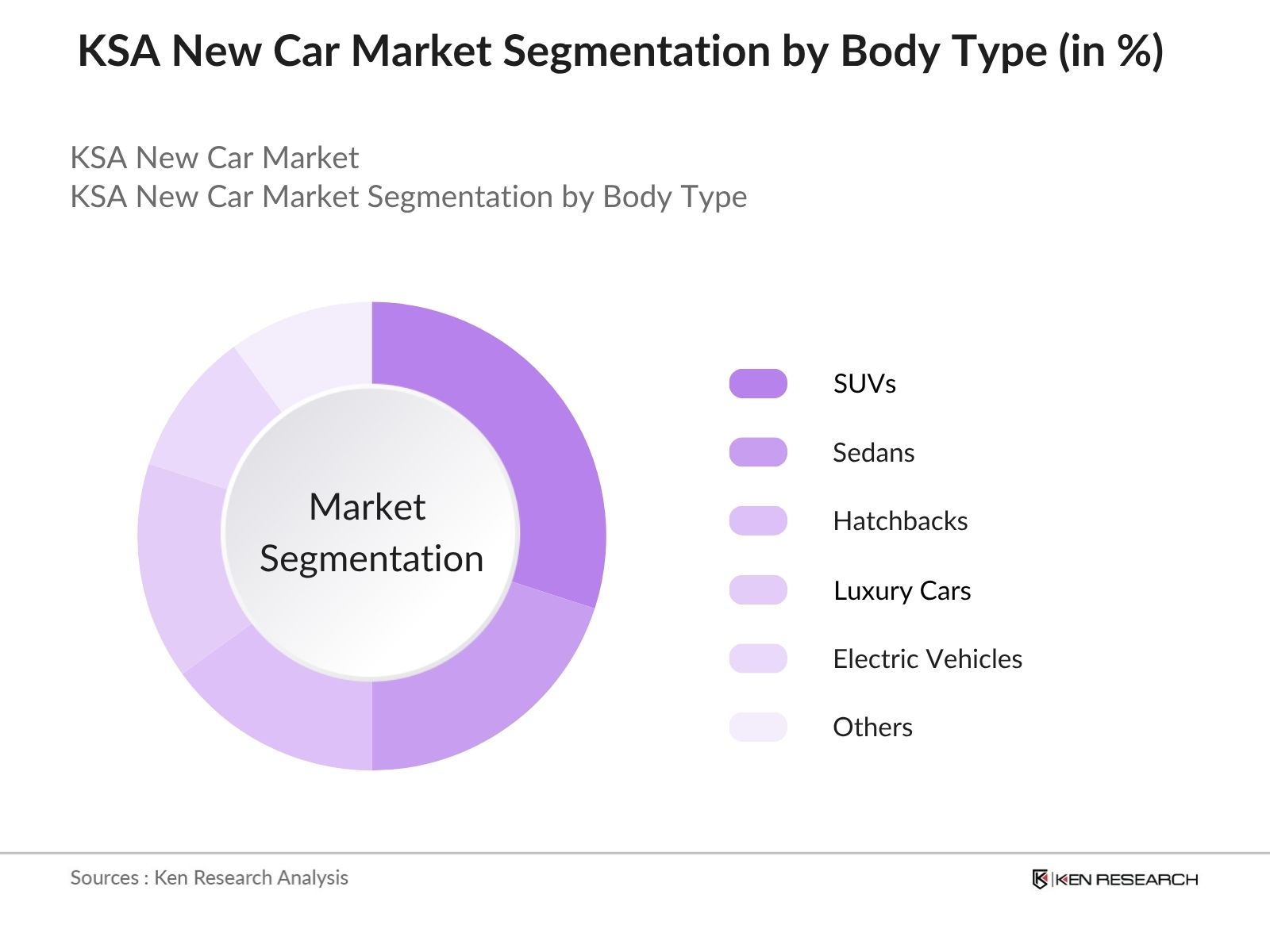

By Body Type: The vehicle body type segmentation includes SUVs, Sedans, Pickup Trucks, Hatchbacks, Luxury Cars, Electric Vehicles, and Others. Each of these subsegments addresses distinct consumer preferences and mobility needs, reflecting the evolving automotive landscape in Saudi Arabia. SUVs are increasingly favored for their versatility and suitability for family and off-road use, while sedans remain popular for urban commuting. Electric vehicles, though still a small segment, are growing rapidly due to government incentives and infrastructure investments.

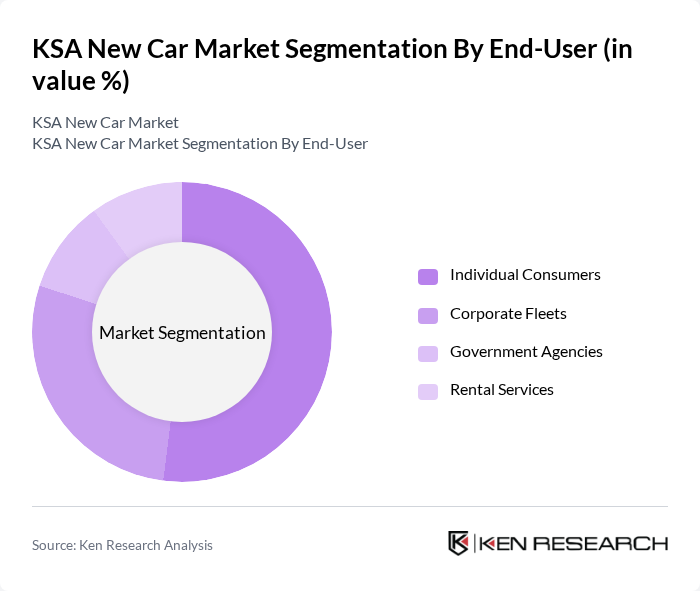

By End-User: The end-user segmentation includes Individual Consumers, Corporate Fleets, Government Agencies, and Rental Services. Individual consumers represent the largest segment, driven by rising middle-class purchasing power, increased vehicle financing options, and a growing preference for personal mobility. Corporate fleets and rental services are also expanding, supported by business growth and tourism sector development.

The KSA New Car Market is characterized by a dynamic mix of regional and international players. Leading participants such as Toyota (Abdul Latif Jameel Motors), Hyundai (Wallan Trading Company), Nissan (Petromin Nissan), Ford (Al Jazirah Vehicles Agencies Co.), and Chevrolet (Aljomaih Automotive Company) contribute to innovation, geographic expansion, and service delivery in this space.

| Toyota (Abdul Latif Jameel Motors) | 1955 | Jeddah, Saudi Arabia | – | – | – | – | – | – |

| Hyundai (Wallan Trading Company) | 1998 | Riyadh, Saudi Arabia | – | – | – | – | – | – |

| Nissan (Petromin Nissan) | 2016 | Jeddah, Saudi Arabia | – | – | – | – | – | – |

| Ford (Al Jazirah Vehicles Agencies Co.) | 1987 | Riyadh, Saudi Arabia | – | – | – | – | – | – |

| Chevrolet (Aljomaih Automotive Company) | 1967 | Riyadh, Saudi Arabia | – | – | – | – | – | – |

| Company | Establishment Year | Headquarters | Group Size (Large, Medium, or Small as per industry convention) | Annual New Car Sales Volume (Units) | Market Share (%) | Revenue from New Car Sales (SAR) | Average Selling Price (SAR) | Distribution Network Coverage (Number of Dealerships/Outlets) |

|---|

The KSA new car market is poised for significant transformation driven by technological advancements and changing consumer preferences. The shift towards electric vehicles is expected to accelerate, supported by government incentives and a growing charging infrastructure. Additionally, the rise of online car sales platforms will reshape the purchasing process, making it more accessible. As urbanization continues, the demand for smart transportation solutions will also increase, fostering innovation and enhancing the overall customer experience in the automotive sector.

| By Body Type |

SUVs Sedans Hatchbacks Luxury Cars Electric Vehicles Others |

| By End-User |

Individual Consumers Corporate Fleets Government Agencies Rental Services |

| By Price Range |

Budget Cars Mid-Range Cars Premium Cars Luxury Cars |

| By Sales Channel |

Dealerships Online Platforms Direct Sales (OEM/Corporate) |

| By Distribution Mode |

Urban Distribution Rural Distribution Export Distribution |

| Scope Item/Segment | Sample Size | Target Respondent Profiles |

|---|---|---|

| New Car Buyers | 120 | Individuals aged 25-55, Middle to Upper Income |

| Automotive Dealerships | 60 | Dealership Owners, Sales Managers |

| Fleet Management Companies | 40 | Fleet Managers, Procurement Officers |

| Automotive Industry Experts | 40 | Market Analysts, Industry Consultants |

| Government Regulatory Bodies | 20 | Policy Makers, Regulatory Officials |

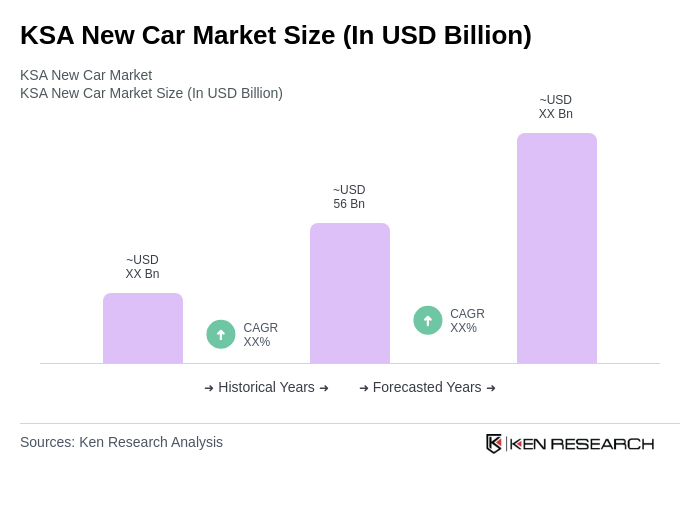

The KSA New Car Market is valued at approximately USD 56 billion, driven by increasing consumer demand, urbanization, and government initiatives like Vision 2030, which aims to diversify the economy and enhance the automotive sector.

Key cities such as Riyadh, Jeddah, and Dammam dominate the KSA New Car Market due to their large populations and robust economic activities, with Riyadh serving as the central hub for automotive sales and services.

In 2023, the Saudi government introduced regulations requiring all new vehicles to comply with updated environmental standards aimed at reducing carbon emissions and promoting electric vehicle adoption, aligning with the sustainability objectives of Vision 2030.

The KSA New Car Market is segmented by vehicle body type, with SUVs currently dominating due to their versatility and appeal for family and off-road use, followed by sedans, pickup trucks, and an emerging interest in electric vehicles.

The primary end-users in the KSA New Car Market include individual consumers, corporate fleets, government agencies, and rental services, with individual consumers representing the largest segment driven by rising middle-class purchasing power and vehicle financing options.

Key growth drivers include increasing disposable income, government initiatives for local manufacturing, and rising urbanization and population growth, which collectively enhance consumer spending power and demand for new vehicles in Saudi Arabia.

The KSA New Car Market faces challenges such as high competition among automotive brands, fluctuating oil prices affecting consumer spending, and regulatory compliance costs, which can impact market dynamics and consumer purchasing behavior.

The electric vehicle market in Saudi Arabia is expected to grow significantly, with government targets aiming for 35% of new vehicle sales to be electric, supported by incentives like tax exemptions and subsidies to attract consumers and manufacturers.

Online sales platforms are projected to grow by 30% in the KSA New Car Market, driven by increased internet penetration and changing consumer behaviors, providing dealerships with opportunities to reach a broader audience and streamline the purchasing process.

Rapid urbanization in Saudi Arabia, with the urban population expected to reach 38 million, drives demand for personal vehicles as residents seek convenient transportation options, further supported by infrastructure development and population growth.

Leading automotive brands in the KSA New Car Market include Toyota, Hyundai, Nissan, Ford, and Chevrolet, among others, contributing to innovation, geographic expansion, and service delivery within the competitive landscape.

New car buyers in Saudi Arabia have various financing options, including cash purchases, loans, leases, and installment plans, which enhance accessibility and affordability for consumers looking to purchase vehicles.

The Saudi government supports local vehicle manufacturing through initiatives like the National Industrial Development and Logistics Program (NIDLP), aiming to produce 350,000 vehicles annually and investing over SAR 12 billion to enhance local production capabilities.

Trends shaping the future of the KSA New Car Market include a shift towards sustainable and eco-friendly vehicles, integration of advanced technology, and the rise of online sales platforms, enhancing customer experience and accessibility.

The KSA New Car Market is expected to see approximately 650,000 new vehicle registrations by 2024, reflecting ongoing growth driven by consumer demand, urbanization, and government initiatives aimed at boosting the automotive sector.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.